TRMD - TORM plc: This Top-Rated Stock Still Has Something To Show

2023-04-06 05:16:40 ET

Summary

- Although 2023 is already bringing economic challenges, there's an excellent opportunity for investors to search for gems in the tanker market.

- TORM achieved a record-high EBITDA of $267 million in Q4, bringing the full year to $743 million, more than the previous 4 years combined.

- In my view, TORM plc's low debt and valuation multiples create a large margin of safety in case of unstable freight rates going forward.

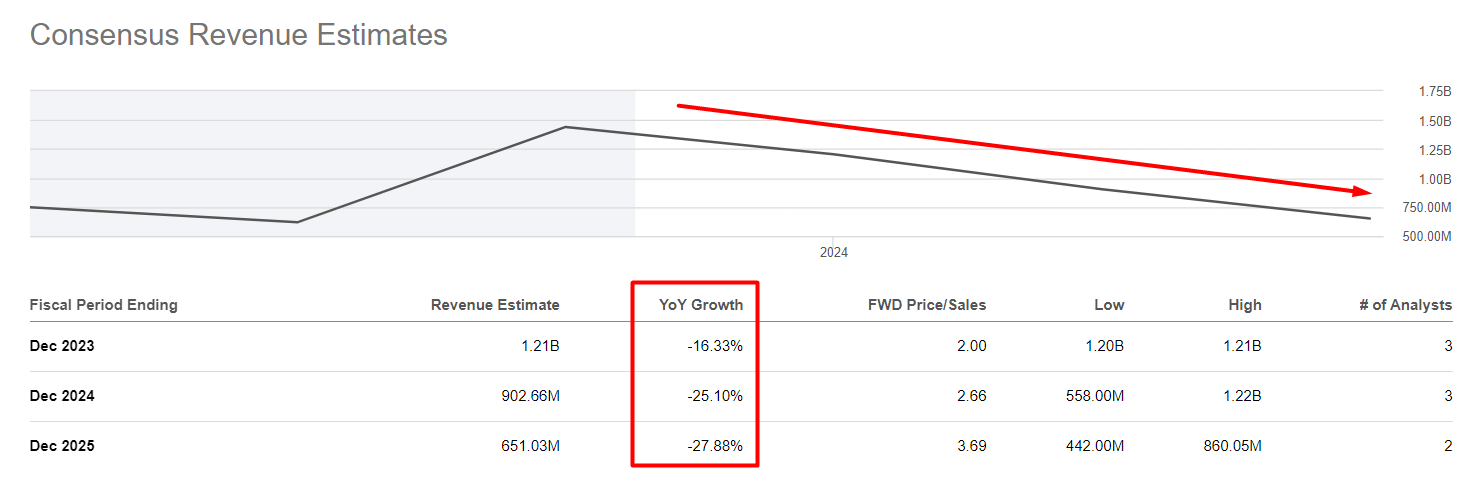

- Mr. Market prices TORM's revenue CAGR of -18.7% for the next 3 years - an easy target to exceed, in my opinion.

- I initiate TORM's coverage with a Buy rating.

Intro & Thesis

In the past, I have written about Ardmore Shipping ( ASC ), a stock once top-rated by Seeking Alpha - I assumed that the tanker shipping market should continue to flourish and that this will create a favorable environment for ASC to capitalize on the attractiveness of its fleet structure to sign new contracts at higher prices.

I am not retracting my thesis, although ASC's share price has fallen slightly since that article was published. On the contrary - I am looking at this market with a more bullish eye and see a lot of other opportunities. One of them is presented by the hero of today's article - TORM plc ( TRMD ), which in my opinion is still very cheap and has no less good prospects for future stock price appreciation. Let me present you with a top-down analysis of this idea.

The Tanker Market Outlook

In an article on ASC, I have already written about what this industry is likely to face in the foreseeable future. I will briefly repeat myself here.

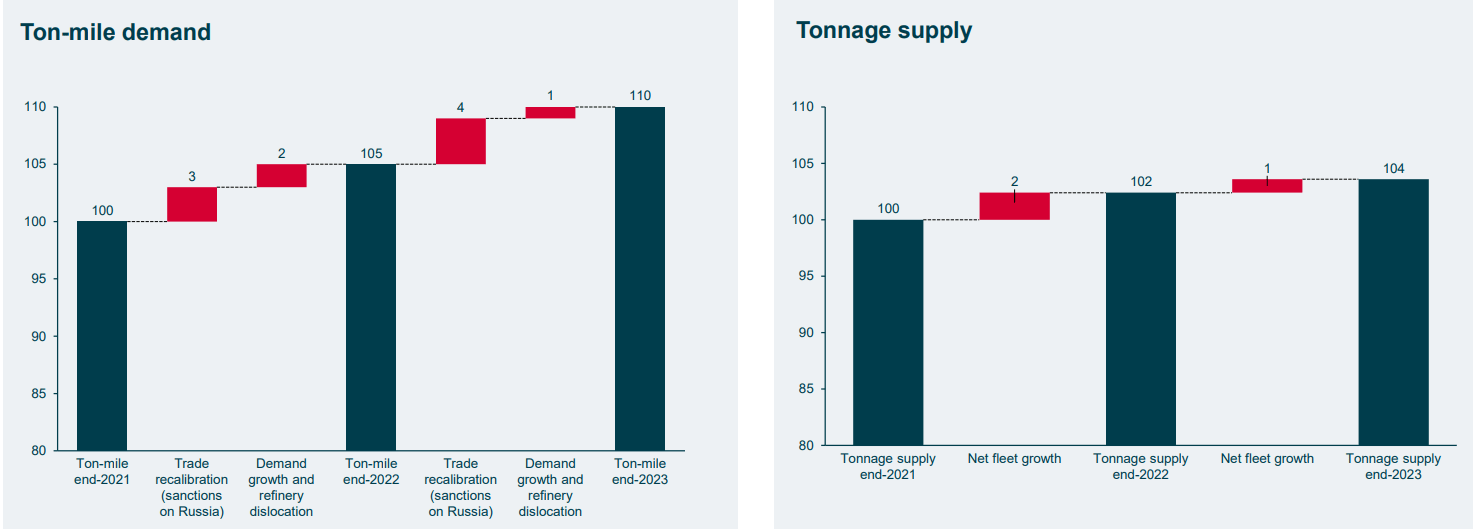

The war in Ukraine has had a profound impact on the energy commodities market in Europe - in an effort to cut off Russian oil, tankers have become the main alternative for delivering hydrocarbons to Western oil importers. Due to severe underinvestment in the oil and gas industry over the past few years, prices for oil and other commodities have skyrocketed in conjunction with strong demand following the pandemic. While the impact of the pandemic has been significant, the market has recognized that since the war in Ukraine, tanker companies have entered a new bull cycle that is expected to last for at least the next 12-18 months.

The low level of backlog, which is at a historic low to date, is a key factor in these super gains. In addition, the tonne miles, displaced by geopolitically unpleasant Russian energy in Europe, have only increased demand for tanker shipments. As Russia builds its shadow fleet due to the shortage of tankers, it is expected that the new market prices will be reflected in the revaluation of tanker companies' assets. So Western public industry players are expected to benefit significantly from this trend by making their vessels available for these purposes. I'd like to remind you that Greece was considered the largest country in the world shipping, which is still true today.

Despite the looming recession, a drop in energy prices will most likely boost demand for tanker companies' services as dwindling supplies of various commodities urgently need to be replenished.

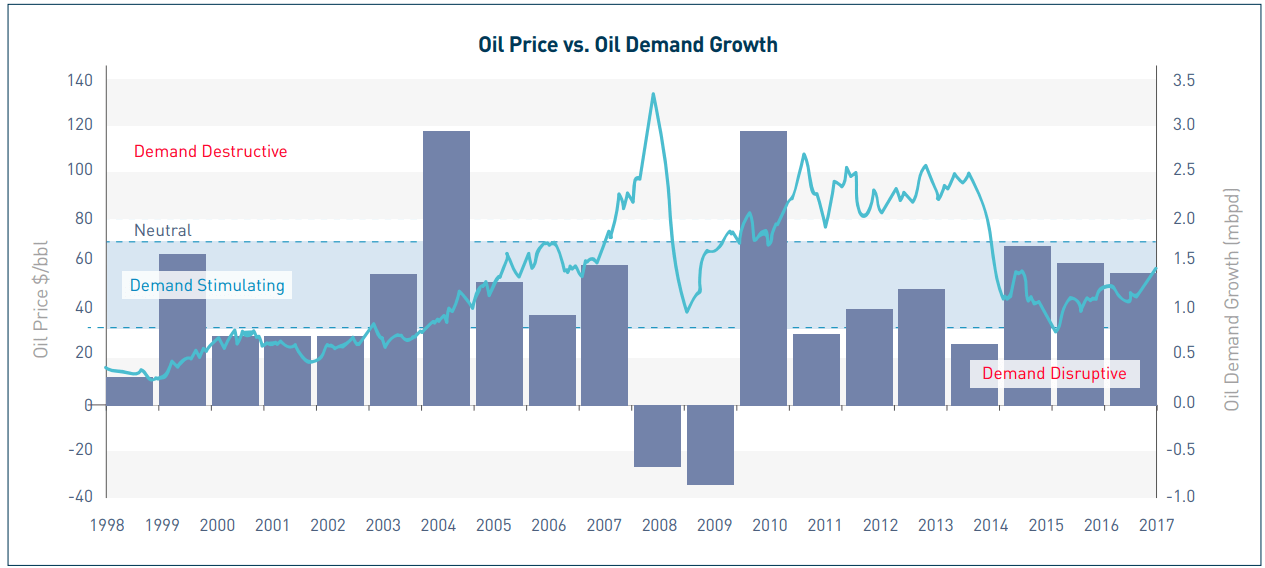

In one of Euronav's ( EURN ) presentation materials, there is a graph showing that demand for tanker transportation is stimulated precisely by the relative stability of oil prices in the $60-70 per barrel range - that is, a possible recession in 2023 in theory, should not leave the ships without work against the backdrop of relatively strong demand in China.

Euronav's presentation materials

{kind=link}

So although 2023 is already bringing economic challenges, there's an excellent opportunity for investors to search for gems in the tanker market.

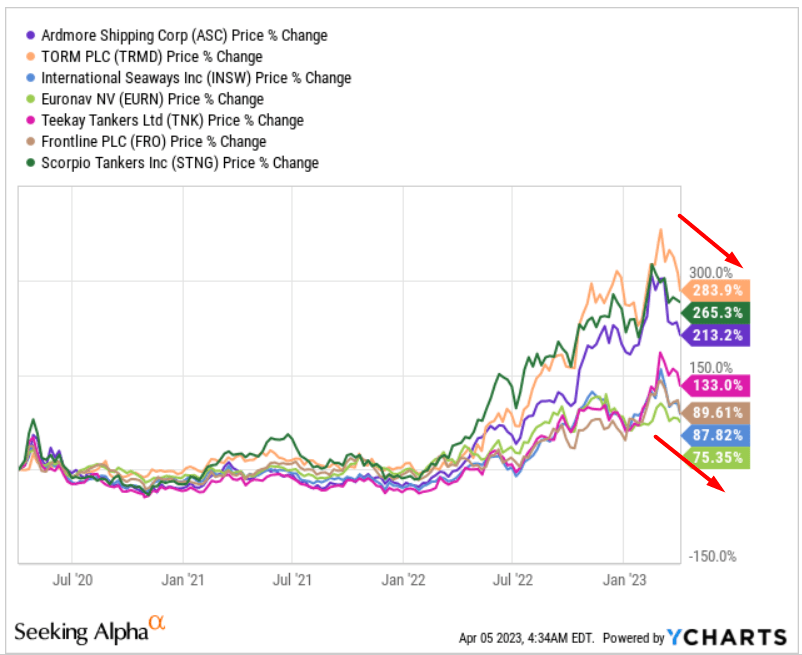

These factors were recognized long before I laid them out here, so tanker stocks eventually priced them in and their quotes have tripled in recent months. However, we are now seeing some of the early investors fixing their triple-digit percentage gains and the industry's stocks entering a correction phase:

{kind=link}

Therefore, I think that the current situation in the tanker market is just a logical profit taking and the continuation of the uptrend is likely to last at least a few more months ahead - investors who want to make super profits should consider investing in tanker companies while they're weak.

TRMD Stock Is A Buy

According to its latest 20-F filing , TORM plc is a publicly traded company incorporated in England and Wales in 2015, while its main commercial and technical activities are managed from its office in Denmark. It's one of the largest carriers of refined oil products in the world and operates in various vessel segments from Medium Range to Long Range 2 tankers. TORM also has several other offices worldwide, including in India, the Philippines, Singapore, and the United States. The company makes money by transporting refined oil products and sometimes crude oil for customers, including major oil companies and international trading houses. Its fleet includes LR1, LR2, MR, and Handy tankers, being a pure-play product tanker market player.

Data provided by E. Finley-Richardson [on Twitter]

{kind=link}

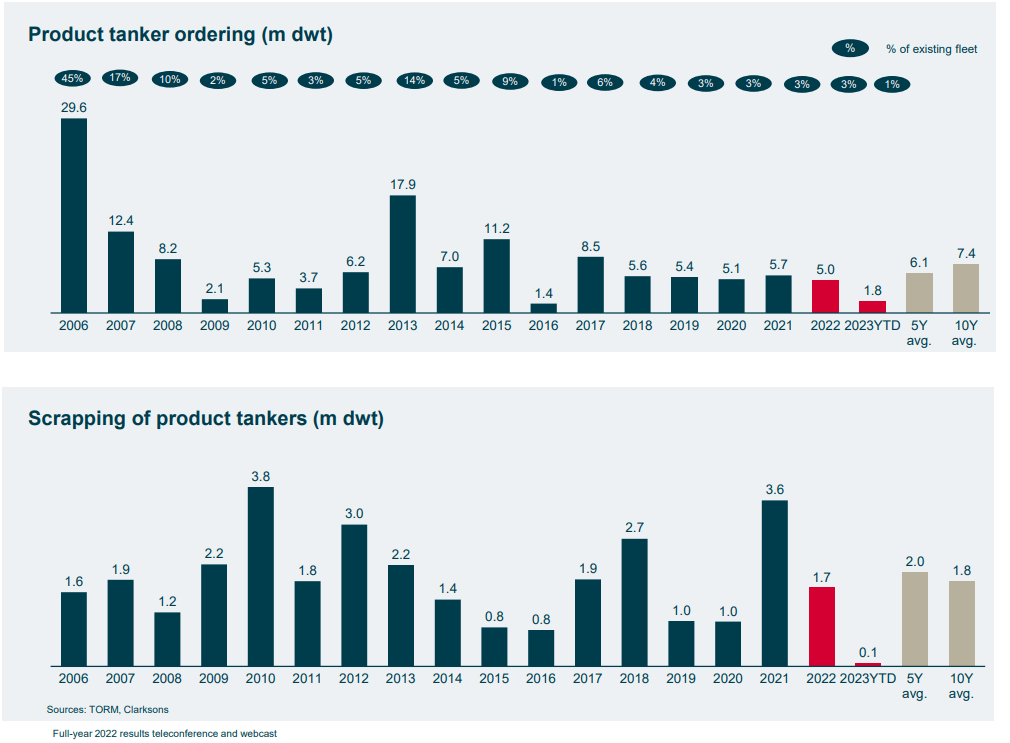

As I mentioned earlier, tanker order books are now at multi-year lows - product tankers in particular stand out among other sub-industries as having some of the lowest levels despite the strong freight market:

{kind=link}

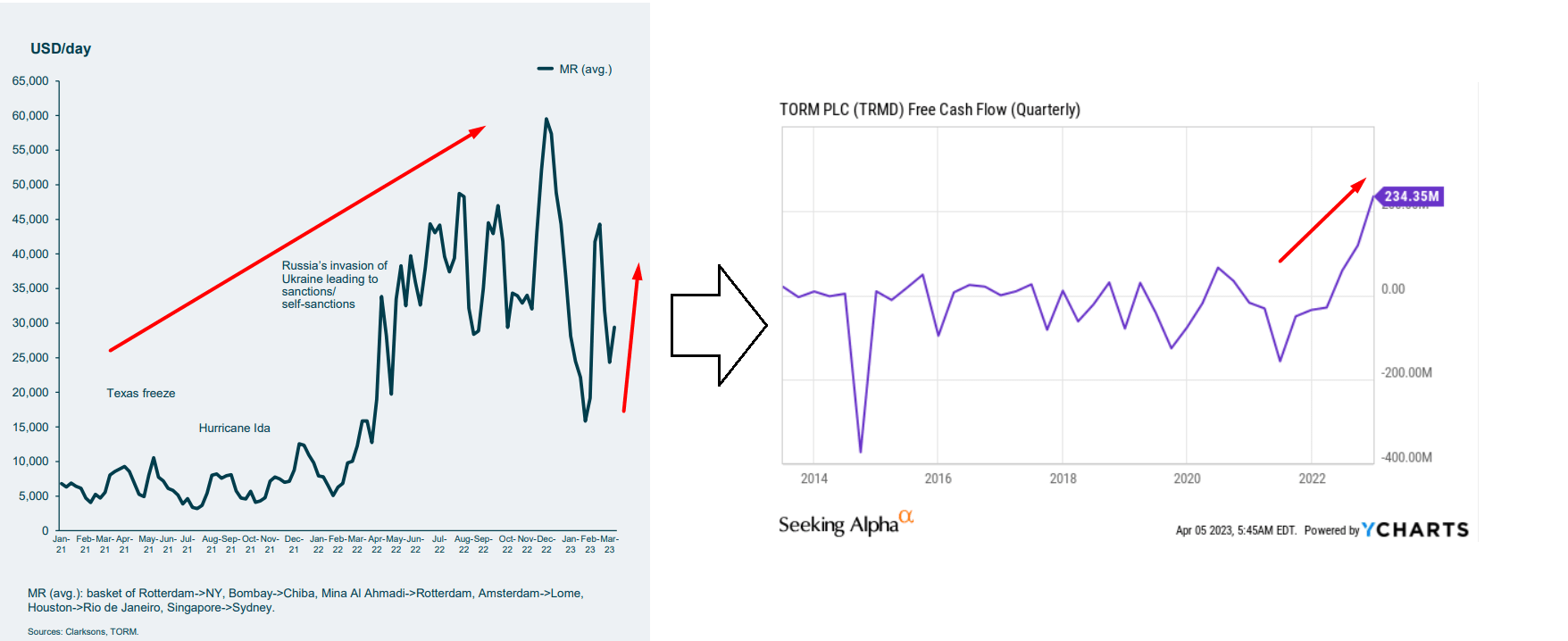

According to the company's IR presentation , the earliest delivery date for potential ordering of product tankers at renowned yards is year-end 2025/beginning 2026, which will limit fleet growth in 2023-2024 - less supply of vessels is going to support astronomically high freight rates, which brings a huge cash flow to the firm:

Author's compilation, based on YCharts and TORM's data

{kind=link}

From the latest earnings call, we know that TORM reported record-high Time Charter Equivalent [TCE] rates in Q3 2022, but managed to obtain even higher rates in Q4 2022. Across the fleet, TORM achieved an average rate of $47,500 per day, an increase of 184% from the 1st to the 4th quarter. As of March 30th, 2023, the company has continued to experience strong market conditions, with high TCE rates. In Q1 2023, TORM fixed 90% of tanker days at an average rate of $43,002 per day, and 89% of MR tanker days at $37,730 per day. LR1 tanker days were fixed at $44,135 per day and LR2 tanker days at $65,950 per day. Fun fact - breakevens for these vessels tend to be ~$15,000 per day, including debt repayments.

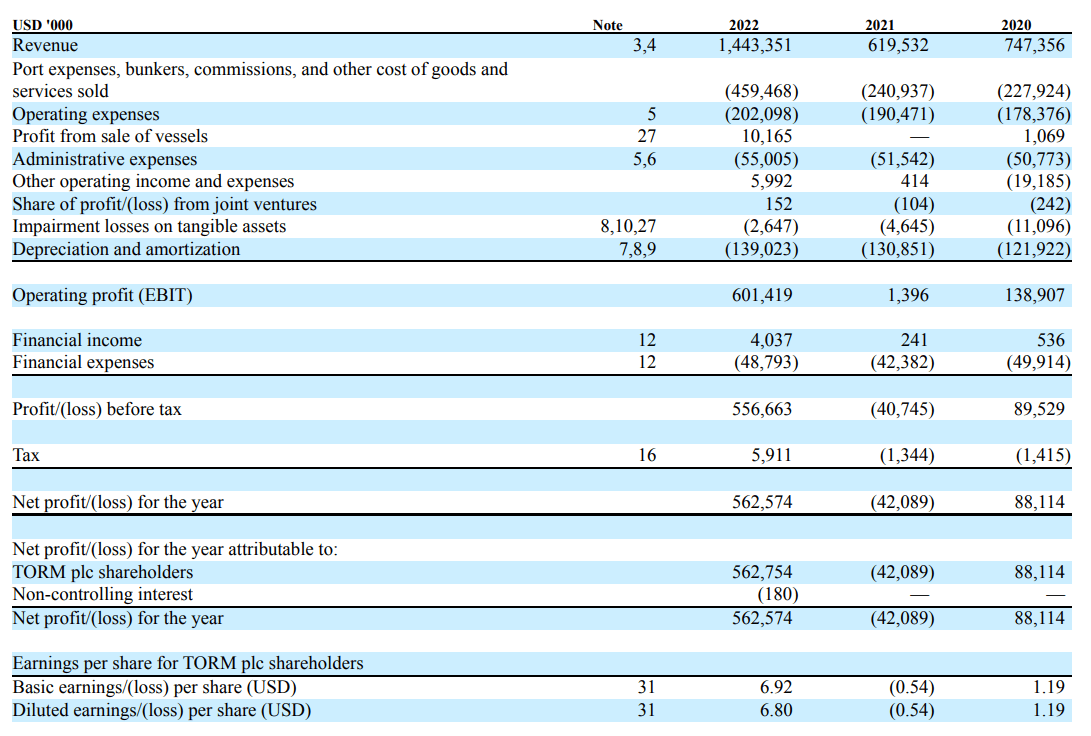

The high TCE rates achieved by TORM led to its highest EBITDA which amounted to $267 million in Q4 bringing the full year to $743 million [ more than the previous 4 years combined ]. The value of TORM's fleet reached $2.65 billion as of December 31, 2022, an increase of more than 37% compared to the end of 2021, even with fewer vessels (78 vs 85).

Management says it will distribute about $212 million, or $2.59 per share, based on Q4 cash balances. The Q4 2022 payout ratio is more than 95% of the $222 million profit, resulting in a total dividend of $378 million for FY 2022. Management does not expect the potential dividend payment in the next quarter to be significantly impacted by the acquisition of the seven LR1 vessels completed in January 2023 - as long as freight rates remain relatively stable at their current high historical levels, TORM should at least keep the dividend in the high single digits, which is still a lot, in my view.

It seems to me that TORM, like many other peers, will be able to maintain its strong financial health due to high rates. This is mainly due to a favorable macro picture, which indicates an imbalance between supply and demand - this is of course a positive sign for all shareholders of tanker stocks.

{kind=link}

So I think the company can maintain its current financials over the next few quarters because market conditions are likely to remain favorable - the cycle will not turn until demand exceeds supply, and this is not projected to happen soon.

{kind=link}

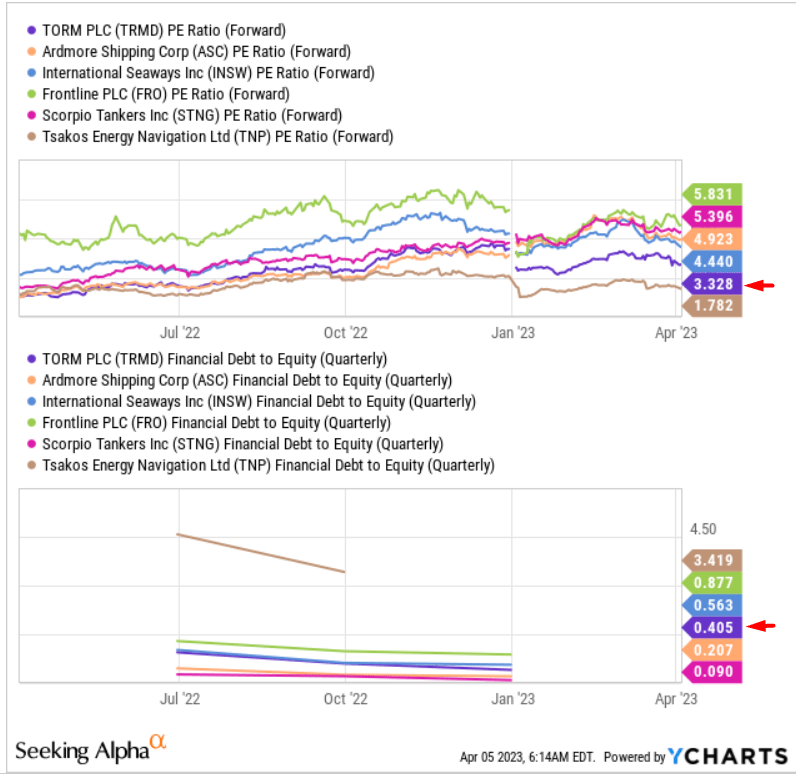

TORM plc's distinctive feature and competitive advantage is its relatively low debt compared to other companies with a similar fleet structure and, at the same time, very low valuation multiples - the fundamental margin of safety is inexplicably large in the event that freight rates become unstable shortly.

YCharts, Seeking Alpha, author's notes

{kind=link}

I hope that in 5 weeks, based on the officially released Q1 FY2023 report, we will see that TRMD will confirm my expectations and that the 14% decline of the stock in the last month will be interrupted. On April 5, TORM will pay a dividend - I expect a natural gap down and a subsequent surge in investor interest in this stock [and closing of this gap in the short term].

Risks Of Investing In TORM

Investing in TORM plc comes with inherent risks that are typical of the product tanker industry. The cyclical nature of the industry leads to volatility in freight rates, vessel values, and overall industry profitability. For example, during the financial crisis of 2008, product tanker freight rates declined significantly, leading to lower vessel values and reduced profitability. While TORM has seen impressive growth in TCE rates in recent years, a worsening of global economic conditions could cause charter rates to decline, making it difficult for TORM to charter or re-charter their vessels profitably.

Additionally, geopolitical events like the conflict in Ukraine can have a significant impact on energy production and trade patterns, including shipping in the Black Sea and elsewhere. While the current impact of the conflict on tanker rates has been positive, the long-term impact remains uncertain, and any changes in industry conditions are unpredictable. TORM's ability to operate its vessels profitably depends on factors beyond its control, such as changes in supply and demand for product tankers, fluctuations in oil prices, and global economic conditions.

The Verdict

Despite the cyclicality risks, I think that with its strong financial performance and low debt, TORM stock is well positioned to continue its growth in the coming quarters. Record TCE rates and limited fleet growth on the product tanker market due to a low orderbook provide a favorable macroeconomic environment resulting in strong free cash flows. With the release of the Q1 FY2023 report, there is a good chance that TORM will continue to exceed Wall Street analysts' expectations - especially those related to the company's prospective revenue [CAGR for the next 3 years = -18.7%].

{kind=link}

Thank you for reading!

For further details see:

TORM plc: This Top-Rated Stock Still Has Something To Show