CAT - Toromont Industries: A 34-Year Dividend Growth Streak

2023-04-09 07:03:43 ET

Summary

- Extending 34 consecutive years of dividend growth, Toromont recently increased its dividend by 10.6%.

- The company boasts an incredible 20-year dividend CAGR of 14.6%.

- Toromont is poised to benefit from an increase in infrastructure spending as well as strong commodity prices.

- The company has more cash on hand than debt, giving it significant optionality to return cash or invest in growth.

Author's Note: All figures in Canadian currency unless otherwise noted.

Investment Thesis

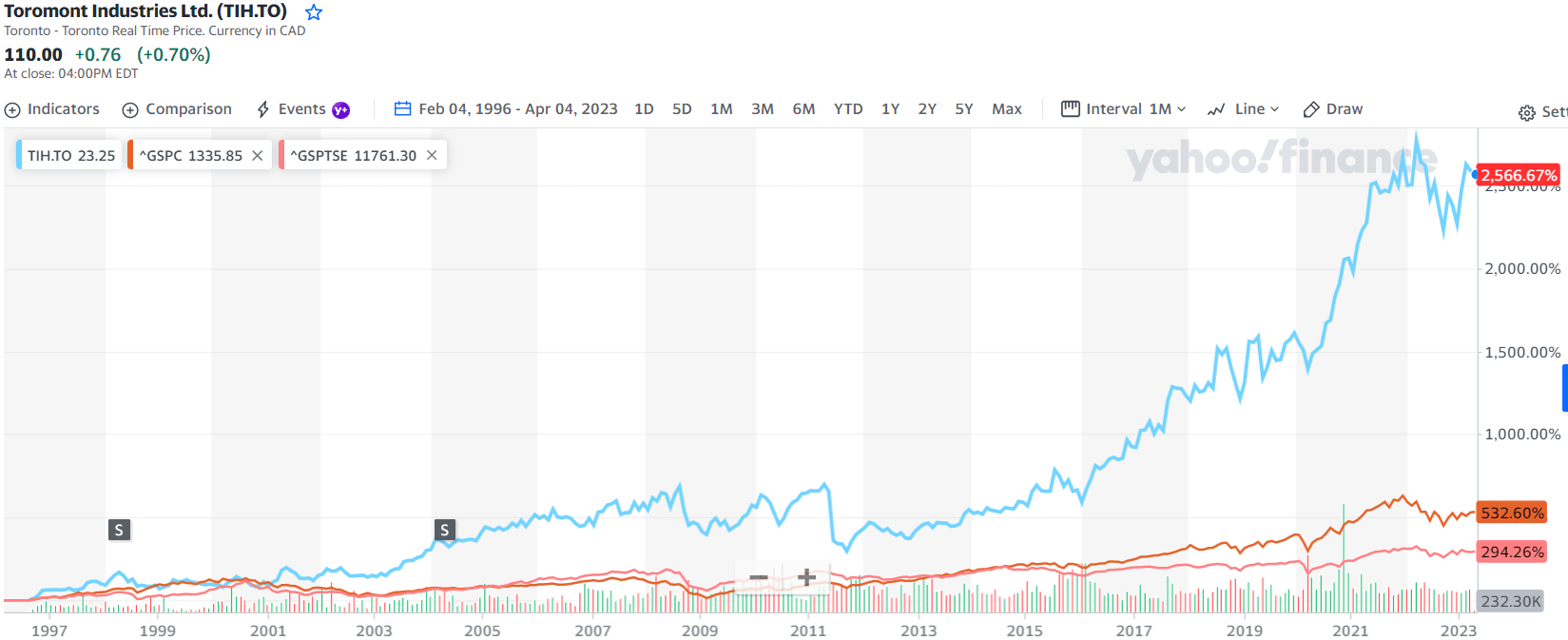

Toromont Industries Ltd. ( TIH:CA ) has paid dividends every year since becoming a publicly traded company in 1968. The company's has one of the best dividend growth records in Canada, measured by both the magnitude and regularity of dividend increases. With essentially no debt, the company has a strong balance sheet and the opportunity to further boost shareholder returns.

Toromont has the privilege of being the exclusive dealer of Caterpillar Inc. ( CAT ) equipment in Eastern and Central Canada. The company is benefiting from the twin tail winds of infrastructure spending and strong commodity prices. In addition to strong sales, the company has been leveraging real time data from increasingly connected equipment to grow its high-margin support and service segment.

Company Profile

Founded in 1961, Toromont is a leading heavy equipment provider, supplying Caterpillar and other brands to industries including construction, roadbuilding, mining, infrastructure, manufacturing, shipping, logistics and waste management. The company earns the highest portion of revenue from ongoing after-purchase support and maintenance. This service business has been supported by connected equipment and better machine specific analytics, which create ongoing revenue opportunities for the dealership. New and used equipment accounted for 43% of 2022 revenues, followed by product support 39%, rentals 11% and 4% from the CIMCO refrigeration segment.

Toromont Business Mix (Toromont)

Toromont has a significant North American presence with 6,800 employees across 160 locations in Canada and the U.S. The Toromont Cat dealership, one of the largest Caterpillar dealers globally, operates in Newfoundland & Labrador, Nova Scotia, New Brunswick, Prince Edward Island, Québec, Ontario and Manitoba and the territory of Nunavut. Toromont's geographic coverage provides diverse market conditions and industries to serve, helping to ensure the business is not overly dependent on any one sector.

In addition to its primary Equipment Group business, the company operates a segment called CIMCO, which designs, builds and installs industrial refrigeration systems for customers ranging from food processing to recreational ice rinks. With a market capitalization of $8.6B, Toromont trades on the Toronto Stock Exchange under the symbol "TIH" with daily average volume of 120,000 shares.

2022 Results

Toromont's average ROE over the past five years is an impressive 19%, exceeding the company's objective after-tax ROE of 18%. Consolidated revenue grew 11.7% and 8.9% in 2021 and 2022 respectively, reflecting strong demand in rentals and growing product support revenue. Gross profit margin improved 1.8% to 26.8% versus 25.0% last year with continued contributions from the equipment segment. Diversified sales growth was driven by strong demand from a variety of industries: construction up 16%, mining up 17%, material handling up 9%, power systems up 8% and agricultural activity up 12%.

Reflecting continued strong demand and improving supply chains, the company's equipment segment backlog improved 4% to $1.1B. Toromont expects to deliver on 90% of backlogged orders in in 2023. While a smaller segment relative to the equipment division, the CIMCO refrigeration business also improved its bookings but saw its backlog grow in 2022 with strong sales, including a natural refrigerant system to National Hockey League's Columbus Blue Jackets.

Dividend Growth

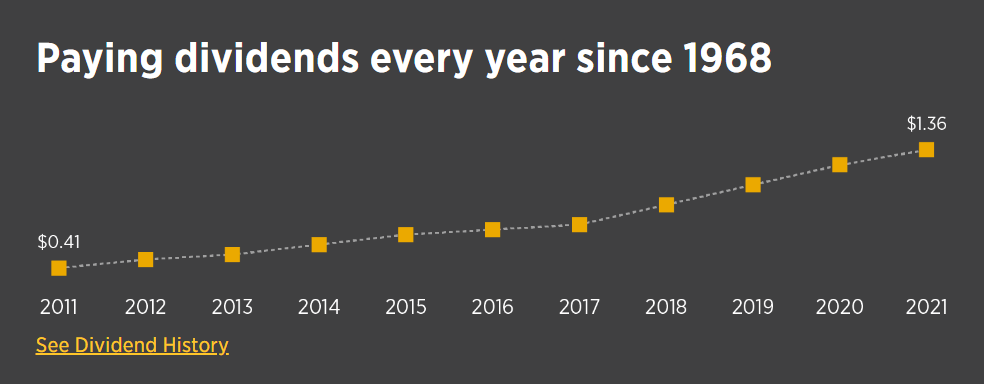

Toromont initiated its dividend program in 1969 and has been rewarding shareholders with regular dividends for 55 years. In 1990, the company began a pattern of regular increases that would see them admitted to the S&P/TSX Canadian Dividend Aristocrats Index. At 34 years, Toromont boasts one of the longest consecutive annual dividend growth streaks in Canada. This duration of uninterrupted increased is a status usually reserved for regulated utilities. Regular readers will know that my favourite investments are ones that can demonstrate consistent dividend growth. This is a clear signal of healthy underlying fundamentals and a business model that generates returns throughout the entire business cycle.

{kind=link}

At current levels, Toromont yields approximately 1.55% with a TTM payout ratio of approximately 29%. While 1.55% may seem inconsequential, the magnitude of this dividend is masked by the company's impressive capital appreciation. With a consistently high annual dividend growth, Toromont is an excellent candidate for building a high yield-on-cost position. Over the past 20 years, the company has achieved a CAGR of its dividend of 14.6%. 10-year yield on cost is approximately 8%.

Toromont Dividend Growth (DGAR)

In February, Toromont declared a quarterly dividend of $0.43, representing an annual increase of 10.3%. In 2023, expected dividends per share is $1.72, compared to $1.56 in 2022 and $1.36 in 2021.

{kind=link}

Returning Capital to Shareholders

Toromont recently renewed its normal current issuer bid, allowing the company to purchase up to approximately 8.2 million common shares or up to 10% of the public float in the 12-month period ending September 2023. In 2022 Toromont purchased and cancelled 473,100 common shares for $48.5M, this is inline with the company's 2021 NCIB which saw it purchase 470,600 common shares for $50.0M. Toromont calls the approximately $50M spent the past few years on share buybacks good "capital hygiene" as it mitigates the dilutive effect of exercised options.

Growth Tailwinds

In an effort to keep up with demand and optimize machine utilization, Toromont invested $215M in rental equipment in 2022, an 81% increase over the previous year. With the rental segment growing 17% year-over-year in 2022, this investment should help drive continued growth in this segment.

As the company clears its equipment sales backlog, Toromont is poised to benefit from a new wave of equipment orders driven by increasing infrastructure spending. The 2023 Federal Budget offers new tax credits to support investment in machinery and equipment used in clean technology supply chains and the extraction of critical minerals to support key clean technologies. This should be a strong tailwind for the Canadian mining sector.

The company's product support category is another growth catalyst for Toromont. The embedded diagnostic and connectivity tools in heavy equipment creates a stickier sales ecosystem that drives customer retention and recurring revenue from service, parts, maintenance and training. This high margin business line helps to diversify revenues and makes the company less dependent on supply chains, albeit more dependent on the availability of skilled labour.

Balance Sheet Strength

Toromont finished FY 2022 with total debt of $647M and cash on hand of $928M for a net cash position of $281M. The company's net debt to total capitalization ratio is an outstanding negative 14%. This strong cash position provides the company significant optionality to pursue M&A activity, invest capital to grow its distribution network or return capital to shareholders.

The company's balance sheet strength also reflects a prudent and conservative approach to leverage that has earned Toromont an "A (low)" credit rating. According to DBRS Morningstar :

DBRS Limited (DBRS Morningstar) upgraded the Issuer Rating and Senior Unsecured Debentures rating of Toromont Industries Ltd.'s (Toromont or the Company) to A (low) from BBB (high). The trend on the ratings has been changed to Stable from Positive.

This rating improvement is the result of several years of deleveraging the company's balance sheet following debt-financed M&A activity in 2017. Toromont maintains a strong liquidity position with $470M available in untapped credit lines provided by a consortium of banks.

Risk Analysis

In Toromont's recent letter to shareholders, the company cited supply chain constraints, general macroeconomic factors such as inflation, high interest rates, and lingering pandemic concerns as the key challenges faced in 2022. Toromont's current order back log is supportive, but the company doesn't want it to grow too large or drag on past 2023. Should the company fail to clear the majority of the backlog as it anticipates in 2023, it could shake customer confidence.

Toromont's growing product support and rental segments highlight the importance of being able to attract and retain skilled technicians. In the current labour market, attracting and retaining staff is a significant challenge that could drive up costs and impact margins.

There is a seasonality and cyclicality to the equipment sales business that can impact the timing of orders and reported results. Toromont's equipment sales segment in particular is highly exposed to the commodity cycle with a substantial portion of sales supporting mining and construction businesses.

Lastly, Toromont's business is inextricably tied to the Caterpillar brand. Should Caterpillar fail to continue its market leadership, or have its brand or corporate reputation tarnished, Toromont would be negatively impacted. Toromont is the exclusive Caterpillar dealer for a contiguous geographical territory in Western and Northern Canada. If Caterpillar ever decided to change its relationship with its dealers or cancel its contract with Toromont, the business would be imperiled. While this seems highly unlikely given that the relationship is long standing and positive for both parties, it is always worth noting an inordinate dependency on any one supplier or customer.

Investor Takeaways

Toromont is an attractive business that is poised to benefit from infrastructure spending and investment in green industries. The company's high-margin product support segment will benefit from connected equipment and real time data from its equipment sales and rentals. With more cash on hand than debt, Toromont has financial flexibility and strategic optionality to return cash or invest in growth segments. This company has one of the best dividend growth records in Canada, both in the magnitude and consistency of dividend increases. Toromont is a great holding for total return and growing dividend income over the long-term.

For further details see:

Toromont Industries: A 34-Year Dividend Growth Streak