TRMLF - Tourmaline Oil: A Must Have Low-Cost Natural Gas Producer Paying Special Dividends

2024-01-12 09:30:00 ET

Summary

- Tourmaline Oil is a large natural gas producer with strong earnings and cash flow, thanks to low operating costs.

- The company reported a net revenue of C$1.19B and a net income of C$275M in Q3.

- Tourmaline has a strong balance sheet and plenty of reserves, making it a low-risk choice for exposure to the natural gas sector.

Introduction

Tourmaline Oil ( TOU:CA ) ( TRMLF ) is a large natural gas producer with a very low production cost . The company is able to cover its entire capex program (including growth investments) while making its base dividend payments as long as the natural gas price trades above US$1.5/mcf. As the natural gas price has been trading above that level, even in the recent months when the natural gas price was pretty weak, Tourmaline has been spoiling its investor base with special dividends.

Q3 was decent, but what about weaker natural gas price?

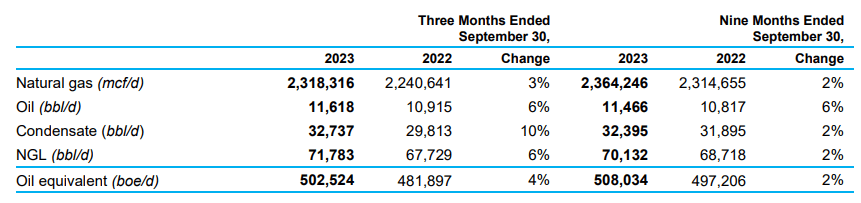

Tourmaline Oil still is a very large fossil fuel producer, with an average production rate of 502,500 barrels of oil-equivalent per day during the third quarter of this year. Oil and condensate accounted for less than 10% of the oil-equivalent production, and despite the name of the company, Tourmaline predominantly is a natural gas producer as natural gas accounted for in excess of 75% of the oil-equivalent output.

{kind=link}

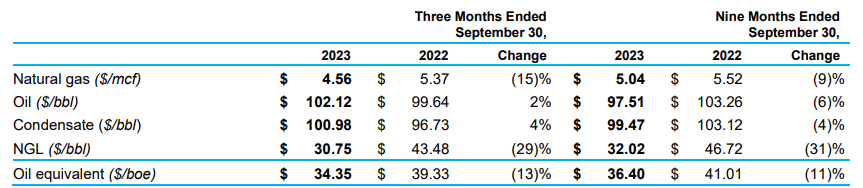

Thanks to its ability to access several different markets and hedge book, Tourmaline reported an average realized price of C$4.56 per mcf for its natural gas. The realized oil and condensate prices also were very strong, resulting in an average realized price of in excess of C$34 per barrel of oil-equivalent.

{kind=link}

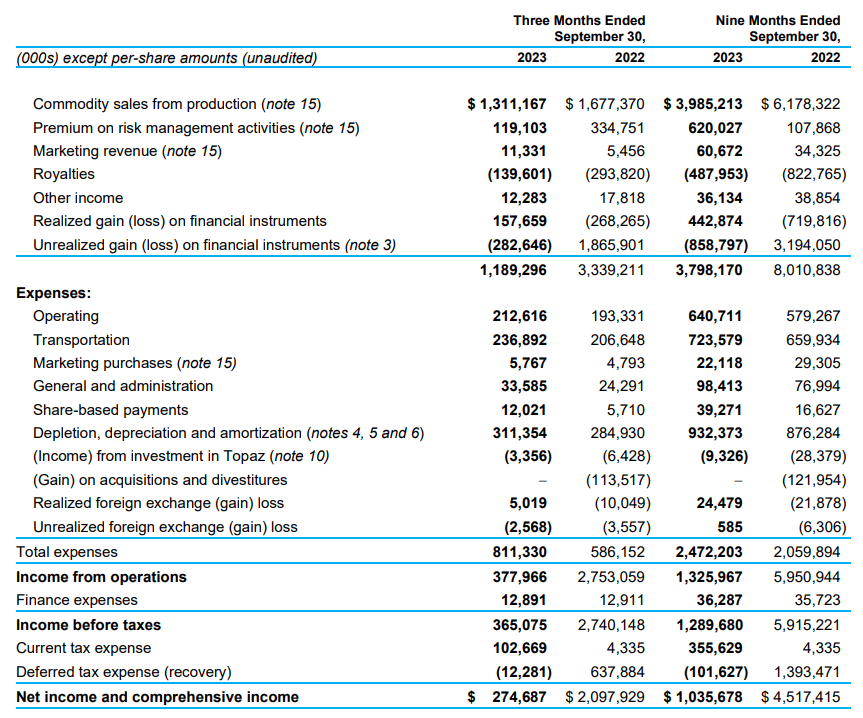

The company reported a total revenue of C$1.31B and a net revenue of C$1.19B after deducting the royalty payments and taking the derivatives into account. The operating costs are still exceptionally low – and that’s the main reason why I like to have exposure to Tourmaline, as the company has the ability to survive a prolonged period of low natural gas prices. The total operating expenses are just around C$0.5B, while the depreciation and depletion expenses add an additional C$311M to that, resulting in a total operating cost of C$811M.

{kind=link}

This means the operating income during the third quarter was approximately C$378M, resulting in a C$365M pre-tax profit and a net income of C$275M for an EPS of C$0.81.

The strong earnings profile indicates Tourmaline also is a cash flow monster. As you can see below, the reported operating cash flow was C$883M, including a C$93M working capital investment. That being said, the company didn’t pay any cash taxes while the C$158M gain on financial instruments (read: hedges) remained included.

{kind=link}

On a fully adjusted basis, the underlying operating cash flow was approximately C$872M including the hedge benefit and approximately C$714M excluding the hedges.

The total capex was approximately C$546M, resulting in a net free cash flow of approximately C$325M during the third quarter.

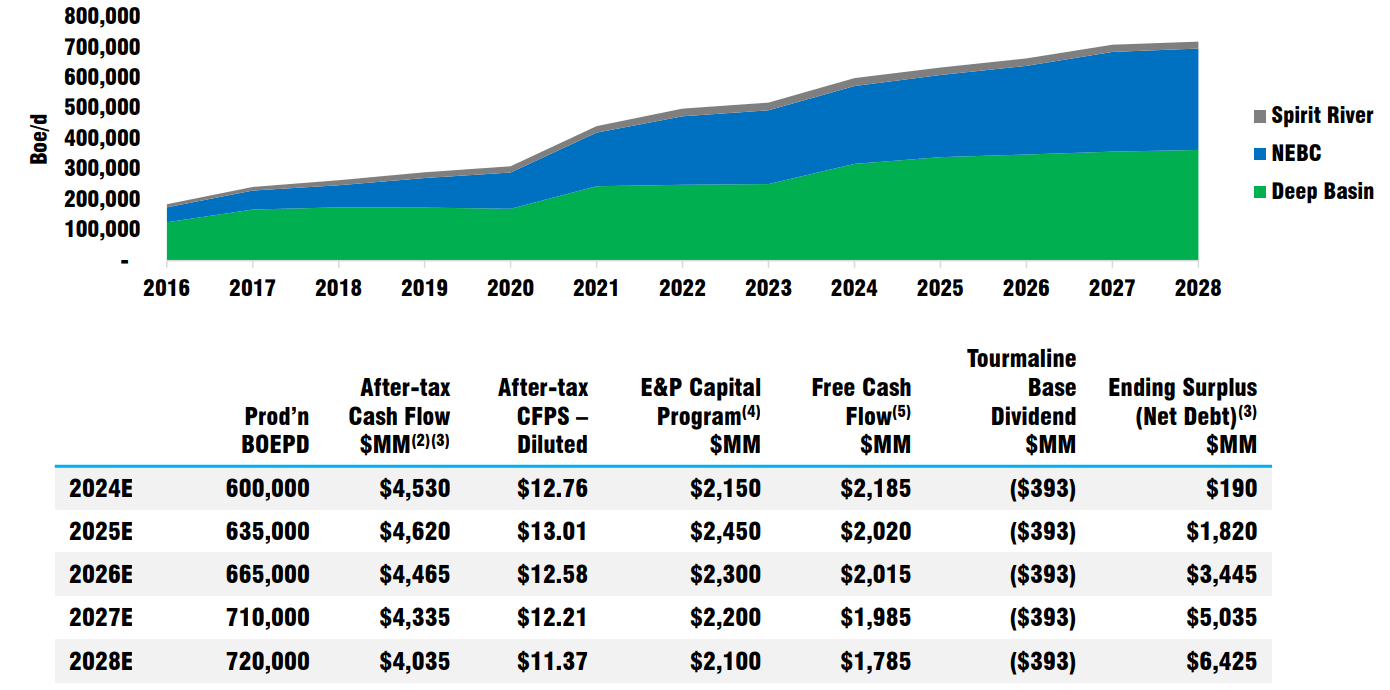

Interestingly, the company continues to invest in growth as its five-year growth plan anticipates a cumulative 20% production increase from 2024 to 2028. The start point of 600,000 boe/day in 2024 includes the impact of the recently closed acquisition of Bonavista Energy.

{kind=link}

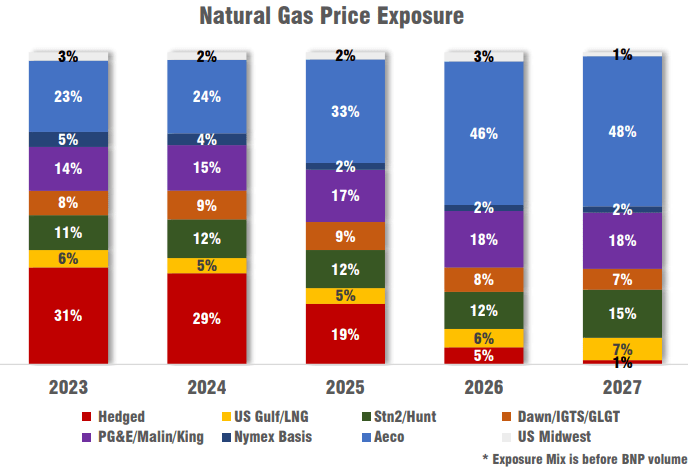

The image above is very important as it shows the long-term planning of Tourmaline and its anticipated annual cash flow and required capex to effectively increase the output. For 2025, for instance, Tourmaline is using a natural gas price of US$4.07 for NYMEX contracts while it uses an AECO natural gas price of just over C$4 per mcf. While those assumed prices are somewhat optimistic especially for AECO natural gas although two-thirds of the anticipated output in 2025 is either hedged or will be redirected to other markets, as you can see below.

{kind=link}

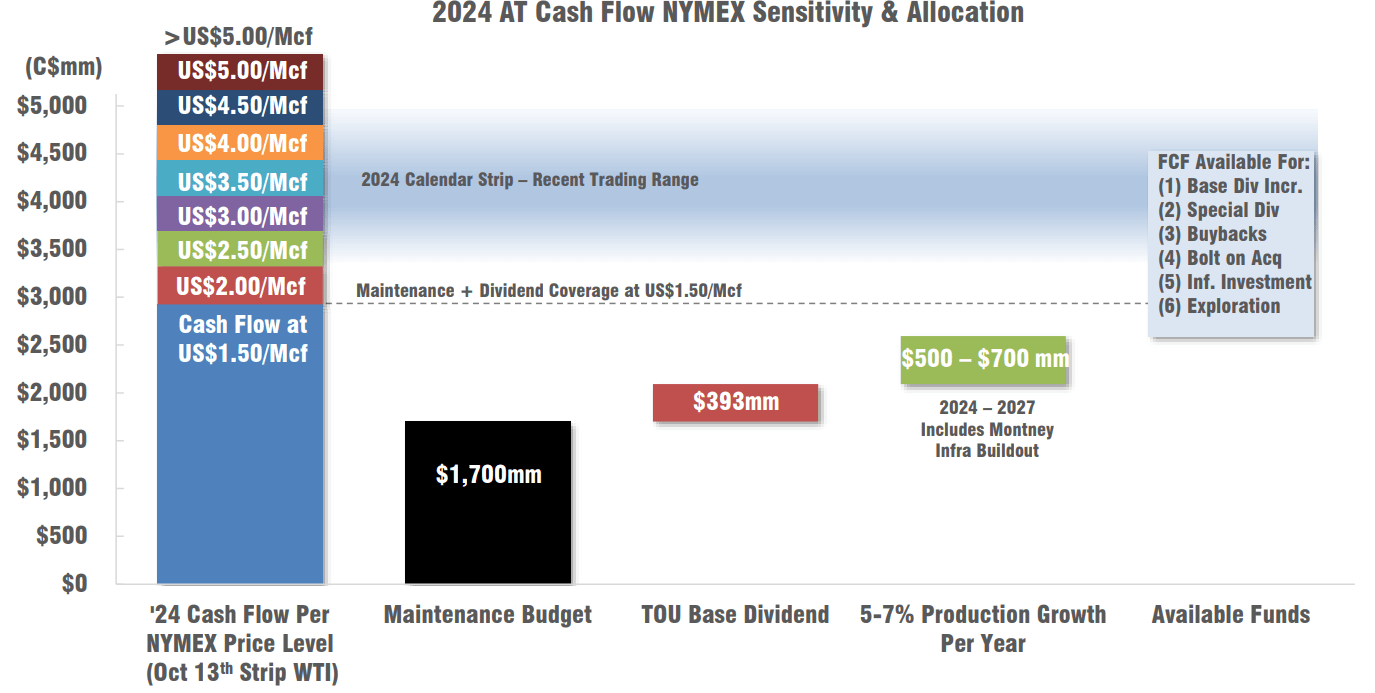

And just to make sure its investors understand the sensitivity of the company to the natural gas price, Tourmaline published this useful chart below. As long as the natural gas price exceeds uS$1.50 per Mcf, Tourmaline is able to cover its C$1.7B in sustaining capex as well as the base dividend. It anticipates it needs an additional C$500-700M per year to indeed grow its production by 5%-7% on an annual basis, and this also is fully covered by the anticipated cash flows at US$1.50.

{kind=link}

This means that even if you would use an average realized natural gas price of US$3/Mcf – which I think is not unreasonable at all – the after-tax operating cash flow would come in at around C$4B, leaving approximately C$1.2B on the table in net discretionary free cash flow after taking all capex and the base dividend into account.

It's my belief that discretionary free cash flow will predominantly end up in the pockets of Tourmaline’s shareholders as the company’s balance sheet is very strong with a total net debt of less than C$400M.

{kind=link}

And with approximately 4.5 billion barrels of oil-equivalent in its 2P reserve calculation, Tourmaline has plenty of reserves booked allowing it to grow at its own pace while being able to act on M&A opportunities like the Bonavista deal while continuing to pay special dividends to its shareholders.

Tourmaline Oil Investor Relations

Investment thesis

Tourmaline Oil is a must-have company if you want exposure to the natural gas sector, as its large reserve base, low-cost nature and very clean balance sheet make the company a pretty obvious choice for low-risk exposure to natural gas. The company will have paid in excess of C$5/share in common and special dividends in 2023, and thanks to the robust cash flow projections, I anticipate the company to continue to declare special dividends.

I have recently started building a position and I remain a buyer on any weakness in its share price.

For further details see:

Tourmaline Oil: A Must Have Low-Cost Natural Gas Producer Paying Special Dividends