INTC - Tower Semiconductor: The Tide Could Turn Soon Enough

2023-10-23 21:19:12 ET

Summary

- Weak industry conditions, a failure to close the merger, and geopolitical tensions have all weighed on Tower Semiconductor's prospects this year.

- TSEM is not sitting on its hands from the failed deal and has moved on to sign a new collaboration with Intel, which makes a lot of sense to us.

- There are signs that the worst is over, and TSEM could deliver solid operating leverage next year.

- The forward valuations are dirt-cheap and we are enthused by the risk-reward on the charts.

Not The Flavor Of The Season

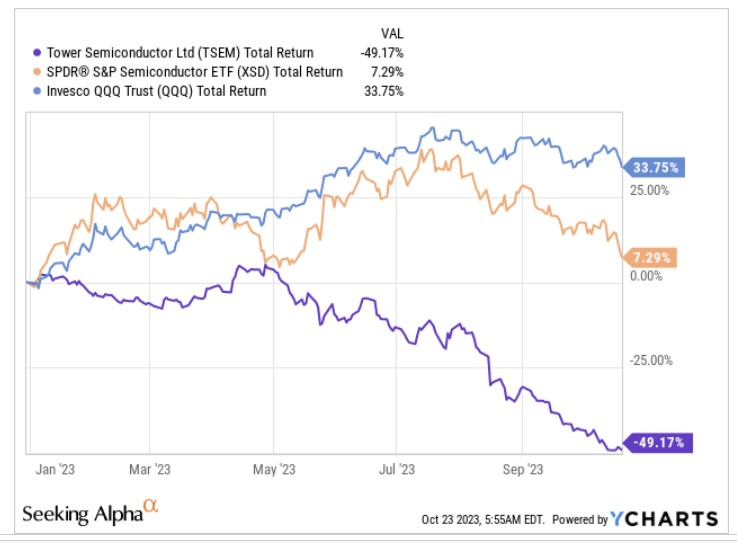

The stock of Tower Semiconductor Ltd. ( TSEM ), a leading foundry play that is noted for its expertise in advanced analog chips, has faced an egregious 2023 so far. Even as the tech benchmark has expanded its value by a third, and TSEM’s semi peers have managed to deliver unremarkable but positive gains, our focus stock has been taken to the cleaners, losing almost half its value this year.

{kind=link}

There are a few reasons why Tower Semi has been on a slump.

Firstly, inventory adjustments particularly across the consumer electronics and smartphone markets for large parts of 2022/2023 have left an adverse mark on demand, then, TSEM received a punch to the gut, when a regulatory impasse prompted Intel ( INTC ) to walk away from a potential $5.4bn deal to acquire the former.

Then, recently, the Israeli-Palestinian tensions too have weighed heavily on sentiment, given that TSEM has two manufacturing facilities (Fab 1 and Fab 2) and a number of sales and corporate offices in Israel. The company has previously noted how its business partners and suppliers have reneged on certain agreements during periods of heightened unrest and tension.

Given all these dynamics, it's no surprise to discover that TSEM isn't the flavor of the season. Nonetheless, we believe most of these challenges are rather ephemeral, and there are still some silver linings that raise TSEM’s allure, particularly at current levels.

Never Mind The Merger Deal, The Recent Intel Collaboration Should Be Welcomed

We feel that the market is unnecessarily fixated on the failure of TSEM and INTC to get the $5.4bn merger deal over the line. What’s heartening is that TSEM management is not wasting time licking its wounds, and has moved on to a new collaboration with Intel, which will now see TSEM use the former’s foundry services and 300mm manufacturing capacity in New Mexico to meet advanced customer requirements.

We mainly like this tie-up for the greater thrust on 300mm capabilities which should advance TSEM’s customer pool greatly. For instance, take TSEM’s RF SOI (Radio frequency silicon on insulator) solutions. It’s evident that the 5G upgrade cycle has legs; here, TSEM’s RF SOI solutions can provide a useful edge in driving greater adoption as it is typically less demanding on the average smartphone battery. These RF SOI solutions are also believed to have rather low Ron-Coff figures of merit and can facilitate high linearity RF switches. Given these merits, TSEM needs to find a cost-effective and quick solution for manufacturing at scale.

Rather than committing significant time and CAPEX in setting up its base, this asset-light tie-up with Intel won’t burn a hole in TSEM’s pockets, as the $300m charge, can comfortably be covered by the $353m fee that the company will anyway receive from Intel for terminating the previous merger.

Even if there are delays in procuring that fee, TSEM still has a solid chunk of short-term deposits and marketable securities that can be liquidated, not to mention the standalone cash balance (in aggregate all these items add up to a hefty $900m ). If this agreement works well, there are suggestions that TSEM could pursue “multiple unique synergistic solutions” with Intel; if not, TSEM can always feel free to walk away as they haven’t bet the farm with huge capital commitments towards this venture.

Potential Operating Leverage and Forward Valuations

Given that a large component of Tower Semi’s cost base comprises of fixed costs, it's important for the business to recommence a phase of decent operating leverage, after what will likely be a difficult FY23. There are now signs that important segments such as PC and smartphones are stabilizing with Counterpoint Research suggesting that the latter segment may already be seeing an end to the trend of YoY decline in sales.

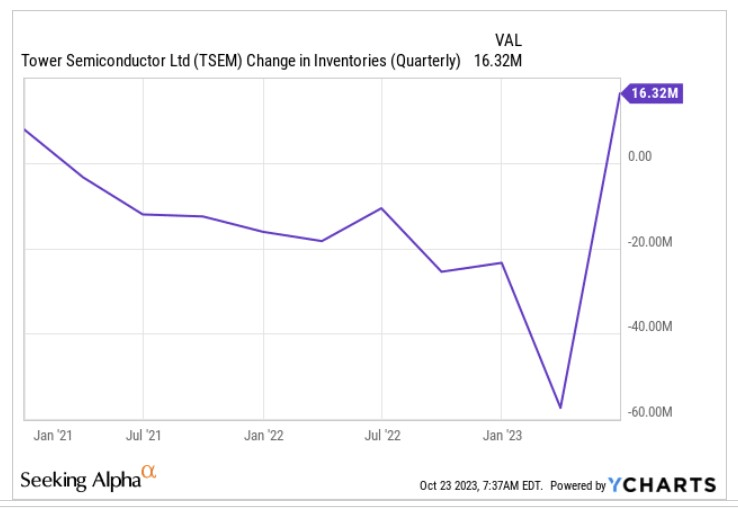

A pickup in the demand environment can also be gleaned by the fact that after 9 straight quarters of building inventory, TSEM resorted to drawing this down in Q2, consequently resulting in this component serving as a source of operating cash flow.

{kind=link}

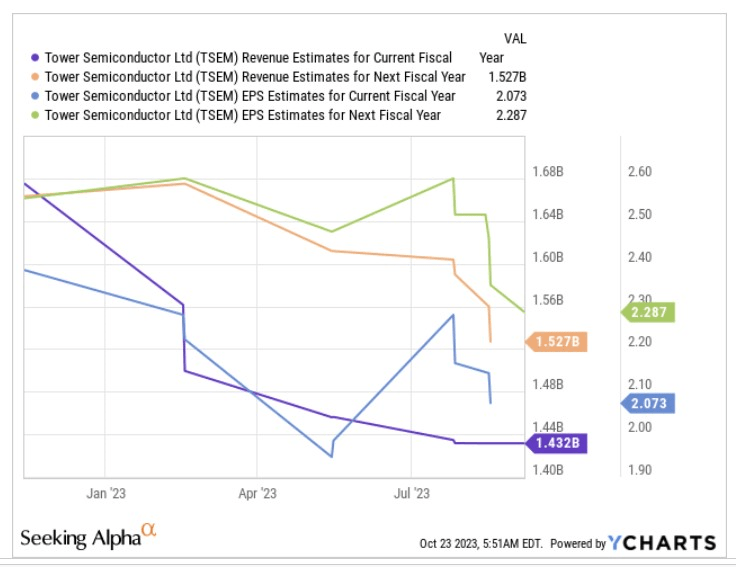

Nonetheless, as per YCharts consensus, once this year is out of the way, in FY24 investors will get to see TSEM throw up a healthy dose of operating leverage, with the company’s FY24 EPS growth of 10.3%, poised to come in at 1.5x the level of topline growth.

{kind=link}

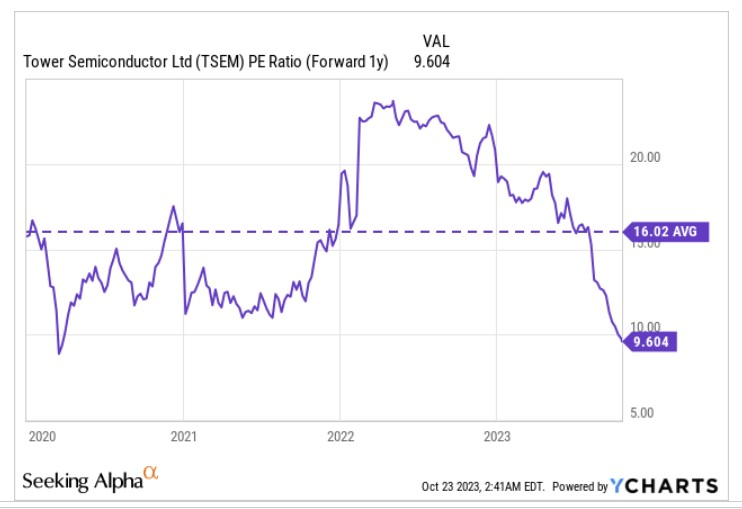

For a business that is poised to generate that level of earnings growth (implied PEG of less than 1x) and solid operating leverage, we feel the stock is very cheaply priced at only high single-digit forward P/E levels (something which doesn’t happen too often). Put another way, getting in now means you get to lock in an attractive 40% discount, relative to the stock’s 5-year average of 16x!

{kind=link}

Closing Thoughts - Technical Considerations

We also like the overall risk-reward on the charts.

The first chart helps to determine if TSEM could work as a suitable rotation option within the broad semiconductor space. We’d like to think that TSEM could be a decent bet as its current strength, relative to XSD, is around 82% off the mid-point of its long-term range. Crucially, the relative strength ratio has now dropped to the cyclical lows, last seen in 2014, and 2009, after which we saw a bounce back.

{kind=link}

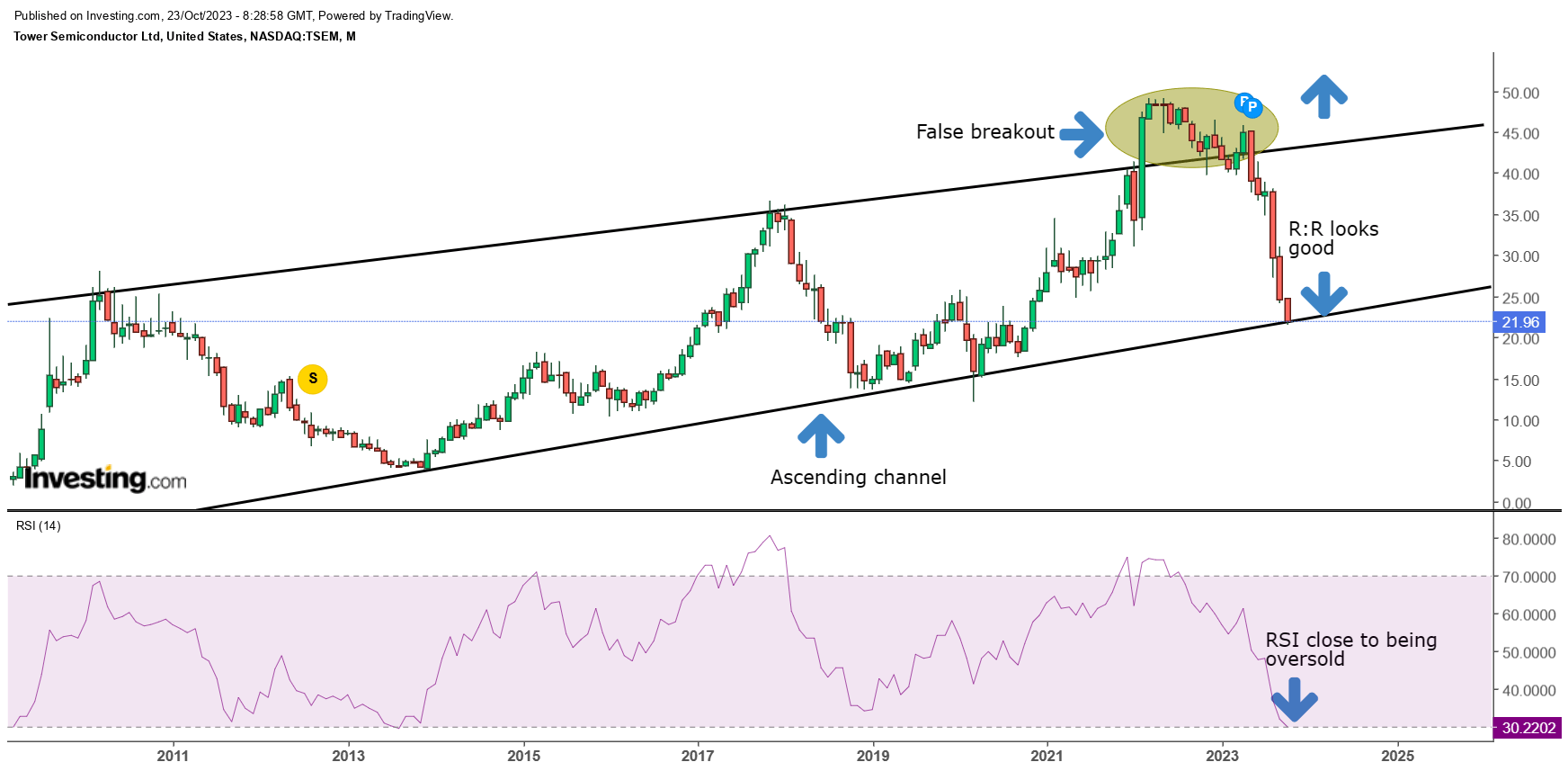

The chart below measures TSEM’s price imprints on a monthly basis, and what we can see is that since the GFC, these imprints have broadly taken place in the form of an ascending channel. Last year in Feb, it first seemed like we had witnessed a breakout from this channel, but the stock failed to build on that momentum, and after spending months dilly-dallying outside the channel boundary, we saw strong bouts of selling since May 2023.

{kind=link}

Interestingly enough, we’ve now seen a rapid fall down to the lower boundary of the channel, making the reward-to-risk dynamics look rather attractive. It's also worth considering that the RSI indicator has dropped to 10-year lows and is hardly a breath away from hitting oversold readings.

If you're an investor with an aggressive risk appetite, we wouldn’t be averse to suggesting a long position at these levels, considering potential support at the lower boundary, supplemented by the RSI almost hitting oversold levels.

Nonetheless, if you're more conservative in nature, we'd urge you to wait until you see the price action flatten out. Whilst this happens, also look out for an RSI divergence , which would only serve to increase the degree of confidence for going long.

For further details see:

Tower Semiconductor: The Tide Could Turn Soon Enough