TPG - TPG And Angelo Gordon Are The Ideal Pair For Growth And Stability

2023-12-23 01:14:25 ET

Summary

- TPG, a multinational private equity firm, has seen a 71.60% YoY decline in Q3'23 revenue but a 577.39% increase in free cash flow due to M&A activities.

- TPG has completed a $2.7bn acquisition of Angelo Gordon and purchased a >$1bn stake in Toronto RE, expanding its revenue base and diversifying its portfolio.

- Despite being no longer undervalued, TPG maintains a 'buy' rating due to its growth potential, low cost of capital, and investor-aligned capital allocation approach.

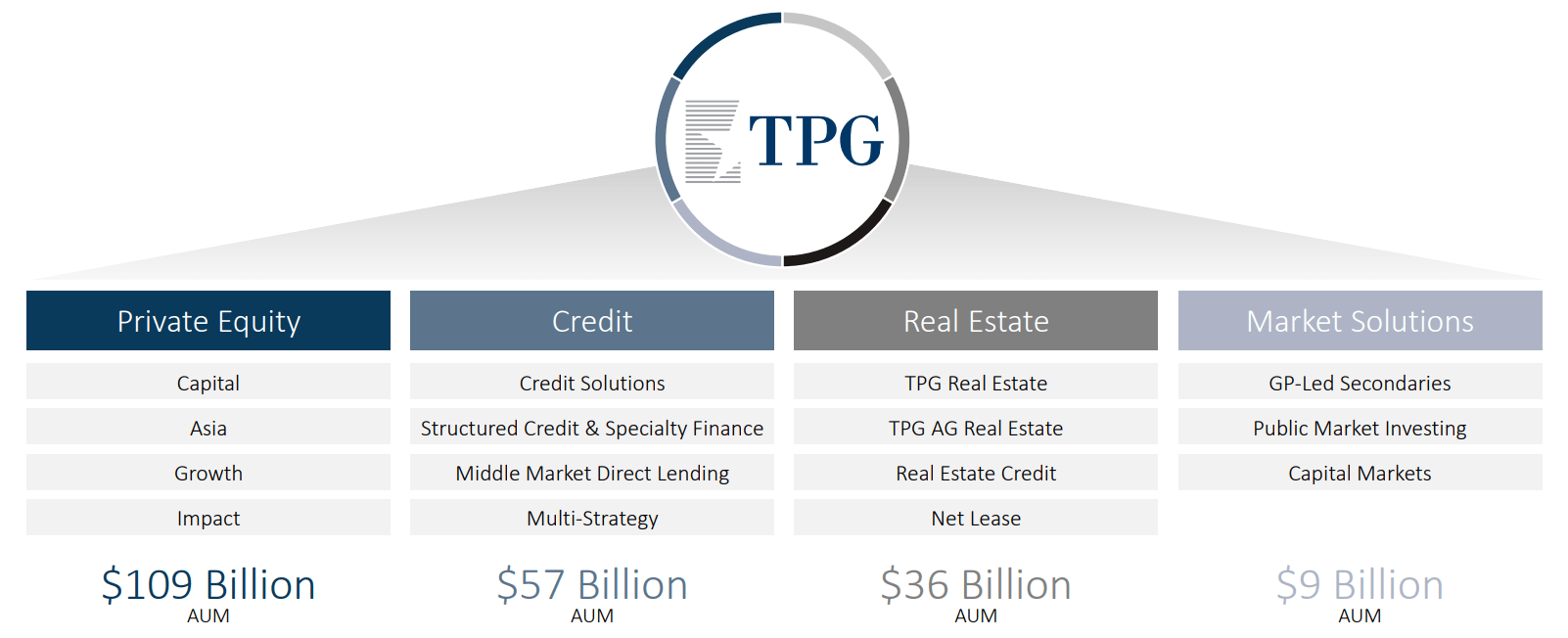

TPG (TPG), formerly the Texas Pacific Group, is a Fort Worth, Texas-based multinational private equity firm with verticals ranging from participation in private equity markets to private credit solutions, from real estate to more specialized market solutions.

{kind=link}

Through these activities, TPG has seen a Q3'23 revenue of $159.39mn- a 71.60% YoY decline- alongside a net income of $11.67mn and a free cash flow of $402.07mn, a 577.39% increase driven by excess cash from operating activities owing to M&A activities.

Introduction

In my previous article- since TPG has returned ~66%, contrary to the ~15% returned by the S&P 500- I rated TPG a 'buy', a decision driven by the company's alternative asset growth and low cost of capital.

Since then, TPG has exercised the significant level of dry powder it maintained to complete its $2.7bn acquisition of Angelo Gordon, helping expand the company's revenue base and diversify its portfolio. Most recently, TPG purchased a >$1bn stake, equivalent to 75% ownership, in Oxford's Greater Toronto Area Industrial portfolio , representing its continued commitment and capability to expand its FAUM.

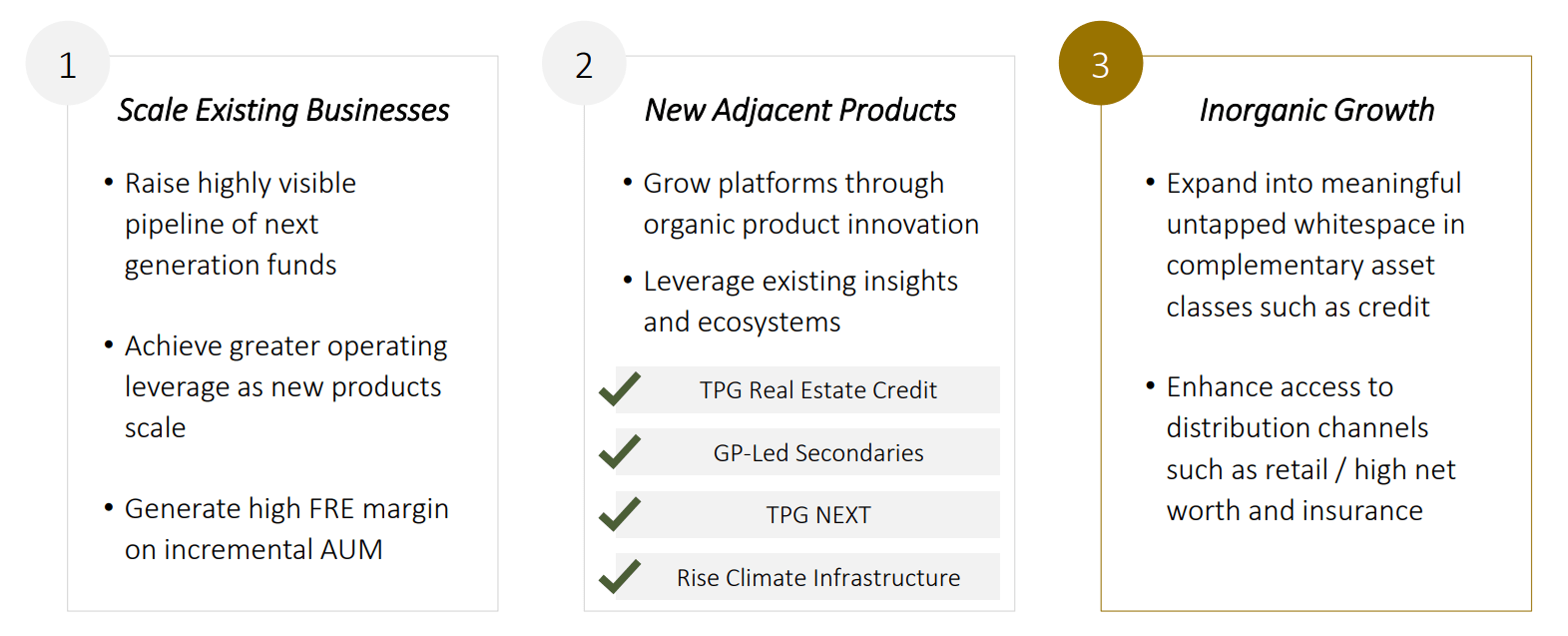

While TPG's value proposition has shifted from being an undervalued firm to one with significant synergistic growth potential, the firm's core operational strategy remains the same; TPG aims to scale existing verticals while moving forward toward organic growth into adjacent offerings, and aggressively pursuing inorganic growth opportunities and undervalued prices.

{kind=link}

This strategic philosophy, combined with TPG's generous capital deployment strategy, and the expected synergetic growth from Angelo Gordon lead me to maintain TPG's 'buy' rating- more caution, however, is necessary, since the company is no longer fundamentally undervalued.

Valuation & Financials

Trailing Year Performance

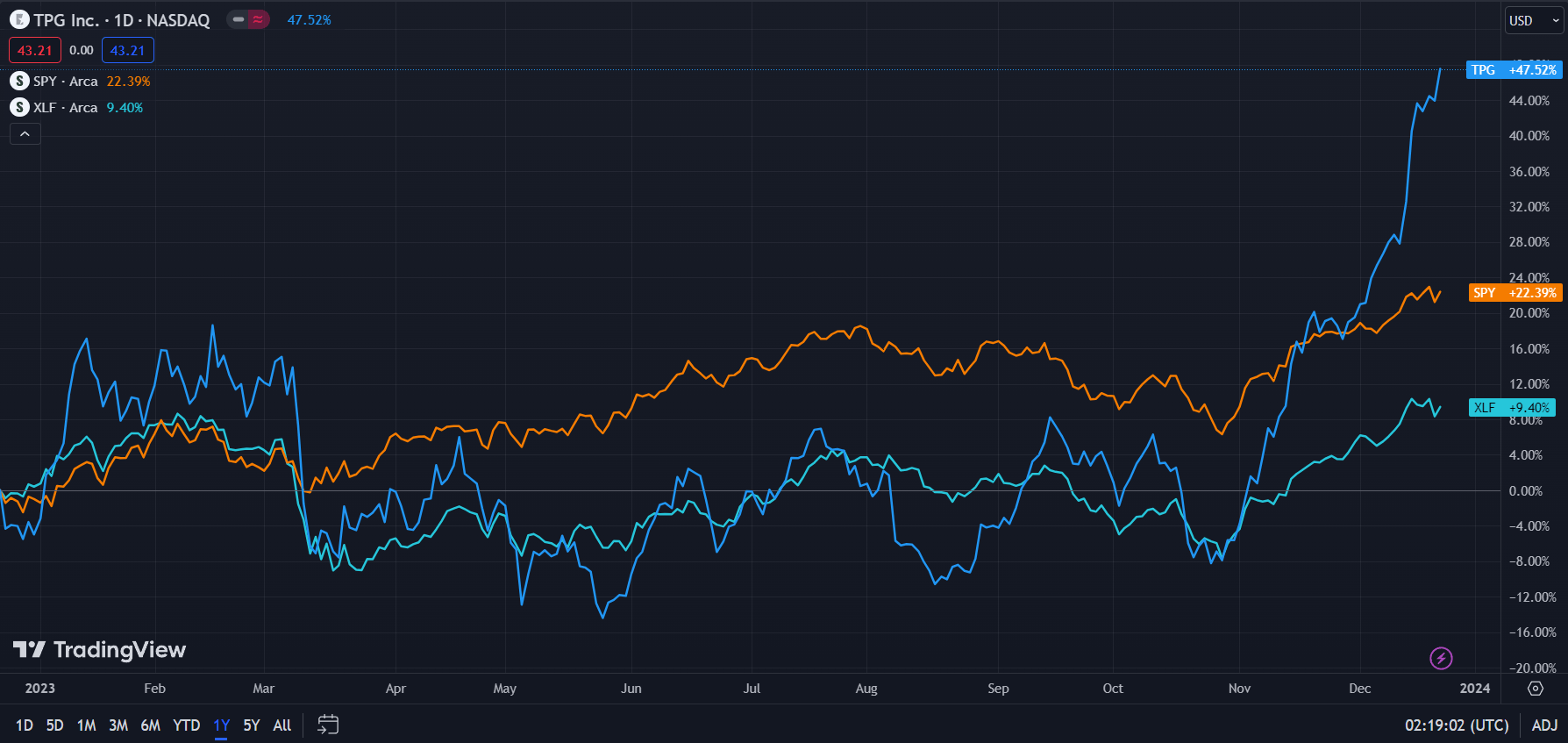

In the TTM period, TPG's stock- up 47.52%- has outperformed both the financial services industry, as represented by the Financial Select Sector SPDR Fund ( XLF )- up 9.40%- and the broader market, represented by the S&P 500 ( SPY ), up 22.39%.

{kind=link}

While the financial services industry has lagged the market likely due to industry-specific volatility- especially associated with macro uncertainties and the bank crises earlier in the year- TPG has seen substantial outperformance, likely a product of its accretive purchase of Angelo Gordon.

Despite this growth, I believe TPG maintains outsized growth potential, with the prospective accretion of the acquisition priced-in but the long-run operational strategy undervalued in my opinion.

Comparable Companies

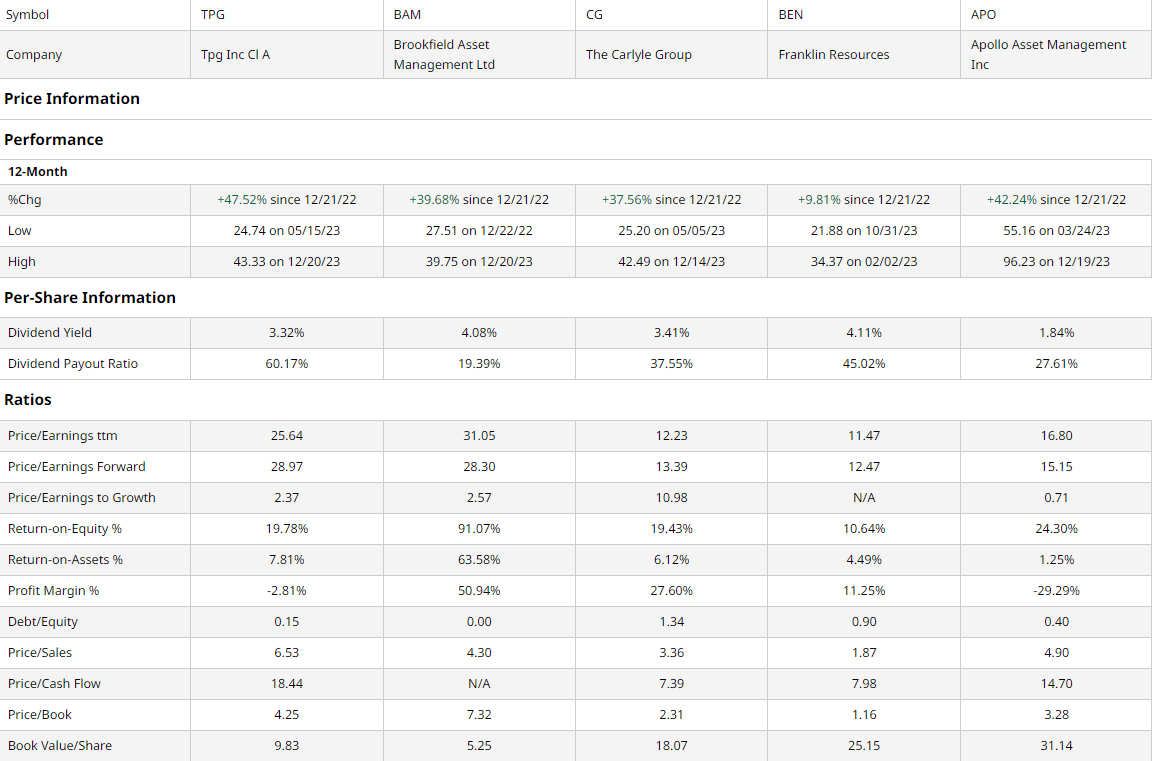

As TPG's focus has evolved beyond the private equity space into private credit and real estate verticals, the firm's competitive horizon has expanded to include broader-focus asset managers in addition to other private equity majors. This includes the Brookfield Corporation ( BN ) spinoff, the Toronto, Canada-based Brookfield Asset Management ( BAM ), the Washington, D.C.-based private equity leader, the Carlyle Group ( CG ), the mutual fund-focused ~$1.4tn AUM asset manager, the New York City-based Franklin Resources ( BEN ), and credit and insurance-focused PE leader, Apollo Global Management ( APO ).

{kind=link}

As demonstrated above, TPG has seen best-in-class TTM returns, seeing 47.52% growth, though the private equity field as a whole has seen superior growth in the market. Despite this growth, I believe TPG maintains a sizeable runway for growth, owing principally to the company's growth capabilities and investor-aligned capital allocation approach.

For example, although TPG may see inferior multiples-based value, based on higher PE, P/S, and P/CF ratios, the company maintains the lowest PEG ratio, third-highest ROE, and second-lowest debt/equity, enabling a lower cost of capital and greater reinvestment capabilities.

Moreover, the firm sees a respectable 3.32% dividend, recently declaring a $0.48/share dividend.

Valuation

According to my discounted cash flow analysis, at its base case, the net present value of TPG is $47.58, meaning, at its current price of $43.21, the stock is undervalued by 9%.

My model, calculated over 5 years without perpetual growth built-in, assumes a discount rate of 9%, raised from my last model due to higher debt levels and a higher cost of capital. I furthermore assume a forward 5Y arithmetic average revenue growth rate of 12%, increased from my previous analysis due to M&A activities, but still lower than the trailing average of ~24.36%.

{kind=link}

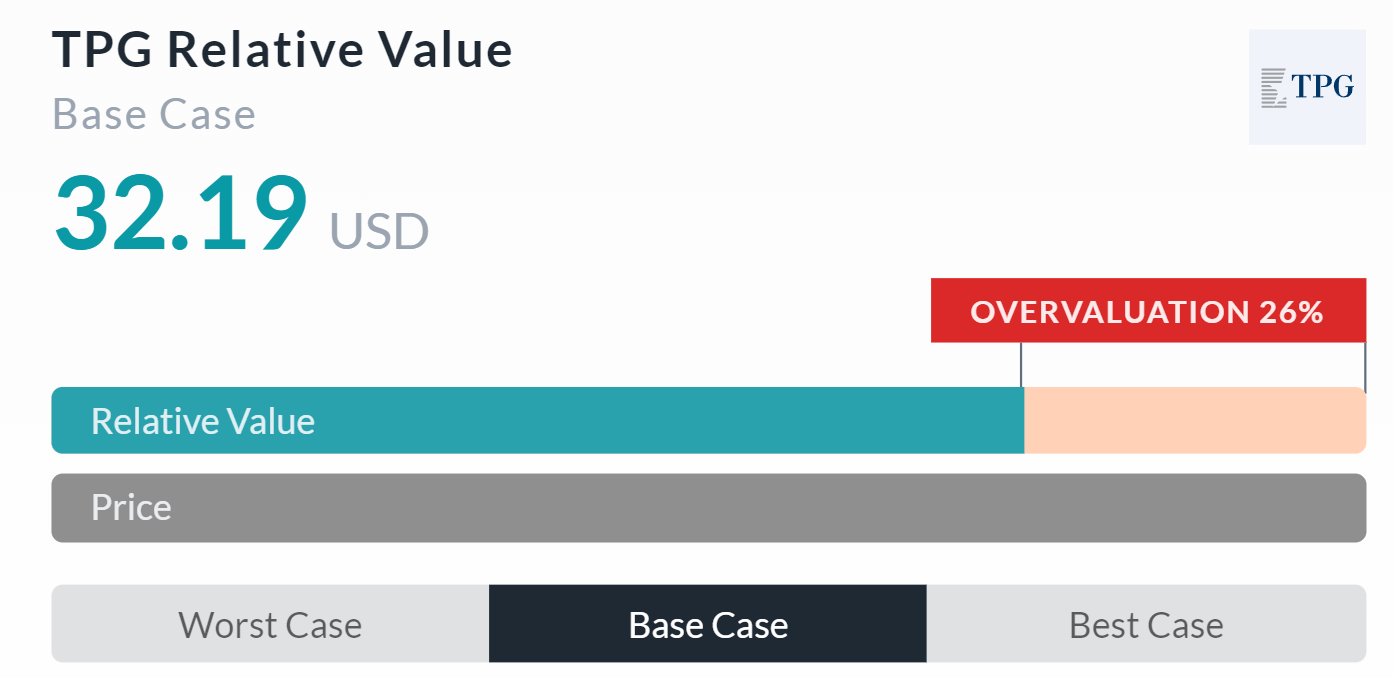

Alpha Spread's multiples-based relative valuation tool, on the other hand, estimates an overvaluation of 26%, with a relative value of $32.19. However, I do believe Alpha Spread's model fails to account for the growth inherent to TPG's M&A strategy and how that growth will temper the firm's multiples-based value.

As such, taking a weighted average between my NPV and Alpha Spread's relative valuation, skewed towards my model, TPG's fair value is $43.95, representing a 2% undervaluation.

TPG's Aggressive Expansion Enables Complementary FAUM & Income Growth

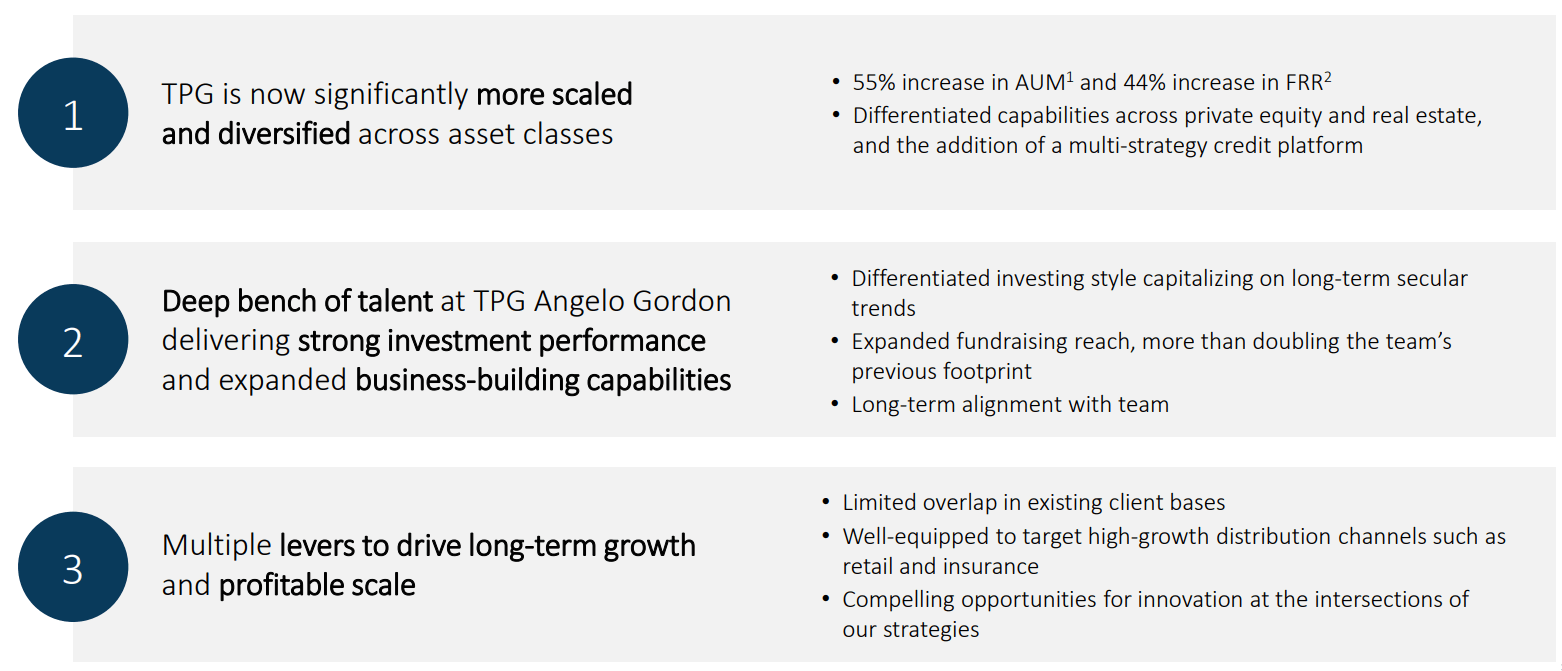

The central bull theme for TPG surrounds its ability to find accretive M&A opportunities and maximize associated synergies. With Angelo Gordon, TPG does just that; the firm looks to integrate Gordon's >$57bn credit platform, allowing TPG to amplify its access to the 12% CAGR private credit industry, broaden TPG's real estate platform, diversifying the TPG portfolio, and meaningfully integrating and upselling existing TPG products to Angelo Gordon clients.

{kind=link}

TPG thus is able to realize significant scalability and diversification and the benefits which come with it- namely lower long-run cost of capital and lower price volatility. In the same vein, TPG may recognize greater operational synergies as well, able to access a pre-existing talent pool, ascertaining a greater volume of personal relationships and contributing to general business-building. And, as aforementioned, TPG may see even greater revenue diversity, with access to retail distribution channels and insurance asset pools.

{kind=link}

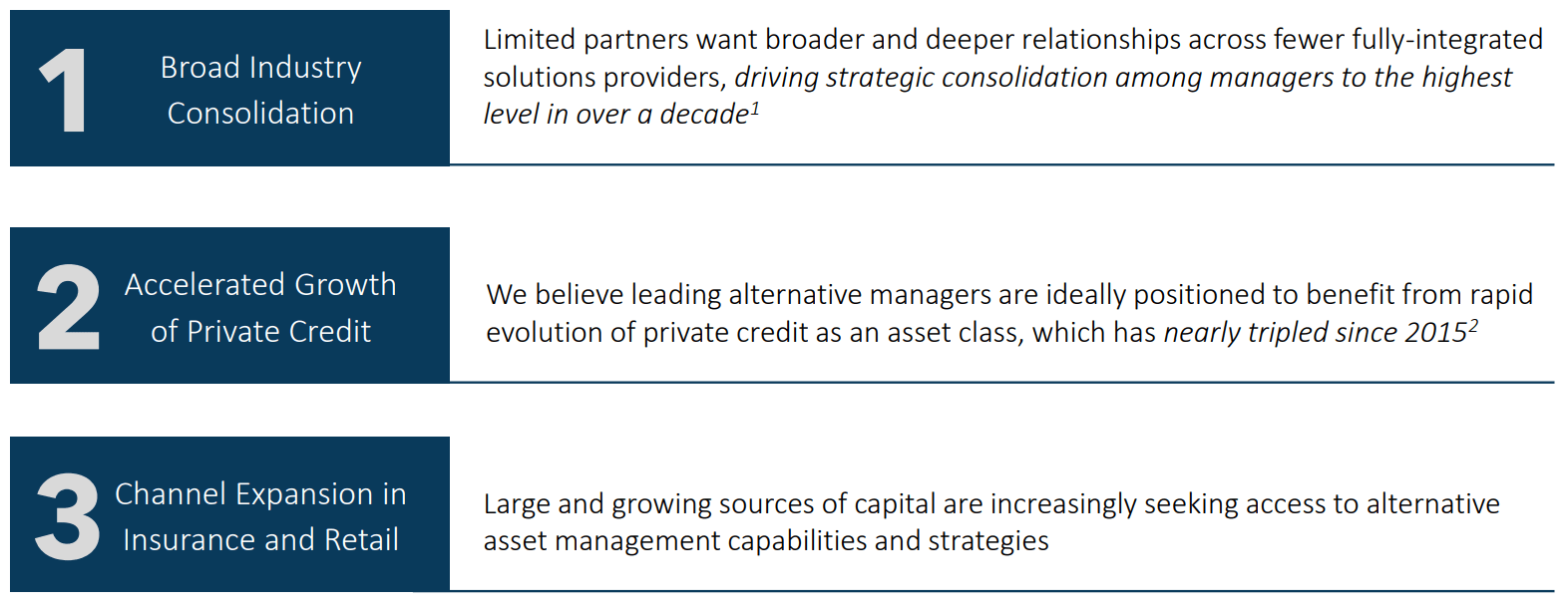

Above all else, TPG seeks to leverage pre-eminent industry megatrends to establish a strong growth base. TPG is already participating in widespread industry consolidation, allowing TPG to carve out its own niche and, through scale, promote stability and a lower cost of capital, in reference to both debt and equity financing. As previously discussed, TPG's parallel organic and inorganic expansion has enabled access to the rapidly developing private credit industry and sources of retail and insurance capital for FAUM.

{kind=link}

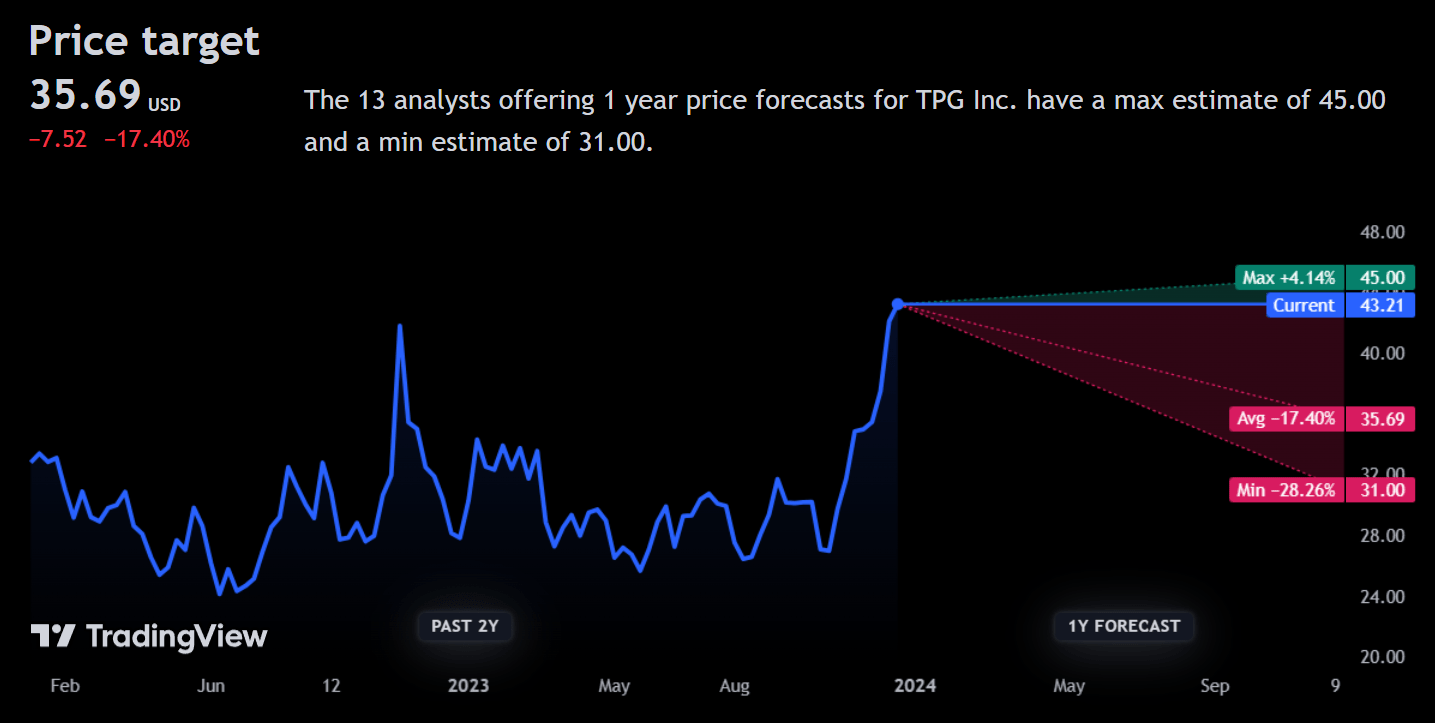

Wall Street Consensus

Analysts generally disagree with my more positive view of TPG, estimating an average 1Y price target of $35.69- a 17.40% decline.

{kind=link}

At the lowest projected price target, analysts remain highly pessimistic, estimating a price of $31.00, reflecting a 28.26% price decline.

However, I do believe that Wall Street's opinion has not yet been updated to indicate the accretive effects of the Angelo Gordon acquisition and the Toronto RE transaction; for instance, GSCO recently updated TPG to a 'buy' , citing the potential of TPG's M&A strategy.

Risks & Challenges

Higher Cost of Capital May Hinder Further Growth & Fundraising Capabilities

Although TPG foundationally retains a flexible cap structure, the company has seen increased debt volumes following its aggressive M&A strategy and thus must contend with higher rates and lower cash flows. Donovan Jones' call for clarity on the long-term outcomes associated with the Angelo Gordon deal is also a key indicator of how higher debt will affect the company.

Regulatory & Consequent Compliance Costs May Compress Margins

Private credit and private equity make up a bulk of both TPG's existing portfolio and its operational strategy; both are under scrutiny for their relative opacity to public credit and equity operations. Therefore, TPG may have to contend with greater regulatory impacts which may inhibit growth, particularly inorganic growth and private credit margins.

Conclusion

Looking forward, although TPG has seen remarkable TTM growth, the company remains growth-oriented with significant synergistic growth across private credit and alternative assets.

For further details see:

TPG And Angelo Gordon Are The Ideal Pair For Growth And Stability