BRSP - TPG RE Finance Trust: 13% Jump In One Week 11% Dividend And 23% More Upside

Summary

- TPG RE Finance Trust or TRTX is one of a number of commercial mortgage REITs I've been investigating this past year.

- Recent earnings results caused a double-digit jump in stock price from levels seen last week. But the stock still sports an 11% dividend.

- Is there still value in the stock after the jump? That's what we'll explore.

TPG RE Finance Trust (TRTX) is a commercial mREIT that I wrote up for our subscription service the Microcap Review back on January 13. The piece was an in-depth review of the company's history including recent turnaround efforts with new CEO Doug Bouquard who joined just last year, as well as a look at their current book to estimate value. The stock price has been pressured for a number of years due to a margin call error back in 2020, and more recently due to the changing nature of office properties which the company is invested in. Since Bouquard joined management has actively reduced their exposure to this sector while building up a sizable chunk of liquidity and cash.

When I started investigating the stock it was trading at nearly half of book value. I did a review of their book and to come up with my base case estimate I discounted all of their risk rated 4 loans by 25% and then further discounted total book value 23% to arrive at my $10.58 1-2 year target. Here's the table from that article with my range of estimates.

| Valuation Method |

| Price |

| Price from January Article |

| Implied Return |

| Dividend Yield |

| 2-Year Implied Return with Dividend |

| Assume specific CECL reserves, 4 rated loans cut 100% [BEAR CASE] |

| $4.87 |

| $7.94 |

| -38.66% |

| 12.10% |

| -14.46% |

| Assume specific CECL reserves, 4 rated loans cut 50% |

| $10.64 |

| $7.94 |

| 34.01% |

| 12.10% |

| 58.21% |

| Assume specific CECL reserves, 4 rated loans cut 25% |

| $13.74 |

| $7.94 |

| 73.05% |

| 12.10% |

| 97.25% |

| Peer Average P/B 0.66 Reversion with 25% implied cut |

| $9.07 |

| $7.94 |

| 14.23% |

| 12.10% |

| 38.43% |

| 5-year Average P/B 0.77 reversion with 25% cut [BASE CASE] |

| $10.58 |

| $7.94 |

| 33.25% |

| 12.10% |

| 57.45% |

| P/B 1x reversion [BULL CASE] |

| $14.28 |

| $7.94 |

| 79.85% |

| 12.10% |

| 104.05% |

What these price targets showed me back in January is that it would require severe losses in their portfolio to justify the current price. Since the article, TRTX released quarterly and full-year results for 2022 last week on February 21st where they beat expectations on both the top and bottom lines. A couple of key things came through this report suggesting portfolio stability:

- GAAP net income was $32.6 million of $0.42 per diluted share, a 16% QoQ increase. This was driven in part by rising benchmark interest rates driving net interest margin.

- Distributable earnings of $0.30 for the quarter covered the $0.24 dividend 1.25x. Full year dividend coverage was 1.17x.

- Book value per share actually increased marginally to $14.48 per share due in part to an $11 million CECL reversal.

- Liquidity was $590.9 million at year end with 39% of ($231.7 million) in cash. Another $297.2 million is CLO reinvestment cash.

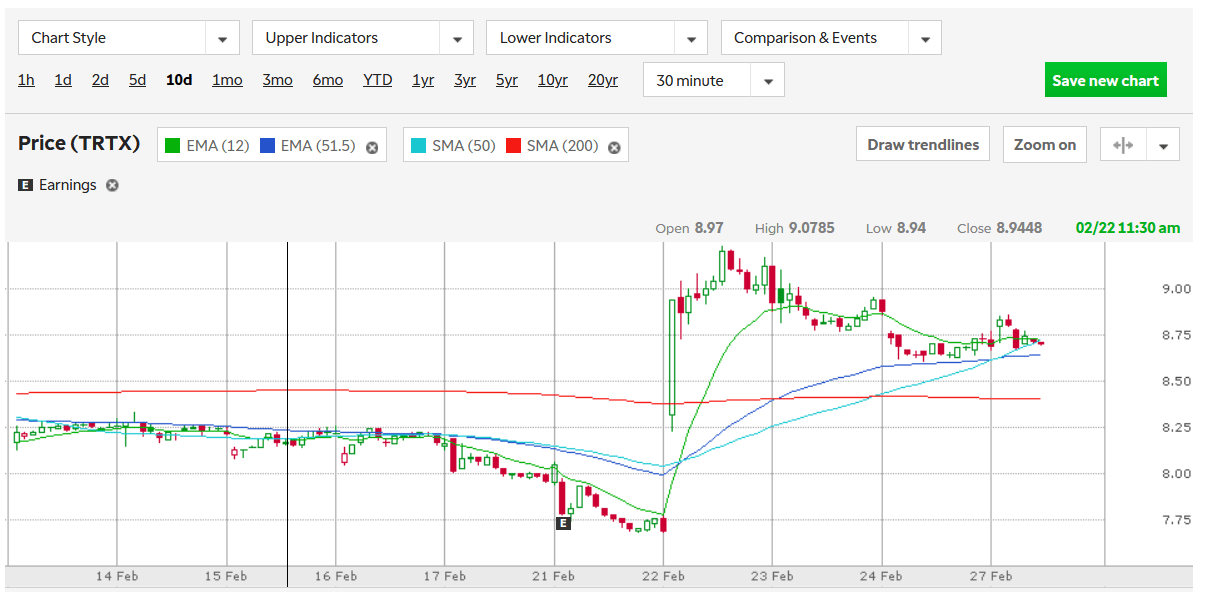

The company continues to trade well below book value with a P/B ratio of ~0.60x based on TRTX stock price as of writing at $8.67. But a look at the chart shows that earnings results triggered a run-up in the stock price last week.

TD Ameritrade: 10-day TRTX Chart.

{kind=link}

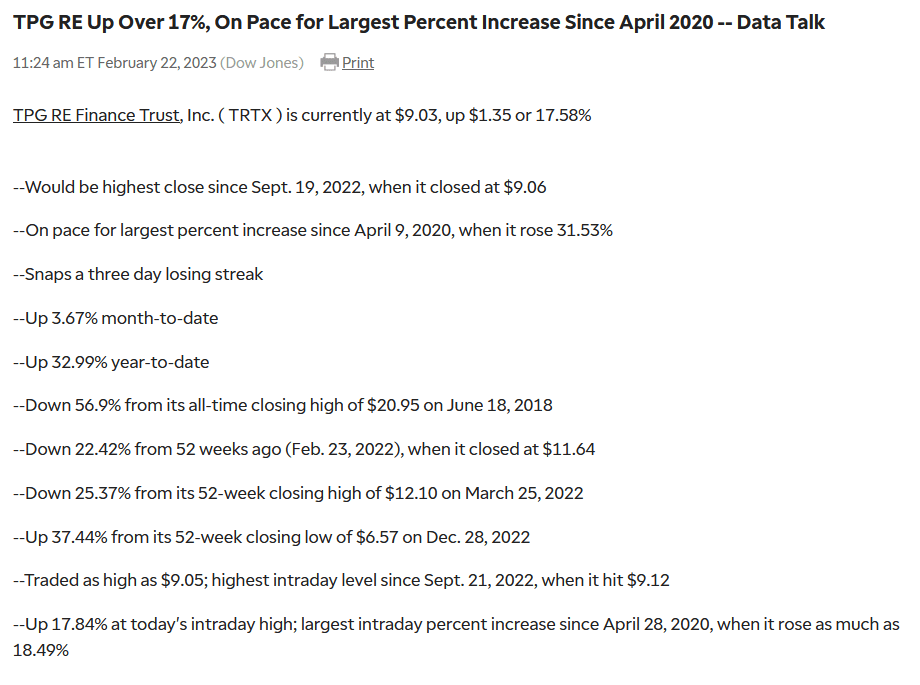

There was a gap from the Feb. 21st close of $7.68 to the $8.32 open the next day as the market digested the news. That jump represented one of the largest percent increases since April 2020:

{kind=link}

Despite the recent run-up, the covered annual dividend still offers an 11% yield and the company remains below book value. In this article, we'll update the price targets given full-year results to get more approximated price targets. Then, we'll compare the universe of peers to get a sense of what is the right P/B multiple to apply for valuation.

TRTX Valuation Updates

Starting with the bear case scenario the key variable here is the loans at a 4 risk rating. The reason here is that the company has a specific CECL reserve largely set aside for their 5 risk rating loans already. I think we can take the specific reserves as a reasonable estimate of the value of those loans. But the 4 risk rating loans are covered through their general CECL reserve.

As of their 2022 10-K amortized cost for their twelve 4-rating loans was ~$990 million. Total stockholder equity came in at $1,121 million which includes a general CECL reserve of $130 million. This reserve would first be depleted before eating into equity value which means we'd end up with stockholder equity of $261 million.

There are 71.41 million shares outstanding as of year end which means per share value of TRTX would be $3.65. From prices of $8.67 that would represent a 58% decline. Our bear price target estimate has actually decreased from $4.87 given in our last analysis. The main reason for this is that there were only 11 loans with a risk rating of four, now there are twelve. I believe it would take extreme circumstances for this scenario to come to pass.

Moving on to a more moderate assumption, let's assume that these 4-rating loans lose 50% of their value. That would result in a $495 million adjustment eating up the general CECL reserve and leaving $756 million in equity value. In that case, the book value per share would be $10.59 or 22% higher than current prices.

And finally, a 25% haircut on these loans would be a $248 million adjustment. When we consider the reserve that would result in an equity value of $1,003 million or $14.05 per share at book value.

I think it's reasonable to assume some losses in the portfolio moving forward though management has shown they are going to move quickly to resolve any issues they find. A tangible reflection of their quickness to act is reflected in their $11 million CECL reversal this quarter. To me, this shows that management is being conservative in their reserves while also being prudent in managing toward successful outcomes.

Reviewing Commercial mREIT Peers: What P/B Multiple Should Be Applied?

From the above, we have a range of estimates regarding potential book value. These estimates assume no growth in the portfolio at all which helps to ensure a measure of conservatism, and as my base case scenario, I use the 25% haircut as a likely outcome given the macro environment. That resulted in the $14.05 per share book value estimate.

But to arrive at a price target that is reasonable, we should consider the multiples that the mREIT universe is trading at currently for a guide. Over the past year, these stocks have seen depressed P/B valuations as rising interest rates caused fears of property value declines and increased credit risk. Here's a comparison amongst 9 mREIT peers.

| Peer |

| P/B |

| Market Capitalization (Millions) |

| Ladder Capital Corp ( LADR ) |

| 0.94 |

| $1,400 |

| Starwood Property Trust ( STWD ) |

| 0.93 |

| $6,000 |

| Ares Commercial Real Estate Corp ( ACRE ) |

| 0.84 |

| $615 |

| Blackstone Mortgage Trust ( BXMT ) |

| 0.82 |

| $3,700 |

| BrightSpire Capital ( BRSP ) |

| 0.69 |

| $939 |

| KKR Real Estate Financial Trust ( KREF ) |

| 0.65 |

| $1,000 |

| TPG RE Finance Trust ( TRTX ) |

| 0.60 |

| $663 |

| Granite Point Mortgage Trust ( GPMT ) |

| 0.32 |

| $310 |

| Acres Commercial Realty Corp ( ACR ) |

| 0.19 |

| $83 |

| Average |

| 0.66 |

| $1,634 |

Source: TD Ameritrade. Data pulled on 2.27.2023.

Here we can see that the average P/B for these companies hasn't changed since January 13th. With TRTX now trading much closer to this peer average, there is less margin of safety here than there was a month ago. If we apply this peer average P/B ratio of 0.66x to our $14.05 estimate, we get a price target of $9.27.

Yet, I think there is undue pressure on commercial mREIT stocks as a whole. In my base case price target, I chose to use the company's 5-year average P/B rating rather than the peer average to reflect this. According to Morningstar, this average has ticked down slightly to 0.76x for TRTX which would yield a price target of $10.68 or 23% higher than current prices.

And, finally, the bull case simply assumed P/B reversion on the current book of 1x over the next 1-2 years. While I believe some losses will be sustained in the portfolio, I think the liquidity of both cash and CLO reinvestable cash can help to grow the portfolio at the same time. The balance between these two, in my opinion, could approximate a stable book value for the next two years while paying out the 11% dividend.

Here's what my updated price targets look like.

| Valuation Method |

| Price |

| Current Price |

| Implied Return |

| Dividend Yield |

| 2-Year Implied Return with Dividend |

| Assume specific CECL reserves, 4 rated loans cut 100% [BEAR CASE] |

| $3.65 |

| $8.67 |

| -57.90% |

| 11.00% |

| -35.90% |

| Assume specific CECL reserves, 4 rated loans cut 50% |

| $10.58 |

| $8.67 |

| 22.03% |

| 11.00% |

| 44.03% |

| Assume specific CECL reserves, 4 rated loans cut 25% |

| $14.05 |

| $8.67 |

| 62.05% |

| 11.00% |

| 84.05% |

| Peer Average P/B 0.66 Reversion with 25% implied cut |

| $9.27 |

| $8.67 |

| 6.92% |

| 11.00% |

| 28.92% |

| 5-year Average P/B 0.76 reversion with 25% cut [BASE CASE] |

| $10.68 |

| $8.67 |

| 23.18% |

| 11.00% |

| 45.18% |

| P/B 1x reversion [BULL CASE] |

| $14.48 |

| $8.67 |

| 67.01% |

| 11.00% |

| 89.01% |

TRTX: Summary and Risks

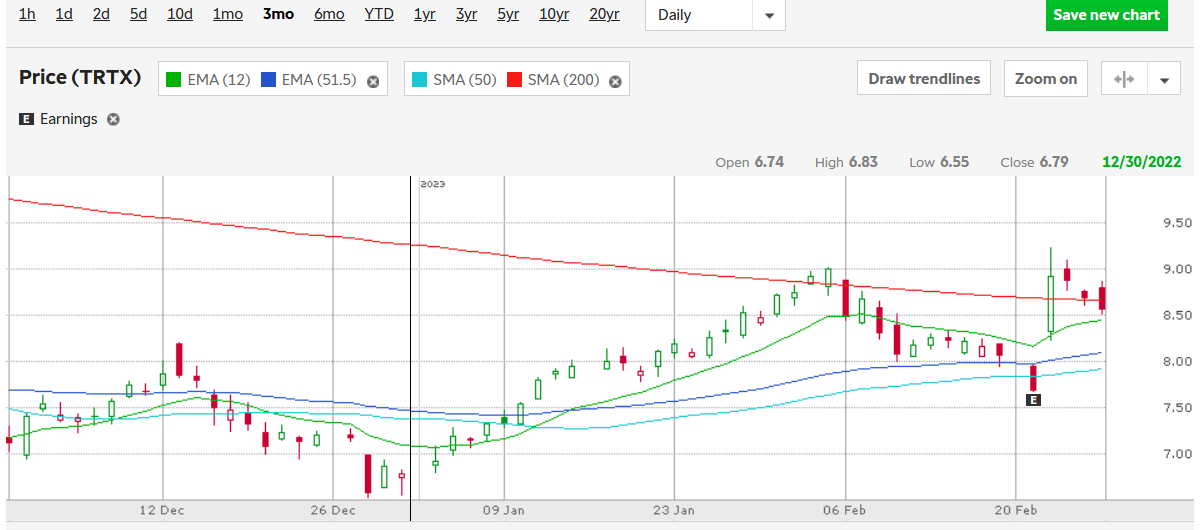

What I've provided above is a recreation of my valuation assessment using the most recent figures from the company. Since I started investigating the company back in December, the stock price has rebounded from the end of year selling lows of around $6.50 to their current levels - a nearly 33% gain in a few months.

TD Ameritrade: 3-month TRTX Chart.

{kind=link}

Recent performance suggested to me that my thesis was intact. The beat on earnings while also recording a reversal on their CECL reflected positive momentum which I think can continue given their sizable liquidity position. It's both a defensive and offensive hoard which represents 11% of their current $5.4 billion portfolio.

While some margin of safety has been squeezed out in this run-up, I still believe that this is a good investment opportunity for the current environment. The portfolio is 100% correlated to rates meaning if they remain elevated or continue to increase, then EPS should benefit as well.

{kind=link}

A lot of these opportunities exist in part due to failures of past management. With Doug Bouquard leading the helm since February 2022, I believe we are witnessing a turnaround of TPG's real estate fund. With the company profitable and I believe unlikely to suffer catastrophic losses through this cycle, over the long term, the market will be forced to more appropriately value this company's portfolio. Meanwhile, the 11% annual dividend alone is a good long-term average return to achieve even if the stock price doesn't move.

As with any stock, there are risks here. These are some of the key ones I'm paying attention to:

- Credit risk is the key one as loans defaulting will decrease earnings and book value. Rising interest rates are generating pressure here as well.

- If interest rates continue to go higher and remain elevated, businesses are going to be pressured which will stress the lenders. We are watching this tightrope dance play out in real time - being mindful of changes in rates will be key to this investment.

- The dividend being cut is always a risk with these types of companies. Even if a dividend cut is conservative and prudent for the company, the market may respond disproportionately. I do not believe a dividend cut is likely, but it is a risk.

- As the REIT is externally managed there is a risk of misalignment of aims here. Management receives a 1.5% on equity value plus performance fees which seemed normal to me.

- The last risk is execution risk. While I believe they are in the midst of a turnaround, they may not be and Doug Bouquard remains to be tested by the passing of years.

For further details see:

TPG RE Finance Trust: 13% Jump In One Week, 11% Dividend, And 23% More Upside