PB - Trading Prosperity Bancshares: Enough Damage Priced In

2023-10-11 14:38:18 ET

Summary

- Prosperity Bancshares, Inc. stock has been crushed.

- The stock is attractively priced relative to book value and offers a 4% plus dividend yield with continued dividend increases.

- Q2 performance showed a decrease in revenues but strong earnings power in a weak macro environment.

- The company is on a merger spree and buying back shares.

We closely follow the operational performance of institutions in the financial sector. We tend to provide a strong review of the key metrics you need to be aware of, but always do your due diligence. Today, we believe that after severe carnage in many of the banks with the erosion in margins due to the relentless march higher in rates, that Prosperity Bancshares, Inc. ( PB ) is a buy. We believe this bank offers sizable upside in the next two to three years as the industry resets itself.

We think you can start to buy now, be paid a healthy dividend to wait, and enjoy future capital appreciation. Successful traders have to have a total disregard for money near-term. You need to be able to stomach buying quality companies when the near-term macro environment is volatile. Volatility is your friend for both trading, and finding long-term investment opportunities.

We believe PB stock represents an opportunity for both, and dividend growth investors should take note of this bank as well. The bank's recently reported earnings show key trends and metrics have softened in this climate. We believe PB stock is a good buy in the $50 range. Let us discuss.

As you can see in the chart, there has been a reset in share prices, particularly here in 2023 as rate hikes ramped up all year and their impacts were felt. We opined numerous times that peak margins had been experienced for banks. Now, banks are adapting to a situation where they are paying more for deposits, but still experiencing decent loan growth and demand, even in a softening economy. We believe a mild recession has been priced in, or is very close. Here is how we would play it.

The play

Target entry 1: $52.85-$53.10 (30% of position)

Target entry 2: $52.00-$52.25 (40% of position)

Target entry 3: $50.75-$51.00 (30% of position)

Stop loss: $45

Target exit: $62

Note: These are the types of trades outlined by our investing group analysts. Often, they come with options considerations. Buy-writes can work here.

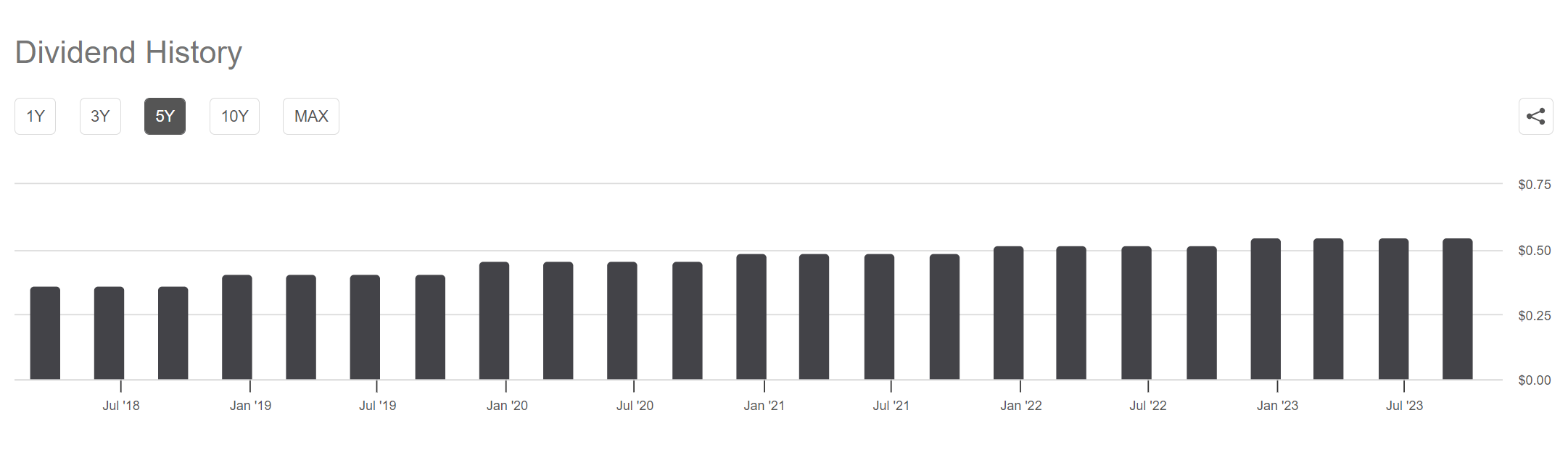

Dividend growth investors take note

Folks, while you can park cash in a money market, or buy bonds to collect yield, you have no opportunity for capital gains, or distribution growth. Here, the bank has been a serial dividend raiser. We like dividend growth stocks in the medium term here, especially those offering a 4% plus yield.

Seeking Alpha PB dividend history

{kind=link}

As you can see, the dividend has been raised every year. We like this, and think that performance of the bank is set to be troughing in the next quarter or two as we see an economic breather taken.

Q2 headline performance

The bank's third quarter report is still weeks out ( expected pre-market October 25th), but Q2 provided a good gauge for where we are going. With Q2 2023 revenues of $276 million, the bank did experience a 3.5% decrease in this metric year-over-year, which was a touch of a surprise as it missed consensus by $7.8 million. Still, this headline revenue miss did not impact earnings power. Net income for Q2 2023 saw a massive increase thanks to the merger. Net income came in at $86.9 million, or $0.94 per share. Backing out some of its merger related expenses, EPS was $1.21. Where are we with book value?

Book value suggests the stock is attractive

We always like to consider the equity price relative to book value. The bank's stock is attractive at $53.30 in our opinion relative to the book value per share reported in Q2. Book value per share $74.35, compared with $74.31 to start the quarter. Thus, it appears we are trading well below book value, with a 28% discount. However, we are trading a bit above tangible book. Tangible book was $37.49. Keep in mind that a premium-to-tangible book is extremely common. Given that we are at a discount-to-book, but a premium-to-tangible book, shares are reasonably priced, especially when we consider where the outlook suggest we are going.

Loans and deposits

Remember, growth in loans and deposits is key for any bank. Loans at the end of Q2 were $21.65 billion, an increase of $3.5 billion or 18% from the year prior. Linked quarter loans also increased $2.3 billion or 12% from Q1 2023. This was a key result. Despite a tough macro situation, loans continue to increase. What about deposits? Deposits were $27.4 billion, an increase of $0.38 billion from the sequential quarter. However, deposits were down from a year ago due to a decline in past quarters from public deposits and some business deposits. However, the increase from Q1 was notable.

Asset quality metrics

In Q2, there was a provision for credit losses of $18.5 million, compared with no provisions in the prior period. These provisions for losses offset earnings power, despite the fact that earnings were strong.

Nonperforming assets totaled $62.7 million or 0.18% of quarterly average interest-earning assets at the end of Q2, compared with $22.2 million or 0.07% of quarterly average interest-earning assets a year ago. The allowance for credit losses for loans was also up. They were $345.2 million or 1.59% of total loans compared to $284.0 million or 1.56% of total loans a year ago. These results were mixed. Much of this has to do with the changing macro situation. However, these numbers are not too dramatic given the assets and loans on hand.

Forward view

We like the fact that the dividend continues to be raised each year. We also like the valuation at these levels, well below book value, but above tangible book. Management bullishly commented that they see "net margin improving in a 12-month time period." This is a strong outlook, but is contingent on rates not dramatically rising from here. The company is also focused on cost controls, but is using capital to repurchase shares. At the start of the year, the company announced a program to buy back up to 5% of the float. The company repurchased 1.21 million shares so far over two quarters. This will boost EPS going forward. The company has also been on a merger spree, first with a recent merger with First Bancshares of Texas, and a pending merger with Lone Star State Bancshares. These mergers will provide more liquidity and increase the loan and customer base. This is bullish for growth.

Given the decline in Prosperity Bancshares, Inc. shares, we think a lot of bad news is priced in, and management's outlook is bullish. We assign a buy rating, and suggest scaling in.

For further details see:

Trading Prosperity Bancshares: Enough Damage Priced In