DKILF - Trane Technologies: Powering A Sustainable And Lucrative Future

2023-09-21 11:51:23 ET

Summary

- Trane’s revenue has grown at a CAGR of 3% during the last decade, although its trajectory has noticeably improved in recent years.

- The business is benefiting from a range of “megatrends”, with climate change, the global sustainability initiative, urbanization, and infrastructure spending (among others) contributing to a significant increase in demand.

- Trane is already a market-leading business but we believe its innovation to improve the sustainability of its products will be a key value driver in the years to come.

- Trane’s margins have improved to a highly attractive level, allowing for strong dividends and buybacks.

- The company is not cheap but at its current valuation, an FCF yield of >5%, and an improved trajectory, we believe there is value here.

Investment thesis

Our current investment thesis is:

- Trane is a pure-play HVAC business that provides investors with strong exposure to the impact of climate change and the wider sustainability trend. The company is benefiting heavily from a number of megatrends, with our belief that growth can consistently increase to HSDs.

- The company’s innovation has been strong, with its focus on sustainability being a game-changer given the carbon emission generated by its industry. The company is positioned to be the go-to choice for infrastructure spending in this segment by those who are seeking to reduce / maintain a low carbon footprint (which should be everyone).

- The business appears expensive but its current NTM FCF yield is already attractive and improved growth will rapidly accelerate shareholder returns given its >30% ROCE.

Company description

Trane Technologies plc ( TT ) is a global climate innovator that provides heating, ventilation, and air conditioning (HVAC) solutions, as well as transport refrigeration systems. Trane is committed to creating more sustainable, efficient, and comfortable environments for homes, buildings, and transportation. The company is headquartered in Swords, Ireland, and operates globally.

Share price

Trane’s share price performance has been exceptional since the company was spun off, gaining over 180% and significantly outperforming the wider market. This has been driven by a continuation of its strong financial trajectory.

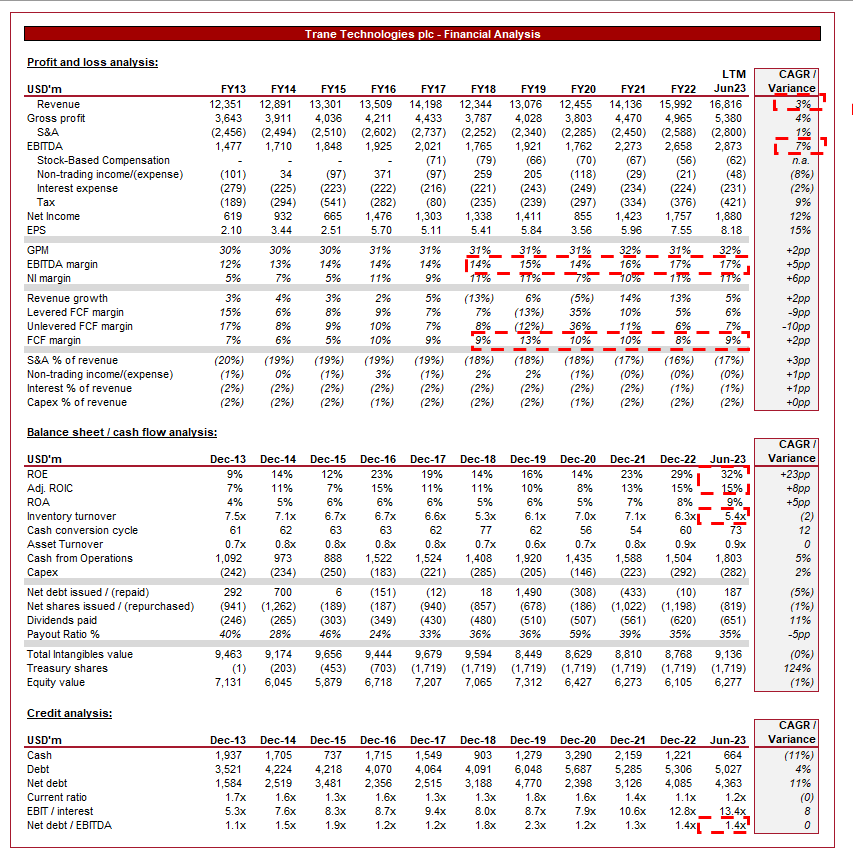

Financial analysis

Trane's financials (Capital IQ)

{kind=link}

Presented above are Trane's financial results.

Revenue & Commercial Factors

Trane’s revenue has grown at a modest 3% CAGR, with broadly consistent gains YoY. The vast majority of this growth has been achieved organically, with product and geographical expansion.

Business Model

Trane is a global leader in providing climate control solutions (HVAC). The company offers a wide range of products and services, such as air conditioners, heat pumps, furnaces, controls, building automation systems, and refrigeration solutions. It serves various sectors, including residential, commercial, industrial, and institutional customers. The company is essentially a pure-play climate control business, with exposure to sustainable technologies and the future direction of energy consumption.

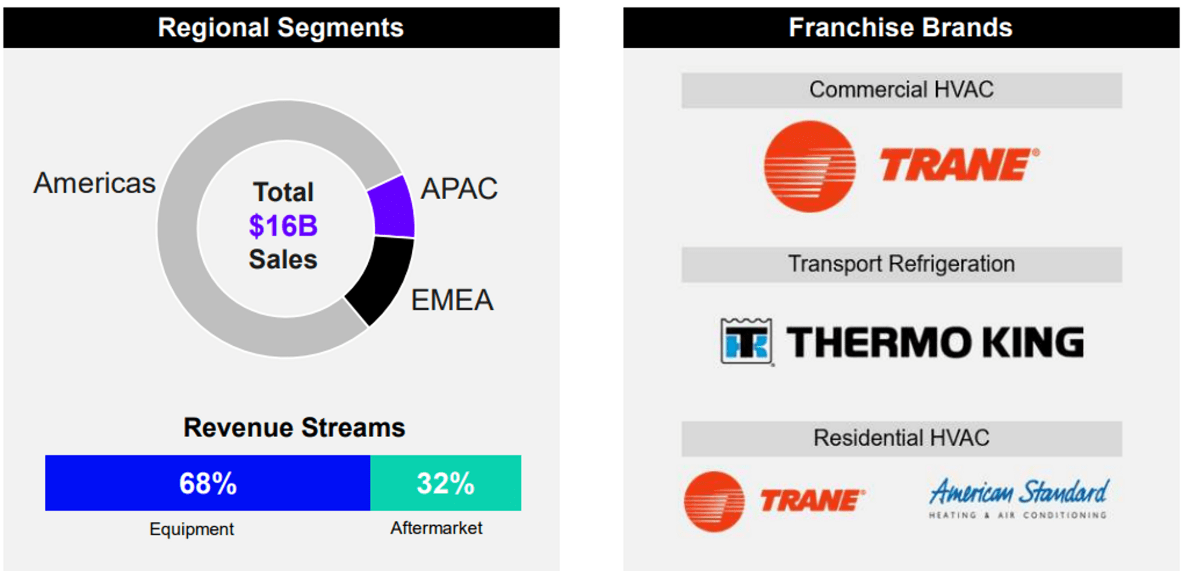

Trane has a global footprint, serving customers in numerous countries. Currently, the majority of its revenue, and core market, is the Americas, followed by EMEA and APAC. This international presence allows it to tap into diverse markets and respond to regional demand variations, while maximizing its returns from product development and industry expertise.

Trane provides comprehensive aftermarket services, including maintenance, repairs, and upgrades. This helps build long-term relationships with customers and generates recurring revenue, which is incredibly important given the cyclical nature of large-scale capital expenditure associated with HVAC. This has allowed Trane to create a smoother upward revenue trajectory, reducing volatility.

{kind=link}

A key criticism of the industry is its energy usage, as HVAC systems contribute a significant amount to global emissions. There is pressure across many industries to reduce their carbon footprint, with pressures slowly creeping toward this industry. Trane differentiates itself through its commitment to sustainability and energy efficiency. Their products and services are designed to reduce energy consumption, lower greenhouse gas emissions, and help customers meet environmental regulations and certifications. The company has yet to reach zero, which is inevitably the end goal but is significantly more environmentally friendly relative to the industry as a whole.

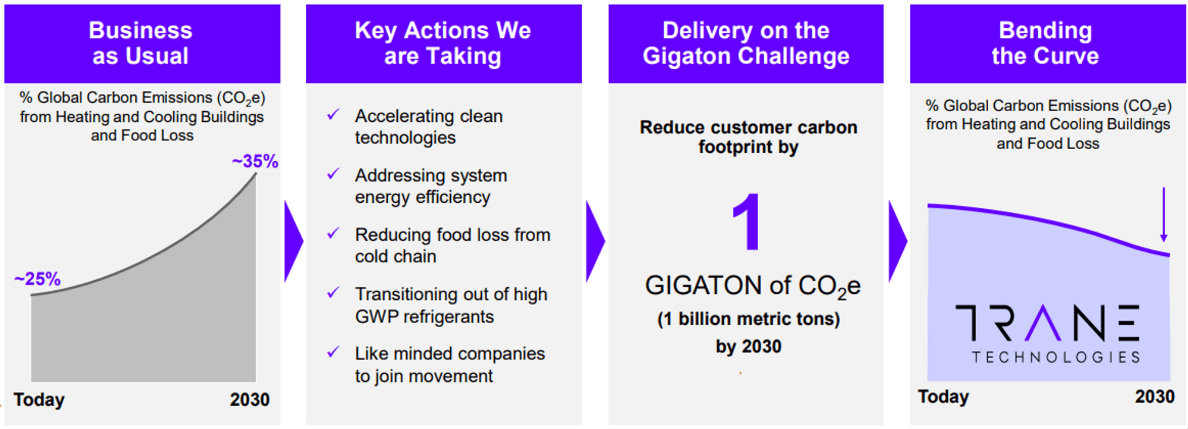

The company has set ambitious sustainability goals, including carbon neutrality and reducing customer carbon emissions by one gigaton by 2030. These commitments align with societal expectations and could significantly enhance its brand among the public and corporates. We believe this will be a major value driver to win clients, in addition to the wider pressures on the industry.

{kind=link}

The company invests heavily in R&D to develop cutting-edge technologies and solutions, much of which is aimed at reducing its carbon footprint currently, as well as other factors such as efficiency, size, and quality. This focus on innovation enables Trane to offer a market-leading offering to the industry. We consider the company’s offering to be compelling, with a future-proof approach due to its focus on sustainability.

As the following illustrates, Trane is well-regarded for its sustainability efforts. It is worth reiterating again that potential customers will see this with extreme positivity, as they themselves are pressured to reduce their carbon footprint, which for many location-based businesses is significantly driven by HVAC systems.

{kind=link}

Management’s current strategy revolves around the following three factors:

- Sustainability innovation - Trane is heavily committed to the Sustainability megatrend, attaching its future growth trajectory to this going forward.

- Exceptional performance - Management is seeking to create leaner processes to improve efficiency and contribute to improved operating cost leverage and margin improvement.

- Structural transformation - Redesigning the company and its product suite to maximize its value within the climate space.

We are extremely positive about how Trane is run by the Management team and their strategy going forward. It is a simple approach but that’s what makes it great. The company is not seeking to set the world on fire but instead do what it does well, exploit megatrends, and operate in an efficient manner through incremental improvements.

Management believes shareholder value will come from the following four factors:

- Secular tailwinds - The HVAC industry is benefiting from a number of megatrends (which we will discuss further next), contributing to a sustained period of outperformance relative to GDP.

- Sustainability-focused innovation - Management believes sustainability will be a critical value driver in the coming years and we concur.

- Margin expansion - Management believes further margin improvement is possible through operational improvements and reinvestment into operational capabilities.

- Financial strength - The company’s strong FCF generation and solid balance sheet will allow for aggressive shareholder returns.

HVAC industry

Trane competes with other leading businesses within the HVAC industry. Key competitors include Johnson Controls ( JCI ), Daikin Industries ( DKILF ), Mitsubishi Electric ( MIELF ), and Lennox International ( LII ), among others.

Increasing regulations and policies aimed at reducing energy consumption and emissions are expected to continue in the coming decade due to climate change. Trane energy-efficient HVAC and refrigeration systems positions the business perfectly to be a market leader in this segment.

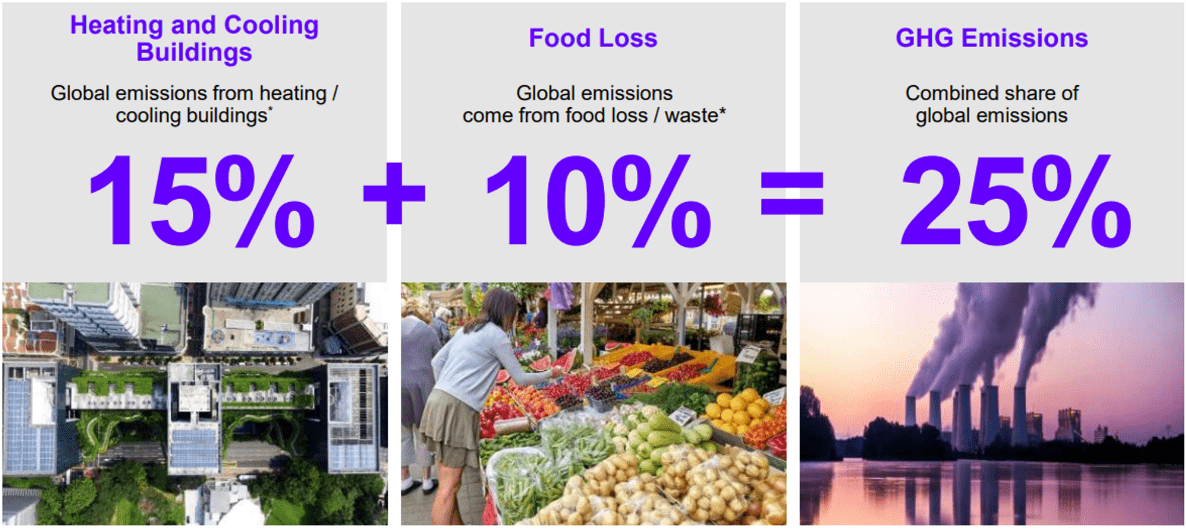

Additionally, global warming and greater weather variability inherently increases the demand for heating and cooling services, contributing to strong demand within the residential segment, as well as continued growth in the commercial and industrial segments. This is why its clean focus works perfectly within the industry, as the business is fighting and benefiting from climate change while minimizing its contribution to it. Management estimates the current contribution to GHG Emissions is a staggering 25%, representing a substantial market it can capture.

{kind=link}

Although this is the biggest “megatrend”, there are a number of other factors that will drive strong demand in the coming years. Such factors include:

- Urbanisation - Increased investment in enhanced infrastructure as Urban locations expand with population inflow.

- Infrastructure spending - The US announced the massive IIJA several years ago, with many other Western nations decades behind in infrastructure spending requirements.

- Resource Scarcity - Contributing to increased demand for sustainable production and output.

- Economic development in developing nations - Growth in demand for HVAC products.

- Indoor environmental quality - Increased utilization of HVAC products to improve indoor quality.

- Digital connectedness - IoT and connectivity of devices between technologies.

These factors will all contribute to varying degrees of enhanced growth, with all factors inherently long-term in nature. When considered in conjunction with the broader Sustainability and Climate change factors, we consider an HSD growth rate to be achievable as a minimum.

In conjunction with these industry growth drivers, we expect Trane to also maintain “the basics”, namely:

- Global Expansion - Expanding into international markets and further growing in markets it operates within will support its growth trajectory.

- Mergers and Acquisitions - Management has conducted M&A where opportunities have been identified. Strategic acquisitions and partnerships will support and expansion of its current portfolio and allow it to expand its expertise. We see this as a key opportunity given the rapid acceleration of technological development in many industries.

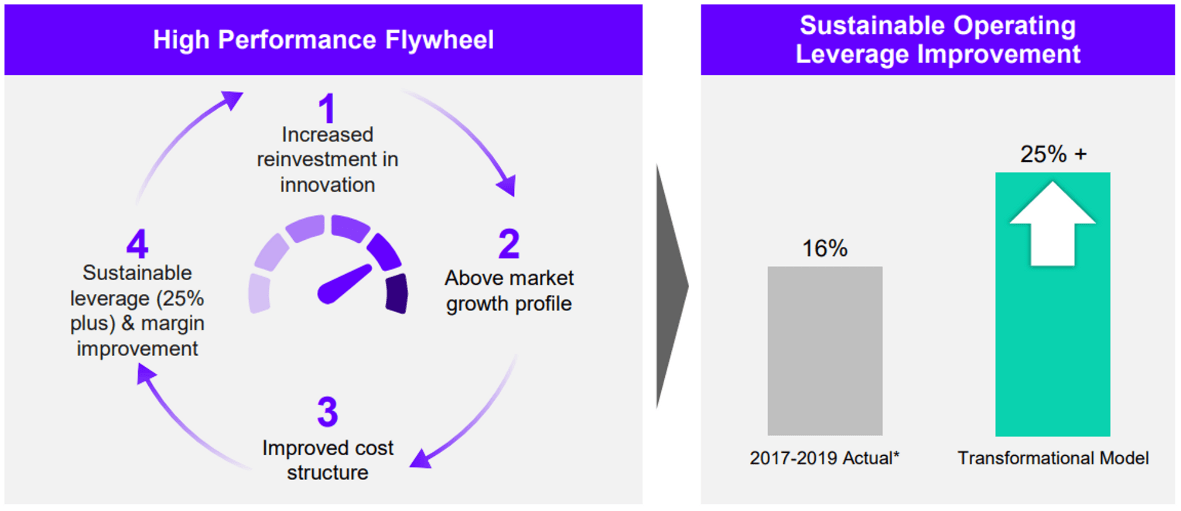

Margins

{kind=link}

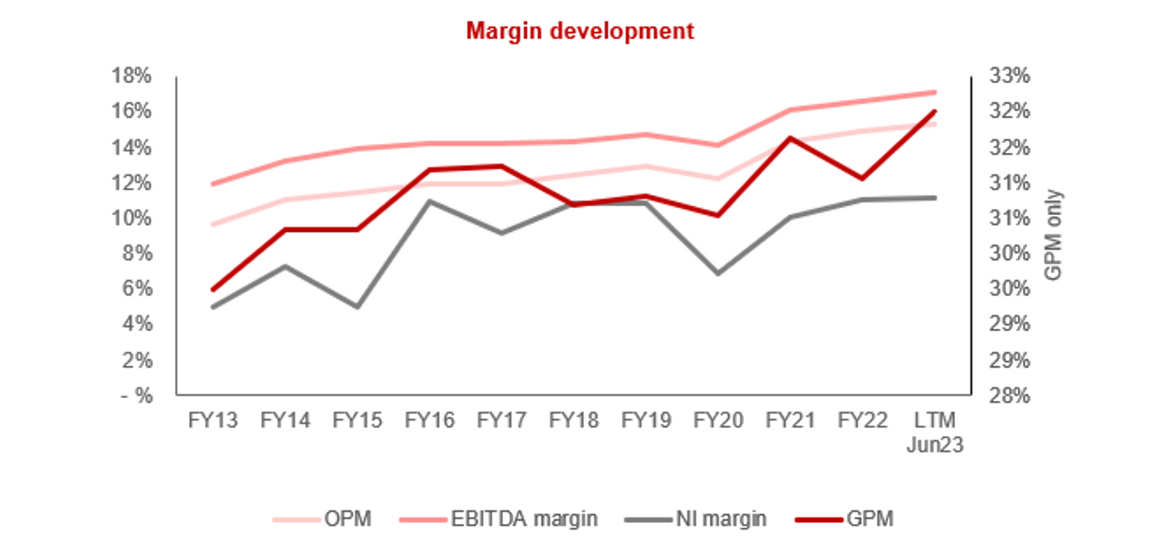

Trane’s margins have impressively improved given the maturity of the industry, with EBTIDA-M increasing from 12% in FY13 to 17% in the LTM period. This has been driven by an operational overhaul by Management, with the belief that further improvements are possible. We are hesitant to suggest this is possible to a material level within a 3-5 year period, although 1-2% is reasonable. Given the level of innovation and its existing market position, we do not see any risks to maintaining its current level.

Operating cost leverage (Trane)

{kind=link}

Q2 results

{kind=link}

{kind=link}

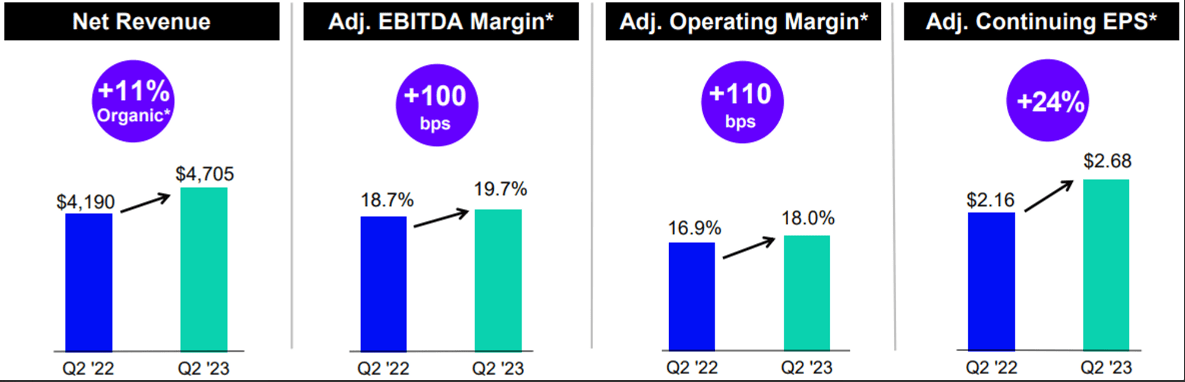

Presented above is Trane's most recent quarterly results.

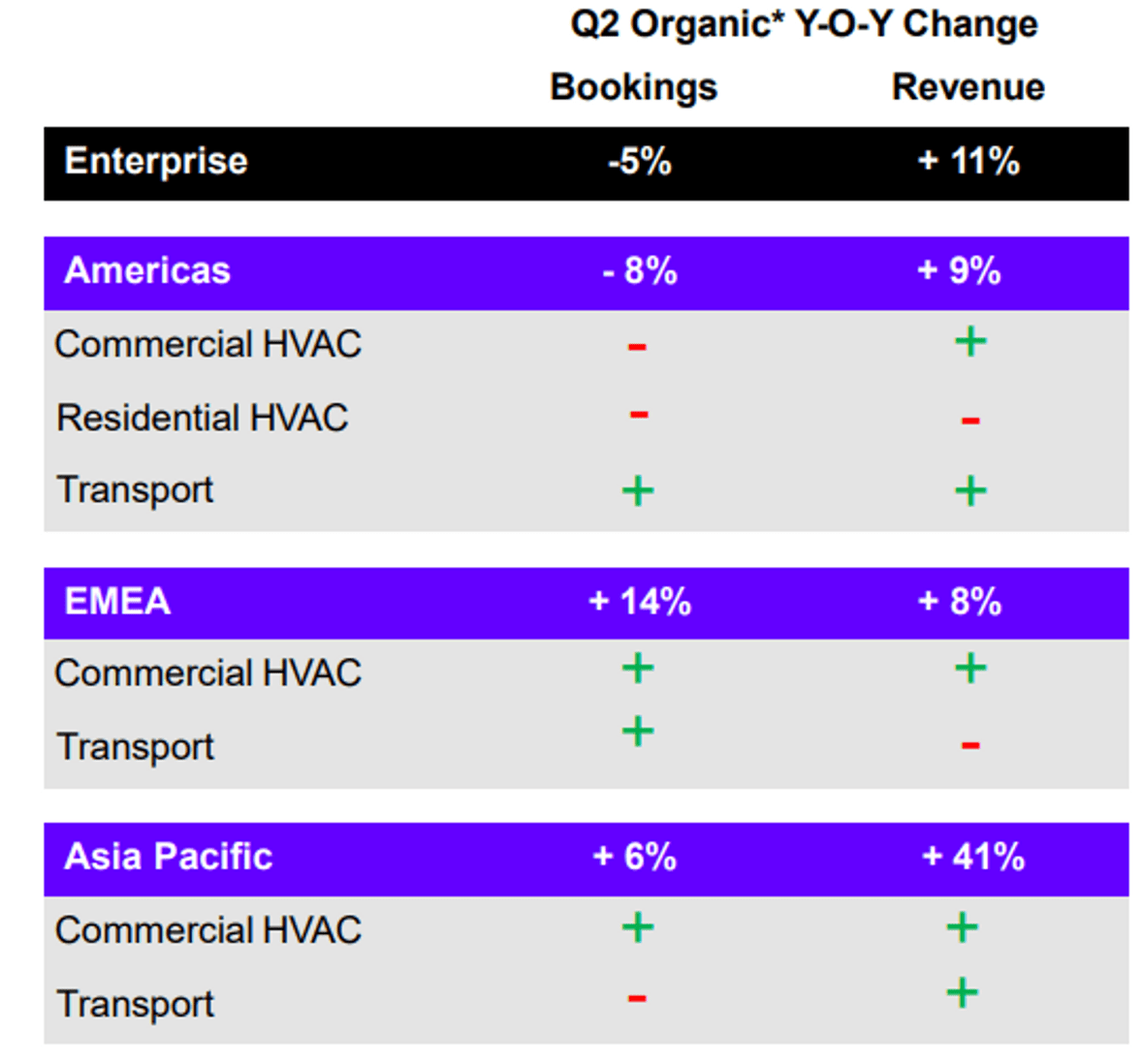

The company has maintained its strong trajectory into Q2, with net revenue growth of +11% and a 1ppt increase in EBITDA-M. This is an impressive performance given the current macro conditions, which we expect to act as a drag on growth as infrastructure investment is discouraged by inflationary pressures and lending costs. This has been driven by impressive growth in APAC, as well as the delivery of healthy bookings across the Americas and EMEA.

While the dip in Americas’ bookings is slightly concerning (-8%), we note backlog is ~3x historical norms, implying an inherently elevated position. With EMEA and APAC continuing to remain strong, with backlog >70% of historical norms, Trane’s current trajectory appears sustainable.

Balance sheet & Cash Flows

Trane’s cash flows are attractive, moving positively in line with EBITDA-M. Further, we see some scope for improvement, as the business has seen inventory turnover fall below its decade average, and noticeably so. This is potentially a reflection of slowing demand (at least relative to Management’s expectation), although this should be monitored further to see ascertain if this is a sustained trend given growth is currently very strong.

Due to the strong cash flows, the use of debt has been limited, allowing the business to commit cash flows to distributions. The business has aggressively repurchased shares, with excess cash returned to shareholders, alongside dividend payments that have grown at an impressive 11% CAGR. Given cash has fallen below its decade average relative to revenue, we believe a slowdown in buybacks is inevitable, although dividend growth should continue.

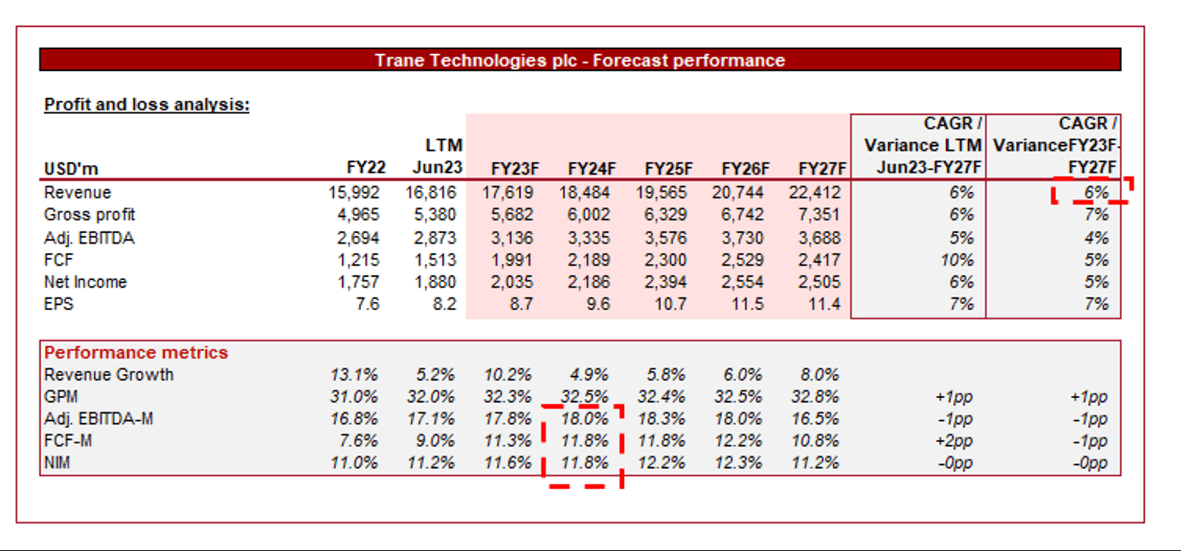

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting revenue growth of 6% into FY27F, with margins remaining broadly flat. This appears reasonable in our view, with the scope for improved growth in the coming years based on our analysis above. In conjunction with this, the growth rate achieved post-FY17 has been noticeably higher, suggesting there is a recent track record of delivering an improved rate.

Margin improvement is always difficult to achieve without a significant moat or transformational operational exercise (which has already been completed), with operational improvements usually offset by defensive actions to protect its competitive position. For this reason, we believe an EBITDA-M of 16-18% is realistic in the next 5 years, although at the top-end, Trane could achieve an improvement of 1-2% (at an EBITDA-M level).

Industry analysis

Building Products Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of Trane's growth and profitability to the average of its industry, as defined by Seeking Alpha (35 companies).

Trane performs well relative to its peers, although not necessarily to the level one would expect given the quality business model. Trane’s revenue growth has lagged the wider market, at both a 3Y and 5Y basis, reflecting a degree of market maturity and poor strategic efforts to grow the business further. Although it has yet to be suggested given how bullish we are of the business model, it could be argued greater reinvestment in the business is required. This could either be R&D or M&A based on what is expected to generate the best ROI.

Margins are the company’s area of strength, yet the business underwhelms (compared to our high expectations). Its EBITDA-M is slightly below the industry average, as is its FCF. The only noticeable positive is Trane’s ROE, which is comfortably higher, owing to strong buybacks alongside its dividend payments.

Valuation

{kind=link}

Trane is currently trading at 18x LTM EBITDA and 15x NTM EBITDA. This is a premium to its historical average.

A premium to the company’s historical average appears reasonable in our view, primarily due to the various industry megatrends that Trane is expected to further benefit from. Additionally, we believe its focus on sustainability is the correct approach, which will yield outsized growth in its core markets.

Further, the company is trading at a 20-30% premium to its peers on an LTM EBITDA, NTM PE, and NTM FCF basis. Again, we believe this is justifiable as within the next 5 years, we see Trane’s growth rate increasing above or in line with the industry’s 5Y average (8.8%), while its EBITDA-M will again reach the average, if not exceed. Given the megatrends, we believe Trane’s improvements will outstrip that of the peer group, while its strong ROE will mean outsized shareholder returns.

At a NTM FCF yield of 5.4% (lower than its historical average), the stock is not cheap, and means a degree of the upward trajectory is already priced in. This said, we still think there is some value here at the current price.

Key risks with our thesis

The risks to our current thesis are:

- Interest rates - The extent to which rates remain elevated has the potential to slow the company’s near-term trajectory, due to reduced spending with financing costs heightened.

- Reduced distributions - Although it should be priced in, investors may respond negatively to reduced distributions in the near term following the decline in cash balance.

- Innovation - With increased innovation and technological development, there is a heightened risk that peers leap ahead of Trane through the creation of new products. As a pure-play business, we expect this risk to be minimized.

Final thoughts

Trane is a fantastic business in our view. The company has grown well in recent years, with megatrends expected to maintain Trane’s heightened trajectory for an extended period of time. underpinning the improved demand is operational and commercial excellence, with quality product development and a focus on margin improvement. We particularly like the focus on sustainable products, which we believe will be a critical value driver in the years to come.

Although Trane is not cheap, we believe its improved trajectory will allow for greater returns in the years to come.

For further details see:

Trane Technologies: Powering A Sustainable And Lucrative Future