TAC - TransAlta: A Major Player A Good Buy At Below $10.5/Share

2023-12-13 11:45:50 ET

Summary

- TransAlta is a utility company that has been undervalued and has not delivered a high dividend yield.

- The company has a solid market cap and generates significant free cash flow.

- TransAlta has plans for significant growth in clean electricity generation and has several high-value projects in the pipeline.

Author's Note: All amounts are in Canadian Currency unless specified

Dear readers/followers,

In this article, I'll initiate coverage on the currently undervalued - as I see it - utility TransAlta (TAC). This is a company that for years has been lauded and called "undervalued" by many, only to then defy these assumptions and guidance by dropping further. My positions in utilities like Enel (ENLAY) are up this year, as well as delivering significant overall dividends.

TAC is not up - nor is it delivering a "great" dividend, at the current 2% yield. The company trades both on the NYSE and the TSX, and in this article, I'll go through it as a potential long-term investment.

It should be mentioned that while the company is not a great yielder, it's actually a good dividend grower - the last bump was less than 3 weeks ago and came at a 9.1% rate.

So, let's see what TransAlta offers us and what can be expected for the longer term here.

TransAlta Corporation - Double-digit negative returns for 2023 so far

The company is, as implied above, down more than 10% this year so far. This should not necessarily be considered reflective of the company's fundamentals, because these are more solid than you might expect.

This is a business with a $3.5B market cap and a $8.7B EV with 1,280 employees. The company is also one of the oldest utilities in all of Canada with a 6,400 MW portfolio with diversified generating facilities not only in Canada but in the US and Australia as well.

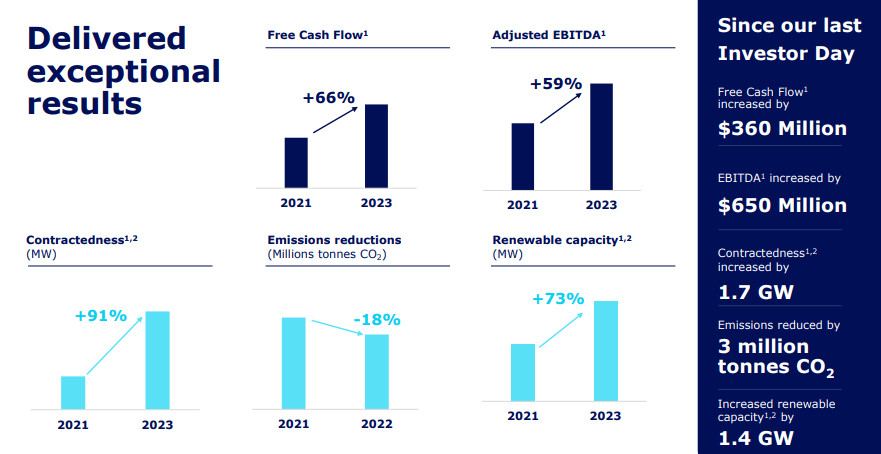

This is also a company that generates upwards of $900M of FCF, despite what you're currently seeing in the company's quarterly trends. TransAlta alone is also responsible for over 30M tonnes of emission reductions since 2005, which is a full 10% of Canada's target.

You can see, therefore, that the company is a clean energy business with a focus on generational assets in Hydro, Solar/Wind, and Gas, as well as businesses in Energy marketing and pipeline and developments.

Since 2021, this company has made large leaps of improvements. TAC has installed 800 MW of wind and solar, and another 2,700 MW in the development pipeline. The same amount, 800 MW, of thermal generation has been retired in the same time. Also, this has been done during a time when the company has not seen lower or worse earnings, but better results.

{kind=link}

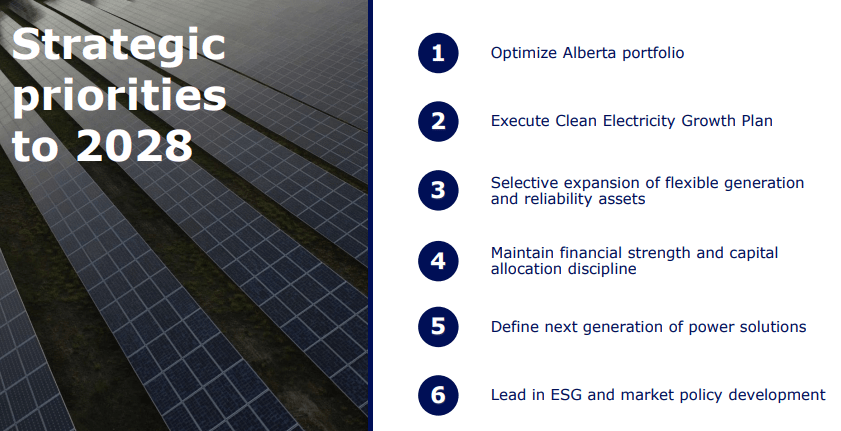

According to TAC, the company has large opportunities in the transition to electrification. Decarbonization is moving forward, and this requires significant investment from market-leading players in order to be met.

To this end, the company has the following priorities until the 2028E fiscal.

{kind=link}

This plan involves another 10,000 MW of clean electricity from $3.5B of growth CapEx that'll add $350M to the company's annual EBITDA, which would put the company at above $1B per year. The focus here will be onshore wind, solar, storage, and hybrid solutions, and optimizing the legacy Alberta mix to maximize company cash flow.

In fact the company already expects to hit that billion in adjusted EBITDA for the next fiscal, at a guidance of $1.15B and $1.3Bn and another $450-$600M worth of FCF.

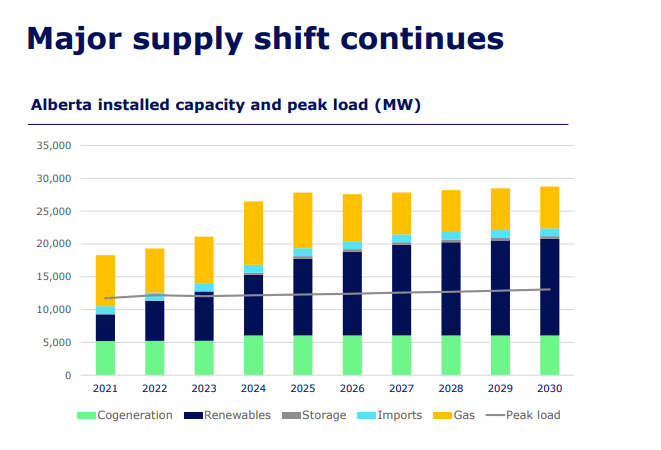

However, the company has recently paused the development of renewables in Alberta, in response to land use, system reliability, and reclamation concerns, expected to be in place at least until February to ensure that enough time is given for regulatory reviews. There is a significant shift expected in Alberta specifically that will massively reduce the gas mix in the company's generation. Take a look.

{kind=link}

The main challenge for the company is the expected price on a per-MWh basis. Supply trends are expected to soften this price in the next 2-3 years before it climbs back up to around the 2021-2023 level at the end of this decade. Of course, aside from the cost challenges, the company also needs to navigate the challenges in output that wind and solar bring to the table - these forms of generation are susceptible to hour-to-hour changes that need to be considered - and this is challenging the reliability of the system, which is also the reason for the current regulatory pause.

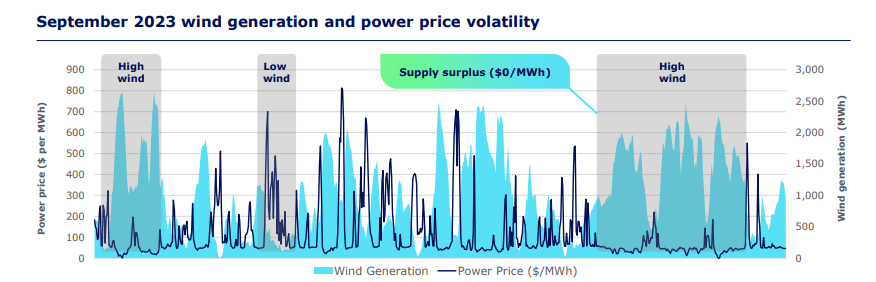

Wind especially will increase the volatility in price - this has been proven over time.

{kind=link}

This means TAC is positioning itself with a high diversification of assets, both in Wind, Hydro, Storage, Gas, and other sectors. Thermal gas especially is a required "compensator" when renewable resources are on the low side.

The company applies a comprehensive hedging strategy, with most of the production for 2024 already hedged in terms of pricing, and over half of the 2025E already hedged as well.

3Q23 is the latest set of operational results we have to consider here. Those were positive, with significant $450M+ EBITDA on an adjusted basis, and over $ 225M worth of FCF with availability of almost 92% for the grid. TAC also continues to have access to just south of $2B worth of liquidity.

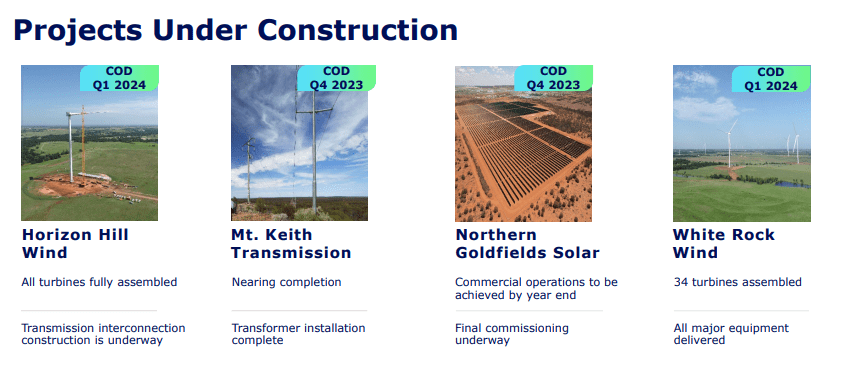

The company has several high-value projects in the pipeline.

{kind=link}

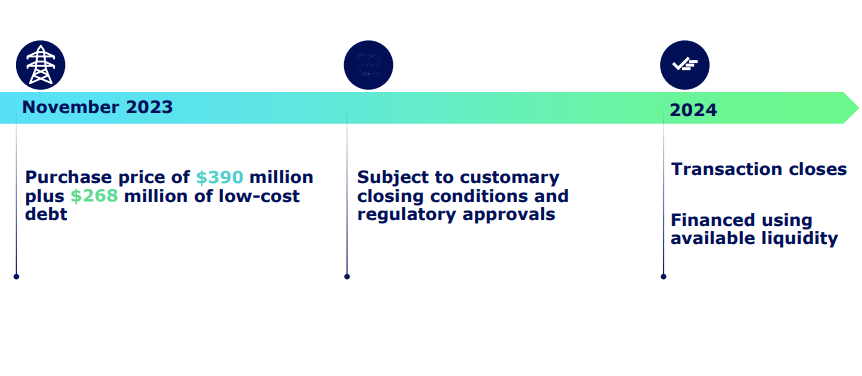

The current development pipeline calls for bringing a total target of 5,000 MW by 2025E. The company is currently in fact on track to beat this target. There are some news on the M&A front, with the Heartland transaction at a 5.5x Multiple with a very attractive EBITDA contribution on an annual basis, but more importantly, this transaction adds flexible capacity to the company's portfolio with a 55% share of contracted revenue.

{kind=link}

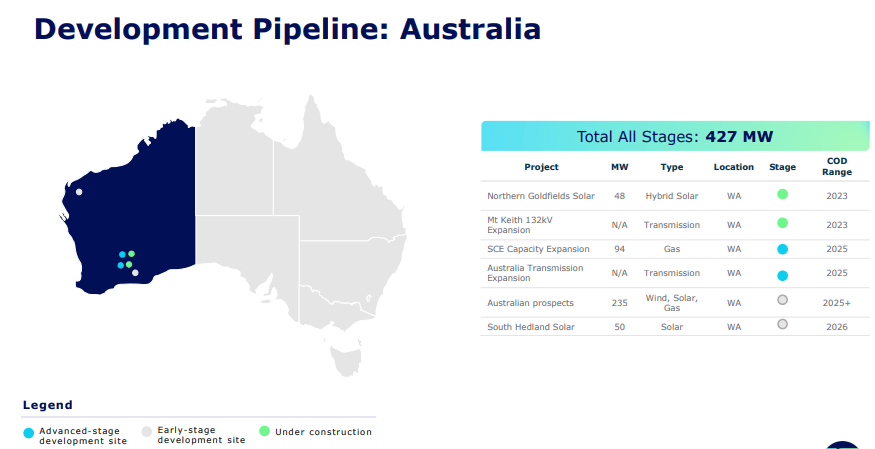

The company isn't just developing in the US either, but has significant developments in the US, with projects all the way until 2027 and beyond. In Canada, the company's main focal point is obviously Alberta, the company's core, and in Australia, the company's focus is on the western part of the country.

{kind=link}

Going forward, I expect TAC to continue to be able to grow and execute on its projects, and I don't see any operational issues that would be cause for significantly elevated risks that are not already mentioned.

Let's clarify this in the Risk & Upsides to the company.

Risks & Upside

The main risk that I see to TA/TAC in the next few years is the combination of pricing and generation uncertainity as the company switches to a far more volatile overall mix. Maintaining flexible percentages of assets can only do so much when, as you can see in the pictures above, some of the fundamental ups and downs in entire generations are dependent on very clear trends - meaning either wind or sunshine. This is not just a risk to TA/TAC but to all companies active in this industry.

In addition to this, fundamental risks to the company do exist, albeit minor (as I see it). The company is not IG-rated, but only BB+, and has a long-term debt/cap of almost 61%, which is somewhat elevated here. Those are really the two main risks.

The upside to the company is very solid return and profitability metrics. The downside is sub-par debt and leverage metrics, with an interest coverage of less than 4x (though this is actually good compared to where TAC has been historically).

Valuation

To state this very clearly, I believe the company is going into several years of relatively negative operational trends, meaning earnings. I believe earnings will actually be declining for as long as we see lower prices on a MWh basis, and I believe the signs are clear that this is going to be happening in the next few years, at least until 2025E-2026E.

Why is this the case in Canada specifically?

Because there's plenty of competition coming to the markets, and there are few changes considered. RRO will be declining in both 2024-2025E and current expectations are for these prices to normalize to the levels seen during 2020 - if not exactly at those cheap levels.

I'd be careful estimating the company at any sort of massive upside in the near term. The analysts following TransAlta have been expecting the company to achieve $15-$17/share for the Canadian ticker for over a year- the company has in fact gone in the opposite direction. S&P Global targets for the company and the main TSX ticker range from $12/share to $18/share with an average of $15. However, despite the fact that every single target by every single analyst is at least $1.2/share higher than the current share price, only 2 analysts out of 9 currently consider this business to be a "BUY". This is weak conviction, or at least a lot of uncertainity on the operational side.

I would say, generally speaking, you're better off investing in the company's preference shares and debt instruments. The reason is the operational uncertainity that will play into the common share valuations for the foreseeable future. Many of these prefs are yielding between 4.5-6% at this time, making them decent options if you're looking at income investments, especially if you consider the resets that are in effect for some of them.

I don't see specific individual advantages due to its operational diversification, given that geographic diversification also increases the costs of compliance, FX and other things.

Because of these factors, I currently consider the company to be a conservative "HOLD", but close to a potential entry point where the minimum price of $12/share would mean a double-digit annual RoR.

Here is my introductory thesis for this company.

Thesis

- TransAlta is one of the leading renewable players in Canada, with a strong generation profile with both Canadian, Australian, and American exposure. Its mix is well-prepared for the challenges that are likely to come in the longer term, and I expect this company's upside and fundamentals to develop positively over the long term.

- Short-term, I expect pressure from lower RRO and power prices in Canada which currently seem likely to bottom within the next 2-3 years. While I believe that the company offers an appealing entry point at a cheap price - including this one - there is a multitude of risk factors that still make this one a bit of a doubt for me.

- I'd say I want to enter the company below $10.5/share to be safe, and this makes the company a "HOLD" here. The company has a strong history of premiumization in terms of price targets, and it has never reached the heights expected - not for the past few years at least.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

TransAlta: A Major Player, A Good Buy At Below $10.5/Share