TA:CC - TransAlta: Earnings Beat And Still Too Cheap

2023-05-11 06:37:26 ET

Summary

- TransAlta dealt the market a big surprise when its Q1 2023 revenue came in 72% above expectation. The analyst community wasn't even in the right ballpark on the FFO.

- TAC has entered into a share purchase program to purchase 14,000,000 shares (5.2% of outstanding shares) which should narrow the discount to fair value.

- TAC's multiple is nearly half the valuation of its peers despite its lower leverage. I see as much as a 150% upside.

All figures in CAD as that is the company's reporting currency unless otherwise noted.

Introduction

I have written articles on both TransAlta Corporation ( TAC ) (TA:CA) and its publicly traded renewables segment TransAlta Renewables ((RNW)) of which it owns 60%. Most recently I wrote on TA in TransAlta: Among The Best Value Plays In The Conventional And Renewable Power Space where I completed a sum of the parts valuation analysis and found it to be at least 51% undervalued from the then price of $12.60/share.

Since this analysis took place in November of 2022, TA has pretty well tracked the iShares S&P/TSX Capped Utilities ( XUT:CA ) while RNW has colossally underperformed even when including its monster monthly dividend payment of 0.078/share and 7%+ dividend yield.

Despite the underperformance of these two investment opportunities, TA dealt the market a big surprise when it released in Q1 2023 earnings. Its Q1 2023 Revenue came in 72% above expectations and the analyst community wasn't even in the right ball park on the FFO expecting $0.21/share when it came in at $0.99/share.

Latest Quarter Earnings (Seeking Alpha)

The earnings beat helped the share price over the past week by 4%. Management has also raised guidance for TA for 2023 versus what was suggested at 2022 YE as I will discuss shortly giving greater credence to my ~$19/share target.

Q1 2023 Results and Outlook

{kind=link}

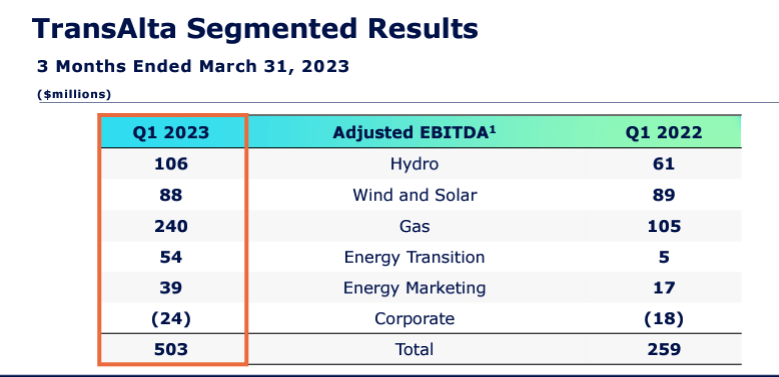

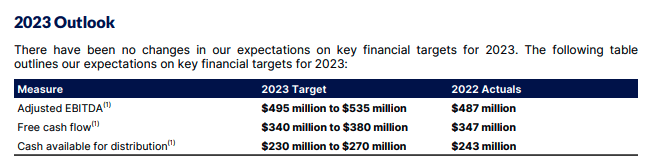

As we can see below profitability was up in all segments aside from the slightly woeful wind and solar segment. To be fair, management did not provide guidance on improved growth in this segment with adjusted EBITDA in the range of $495 million to $535 million as revenues should increase in the back half of the year as rehabilitation of the Kent Hills 1 and 2 wind facilities is underway and all turbines will return to full service.

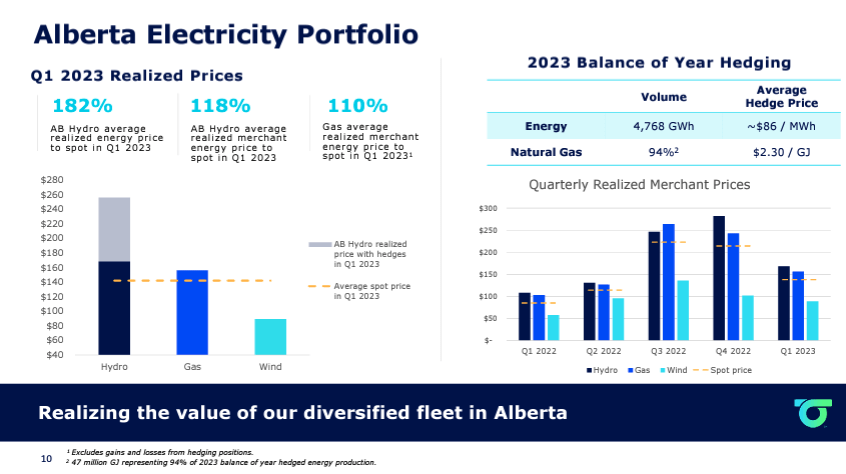

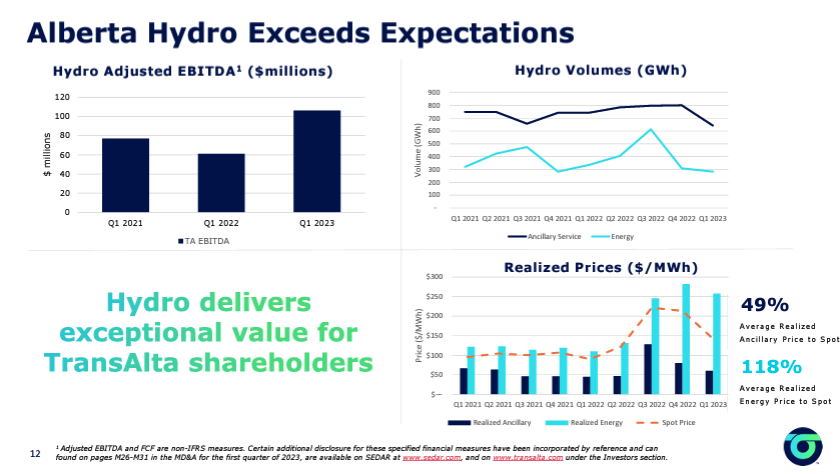

Everything else performed in spades. Revenues for the three months ended increased $354 Million compared to the same period in 2022, due to combination of increased production (up 11%), higher realized energy prices within the Alberta electricity market (up 182%), higher services prices in the Hydro segment (up 118%) and higher gas prices in the merchant market (up 110%).

Q1 2023 Results (TransAlta) Q1 2023 Results (TransAlta)

{kind=link}

{kind=link}

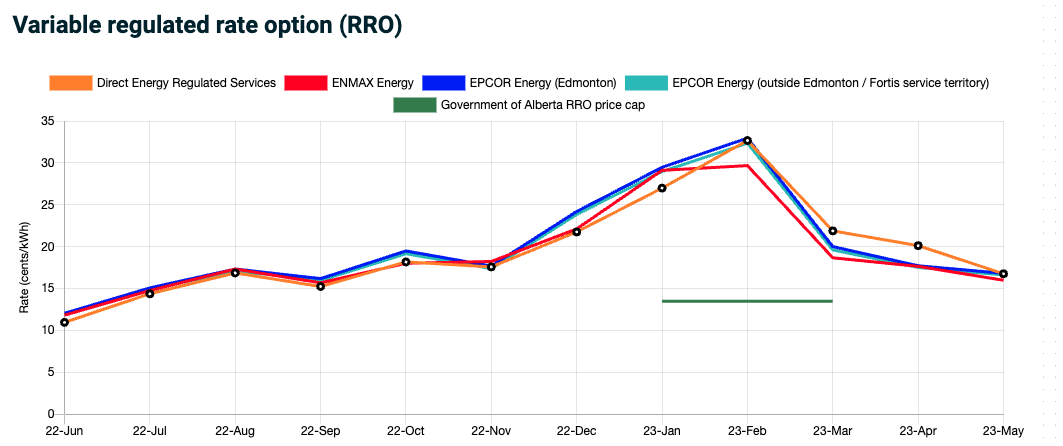

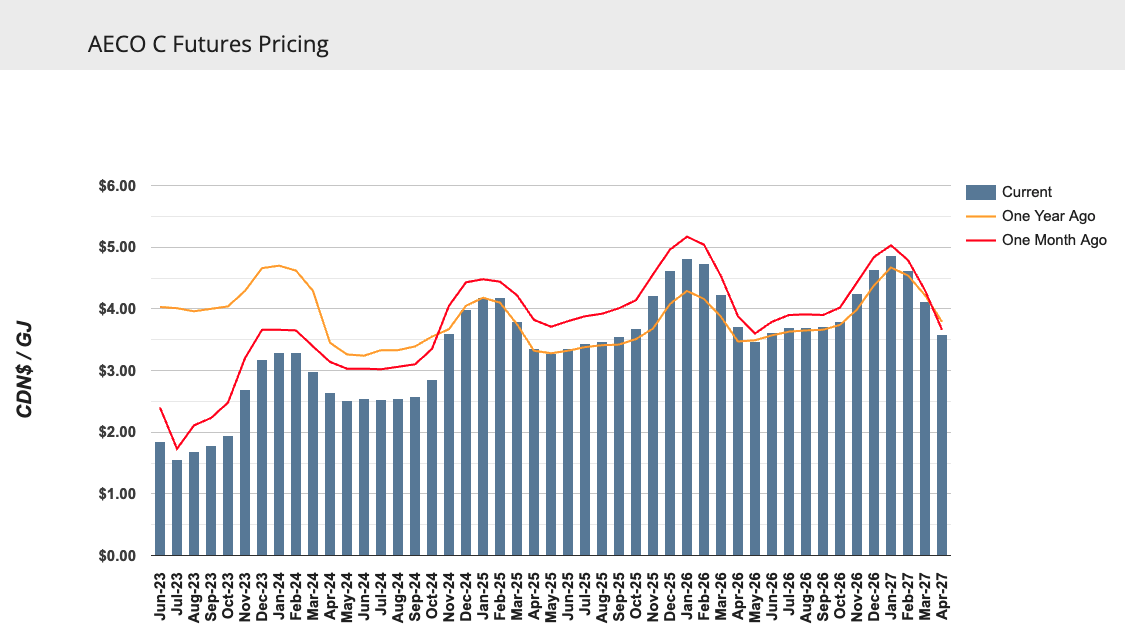

For fiscal 2023 TA has hedged ~79% of its production. Alberta power prices reached highs of over $190/MWH in February 2023 so has locked in very high price. Prices have begun to soften since March however. TA does also hedge their natural gas exposure (94%) for which they are exposed in a negative way as it increases fuel and purchase power costs and unfortunately realized increased costs of $87 Million from Q1 2022. This cost should reduce in the remainder of the fiscal year as a result of weakened natural gas pricing. April pricing is down to $3.00/GJ from over $5.00/GJ for much of 2022. TA has locked in prices as low as $2.60/GJ on their hedges.

Variable regulated rate option (RRO) (Alberta Utilities Commission) AECO Futures Pricing (Gas Alberta)

{kind=link}

{kind=link}

Management has been able to increase their EBITDA and FCF guidance primarily due to locking in strong energy prices over the coming year. Estimates are likely conservative as 2022 FYE results were better than management had originally forecast mid-year in 2022 and energy prices are even higher than last year combined with lower natural gas prices. It would not be a surprise to see profitability reach the same levels as 2022.

Q1 2023 Results (TransAlta) Q1 2023 Results (TransAlta)

{kind=link}

Even if FCF comes in at the lower end of guidance, TA would still trade at an attractive FCF yield of 18% at its current market capitalization. TA has been slow to repurchase shares with its excess free cash flow and is not too generous with its dividend but this doesn't mean shareholder returns won't come. Although the share count has only reduced from 280 Million to 268 Million since 2020, TA has purchased a total of 3,169,300 common shares at an average price of $11.23 per common share in 2023, for a total cost of $36 million which represents 1% of their market capitalization.

In March 2023 TA entered into an automatic share purchase plan to purchase up to 14,000,000 common shares over the next 12 months, representing approximately 5.2 per cent of the Company's currently issued and outstanding common shares. Even at $650 Million in FCF, this would leave $468 Million for debt repayment or dividend increases. TA is only moderately leveraged anyway at 1.81x Net Debt/Forward EBITDA.

Valuation

RNW may appeal more to the dividend oriented investors given its much higher yield but is certainly not set up to beat the parent company from a total return perspective when looking at its valuation relative to TA.

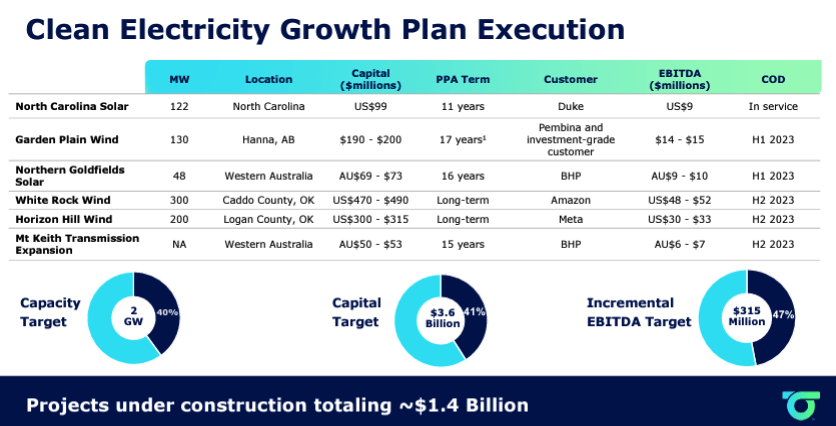

RNW has a number of projects that are expected to come online in 2023 which will add at least $80 Million in annual EBITDA. Management believes the projects will add $315 Million in incremental EBITDA at full capacity. The largest projects include the White Rock and Horizon Hill Winds projects. However, management has guided for relatively flat results for 2023 and the payout ratio of dividends to CAFD in 2022 was 103 per cent so this doesn't provide confidence in the sustainability of the dividend in the near term. Dividends are primarily going to TAC, so would not impact the consolidated tangible book value.

Q1 2023 Results (TransAlta) Q1 2023 Results (TransAlta Renewables)

{kind=link}

{kind=link}

The current market capitalization of the two is almost identical so you are getting TA that has been a free cash flow machine versus RNW that is trying to manage its payout ratio for the same price. You are also able to buy exposure to RNW at a discounted valuation by buying shares of TA as well.

My previous article showed a sum of the parts valuation of TA where it was determined fair value was $19/share indicating TA is 42% undervalued from its current price of $13.30/share. When compared to other Canadian utility companies, its valuation pales in comparison, which is surprising given its lower leverage. It's surprising Algonquin Power & Utilities ( AQN ) is so much higher considering their recent dividend cut as well. Assuming even a 10x EV to EBITDA valuation is fair, would indicate up to 150% upside for TA.

Although TA is the better buy over RNW, RNW is still cheaper than its renewable peers so you get the renewable assets at a discount on top of a discount when you buy through TA.

Conclusion

Overall I maintain the same buy thesis as I previously did. TA is badly undervalued, but through its aggressive buyback program that will be funded through its excess free cash flows it should be able to narrow the discount.

Alternatively, the Brookfield entities could help unlock value. Brookfield Renewable Partners (BEP) has shown an interest in the renewable assets of RNW and its parent companies Brookfield Corporation ( BN ) and Brookfield Asset Management ( BAM ) already own a minority stake in TA. BAM and its affiliates could partially finance a takeover based on their higher multiples and could realize synergies through corporate overhead.

For further details see:

TransAlta: Earnings Beat And Still Too Cheap