TRNS - Transcat: Might Be The Right Time To Exit

2023-11-05 12:37:16 ET

Summary

- TRNS recently announced Q2 FY24 revenue growth of 11.2%, driven by strong demand in the life science market and acquisitions.

- Technical analysis suggests a bearish trend for TRNS, with a potential downside of 19% from the current level.

- Insider selling, decreased institutional holdings, and high valuation indicate it is time to sell TRNS.

The last time I wrote about (TRNS), I mentioned that it is overvalued, and even though it is experiencing growth, it doesn’t justify its high valuation, and recently the stock has started to correct. I still stand by my stance, but this time, I think it is time to exit the stock as there are many alarming things that I will discuss in this report. I now change my rating to a sell from a hold.

Financial Analysis

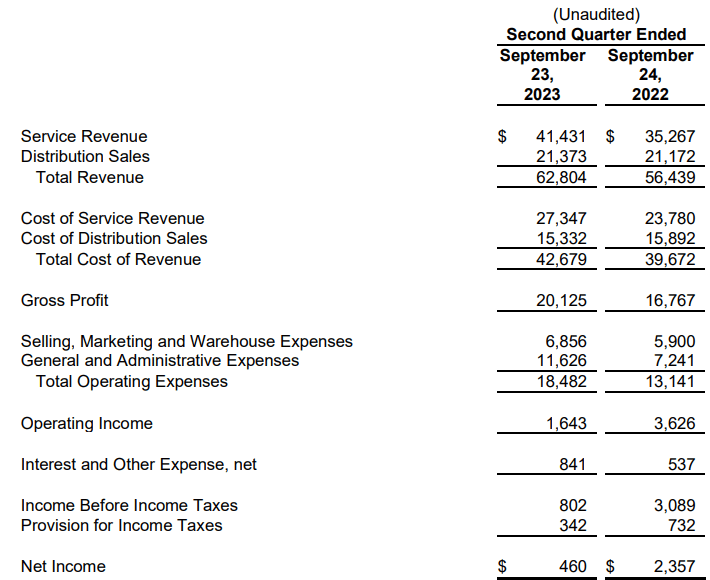

TRNS recently announced its Q2 FY24 results . The revenue for Q2 FY24 was $62.8 million, a rise of 11.2% compared to Q2 FY23. A strong growth in its service segment, which mainly happened due to strong demand in the life science market, was the major reason behind the company’s revenue growth. The revenue from the service segment grew by 17% in Q2 FY24 compared to Q2 FY23, and other than the growth in the service segment, its acquisitions also boosted its revenue growth. The acquisitions contributed 7% of the revenue growth in the service segment. The gross profit margin for Q2 FY24 was 32%, which was 29.7% in Q2 FY23. The margin improvement was mainly due to better execution of betterment initiatives like automation, and the other reason was an increased mix that included higher margin rental sales.

{kind=link}

The company suffered a one-time non-cash charge. So, if we ignore the charge of $2.8 million, its net income increased by 39% in Q2 FY24 compared to Q2 FY23. Expanding its business through acquisitions is one of the major strategies of the company, and acquisitions like SteriQual complemented its services segment by boosting its sales growth and also benefitted the margins. They completed one more acquisition in Q2 FY24 named Axiom Test Equipment. The purpose of this acquisition is to broaden their rental service. Axiom is an electronic test equipment provider that serves across the U.S. The rental service is a high-margin and growing business. So if the integration of the acquisition is successful, then it will not only boost the sales, it will also improve the margins.

Technical Analysis

{kind=link}

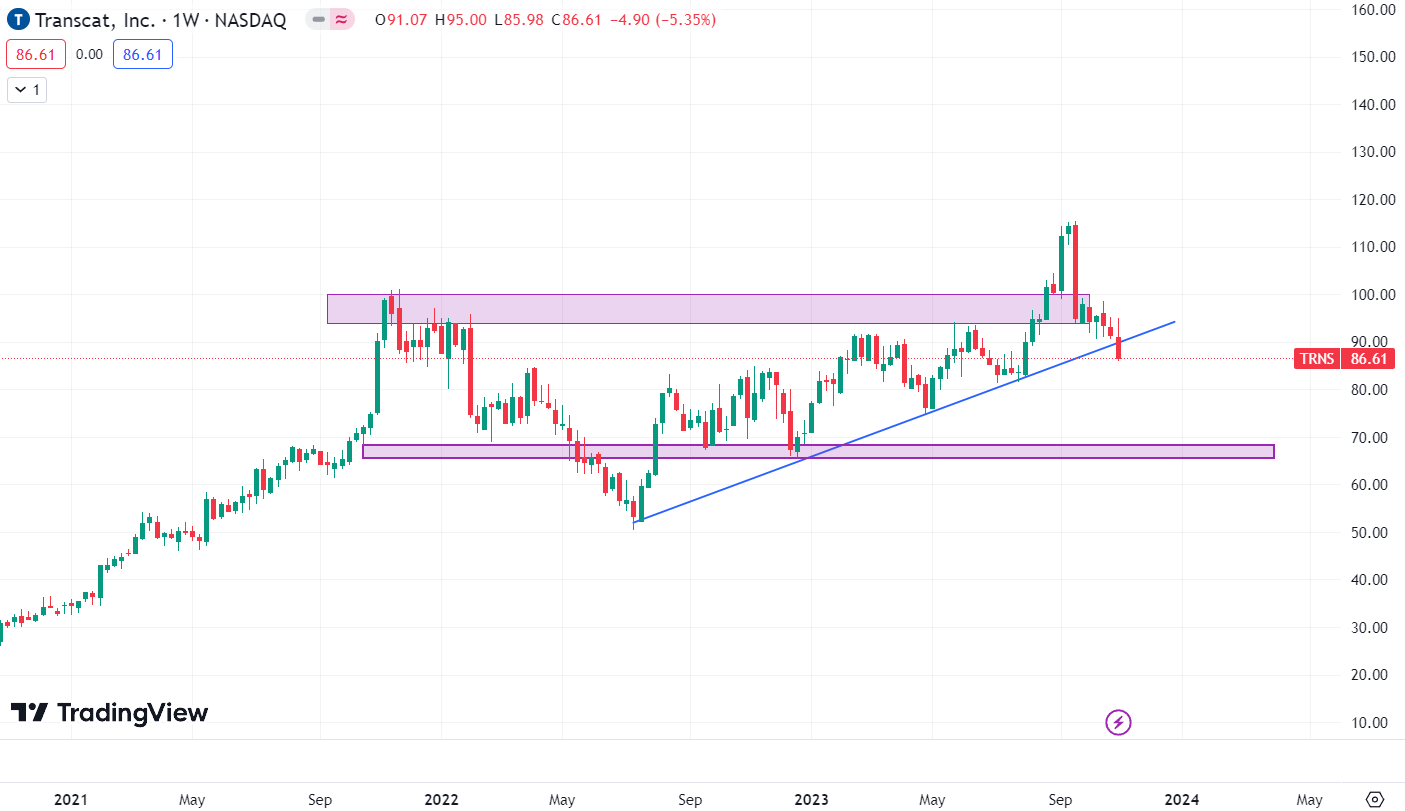

It is trading at $86.6. In the last three months, the stock price has moved a lot. In the month of September, the price gave a huge breakout, but it turned out to be a classic case of breakout failure trapping a lot of investors. Soon after giving a breakout, the stock reversed and went below the breakout level of $100. In my opinion, the current setup of TRNS is quite bearish because it has broken the trendline that the stock has been following since July 2022. This shows that the breakout was just to trap investors. In the last week, the American markets were up by around 6%, but this stock was down 5%, which shows sellers are active in this stock. Looking at the price chart, I think the stock might reach the $70 level in the coming times, as $70 is a strong support for the stock. This gives us a downside of 19% from the current level, and looking at the size of the candles and the time of breakdown, I think the possibility of it reaching $70 becomes high. Hence I would advise to get out of the stock.

Should One Invest In TRNS?

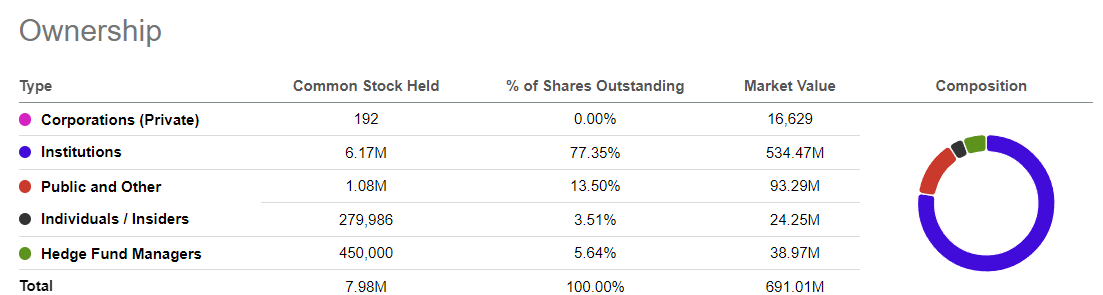

The recent breakout trap and the breakdown are not positive signs, and recently, there was insider selling in the stock in the month of September, which might be causing the share price to drop. Now, if we check its current shareholding pattern and compare it to the last time I covered this company, we can see that the shareholding pattern is also alarming.

{kind=link}

Currently, the institutions hold 77.35% of the shares of the company. The last time, it was 81.2%, so the institutions have slashed their positions, and not only the institution but the hedge fund managers have decreased their positions. However, the public holding has increased to 13.5% from 9%, and I believe the recent breakout was the major reason for the increase, and many individuals got trapped. I believe the main reason behind insider selling and institution selling is overvaluation. I mentioned it last time, and I am still firm on my stance. I still believe TRNS is overvalued. I know that they are experiencing growth, but is it that significant that can justify its overvaluation? The simple answer is no. Now, looking at its valuation . It is trading at a P/E [FWD] ratio of 40.04x, which is higher than its historical average of 38.27x and the sector median of 16.78x. Now, if we compare the valuation to some of the similar firms, we can see that TRNS is trading at way higher valuation. ALTG and DXPE has a P/E ratio of 22.34x and 8.77x.

A breakdown in the stock price, insider selling and institutions decreasing their holdings, high valuation. These things are alarming and suggest that it is time to get out of it. Hence, I am changing my rating to sell from a hold.

Risk

Their capacity to create services and solutions that stay up with changing industry standards, customer preferences in the industries they serve, and technology advancements will decide how successful they will be. For instance, they cater to clients in several sectors, such as life sciences, pharmaceuticals, and other FDA-regulated or industrial manufacturing sectors, that could see quick technological changes, the launch of new products, and adjustments to industry standards. It is impossible to predict whether they can provide new services or adapt current technology in a timely or economical manner or whether the solutions they create will find a market. Their inability to stay updated with technological advancements, industry norms, and consumer preferences in their service markets may negatively affect their business's capacity to attract new customers and maintain a competitive edge.

Bottom Line

Its financial result was decent, and the acquisitions are helping it to boost its growth. But I think the growth isn’t significant enough to justify its high valuation. Aside from the high valuation, many alarming factors make TRNS a sell. First, a huge breakout happened in the stock that turned out to be a trap. At the same time, the shareholding pattern indicates that the institutions and big players have exited the stock in recent times. Additionally, the stock has given a breakdown, suggesting a downside in the coming times. Hence, I am changing my rating to sell from a hold.

For further details see:

Transcat: Might Be The Right Time To Exit