TCLCF - Transcontinental: Print Consistent Dividends With This 6.2% Yield

2023-05-06 04:17:23 ET

Summary

- Transcontinental is a printing and packaging company that is shifting its business mix from a declining industry to a growth industry.

- Since 2017, it has increased the growing segments of its business from 30% of total revenues to over 70% of total revenues.

- While printing may be seen as a 'melting ice cube', the company still derives significant cash flows from this division.

- The company's financial position is solid with consistent free cash flows year to year that more than cover dividend payments.

- At 5.3x EV/EBITDA, Transcontinental is being valued more like a printing company and trades at an unfair discount to its packaging peers.

Introduction

Transcontinental Inc. ( TCL.A:CA ) is a Canadian printing and packaging company. Founded in 1976, the company has diversified from printing into various areas, including flexible packaging, publishing and digital media. The company is one of the largest printers in Canada and is a leader in the flexible packaging space. The company employees over 8000 people and has 41 production facilities across North America.

By segment, about 56% of revenues come from its North American packaging segment, 40% from printing, and 4% from media and publishing. Transcontinental's packaging operations include a diverse portfolio of products that sell to retail, dairy, agricultural, and industrial end-markets. This includes products like shrink bags, thermoforming films, plastic bags, composite bags, and outdoor films and wraps. Transcontinental's printing segment includes a range of products such as flyers, catalogs, books, and magazines, which are primarily sold to retailers and publishers in Canada and the United States. To reduce costs at its printing operations, the company has invested in technology and automation to improve efficiency. Lastly, the media and publishing segment of Transcontinental's business includes newspapers, magazines, and digital platforms, which primarily serve the Quebec market and include the daily newspaper La Presse, as well as magazines such as Elle Canada, Canadian Living, and Style at Home.

{kind=link}

Strategy and Outlook

Over the years, Transcontinental has undergone a shift from being mostly a printing company to a packaging company. As you might expect, printing is a declining business, hence the company has made a strategic shift towards the growing packaging space. Since 2017, it has increased the growth segments of its business from 30% of total revenues to over 70% of total revenues. These growth segments include packaging, but they also reflect a shift in the types of printing the company performs. While flyers continue to generate significant revenues for the company given the unmatched reach and return on investment for retailers, the company has also grown its ISM, book, and pre-media mix from 13% of printing revenues to 32% of printing revenues.

While printing may be seen as a 'melting ice cube', the company still derives significant cash flows from this division. The company aims to be the 'last man standing' on the newspaper segment and capture additional volume as there are still some publishers, but they are not economically efficient to print for themselves.

On the packaging front, Transcontinental's shift towards the packaging industry has helped the company to diversify its revenue streams and mitigate the challenges facing the printing industry. This strategic move has enabled the company to maintain its position as a leading player in the printing and packaging industries in North America. With its focus on innovative and sustainable packaging solutions, the company has also been able to capture a significant share of this growing market.

For the packaging segment, the industry is growing in the high-single digits where demand is driven by consumer's demand for convenience, portability, and sustainability. A key trend in the industry is making packaging 'greener' by using less water and emitting less greenhouse gas emissions. Transcontinental has rolled out a number of products through its sustainable packaging line. It has been recognized by Corporate Knights as #16 on a list of the 100 most sustainable corporations in the world and is included in the Top 50 of the Jantzi Social Index in Canada. The company also has an A rating from MSCI ESG, illustrating its strong performance on environmental, social, and governance criteria that customers increasingly view as important.

Financials

Transcontinental's financial position is solid with consistent free cash flows year to year and no major debt maturities until 2025. With $25.2 million of cash and nearly a billion dollars of debt, most of the debt has been as a result of acquisitions over the years. Nevertheless, the company has reduced its debt by $477 million since 2018 and has a Debt/Equity ratio of 0.66 and Net Debt/EBITDA of 2.8x. In my view, Transcontinental has shown a disciplined approach to profitable growth while reducing net debt.

{kind=link}

One of the first things that attracted me to Transcontinental was its dividend. With a payout ratio of 51%, the shares yield 6.2% at the current price. Since 1993, it has grown its dividend at a 9.8% CAGR and has had a track record of paying a quarterly dividend for nearly 30 years. This is impressive in my view as it demonstrates the company's commitment to returning value to shareholders over the long term, even as it has evolved and diversified its business.

With low debt levels and a solid liquidity position, Transcontinental has the financial flexibility to pursue strategic opportunities, buyback shares or continue issuing dividends. Moreover, with Standard & Poor's recently reaffirmed the company's investment grade rating, this reflects the agency's confidence in Transcontinental's ability to generate consistent cash flows and maintain its dividend payments.

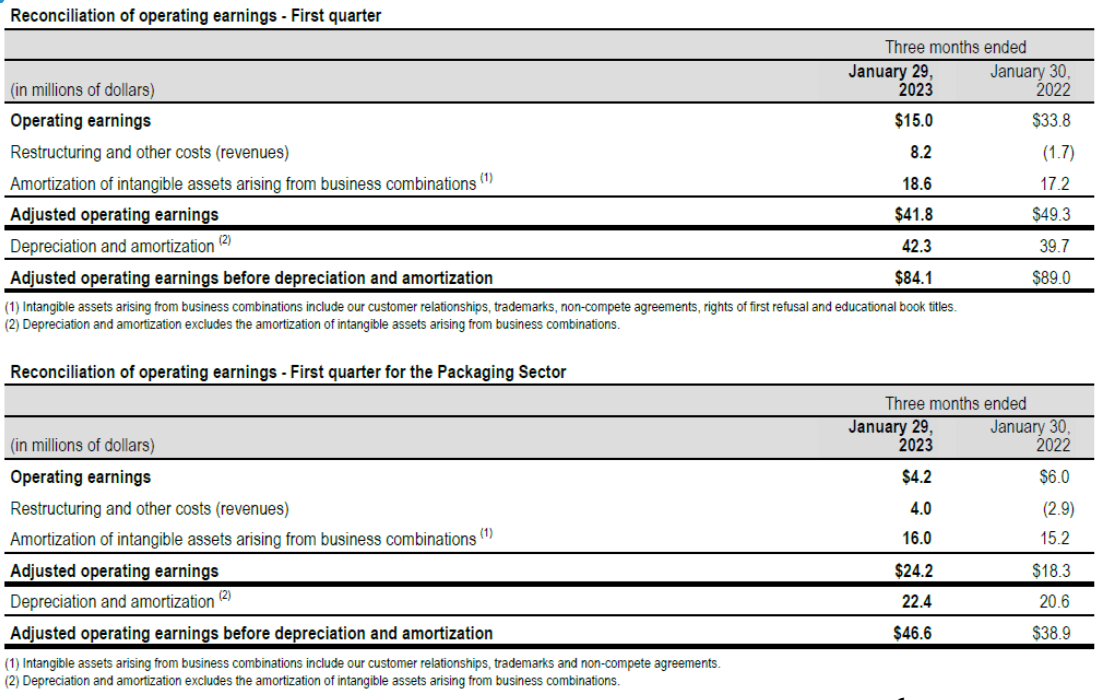

In its most recent quarter , Transcontinental saw printing revenues down 3.1% for the quarter, offset by packaging revenues up 5.7%. Total revenues came in at $707.0 million with adjusted EBITDA of $84.1 million. With operating of $41.8 million, the company's $19.5 million in dividends to shareholders for the quarter is sufficiently supported cash flows from the business.

{kind=link}

Looking forward, management expects that some of the company's cost reduction initiatives in the following quarters will generate significant and recurrent savings , improving financial performance. For packaging volume growth and improved profitability are expected, however, the economic conditions remain uncertain and could affect demand in the short-term. For printing, the company saw growth in ISM and book printing activities, but expects headwinds from inflationary pressures impacting costs and margins.

Valuation

Based on the 4 analysts with one year target prices for Transcontinental, the average price target is $17.25, with a high estimate of $19.00 and a low estimate of $16.00. From the average price target, this implies about 17.5% from the current price. At an EV/EBITDA of 5.3x and P/E of 10.0x, these seem like reasonable multiples to pay for a business that shouldn't see too much growth.

However, when we consider that the share price has done nothing since 2018 despite the business' revenue mix being 73% growth segments as compared with 13%, it seems the market is valuing the company more like a printing company than a packaging company. With other packaging peers like Cascades ( CAS:CA ), CCL Industries ( CCL.B:CA ), and Winpak ( WPK:CA ) being valued at 8.4x, 10.4x, and 7.8x EV/EBITDA, respectively, well above Transcontinental's 5.3x EV/EBITDA, I believe there is an unfair valuation disconnect between Transcontinental and its packaging peers. As the packaging segment grows and the printing segment becomes a smaller part of the company's revenues, I believe the market will reprice the company more in line with its Canadian packaging peers.

Conclusion

In summary, Transcontinental is a leading printing and packaging that has been undergoing a strategic shift from a declining industry (printing) to a growth industry (packaging), driven by its recognition of changing market trends and consumer demand for sustainable packaging solutions. Through its dividend track record and commitment to returning value to shareholders, the company has shown that it is focused on generating long-term value for its shareholders. With its diversified business model and financial discipline, the company's dividend is well-covered by its cash flows and earnings, making this an attractive investment opportunity for income-seeking investors.

For further details see:

Transcontinental: Print Consistent Dividends With This 6.2% Yield