TDG - TransDigm: A Monster Compounder But Does Not Offer Any Margin Of Safety

2023-11-10 23:30:58 ET

Summary

- TransDigm Group has been a monster compounder that has outperformed the S&P 500 and even legends like Warren Buffett and Seth Klarman.

- TransDigm Group is a wide-moat company that investors should consider owning.

- Despite its excellent business model and multi-year double-digit growth potential, TransDigm Group's current valuation does not offer any margin of safety.

Introduction

TransDigm Group ( TDG ) is a group of 48 different companies that, in the words of the CEO Kevin Stein, " own and operate proprietary aerospace businesses with significant aftermarket content ".

According to TDG's 2022 10k, it primarily "design, produce and supply highly engineered proprietary aerospace components". The company sells pumps and valves, motors, actuators and controls, water faucets, and systems, batteries, chargers and power conditioning, aircraft hardware and cockpit security systems, ignition systems and engine sensors, engineered composites, elastomers and laminants, audio systems, lighting and instrumentation, safety restraints and parachutes, all geared towards the aerospace and defense industry.

9 Reasons Why I Like TransDigm Group

As a value investor, I seek value in the companies I invest in. However, more than value, I crave quality first and foremost. A cheap company that has no moat, is easily displaced, and offers no growth, does not interest me. A quality company is what I desire. Not at any price, mind you. My main job as my own portfolio manager is to identify such companies with all the right attributes. Quality always comes at a premium, so I will determine a suitable entry price, and wait for an opportunity to start to dollar-cost-average into the company.

TransDigm Group is a quality company, and let me share nine reasons with you why I believe it is so.

TDG Is A Monster Compounder

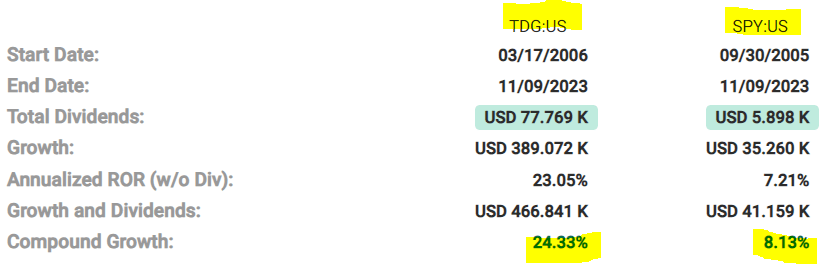

Since TDG's IPO in 2006, the company has demonstrated that it can provide an impressive annualized rate of return of 23.05%, outpacing a similar investment in the S&P by more than three times. With dividends reinvested, long-term TDG investors would have improved their returns by an additional 1.28%, turning a $10,000 investment in 2006 into almost half a million at $466,841 by 2023.

{kind=link}

This 24.33% compound annual growth rate exceeds even the 20% annualized rate of return of legendary investors like Warren Buffet and Seth Klarman.

TDG Is Expected To Grow Earnings At Double-Digit Rates

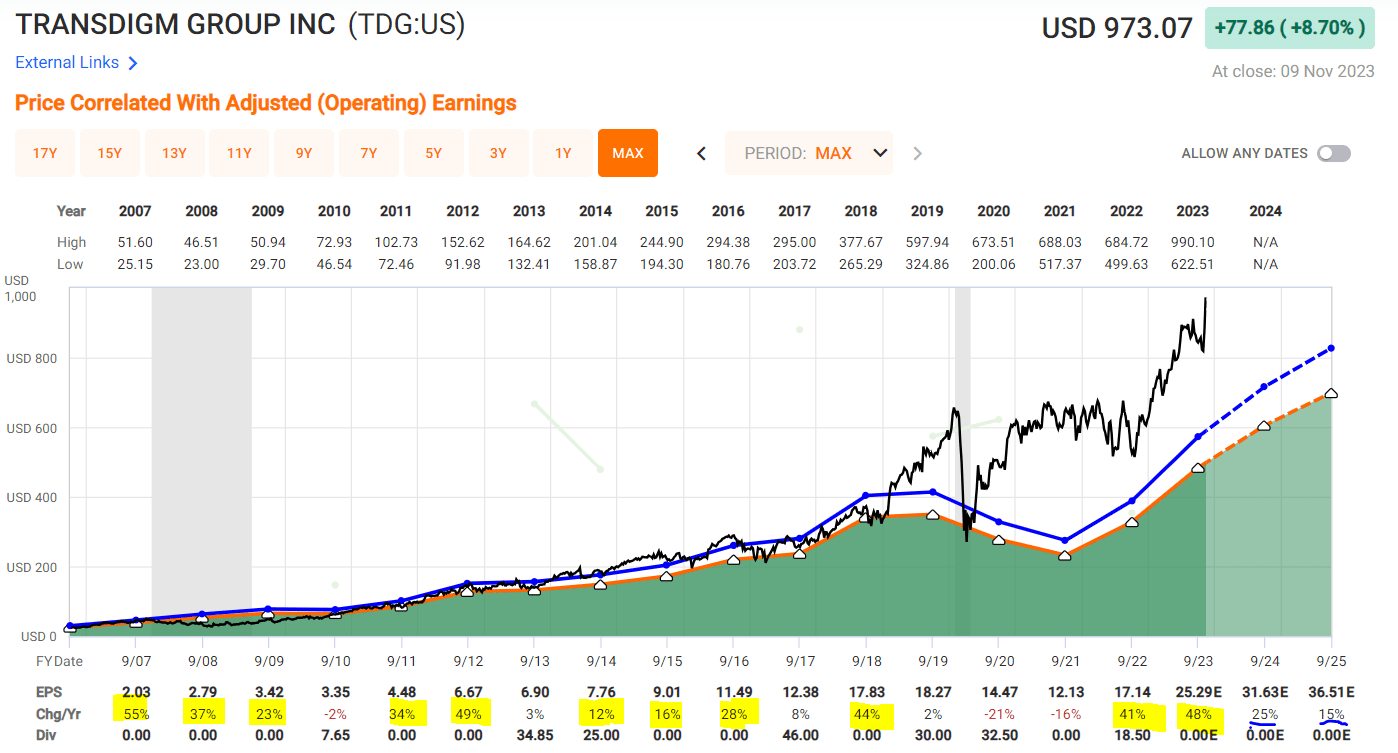

It is important to note that TDG has managed double-digit adjusted operating earnings growth rates multiple times in the past ranging between 12% and 55%.

{kind=link}

Investors should not stop at just doing a backward-looking analysis of a company since past glories are not a guarantee of future performance. Therefore, it is more important to note that consensus analysts' estimates of TDG's earnings growth rate for the next 1-3 years exceed 22% annually (more on this in the Valuation section later).

{kind=link}

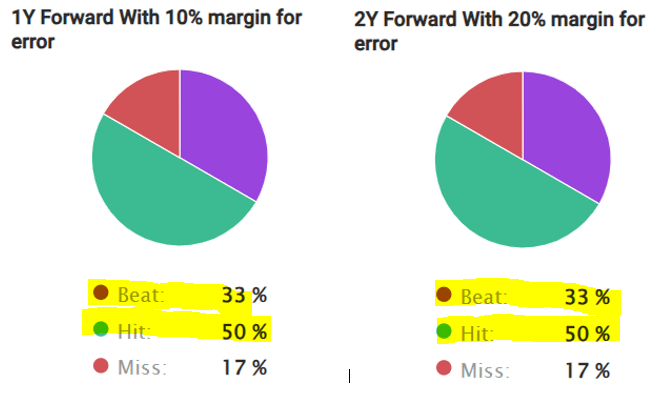

If that growth rate comes to pass, TDG will double its earnings in under three and a half years. Since TDG has beaten or met (FactSet) analysts' 1-year and 2-year adjusted operating earnings projections 83% of the time, I would say it is very probable that TDG can meet or exceed these projections.

In the latest Q4 2023 earnings call , management was cautiously optimistic regarding TDG's growth prospects. CEO Kevin Stein said,

The midpoint of our fiscal 2024 revenue guidance of $7.58 billion or up approximately 15%... This revenue guidance is based on the following market channel growth rate assumptions. We expect commercial OEM revenue growth around 20%. Commercial aftermarket revenue growth in the mid-teens percentage range and defense revenue growth in the mid to high single-digit percentage range.

The midpoint of fiscal 2024 EBITDA as defined guidance is $3.94 billion or up approximately 16% with an expected margin of around 52%...

The midpoint of adjusted EPS is anticipated to be $31.97 or up approximately 24%.

All these bode well for an even better FY 2024.

TDG Has Three Growth Tailwinds Behind It

The hangover from supply chain disruptions that started during the onset of COVID is still present, although to a lesser degree. Co-COO Mike Lisman explained in the recent Q4 2023 earnings call,

The supply chain side, that is starting to ease a little bit. It's with regard to getting the stuff we need in to build – build our components and ship them out the door, we're probably in a better spot than we were, say, 12 or 18 months ago, but the supply chain, our supply chain is still not back to where it was pre-COVID in terms of hitting on-time deliveries and getting stuff to us perfectly on time . So heading in the right direction, but probably still a bit more work to do there and definitely not as much of a headwind as it was, say, 12 months ago.

In spite of the supply chain headwinds, TDG is already posting strong earnings. The latest Q4 2023 earnings that just came out blew expectations out of the water with a double beat on the top line (sales grew 23% in the three-month period ending 30 September to $1.85 billion) and the bottom line (net income grew 56% from $266 million a year earlier to $414 million). As the supply chain increasingly normalizes, TDG will be able to get the raw materials it needs to manufacture its products, and it will get to ship them out to its clients in time, resulting in higher revenue being booked for each subsequent quarter. That is the first growth driver.

The second growth driver comes from the normalization of the businesses like aircraft manufacturers that TDG serves . According to Travel Weekly , a travel industry business-to-business news and research resource trade publication, aviation leaders warned that delivery delays for aircraft and aircraft parts are not easing anytime soon. These delays affect both aircraft manufacturers like Boeing and Airbus, as well as carriers.

The latest 2023 10-K explains the normalization of aircraft manufacturers,

The commercial OEM market recovery is progressing with airlines returning to the commercial OEMs to place orders; however, the continuation of commercial OEM supply chain challenges impacting manufacturers such as Boeing and Airbus are slowing the pace of new aircraft manufacturing . Our commercial transport OEM shipments and revenues generally run ahead of Boeing and Airbus aircraft delivery schedules. As a result, and consistent with prior years, our fiscal 2024 shipments will be a function of, among other things, the estimated 2024 and 2025 commercial aircraft production rates. In fiscal 2023, we experienced improved sales in the commercial OEM sector primarily due to increased production by Boeing and Airbus. Both Boeing and Airbus have disclosed further planned OEM production rate increases for calendar 2024 .

In other words, with increasing normalization of build rates, more multi-year orders will come in from aircraft manufacturers like Boeing and Airbus, thus bringing more orders to TDG.

The third growth driver comes from the normalization of businesses in the commercial end markets that TDG serves. In the past two years, when aircraft manufacturers cannot deliver enough planes to carriers, carriers cannot reach their full capacity even with the resumption of full international air travel. For instance, Airbus could only target 720 deliveries in 2023, which is below the 863 it delivered in 2019. This forces carriers to deploy planes that were originally scheduled to be retired. Using older planes has its issues; more maintenance and longer downtime are expected, more repair parts are needed, and the supply chain issue exacerbates the problem to the extent that some airlines like Air New Zealand have to cannibalize parts from some planes to keep other planes in the air. As explained in the 2023 10K,

Throughout fiscal 2023, we continued to see a rebound in our commercial aerospace end markets from the COVID-19 pandemic and are encouraged by the progression of the commercial aerospace market recovery to date. Commercial air travel in domestic markets continues to lead the air traffic recovery with most domestic markets nearing, achieving or surpassing pre-pandemic air traffic levels.

Thus, the normalization of the commercial aerospace end market has provided a boost to TDG's sales in 2023, and it will continue to do so in 2024 and beyond.

TDG Has A Wide Moat

Recently, Forbes senior editor Jeremy Bogaisky investigated TDG's businesses after the Department of Defense (DoD) accused it of overcharging for the products it procured from TDG, in some cases upwards of 4000% profit margin. In the interview , Jeremy recounted a source of his who said, " Without TDG's products, your planes don't fly ".

In the interview, Jeremy Bogaisky revealed that DoD, in an initiative to reduce costs, set up a division to look into replicating some of the products they are buying from TDG but the "progress is slow", and understandably so. According to the 2023 10K,

The commercial aircraft component industry is highly regulated by the Federal Aviation Administration (“FAA”) in the United States and by the European Union Aviation Safety Agency in Europe and other agencies throughout the world, while the military aircraft component industry is governed by military quality specifications. We, and the components we manufacture, are required to be certified by one or more of these entities or agencies, and, in many cases, by individual OEMs, in order to engineer and service parts and components used in specific aircraft models .

It is a tall order for the DoD and any competitor out there who thinks it can just swoop in to replace TDG's products that are used in mission-critical machines like airplanes and helicopters. TDG does not make easily replaceable nuts and bolts. 2023 10K states that " 90% of our net sales for fiscal year 2023 were generated by proprietary products ". TDG designs, produces, and supplies highly engineered aircraft components for use on nearly all commercial and military aircraft in service today .

Now, talk about having a wide moat.

TDG Can Raise Prices To Pass Costs On

Because TDG's products are so mission-critical, and planes cannot fly without them, and TDG is the only one able to sell these, it can raise prices pretty much however and whenever it wants to. In the Q3 2023 earnings call, CEO Kevin Stein admitted that TDG can even raise prices more than once a year,

I think we do regular catalog price increases, but in a high inflationary environment, dynamic pricing becomes more of the norm . So I don't think our businesses necessarily are augured into, only once a year.

TDG Business Model Has Recurring Revenue

The 2023 10K states this,

Most of our products generate significant aftermarket revenue . Once our parts are designed into and sold on a new aircraft, we generate net sales from aftermarket consumption over the life of that aircraft, which is generally estimated to be approximately 25 to 30 years. A typical platform can be produced for 20 to 30 years, giving us an estimated product life cycle in excess of 50 years . We estimate that approximately 56% of our net sales in fiscal year 2023 were generated from the aftermarket , the vast majority of which come from the commercial and military aftermarkets. Historically, these aftermarket revenues have produced a higher gross profit and have been more stable than net sales to original equipment manufacturers (“OEMs”).

Net sales, especially those stemming from defense contracts, can be lumpy, so having the bulk of the revenue of a recurring nature, helps to smoothen the earnings from quarter to quarter.

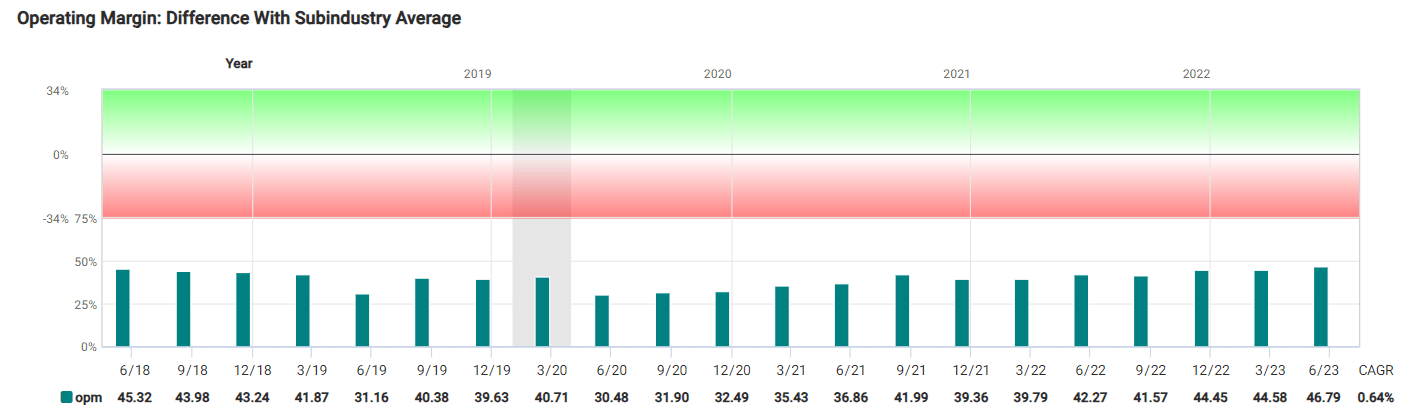

TDG's Business Has High-Profit Margin

All the above - proprietary products, wide moat, recurring revenue which is even more profitable from net sales - points to one logical conclusion, and that is TDG runs a business that spits cash.

{kind=link}

TDG runs a business that generates consistently high operating profit margins that average 40% over the years, which leads it to generate high amounts of free cash flow.

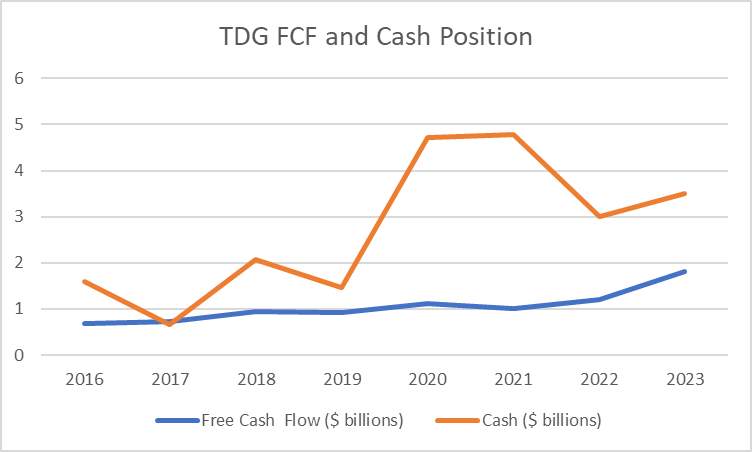

TDG Generates Strong Free Cash Flow

This is a business that is so resilient that it was free cash flow positive even during the depths of the pandemic. In the current fiscal year, TDG generated around $1.8 billion in free cash flow, better than the $1.2 billion it did in FY 2022.

{kind=link}

For a business that seeks to grow via acquisition, it is important that it can generate strong free cash flow that grows yearly, and has a strong cash stash. TDG is in the enviable position of having both. Management is confident that TDG will continue to grow free cash flow in FY 2024. CFO Sarah Wynne said,

With regard to liquidity and leverage for fiscal 2024, as we would traditionally define our free cash flow from operations at TransDigm , which again, is EBITDA as defined less cash interest payments, CapEx and cash taxes, we estimate this metric to be close to $2 billion in fiscal 2024 .

With a business as strong as this, it is no wonder that TDG is able to reward its shareholders well.

TDG Rewards Shareholders Handsomely

I have already described TDG as a monster compounder but it rewards shareholders with generous special dividends too.

Fast Graph

In the most recent press release, management announced a dividend of $35 per share in lieu of its better-than-expected profit . CFO Sarah Wynne announced,

As Kevin mentioned, we ended the year with approximately $3.5 billion of cash on the balance sheet or over $1.4 billion when pro forma for the $35 dividend. At year-end, our net debt-to-EBITDA ratio was 4.8x, down from 5.3x at the end of last quarter. Pro forma for the $35 per share dividend announced this morning, our net debt-to-EBITDA ratio is 5.4x.

Risks

I have articulated TDG's nine defining attributes of quality above. TDG is a wide-moat business that has a high operating margin, able to jack up prices whenever it needs to, has profitable recurring revenue streams that last for decades, has billions of cash on hand, and is able to generate billions more next year.

However, I believe that no business, no matter how excellent, is worth buying at any price. And no business is risk-free, regardless of its quality attributes.

There are two risks that I think investors have to take note of.

High Dependence on Debt for Growth

A company's long-term debt-to-capitalization ratio shows its financial leverage. A higher ratio indicates a riskier investment since debt is the primary source of financing and introduces a greater risk of insolvency.

TDG's current long-term debt-to-capitalization ratio is 111%. That was not always the case. It was only after 2012 that TDG's long-term debt-to-capitalization ratio exceeded 100% every year since.

{kind=link}

To be clear, I am definitely not saying that TDG, a company that is expected to generate $2 billion of operational free cash flow in FY 2024 and is exiting FY 2023 with $3.5 billion of cash, is at risk of insolvency. Management has successfully brought the net debt-to-leverage ratio down from 6.4x at the end of FY 2022 to 4.8x and is expected to reach 4x by the end of FY 2024 (excluding the pending acquisition of CPI's Electron Device Business). Besides, the core management team comprises TDG veterans; CEO Kevin Stein has been at TDG for 8 years, co-COOs Mike Lisman and Joel Reiss spent 8 years at TDG, and CFO Sarah Wynne has been with TDG since 2009. Those are definitely positive signs, but it would be remiss of me not to highlight this to investors, especially in an environment where many expect interest rates to stay higher for longer.

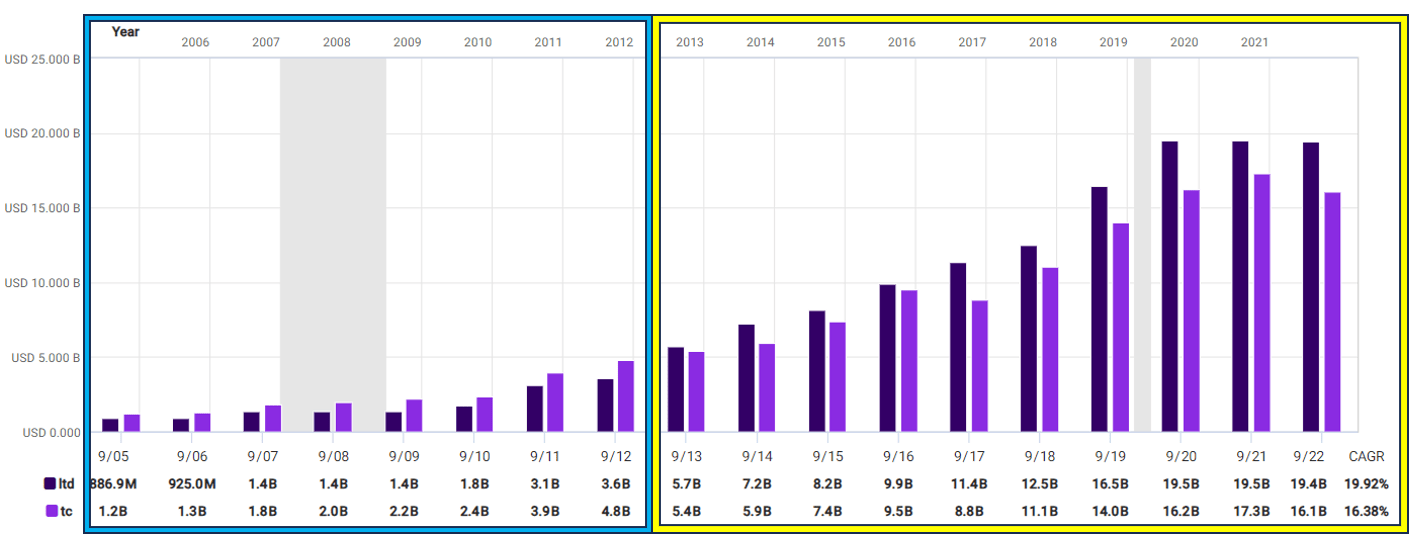

A debt-dependent growth approach also means that TDG will continue to incur higher interest expenses. Interest expense has more than doubled since FY 2016 and has exceeded $1 billion yearly for the past 4 years and management expects interest expenses to reach $1.25 billion in FY 2024.

{kind=link}

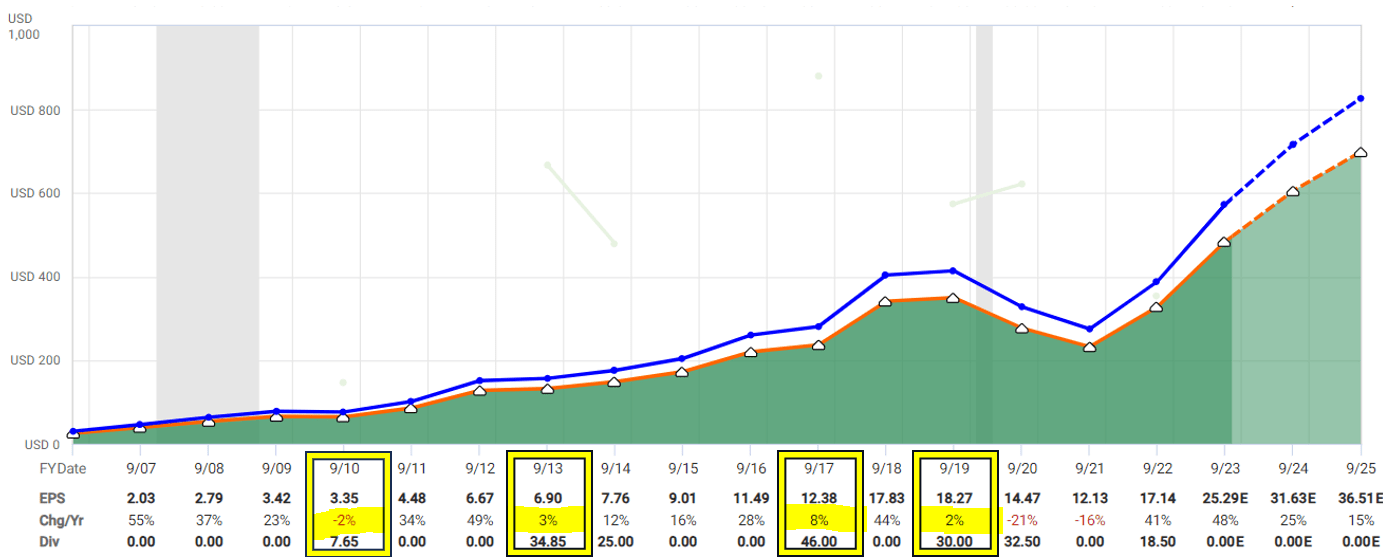

So long as revenue, earnings, and free cash flow continue to grow faster than interest expenses, all will be fine. But downturns can come unexpectedly. Excluding the pandemic years of 2020 and 2021, there were times in the past when the adjusted operating earnings growth rate turned negative (2009) or grew at single-digit rates (2013, 2017, 2019).

{kind=link}

Valuation

At the time of writing, TDG was trading at $973.07 a share after gaining more than 8% after the fantastic Q4 2023 double beat.

Personally, after considering the different scenarios that may happen (see table below) and thinking about the strong tailwinds that will support its growth moving forward, I think TDG is fairly priced for its future growth potential at the price of $973.07.

Author's DCF

In the best-case scenario, if the growth expectations pan out, TDG could be 72% undervalued but if the growth slows, it would be worth a lot less. A more aggressive investor may peg TDG as a dollar-cost-average buy now with a potential 72% upside versus a 27% downside.

I am more conservative and would prefer to wait for a better entry point. No one knows when that will happen but history has shown me two things. One, a slowdown in earnings can happen to even an amazing business like TDG. Two, TDG's stock price has fluctuated wildly every year (see table below) and will continue to do so in the future, and therein lies the opportunity to buy a stake with a margin of safety.

{kind=link}

Conclusion

There are very few companies that I consider belong to the buy-and-hold-forever category. TransDigm Group is one of them. TDG has been a monster compounder. It has been consistently beating or meeting analysts' earnings expectations 83% of the time for both their 1-year and 2-year forecasts so there is a high probability that it can continue to do so.

TDG is a quality stock and quality deserves a premium but a forward P/E of 31 for a company that in the best-case scenario is expected to grow earnings at 25% a year is still too rich in my opinion. As a value investor, "margin of safety" is my mantra, and it is my view that TDG does not offer any margin of safety at $973.07 a share. If I can get at least a 15% to 20% margin of safety on TDG at a price closer to $800 a share, I will definitely start buying. I am definitely willing to pay up to 25 times earnings for a company growing earnings at a rate of 25% and that has crushed the S&P and outperformed legends like Warren Buffet and Seth Klarman.

For further details see:

TransDigm: A Monster Compounder, But Does Not Offer Any Margin Of Safety