TDG - TransDigm: Can The Stock Continue To Fly Higher?

2023-11-06 10:00:56 ET

Summary

- TransDigm Group has a unique operating model in the Aerospace Aftermarket, leading to strong market performance.

- The Aerospace Aftermarket is attractive due to small ticket items, regulatory hurdles, long maintenance and service needs, and long product lifecycles.

- The company seems to be priced for perfection and trades close to its all time highs.

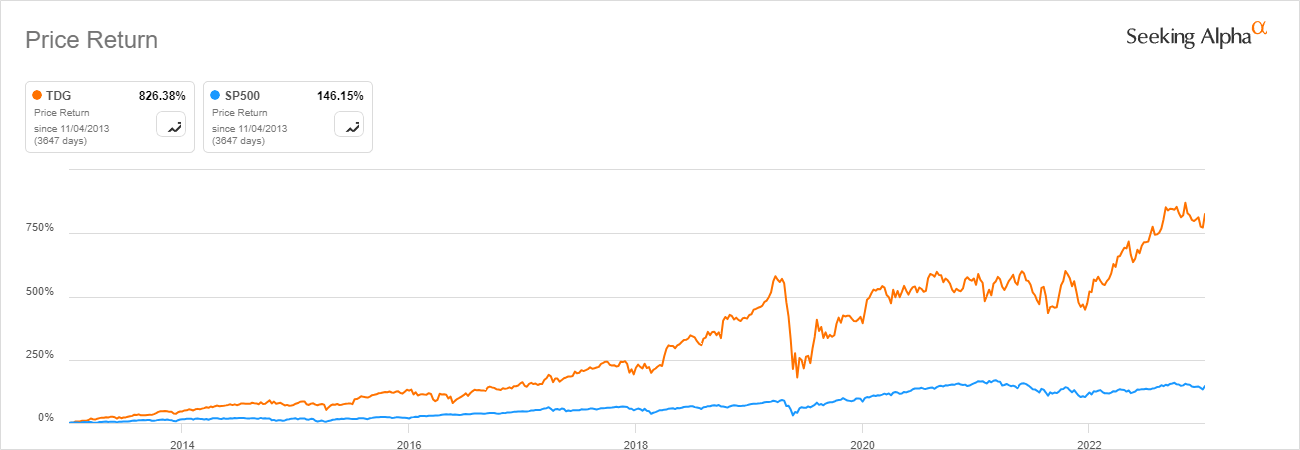

TransDigm Group Incorporated ( TDG ) has crushed the market over the last ten years and beyond with its unique, Private Equity-like operating model in the Aerospace Aftermarket. Let's see if TDG is well-positioned to continue its outperformance.

TransDigm outperformance versus SPY (Seeking Alpha)

{kind=link}

Aerospace Aftermarket

The Aerospace Aftermarket is highly attractive due to several reasons:

- Small ticket items.

- Regulatory hurdles.

- Long maintenance and service needs.

- Long product lifecycles.

I also discussed this industry in my article on HEICO Corporation ( HEI ), another outstanding business. Let's get into detail on the reasons.

TransDigm provides a large and growing number of components to aircraft manufacturers (OEMs), airlines, and defense companies. It estimates its parts to be installed on over 100,000 aircraft, with the vast majority (90%) being proprietary products. The beauty of this business is that air flight is a highly regulated industry with tight safety standards: Every newly introduced product needs to be approved by the US Federal Aviation Administration ((FAA)), the European Union Aviation Safety Agency or equivalent entities worldwide. These regulatory hurdles benefit large players and make it harder for new entrants into the market. Overall, the industry is highly fragmented, from large players down to small companies selling just one or two products into the market.

The usual life span of an aircraft is 25 to 30 years and throughout this whole time, there is an aftermarket demand for these products. You can't easily design new ones into it to replace a part due to regulatory constraints and also the fact that most parts are a tiny fraction of the overall costs of buying and running an aircraft. This locks customers into a product for many years. A product typically can stay in the market for 20-30 years, so combined with a lifespan of 25-30 years, TDG can generate sales for up to 55 years from any given part. As you can see, the Aerospace market is highly lucrative for large players like TDG and HEI.

What makes TransDigm unique?

TransDigm calls its approach a "Private Equity-Like Growth in Value with Liquidity of a Public Market" and expects between 15-20% growth a year on average. To achieve this, they employ their Value-Driven Operating Strategy in combination with levered M&A. Here, three core drivers drive value:

- Obtaining profitable new business: Develop or acquire new products within the existing customer base and relationships by identifying pain points and market gaps.

- Improve our cost structure: Rigorous cost improvements through manufacturing, sourcing, real estate and employee cost improvement.

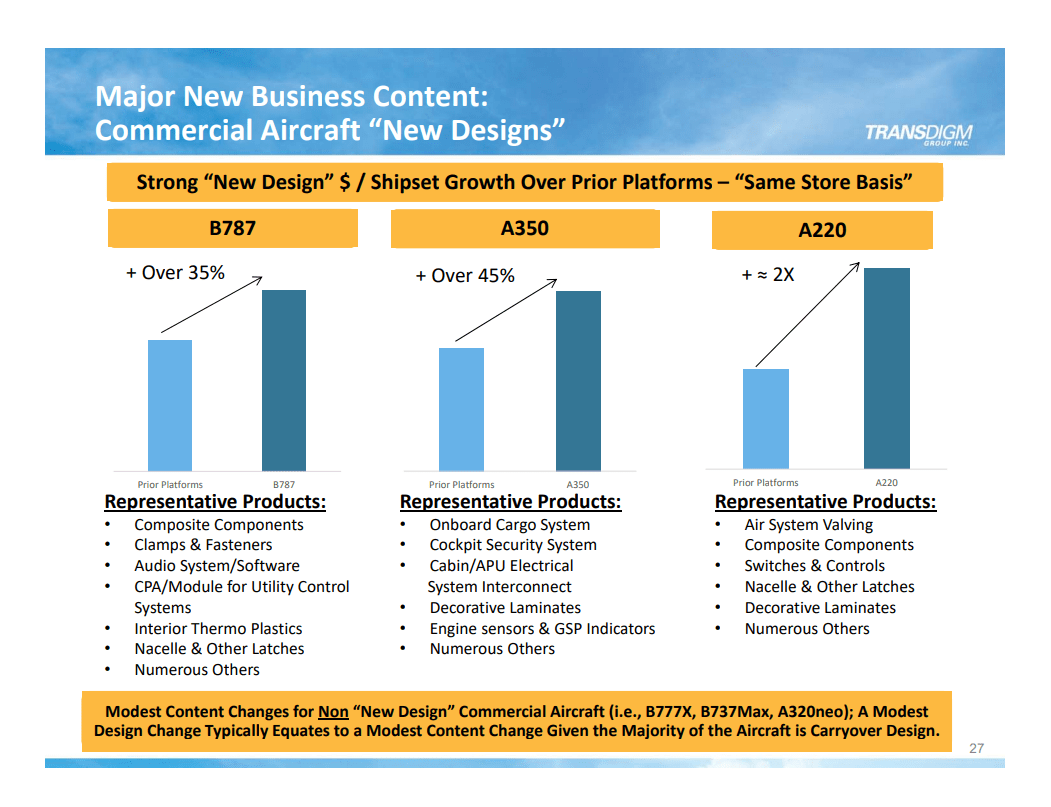

- Providing highly engineered Value-Added products to customers: TDG knows customer service is a considerable competitive advantage in their market. Aircraft owners don't want to worry about small parts; they want reliable partners who quickly act if something doesn't work. This is one of the main differentiators to competition, according to the company. This enables TDG to raise its prices along with improvements in its products. The slide below shows an example of the kind of increased sales a new design can bring for example.

New Design upselling (TDG Investor Presentation)

{kind=link}

TDG typically searches for businesses at 12-15 times EBITDA to bring this multiple down by around 50% post-acquisition by raising the margin through the Value-Driven Operating Strategy. This often includes selling off operating units that didn't live up to the company's standards as well.

Culture

Like many other successful acquirers, TDG uses a decentralized operating model, where management teams at small operating units have significant local autonomy and accountability and can make decisions regarding operations and reinvestment with a focus on creating value. This high-performance culture is topped off with a compensation structure with a high at-risk equity compensation component and low cash compensation to align with shareholders.

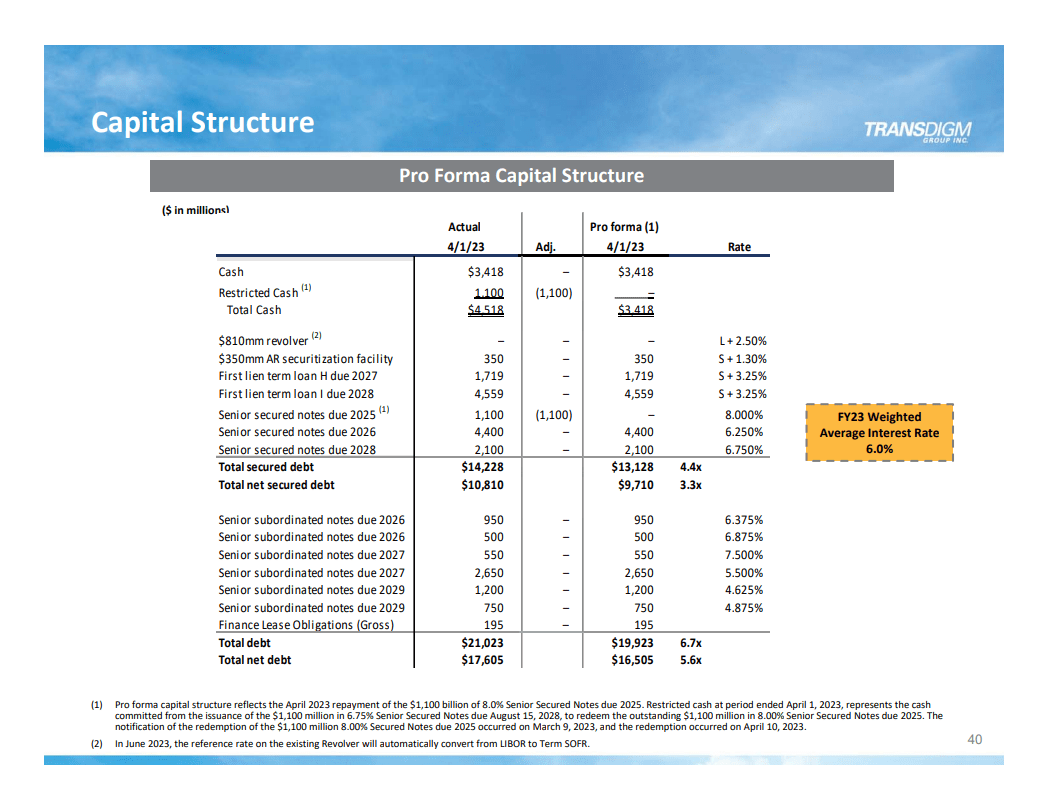

A levered Balance Sheet

TransDigm is a highly leveraged business with a net debt/EBITDA level of 5.5 times. This poses a considerable risk, especially given the high-interest rate environment we are currently in. Fortunately, around 75% of debt is secured or hedged and the weighted average interest rate is reasonable at 6%.

TDG Debt overview (TDG Investor Presentation)

{kind=link}

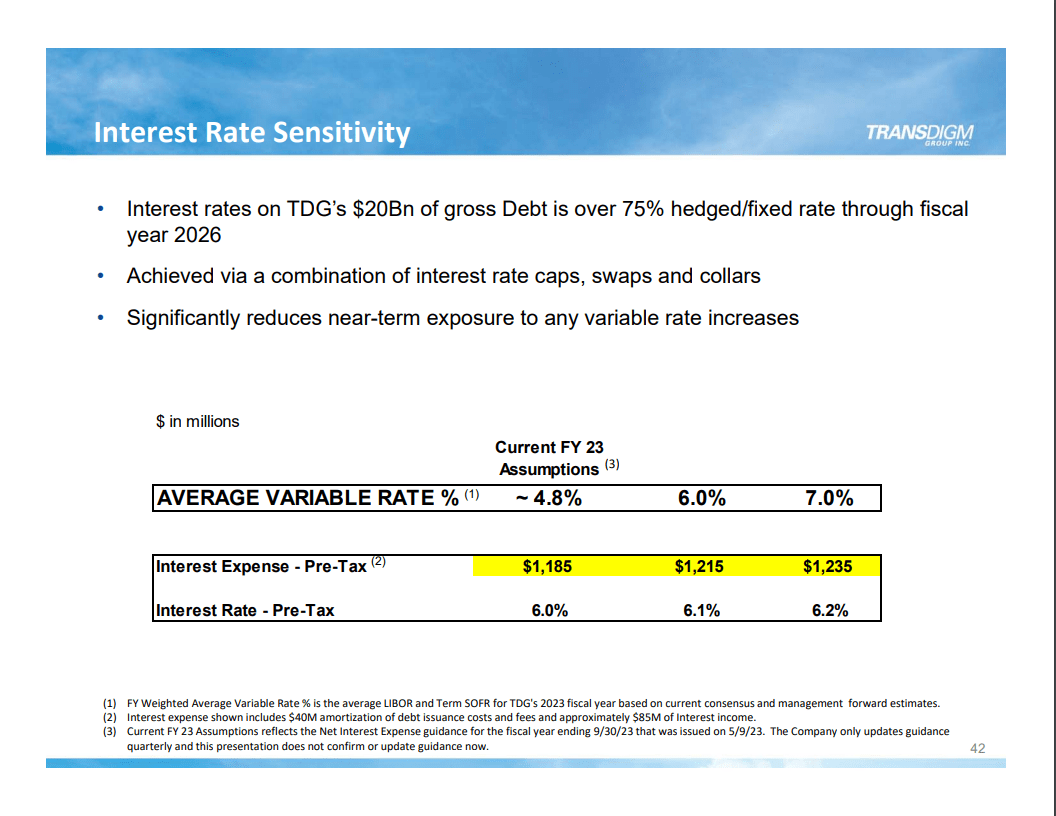

The next maturities are only in 2026 at close to $6 billion and due to the large fixed-rate debt, TDG isn't very sensitive to rate increases, as seen below. I am not comfortable with a company that levers. Still, due to the stable and predictable cash flows and long-term customer relationships, I do not see a large structural risk for the organization.

TDG interest rate sensitivity (TDG Investor Presentation)

{kind=link}

Upcoming Earnings

TDG is going to report earnings on the 9th of November. Over the past eight quarters, TDG has been pretty consistent in beating EPS expectations (7/8 times with beats between 4-14% and only one 5% miss) but more volatile in revenue (5/8 beats but only fluctuating a few percentage points in either direction). Analysts expect EPS to come in 36% higher Y/Y and revenue to grow by 21%, followed by a rapid deceleration in the following quarters. The commercial part of TDG's business still is recovering from COVID-19, while Defense is expected to grow just in the mid to high single-digits range.

Priced for perfection

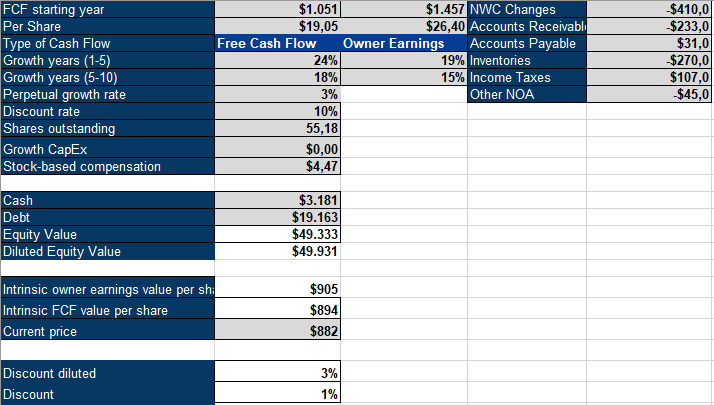

To value TransDigm, I'll use an inverse DCF model. TransDigm is a much more leveraged company than what I usually look at, so it is important to look at Free Cash Flows, in my opinion. EBITDA is significantly higher due to the aforementioned large interest payments. Based on its cash flows, TDG looks to be pretty expensive. A DCF requires a strong growth rate of around 19% for the next five years, followed by a 15% growth rate if we use Owner Earnings. Over the last 30 years, TDG managed to grow revenues at 18% and EBITDA at a 21% CAGR, but as the company scales, this becomes harder to keep up.

TDG Inverse DCF (Authors Model)

{kind=link}

Conclusion

To conclude, TransDigm is a wonderful business and an interesting case study. Currently, the aerospace market is still recovering from the Covid disruption, but it is a mature market and, over the long term, will not outgrow GDP (~3%) too much. While TDG has a repeatable growth process, it is priced for a best-case scenario, in my opinion. Analysts agree and see revenue growth falling behind historical levels of 18%. TransDigm is a wonderful business operating in a great industry, but the market acknowledges this and prices it accordingly. There are a lot of great opportunities in the market right now, with high uncertainty and fear , so I believe investors could be better off putting TDG on a watchlist and waiting for a more attractive entry. Debt remains my main obstacle and the reason why I personally prefer HEICO in the Aerospace aftermarket.

For further details see:

TransDigm: Can The Stock Continue To Fly Higher?