TDG - TransDigm Group: Strong Quarterly Results But Expectations Seem To Be Running Hot Ahead

2023-08-28 03:18:45 ET

Summary

- TransDigm Group has had a strong year, with a 70% rally, but the current valuation is not favorable for investment.

- TDG's recent performance exceeded expectations, with significant revenue growth in the commercial aerospace and defense segments.

- The company's M&A strategy and potential acquisitions could help offset any slowdown in aftermarket growth, but regulatory scrutiny is a concern.

Investment action

Based on my current outlook and analysis of TransDigm Group ( TDG ), I recommend a hold rating. While I really like the business, growth momentum, and capital allocation policies, I am not in favor of investing at the current valuation. The stock has done really well this year, putting up a rally of nearly 70%. I believe expectations are running high, and investing today puts my capital at risk of sharp derating in the near term if TDG fails to meet expectations.

Basic info

TDG is a popular name among investors and hedge funds. The business designs, produces, and supplies highly engineered aerospace systems, subsystems, and component parts for nearly all aircraft currently in service.

Review

TDG historical performance is nothing but outstanding when reviewed over the past 15 years. Revenue grew by ~15x from $435 million in FY11 to $6.2 billion LTM, fueled by consistent contribution of organic and M&A, which goes hand in hand. TDG would acquire subscale assets but complementary to the business, and drive a serious of price increase (organic growth contribution) that carries very high margins. The high margins gave TDG a lot of purchasing dry powder as it generates a lot of cash (EBITDA as proxy). For perspective, TDG increased its EBITDA from $182 million in FY06 to $3 billion over the LTM. The business has also always generated FCF over the past 15 years, indicating the business ability to be flexibility in managing its working capital and CAPEX requirements. While TDG is running a very levered balance sheet, note that the business has always been profitable and spits cash. The highly re-occurring business nature gives the business very high visibility into its upcoming cash flow. Hence, even at 6+x net debt to EBTIDA, I don't think there is major balance sheet risk here. Also note that TDG got through the covid period fairly unscathed (stock is up more than 100% since then), which arguably is the worst period for TDG as global flights come to a halt.

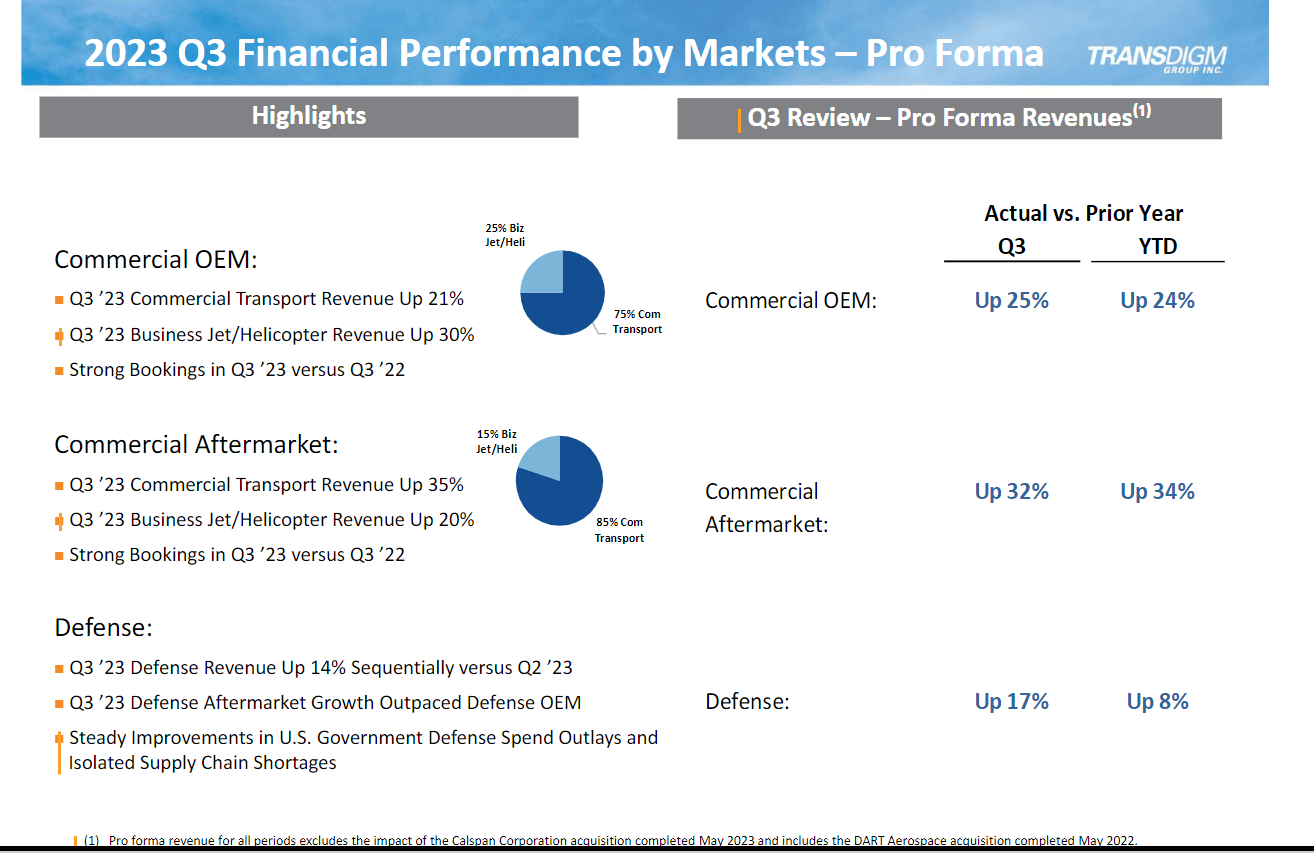

In Q3 2023, TDG once again significantly outperformed expectations. Commercial Aerospace OEM PF revenue grew by 25%, contributing to total revenue growth of 21% to $1.74 billion. Within that, business jet and helicopter revenue increased by 30% and commercial transport by 21%. Sales in the Commercial Aerospace Aftermarket [AM] PF increased 32% overall, with commercial transport contributing 35% and business jets and helicopters contributing 20%. Finally, OEM & Aftermarket PF sales for the defense aerospace industry increased by 17%. Strong revenue growth resulted in an increase in EBITDA margin by 270bps to 52.5%, which in turn led to an increase in EPS to $7.25 from $6.38.

{kind=link}

There are two areas I think it is worth highlighting in 3Q23.

First, the Defense segment has begun to grow again. You may remember that TDG's Defense segment performance has not been good in recent history as outlays fell behind budget and supply chain issues. However, as TDG's outlays have increased and its supply chain has improved, sales have followed suit. In my opinion, defense growth could potentially exceed guidance in FY23 due to accelerating activity and easy comps. Second, similar to the previous quarter, TDG's management reported that the pipeline for potential acquisitions was still active. However, I also take note of TDG's intention to maintain its discipline, which is important in light of current high valuations. Based on my cash analysis, using consensus EBITDA and FCF estimates, TDG should be able to reduce its net debt to EBITDA ratio in FY25. If we assume that TDG will maintain its leverage ratio at the current level, they would be able to draw an additional $11 billion of debt in FY25, which is a significant amount of dry powder for them to conduct M&A. I note here that TDG has historically maintained leverage ratios >6x, so the amount of dry powder available to drawdown could be a lot more than I expect.

Author's work

This M&A strategy is not only important for shareholders in terms of capital allocation; it also helps negate the negative sentiment of TDG AM segment growth slowing. Despite another quarter of strong growth in commercial AM sales of more than 30%, book-to-bill fell below 1x in 3Q23. Pro forma sequential AM growth also decelerated to 2% in 3Q23. As normalization of traffic growth occurs and higher OEM deliveries drive retirements, I expect aftermarket growth to slow eventually. With so much cash on hand and proven M&A chops, TDG may be able to buy more time for its AM sales to grow. Even if TDG doesn't acquire assets, paying out dividends should be an eventual move that could also yield attractive returns. For instance, the additional $11 billion in debt is around 25% of TDG's current market cap.

Valuation

Author's work

I believe TDG can grow at the consensus expected growth rates for the near term, given the strong underlying performance so far. Given the elevated risk in FY23, growth in FY24 and FY25 should start normalizing back to historical organic growth rates in the mid-single digits. Margins should expand as TDG continues its strategy of raising prices and reaping synergies from any M&A deals. However, I think the market has already priced all of this optimism and expectation into the stock. Currently trading at 17x forward EBITDA, TDG is fairly valued, in my opinion. Comparing TDG to peers, the current forward EBITDA is within its fair range as well. While the expected revenue growth rate is similar to peers, TDG has a much better margin profile and competitive position in the industry (TDG is as good as a monopoly). In addition, even when compared to TDG own historical trading range, it is now trading at the higher end, which means more room for multiples to fall. Over the past 10 years, TDG traded in the range of 13x to 18x forward EBITDA. If we exclude the covid years, TDG would be trading in the 13x to 16x forward EBITDA range, making the current 17x forward EBITDA seem more overvalued.

Author's work

Risk and final thoughts

The death nail to TDG's business model is regulators stepping in and limiting TDG's ability to raise prices. A key part of the TDG business model is to acquire airplane parts companies and raise prices, which is a very appealing and lucrative model. Here is a summary of why TDG might be a target of regulators, by Citron Research .

Citron compared the TransDigm's business model to that of Valeant Pharmaceuticals , which the firm previously called the "pharmaceutical Enron." Citron said TransDigm "acquires airplane parts companies (over 50 in total), fires employees, and egregiously raises prices." Citron's executive editor, Left, is an activist short seller.

In conclusion, while TDG continues to demonstrate impressive growth and strong financial performance, I recommend a hold rating for now. The stock's current valuation seems to incorporate high expectations, potentially exposing investors to downside risk if these expectations are not met. TDG's historical success in raising prices and its M&A strategy are noteworthy, but the concern of regulatory scrutiny adds an element of uncertainty. Despite its solid competitive position and margins, the stock's current trading level appears to reflect its strengths.

For further details see:

TransDigm Group: Strong Quarterly Results, But Expectations Seem To Be Running Hot Ahead