TDG - TransDigm Is A Superior Aerospace Stock

2023-05-23 09:11:31 ET

Summary

- TransDigm is a unique aerospace supplier with significant pricing power, after-market exposure, and a strong commercial/defense mix.

- The company's stock price is having a great year thanks to rebounding demand and higher margins.

- Despite elevated debt levels, the company has a healthy balance sheet and opportunities to accelerate M&A.

- The valuation has become a bit lofty, which is why I am waiting for a 10% to 15% stock price correction before buying.

Introduction

One of the biggest mistakes of my investment career so far is not owning TransDigm Group ( TDG ) shares in my dividend growth portfolio. While the company isn't a traditional dividend growth stock, it is a fast-growing M&A-driven aerospace supplier with a superior business model, which uses special dividends to further boost the total return.

This year, the stock has broken out. TDG shares are up 28% year-to-date and 53% higher compared to May 2022.

This move is fully backed by recovering aerospace demand. Both commercial and defense aerospace demand is recovering, allowing the company to use pricing power to further boost its bottom line.

In this article, we'll discuss all of that, including my decision to buy the stock the moment it gives us a buying opportunity.

So, let's get to it!

What Makes TDG So Special

Before we dive into its earnings, it's important to start this article by highlighting what makes TDG such a special stock.

With a market cap of $44 billion, Cleveland-based TransDigm is one of the world's largest aerospace suppliers. The company produces a wide range of supplies used in almost every airplane in the world.

The company expands its portfolio by consistently buying new firms, which are then improved to boost earnings power. Essentially, TDG is an aerospace-focused private equity company.

We have a decentralized organizational structure and a unique compensation system closely aligned with shareholders. We acquire businesses that fit this strategy and where we see a clear path to PE-like returns. - Kevin Stein, President & CEO

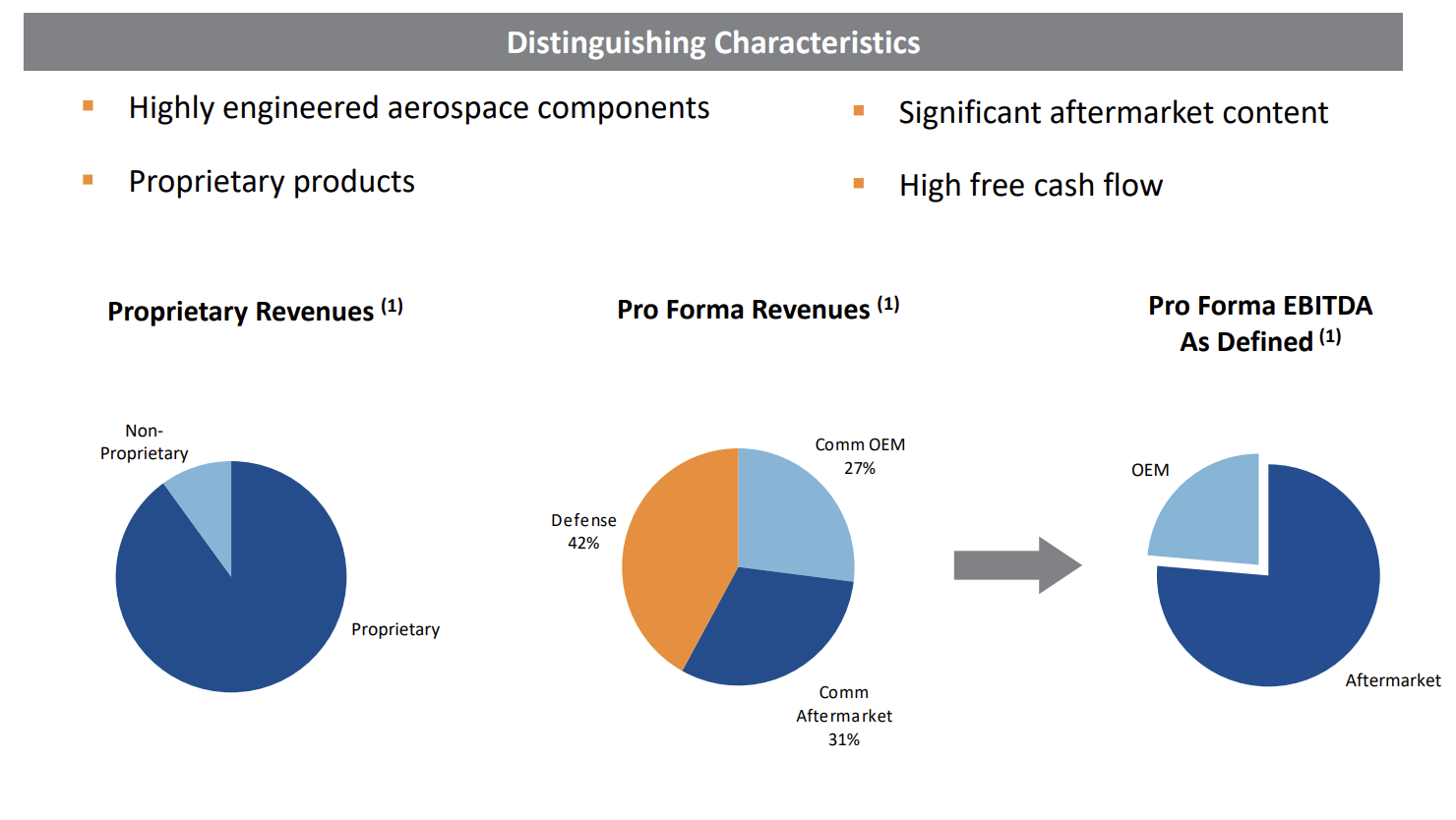

Not only that, but TransDigm is focusing on exclusive products that are difficult for competitors to replicate, enabling the company to wield considerable control over pricing.

TransDigm's market position is further reinforced by the fact that it often stands alone as the sole provider of its products, with a whopping 80% of them lacking any feasible alternatives.

What's more, over 75% of TransDigm's products cater to aftermarket sales, which opens up tremendous opportunities for long-term customer relationships and recurring revenue.

{kind=link}

TransDigm Group

Hence, as I wrote in my last article , TransDigm's success can be attributed to...

- Its ability to identify and acquire smaller suppliers with limited competition.

- Building a portfolio of niche products with high-pricing power.

- Generating increasing free cash flow, which is used to reduce M&A-related debt.

When looking at the bigger picture, we see that revenues are at pre-pandemic levels. EBITDA has exceeded pre-pandemic levels.

With that in mind, earlier this month, the company released its earnings, which confirmed that business is back to normal.

TransDigm Is Firing On All Cylinders

2Q23 Performance

TDG had a strong second fiscal quarter that exceeded expectations.

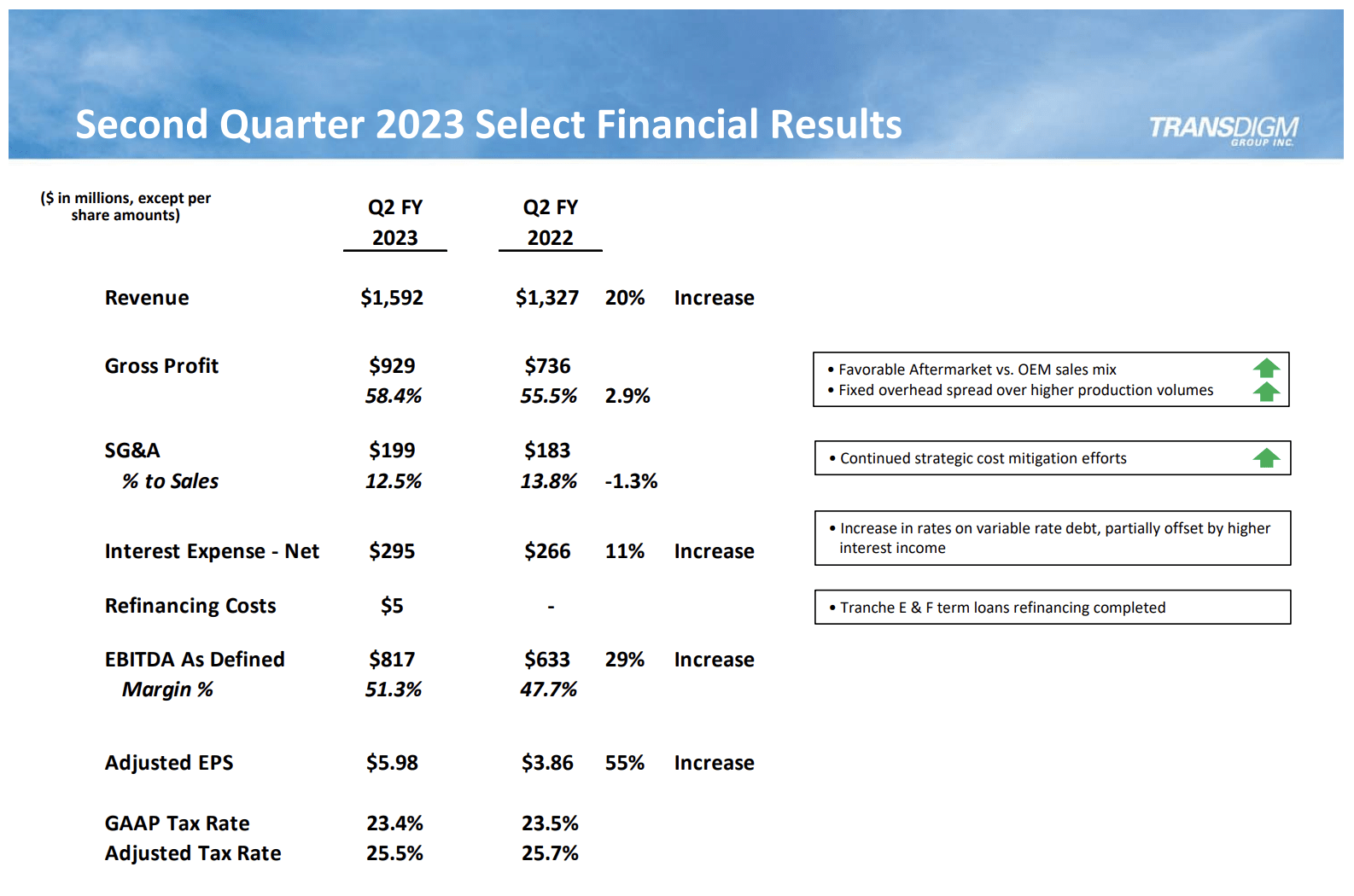

Adjusted EPS came in at $5.98, beating estimates by $0.51. Revenue came in at $1.59 billion, rising 19.5% year-on-year and beating estimates by $60 million.

The commercial aerospace market continues to recover, with favorable trends and robust demand for travel, particularly in global domestic air traffic.

While international travel is also progressing, the industry's results are still slightly depressed compared to pre-pandemic levels.

The reopening of China has had a positive impact on the air cargo outlook, although global trade signals remain mixed.

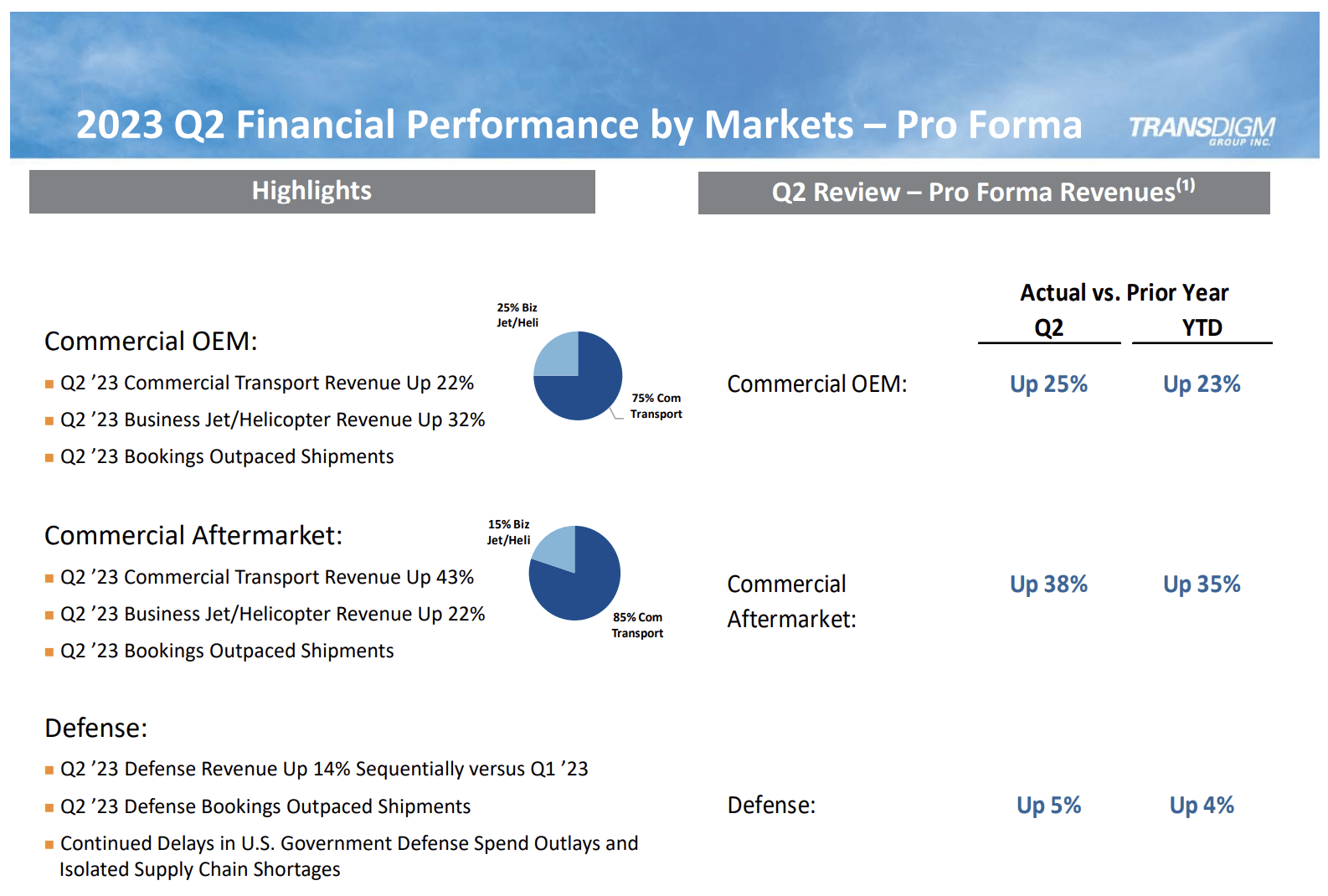

TDG experienced substantial growth in total commercial revenues and bookings across all major market channels: commercial OEM, commercial aftermarket, and defense.

{kind=link}

TransDigm Group

- Commercial original equipment manufacturer ("OEM") revenue increased by approximately 25% compared to the prior year period, with sequential growth of 17%. Bookings also showed significant improvement, with a growth rate of over 15% compared to Q1.

- Commercial aftermarket revenue increased by roughly 38% in Q2, mainly driven by strength in the passenger sub-market. All commercial aftermarket sub-markets experienced significant growth compared to the prior year period, and sequential revenue increased by approximately 14%.

- The EBITDA margin improved to 51.3%, driven by the company's operating strategy and recovery in commercial aftermarket revenues.

{kind=link}

TransDigm Group

TransDigm generated $130 million of operating cash flow in Q2 and ended the quarter with over $3.4 billion of cash.

TDG expects to steadily generate significant additional cash throughout 2023. It also believes that its operating units are in a good spot to support higher production targets in light of improving demand.

Furthermore, defense sales were a tailwind, too. Generally speaking, defense sales account for roughly 35% of total sales.

- Year-on-year revenue growth was 5%. Sequential growth was 14%.

Adding to that, the company noted that defense bookings outpaced sales, indicating positive future defense order activity. This is in line with comments from other defense majors, who are seeing book-to-bill ratios above 1.0.

Defense market revenues continue to be impacted by the lag in US government defense spending outlays.

TDG expects low to mid-single-digit percent range growth in defense market revenues for the year.

M&A - Calspan Corporation

Another thing worth mentioning is the fact that TDG acquired the Calspan Corporation for roughly $725 million in cash.

Calspan is engaged in aftermarket-focused aerospace and defense development and testing services, with a state-of-the-art transonic wind tunnel for commercial and defense markets.

The acquisition is expected to contribute just over $100 million to fiscal year 2023 revenue and have an EBITDA margin slightly less than TransDigm's total company margin.

Furthermore, the company mentioned that the M&A pipeline appeared to be more favorable than before - despite higher rates.

This is due to an increase in the number of properties available for acquisition, including long-rumored properties that have now come to market. The pricing environment for these acquisitions has remained relatively stable, with only slight decreases, and high multiples are still expected.

This brings me to the outlook.

Outlook

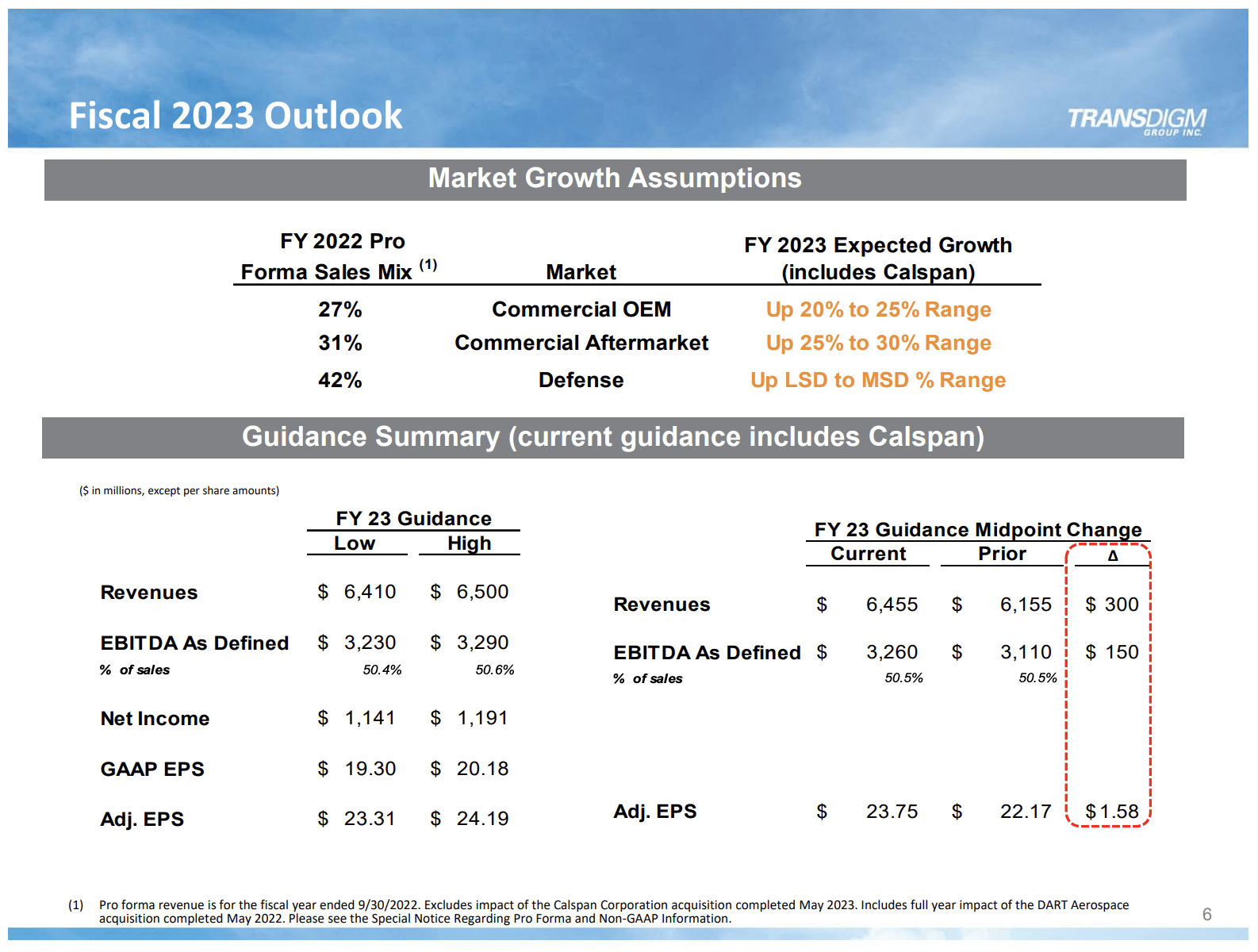

The company's 2023 outlook reflects its strong Q2 results, the Calspan acquisition, and expectations for the rest of the year.

At the midpoint, sales guidance was raised by $300 million, and EBITDA guidance was raised by $150 million.

TDG expects continued recovery in its primary commercial end markets without assuming additional acquisitions or divestitures.

{kind=link}

TransDigm Group

Furthermore, with regard to post-pandemic supply chain issues, the supply chain was reported to have recovered well, with a stable and predictable performance from suppliers. Some minor challenges remained with electronic components, but overall improvement was observed.

Labor market conditions improved at most locations, particularly for production labor, while the availability of higher technical and engineering expertise remained somewhat tight but showed signs of improvement.

Balance Sheet & Valuation

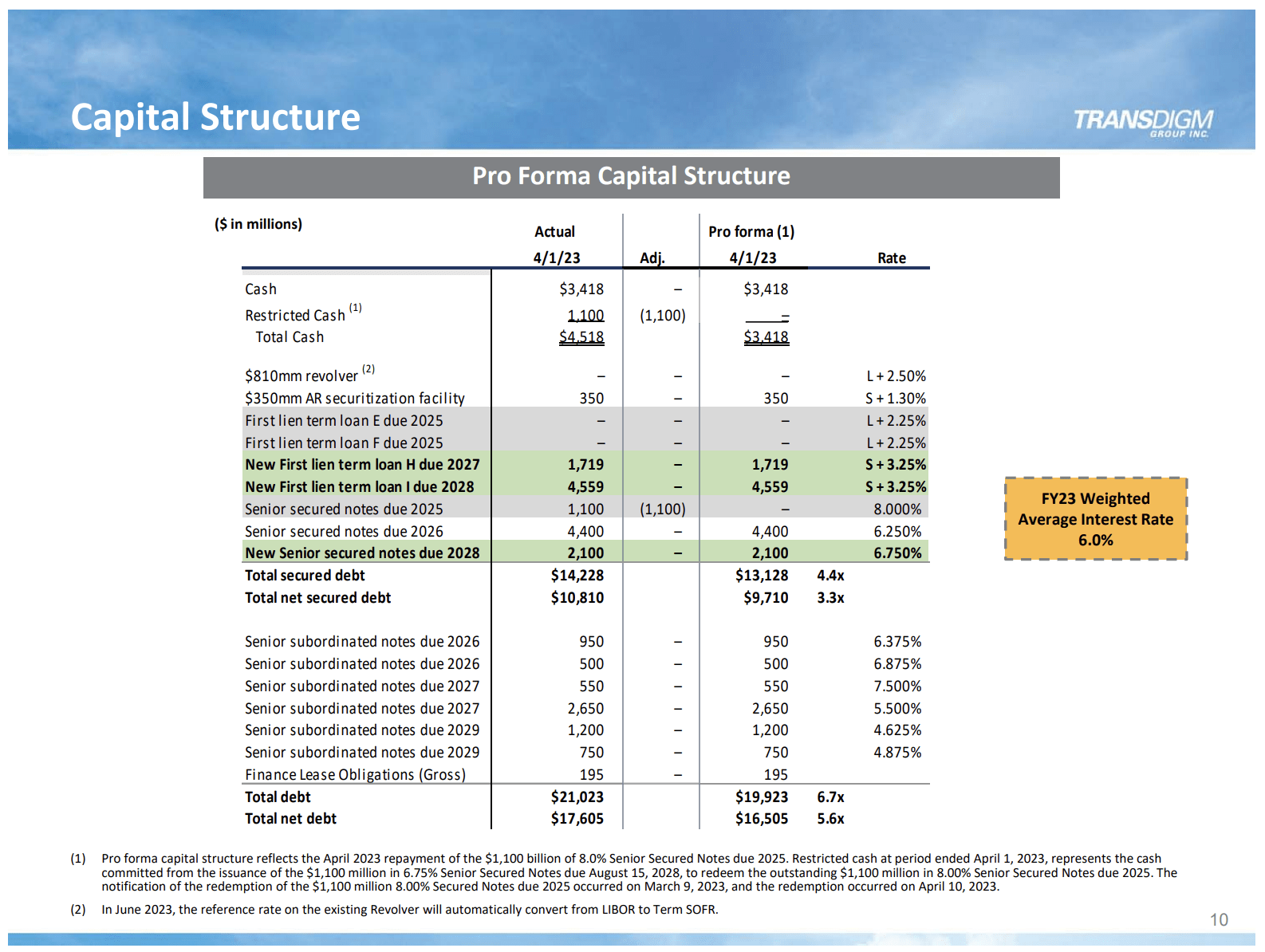

TransDigm has a lot of debt, which is why discussing its balance sheet is so important - especially in light of the current high-rate environment.

The company ended the second quarter with $19.9 billion in gross debt. Net debt was $16.5 billion. This translates to a net leverage ratio of 5.6x, which is somewhat elevated - but not unusually high for TDG.

{kind=link}

TransDigm Group

The company's FY23 weighted average interest rate is 6.0%, which reflects its elevated debt load.

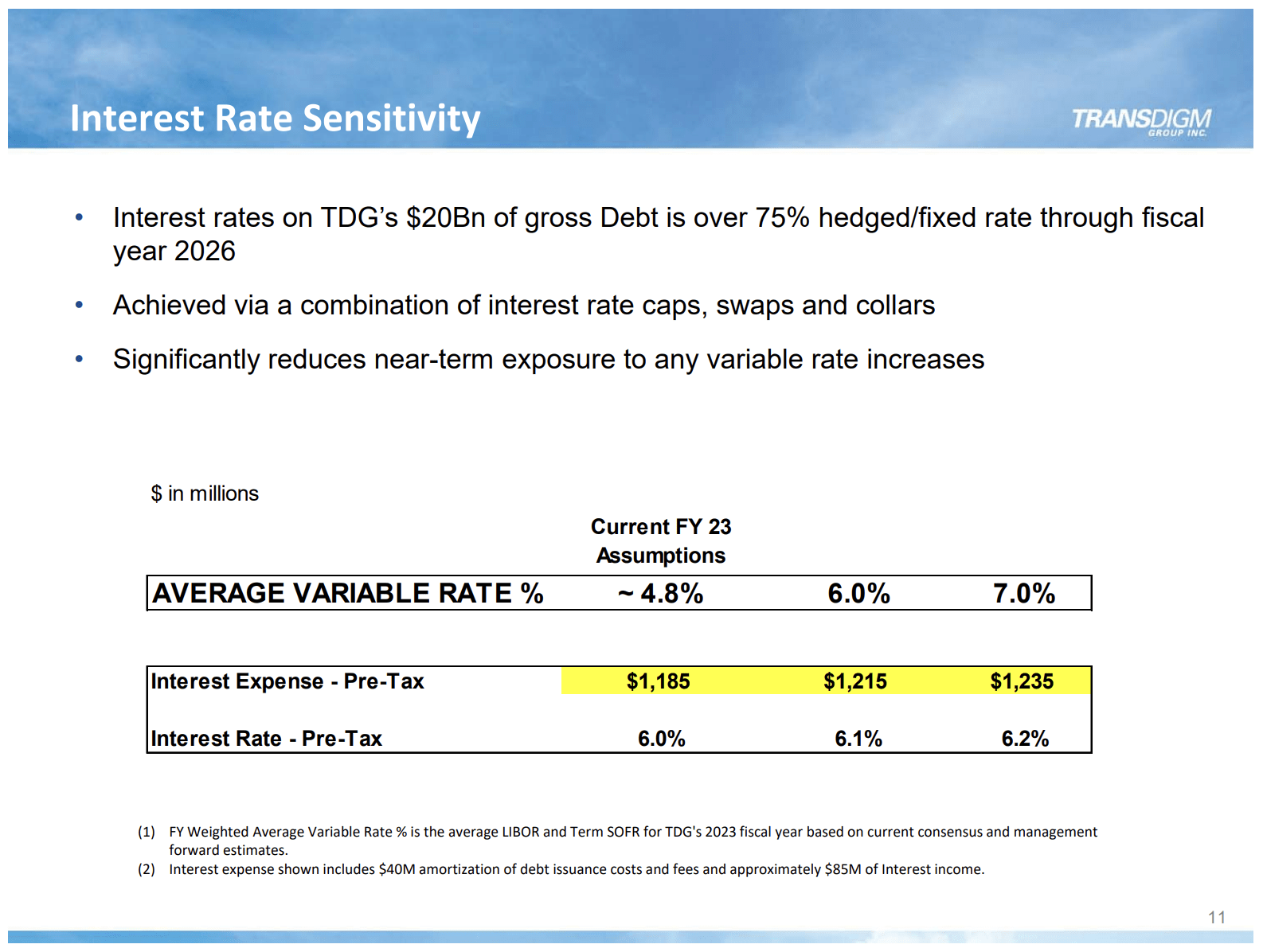

With that said, the company has hedged most of its interest rate risks. Over 75% of its debt is hedged/fixed through fiscal year 2026. Even if rates continue to rise, the company is likely to maintain steady interest expenses.

{kind=link}

TransDigm Group

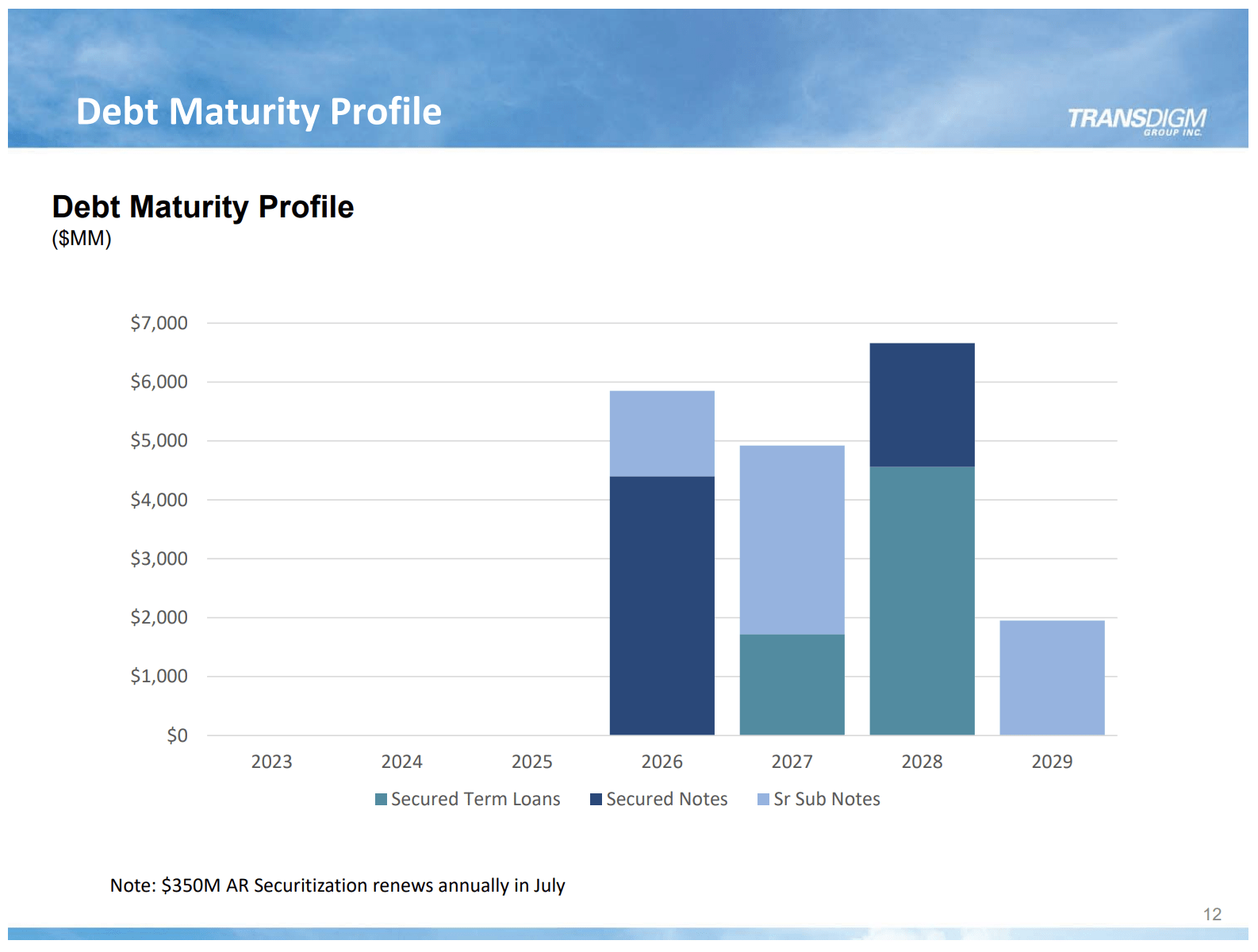

Furthermore, TransDigm has no debt maturities until 2026, which buys the company a lot of time in this high-rate environment.

{kind=link}

TransDigm Group

Unfortunately, the valuation is a bit elevated after the recent rally.

The company is trading at 19x NTM EBITDA. The longer-term multiple is close to 16x.

While a certain premium is certainly appropriate, given the surge in demand, I believe that TDG shares are a good buy on a 10% to 15% drawdown.

FINVIZ

While waiting for a correction comes with the risk of missing more upside, I am looking to buy TDG at $700.

Takeaway

TransDigm Group is a fast-growing aerospace supplier with a unique business model and a focus on exclusive products. The company's success can be attributed to its ability to acquire smaller suppliers with limited competition, build a portfolio of niche products with high pricing power, and generate increasing free cash flow to reduce debt from acquisitions.

TDG had a strong second fiscal quarter, surpassing expectations with adjusted EPS of $5.98 and revenue of $1.59 billion, driven by the recovery of the commercial aerospace market. The company experienced substantial growth in commercial OEM and aftermarket revenues, with improved EBITDA margins. Defense sales also provided a boost, with positive future defense order activity expected.

Furthermore, TDG acquired the Calspan Corporation, expanding its aftermarket-focused aerospace and defense development and testing services. The company's M&A pipeline appears favorable, and the outlook for acquisitions remains positive.

While TransDigm has a significant amount of debt, it has hedged most of its interest rate risks and has no debt maturities until 2026. The company's balance sheet remains stable despite the high-rate environment.

Although the valuation is currently elevated, with TDG trading at 19x NTM EBITDA, the stock is considered a good buy on a 10% to 15% drawdown.

Investors interested in TransDigm may consider waiting for a correction before entering a position.

For further details see:

TransDigm Is A Superior Aerospace Stock