TDG - TransDigm: Rating Upgrade As Growth Outlook For FY24 Is Stronger Than Expected

2023-12-18 14:30:09 ET

Summary

- TransDigm Group's stock price reached an all-time high of $1015 after a strong 4Q23 and better-than-expected growth outlook for FY24.

- The company reported beating consensus estimates for revenue, EBITDA, and EPS in 4Q23, accompanied by a $2 billion special dividend.

- Positive macroeconomic indicators, strong bookings growth, and a continuous recovery in air travel support a sustained growth outlook for TransDigm Group.

Investment Action

I recommended a hold rating for TransDigm Group ( TDG ) when I wrote about it the last time , as I believed the valuation was too high. That recommendation played out well from August to October, when the stock traded down by more than 10%. What I did not expect was a very strong 4Q23 that drove a sharp rerating in valuation, leading to an all-time high share price of $1015. Based on my current outlook and analysis of TDG, I am revising my rating to buy as the growth outlook for FY24 is better than I expected. The strong 3Q23 also proved that growth momentum is not slowing down. With this revised growth outlook, even if valuation re-rates to the historical average, the upside is still attractive. TDG's balance sheet also remains strong, suggesting more opportunities for M&A.

Review

TDG fared very well for the 4Q23 quarter , beating consensus on all major fronts: revenue, EBITDA, and EPS. FY24 guidance also came in above consensus estimate. The strong quarter was accompanied by a new $2 billion special dividend. In details, TDG reported 4Q23 EPS of $8.03 vs. consensus of $7.55. The strong EPS performance was driven by strong organic revenue growth of 19%, supported by Commercial aftermarket growth of 27%, Commercial OEM growth of 22%, and Defense growth of 15%. EBITDA grew consistent with revenue strength, touching $963 million, which reflects a margin of 52%, an increase of 220bps. Looking ahead, management provided the initial FY24 information:

- Revenue guidance range of $7.48 to $7.68 billion, exceeding consensus pre-results expectation of $7.4 billion;

- EBITDA guidance range of $3.87 to $4.01 billion;

- Adjusted EPS of $31 to $32.94.

I remain positive on all of TDG's primary end markets and expect the strong growth to continue into FY24. Firstly, I view the strong bookings comment (refer to the 3Q23 earnings call) for each end market as a leading indicator of growth. Recall that TDG saw similar strength in bookings last year, and FY23 growth performance followed through nicely.

Secondly, TDG should see a favorable macro environment in FY24 as the world's largest economy (the US) appears to be recovering from the painful inflationary and high rates of 2023. Suppose the Fed cut rates as hinted; this would be a major boost to the economy, which should flow through to consumers' discretionary wallets as the cost of living comes down (leading to more potential air travel).

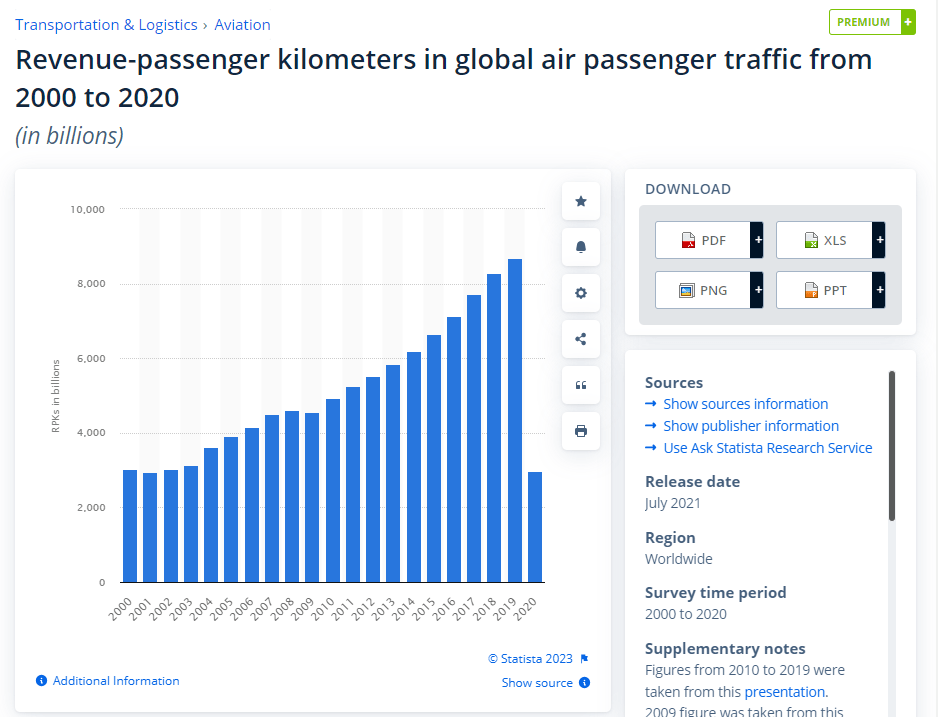

Thirdly, according to the International Air Transport Association ((IATA)), passenger growth continues to recover steadily with no major slowdown in momentum. Notably, global international revenue passenger kilometers (RPKs) are still below the CY19 level, indicating that we are far from reaching the normalized level yet. As consumers' discretionary income improves (if the US economy recovers as the Fed indicates), I expect RPK to continue growing. Historically, TDG aftermarket volume is well aligned with global RPK growth, and I expect the trend to continue as nothing structurally has changed.

IATA IATA

Management comments also suggest that overall TDG is still far from a normalized level, as volumes are still modestly below 2019 levels today. While they noted Freight and business aircraft are above pre-COVID levels, the remaining business (passenger and interiors) is still down 15+%. As such, if we think about where the industry should have been if COVID did not happen, TDG still has a large room to recover. This is especially considering the historical passenger market strength (RPK growth has been 1 way up since the 2000s), four years of GDP growth, and the potential recovery of Chinese travelers. Air traffic should continue to grow from here on out, thanks to all of these factors.

{kind=link}

Lastly, I like the $1.4 billion acquisition of CPI International's Electronic Device Business ((EDB)). This aligns nicely with TDG's business model from a business standpoint. Approximately 70% of EDB's revenue comes from the aftermarket, and nearly all of its revenue comes from proprietary products. Given the current level of uncertainty surrounding the outcome, I will not be factoring this into my estimates. Assuming, however, that it does pass, TDG will have a chance to implement its playbook (changing prices, cross-selling, etc.) and increase growth and margin.

On the point of margin, management laid out their FY24 guidance for EBITDA margin to be at 52% at the midpoint, which implies an improvement of 50 bps on a year-over-year basis. At first glance, this appears to be a weak guide, as Calspan is a headwind to margin. However, my sense is that management might be too conservative in their guidance, as the adj EBITDA margin rate for 2H23 was already at 52.2% and most of this period already included Calspan.

In terms of balance sheet and capital allocation, TDG ended the quarter with a net debt of ~$16.4 billion, and if the EDB acquisition goes through, net debt should touch $20 billion. This implies an FY24 net debt to EBITDA leverage of around 5x. This is still a major improvement compared to the historical leverage ratio, and as such, I do not see the business facing any liquidity issues. Importantly, if the Fed really cuts rates, TDG should see a positive interest expense tailwind over the coming quarters. TDG should also have no issue reducing leverage as the business continues to generate more than $1 billion of FCF and is expected to generate ~$4 billion of FCF in FY24/FY25 based on consensus estimates.

Valuation

Author's work

With the strong 4Q23 performance and visible growth drivers, I am pushing out the growth deceleration into FY25 and FY26 (I modeled the slowing to be FY24 and FY25 previously). My FY24 assumption is based on management guidance, which has historically been accurate. Since FY13, reported revenue has generally been in line with guidance (<1% difference on average). As for margin, I believe management is downplaying expectations as the 2H23 EBITDA margin is already above guidance. However, for conservative sake, I assume the same margin as guidance and expect expansion in FY25. Previously, I thought that the TDG valuation was too high; however, with the revised outlook, I think the valuation is now attractive, even if it reverts back to the historical average . There is a good chance for valuation to sustain at 17x forward EBITDA, and if so, the upside in the near term could be higher than I expect.

Risk and Final Thoughts

Integration risk remains an inherent risk to TDG's M&A-driven strategy. I acknowledge that TDG management has strong competency in integrating their acquired targets. However, that does not eliminate this risk. A series of bad acquisition and integration hiccups could damage the management reputation and the credit that the market gives to the management team. All in all, I am upgrading my rating for TDG to a buy due to the stronger-than-anticipated growth outlook for FY24. Looking ahead, positive macroeconomic indicators, bookings growth, and continuous recovery in air travel should sustain growth for longer than I originally expected.

For further details see:

TransDigm: Rating Upgrade As Growth Outlook For FY24 Is Stronger Than Expected