TMDX - TransMedics: Transforming The Landscape But No Rush To Buy

2023-10-18 09:19:54 ET

Summary

- TransMedics is a medical tech company focused on organ transplants in the US.

- TMDX looks set to be a key enabler in raising the transplant volumes carried out in the country.

- TMDX has experienced strong topline growth and has the potential for continued growth, but short-term risks and technical considerations warrant some caution.

The Underlying Thesis For Pursuing TMDX

TransMedics Group ( TMDX ) is a small-cap medical tech business that is currently making waves in the organ transplant space in the US. The country is witnessing a surge in chronic illnesses and when these diseases are in their final stage, organ transplants can often prove to be the only option at saving patients. Studies have shown that every other year, the number of organ transplants being carried out on the domestic shores continues to hit new annual records, with the current run rate pointing to 4% annual growth p.a. We’d like to think that if a company like TMDX gets its act together, one could expect a manifold surge in the transplant growth rate. Why so?

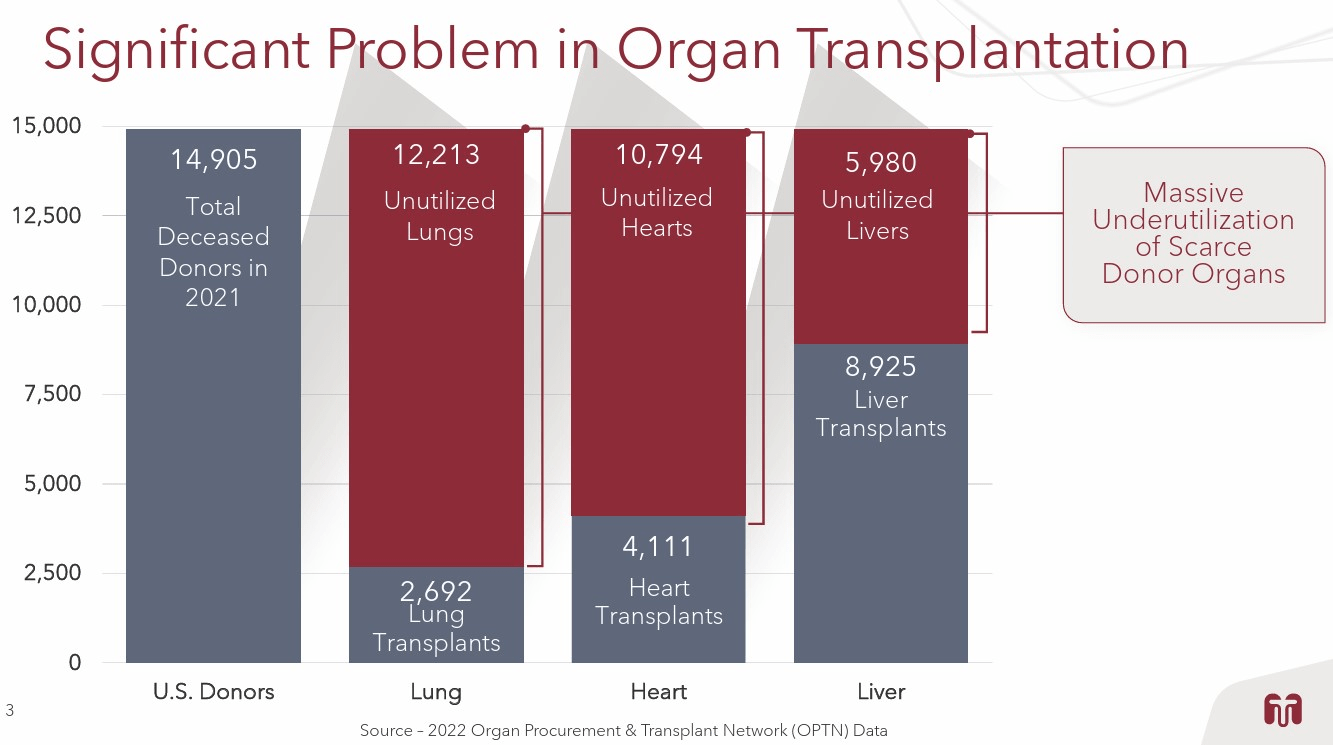

Well, the demand for organ transplants has always been resplendent, but there are massive deficiencies in the current system which is heavily tilted to the cold storage manner of organ preservation which often leads to significant underutilization and wastage of the precious organs. The image below helps contextualize the gap that exists due to the flawed cold storage system.

{kind=link}

{kind=link}

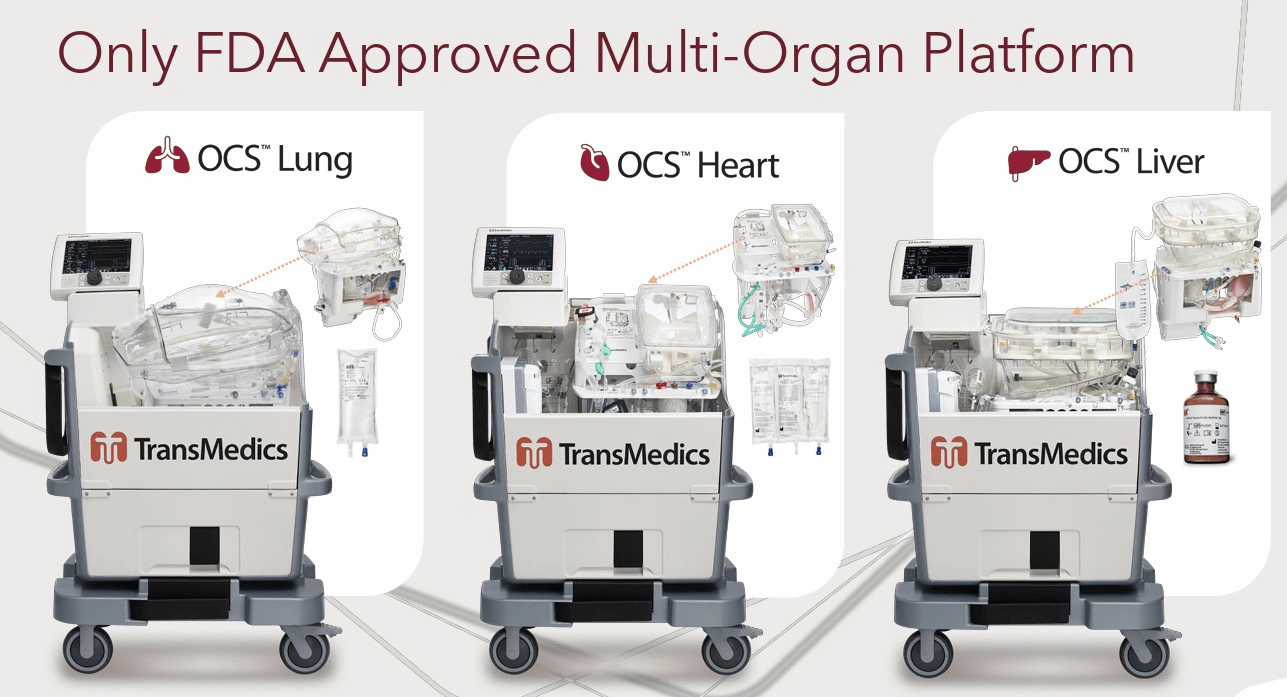

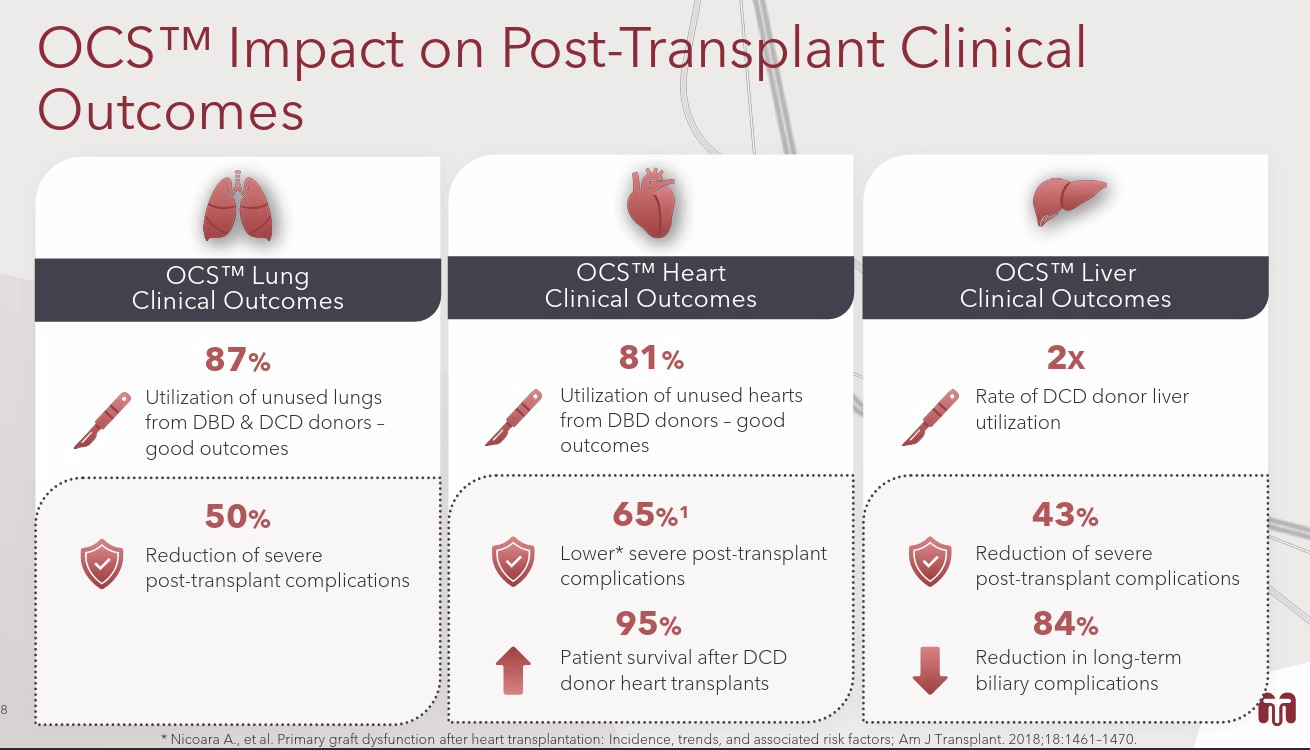

TMDX’s proprietary portable product- the Organ Care System ((OCS)) does not follow cold storage but is rather based on warm perfusion technology, which does a much better job of replicating near-physiologic conditions for these organs, once they leave the human body. The portability factor also helps bring down the risk of ischemic injury. Since the organs are maintained in a better state, the clinical outcomes after a transplant too are a lot more encouraging.

{kind=link}

Supplementing the core OCS product, TMDX also operates a National OCS program (NOP) that plays an efficient role in the entire organ sourcing, retrieval, and organ management process. The combination of OCS and NOP together has the potential to really transform the volumes of transplants carried out by potential transplant centers.

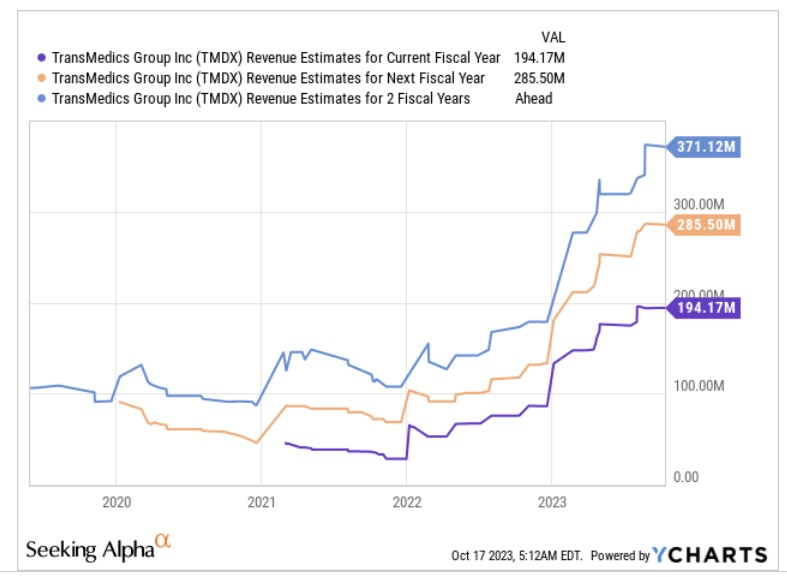

All in all, the strong need for TMDX’s proposition in the market can be gleaned through the degree of topline growth that this business has been generating off late. Last year, the topline grew at a whopping 193% YoY, and given such a mammoth base effect of growth, one wouldn’t normally expect a company to come back and do it again two years on the trot. However note that in Q1 and Q2, the topline has grown at 162% YoY and 156% YoY respectively, and the company now looks set to close FY23 with expected topline growth of 108% (based on the consensus figure of $194m)!

{kind=link}

It would certainly be asking for the moon if you expect TMDX to deliver triple-digit topline growth for the third year running, but if you consider a medium-term time frame (from FY22-FY25) you could still be looking at rather resilient topline CAGR of 58%.

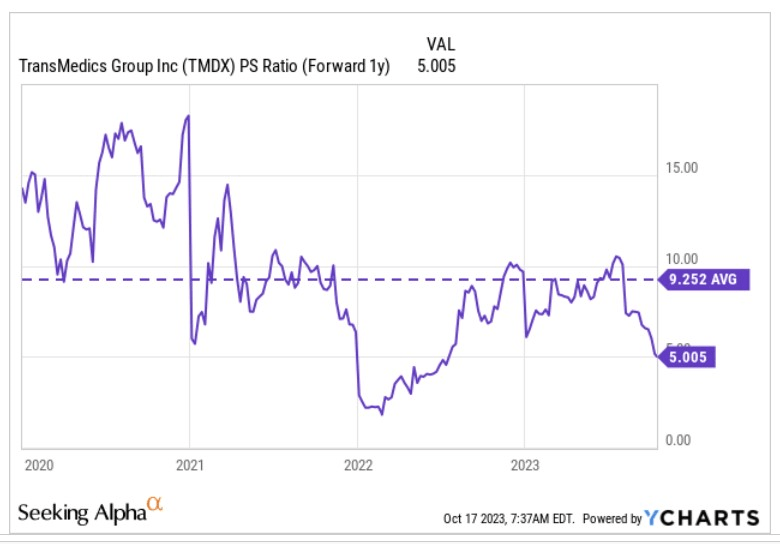

Given this ferocity of medium-term earnings growth, we think the forward price-to-sales multiple of 5x looks very cheap. The affordability quotient becomes harder to ignore when you consider that the long-term forward average is around 45% higher at 9.2x

{kind=link}

Risks

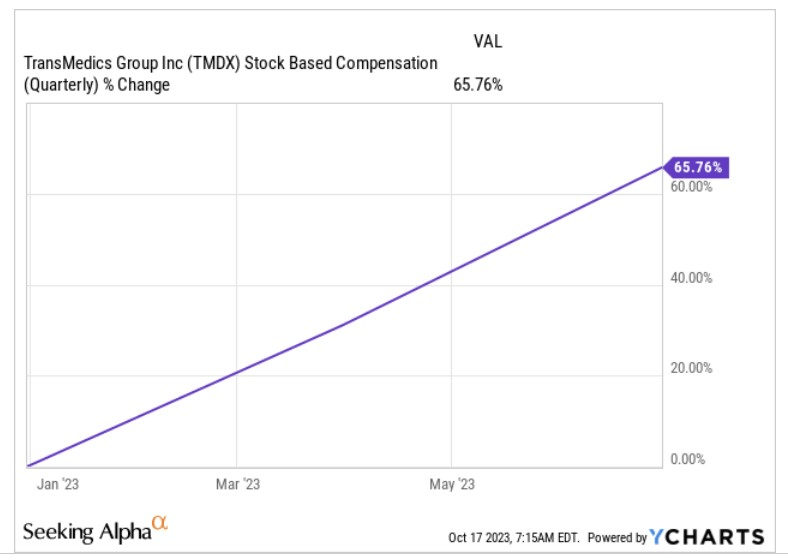

Whilst the long-term story looks promising, the next few quarters could be a tad dicey from an operating leverage perspective, as TMDX seeks to deal with integration challenges linked to the acquisition of charter flight operator- Summit Aviation . Already TMDX is not profitable at the operational level, and in H2, the cadence of OPEX should step up as they integrate this acquisition. Besides this, management also stated that they would be ramping up their clinical and surgical staffing related to NOP services over the next 18-24 months. Now what this also means is that the future risk of dilution linked to stock-based compensation will only snowball. In the past year itself, it has already grown by 65%!

{kind=link}

TMDX did also confirm that in Q2 they lost out on the ability to fulfill certain business volume (particularly in the lung domain) and reach certain locations, due to the limited availability of 3rd party fleet. They also implied that this trend may well linger stating that they could have “additional cases in the second half of the year that go uncovered”.

Capital requirements too could be a major drag on the company’s financial resources (recently bolstered by a convertible debt offering) as they plan to purchase additional planes besides the fleet they’ve procured from Summit Aviation. TMDX’s goal is to have 10-15 planes by operation in H1-24, and each plane typically costs $10-$12m (TMDX does not plan to lease the planes), so you could be potentially looking at capital costs of $100-$180m through H1-23.

Of course over time, with a dedicated fleet that can travel mid and long-distance, TMDX will be really well-positioned to garner ample volumes, but it's fair to say that in the short term, TMDX will likely be adopting a defensive posturing.

Closing Thoughts- Technical Considerations

The conditions on the charts suggest that investors don’t necessarily have to be too enthusiastic to buy into this story now.

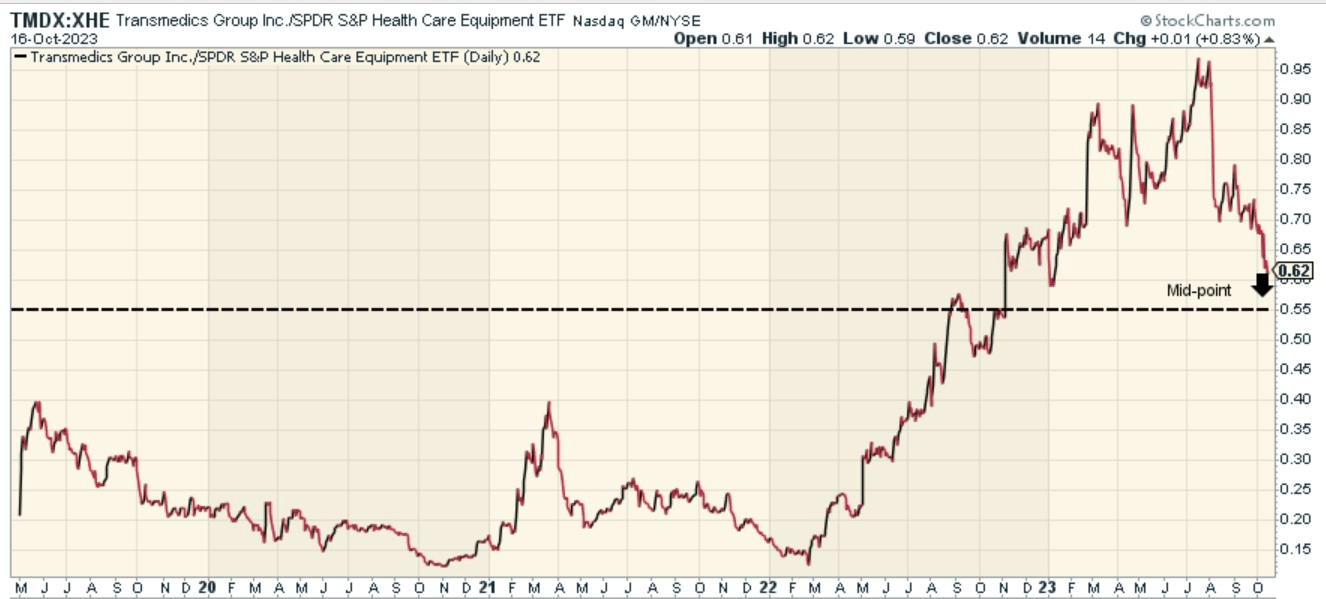

Firstly, if one were fishing for beaten-down names within the medical equipment universe, the TMDX stock is unlikely to be one of the first names on the shopping list. The image below highlights how the latter’s relative strength versus its peers from the SPDR S&P Health Care Equipment ETF ( XHE ) is still trading above the mid-point of its trading range. For the uninitiated, when contemplating a long position, we prefer gravitating to opportunities where the relative strength ratio is overextended to the downside and could benefit from some mean-reversion.

{kind=link}

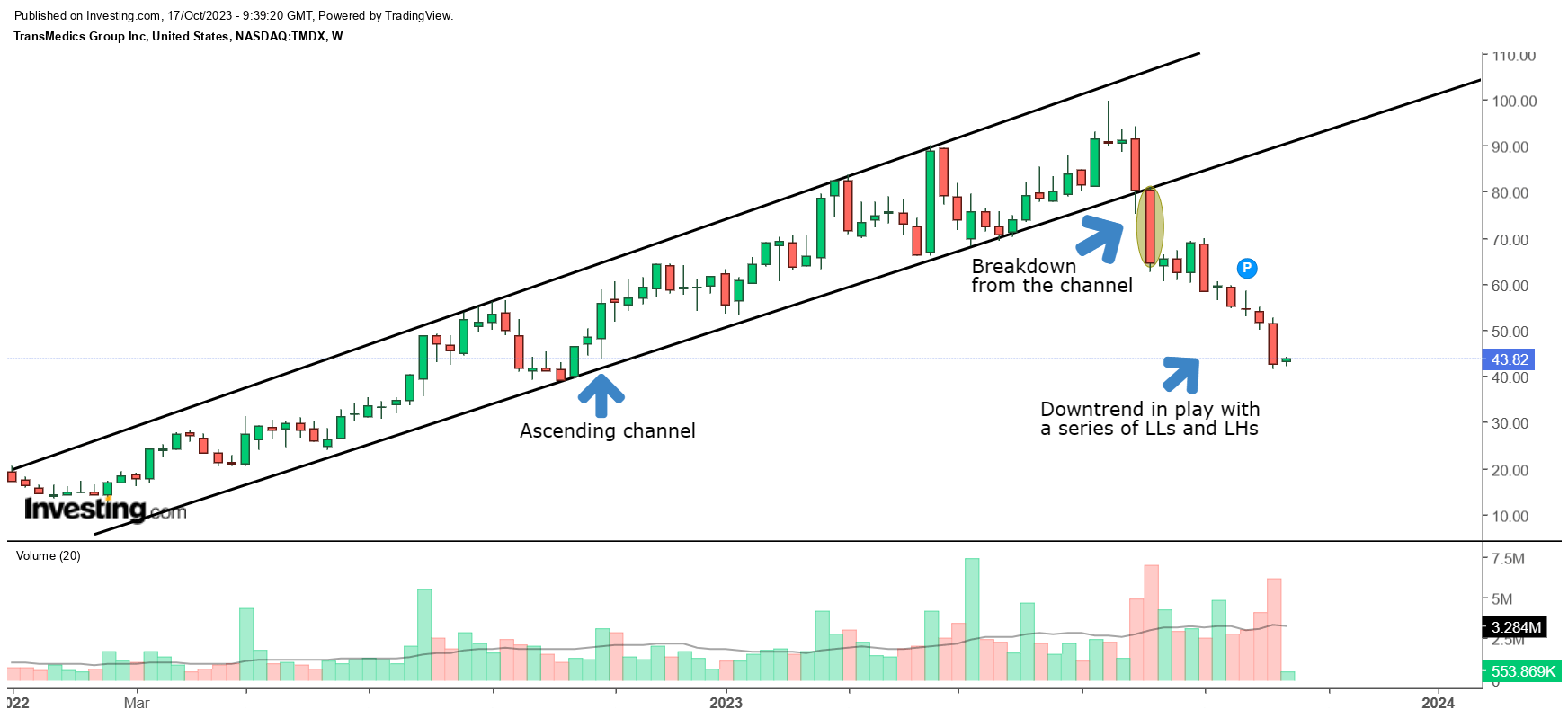

Recent developments on TMDX’s own weekly chart too don’t fill us with a great deal of confidence.

{kind=link}

For around 20 odd months until August this year, the TMDX stock had been trending up in the shape of a resolute ascending channel. However, since late July, we’ve seen the onset of a strong downtrend, as well as a breakdown from the lower boundary of the channel.

The relentless selling has persisted well into last week, and until we see the end of the sequence of lower lows (LLs) and lower highs (LHs) in the weekly price action, we don’t believe it would be advisable to commence a long position in this counter.

{kind=link}

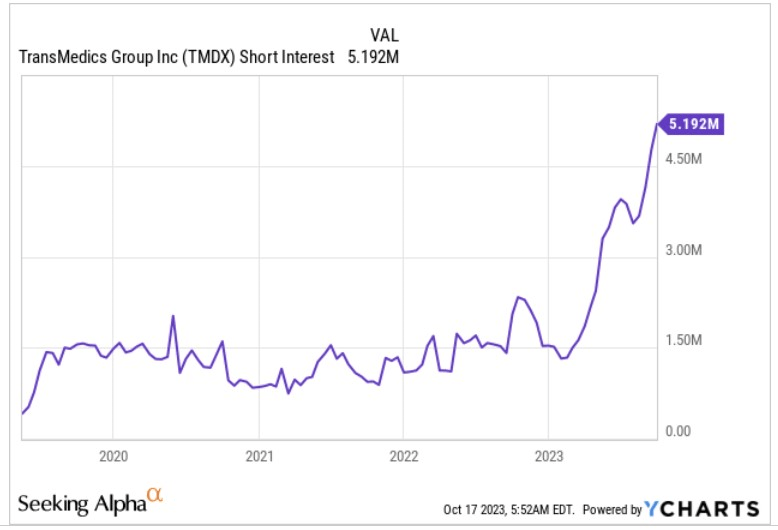

We also feel some caution is warranted as there does not appear to be any attrition in the strong short-selling momentum, even after a +50% drop in the share price since mid-July. If anything, short-selling momentum only continues to deepen at lower levels, with the short interest currently at record highs.

All in all, given that the company is going to witness a spike in the OPEX base and focus on integrating the Summit acquisition through the end of this year, we don’t see a need to make a desperate lunge to own TMDX any time soon. The stock is a HOLD.

For further details see:

TransMedics: Transforming The Landscape, But No Rush To Buy