ODFL - Transportation Excellence: In 2024 I'm Watching Old Dominion Freight Line

2023-12-12 11:39:38 ET

Summary

- Old Dominion Freight Line has a strong track record of growth, with a 330% return over the past five years.

- The company has a superior service and pricing power in a competitive market, with impressive quality awards and on-time service ratios.

- ODFL has seen some declines in LTL metrics due to economic challenges, but its efficient operations and financial health make it a compelling investment.

(A Lengthy) Introduction

It's time to do two things:

- Assess the health of the American logistics industry.

- Discuss why I'm looking for a dip to buy one of my favorite transportation companies on the market, Old Dominion Freight Line ( ODFL ) .

I started covering the company behind the ODFL ticker more than five years ago. Unfortunately, I wasn't smart enough to start a (meaningful) long position back then.

Over the past five years, ODFL has returned more than 330%, beating the S&P 500 and the iShares Transportation ETF ( IYT ) by an enormous margin.

My most recent article on the company was written on August 17, when I discussed the company's impressive business model.

Although I usually stay away from industries like car manufacturing and trucking due to their cyclical nature, low entry barriers, and capital-intensive natures, I like what ODFL is bringing to the table.

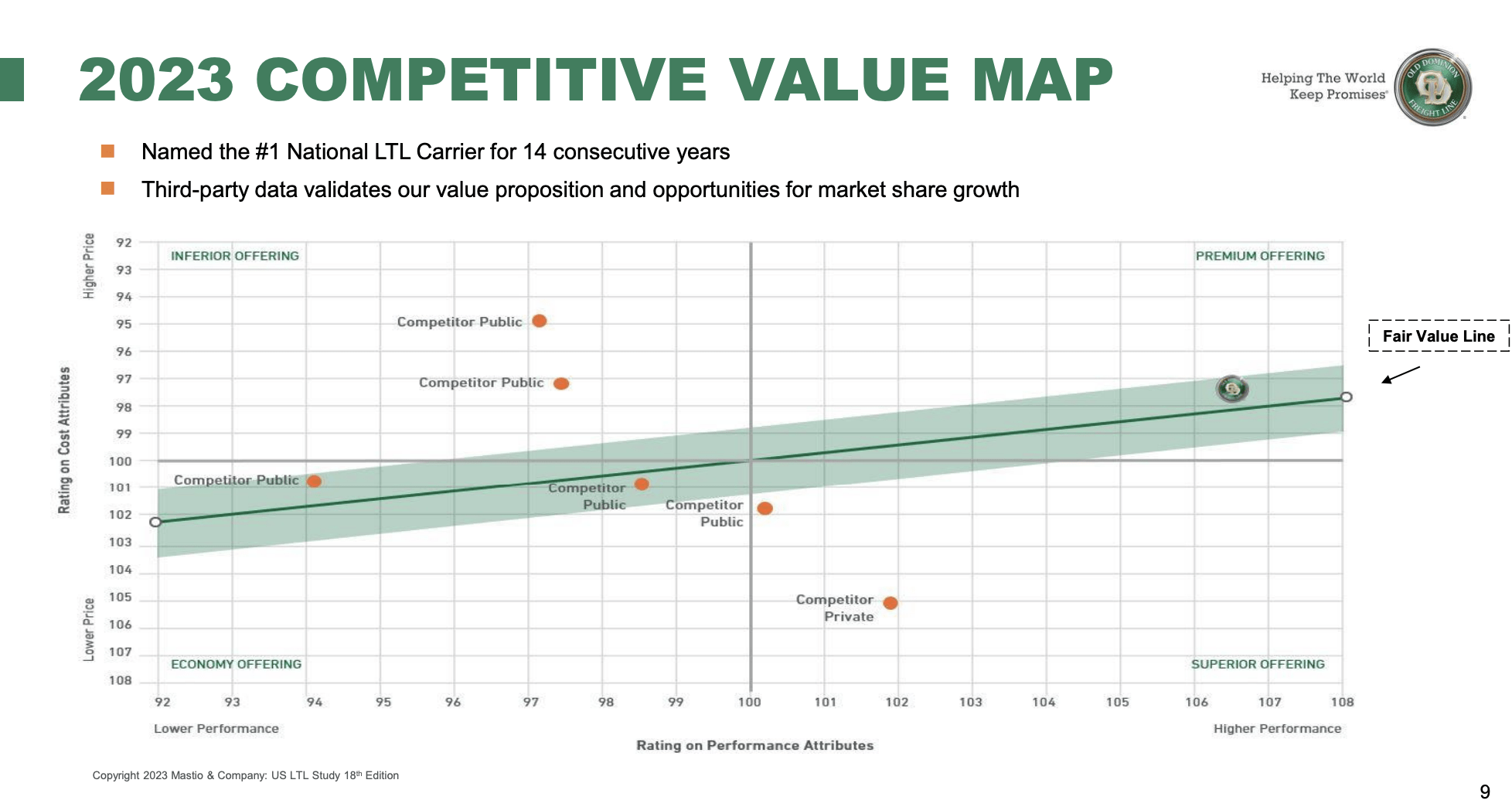

Like no other company in its industry, ODFL has perfected the art of becoming very competitive at a great price point.

While ODFL charges a slightly higher price than some of its competitors, it does have a superior service, giving it a tremendous position with pricing power in a very competitive market.

{kind=link}

Old Dominion Freight Line

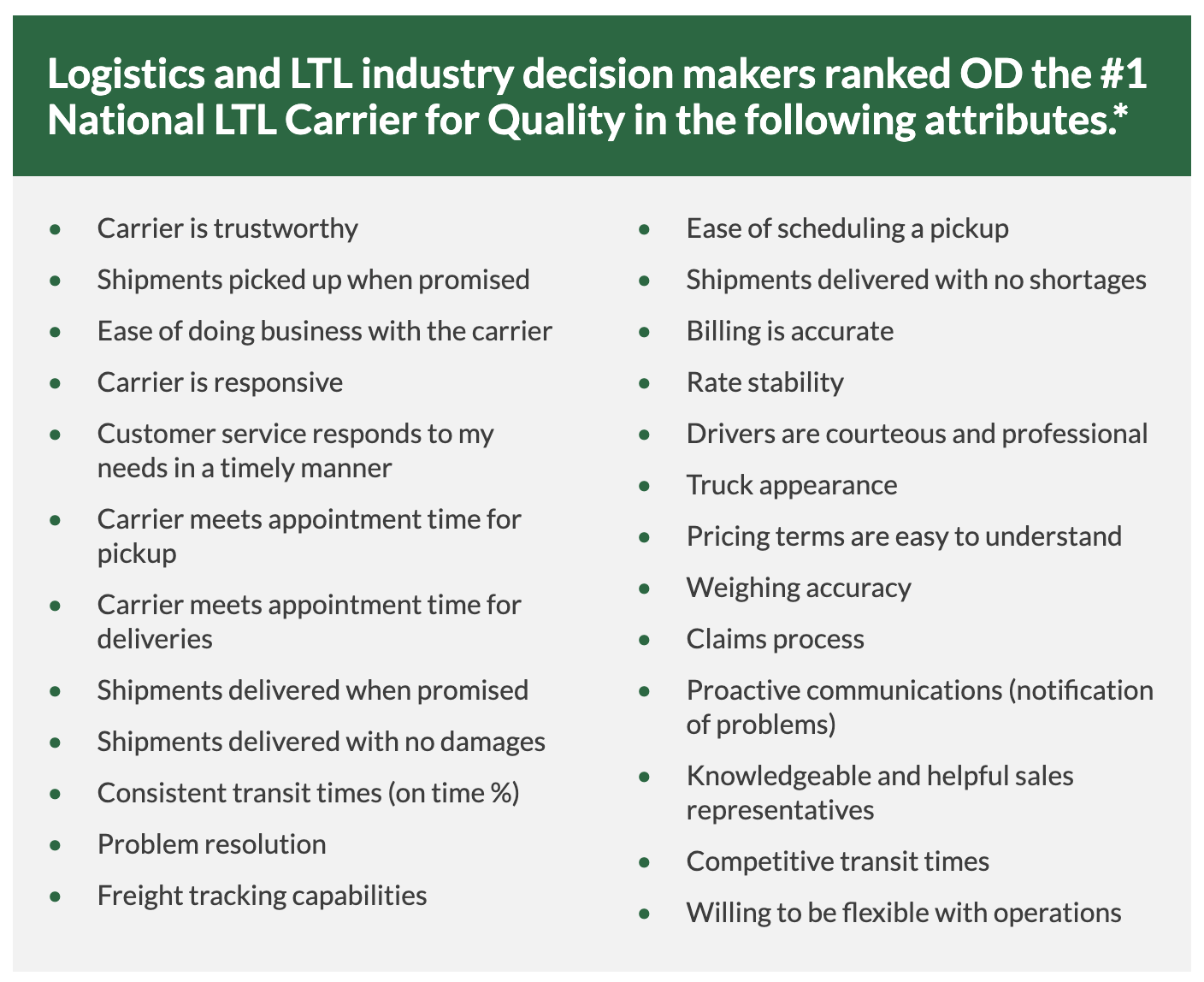

For example, the company has won the Mastio Quality Award for 14 straight years, and it has an on-time service ratio of 99% (as of 2022).

{kind=link}

Old Dominion Freight Line

Its cargo-claims ratio has dropped from 1.5% in 2022 to just 0.1% in 2022.

As a result, the company has grown its revenue at an annual compounding rate of 12.8% since 2002 - almost entirely organic!

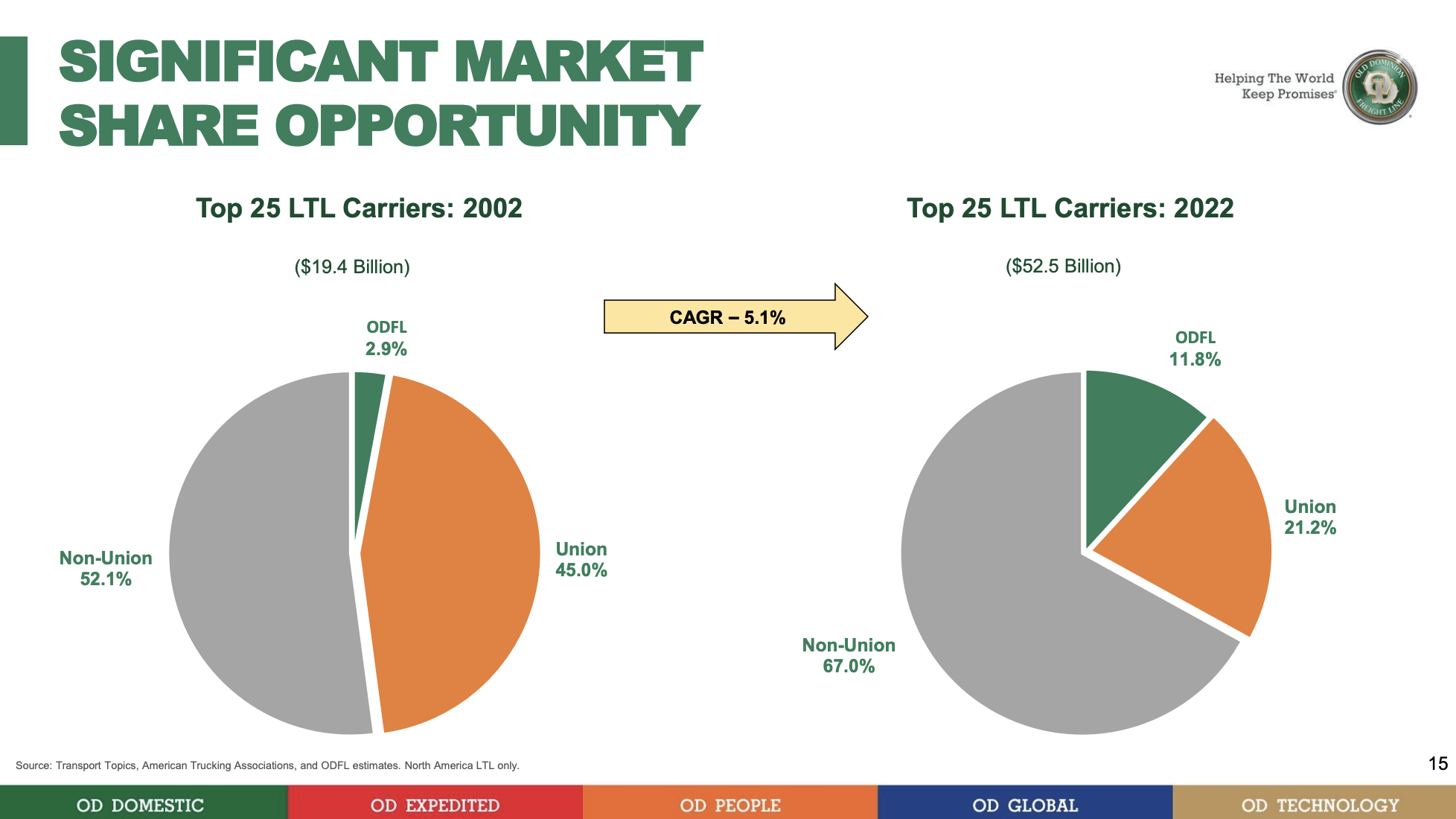

The company's dense network of close to 260 service centers has allowed it to reach almost every part of America and grow its market share from 2.9% in 2022 to roughly 12% in 2022.

{kind=link}

Old Dominion Freight Line

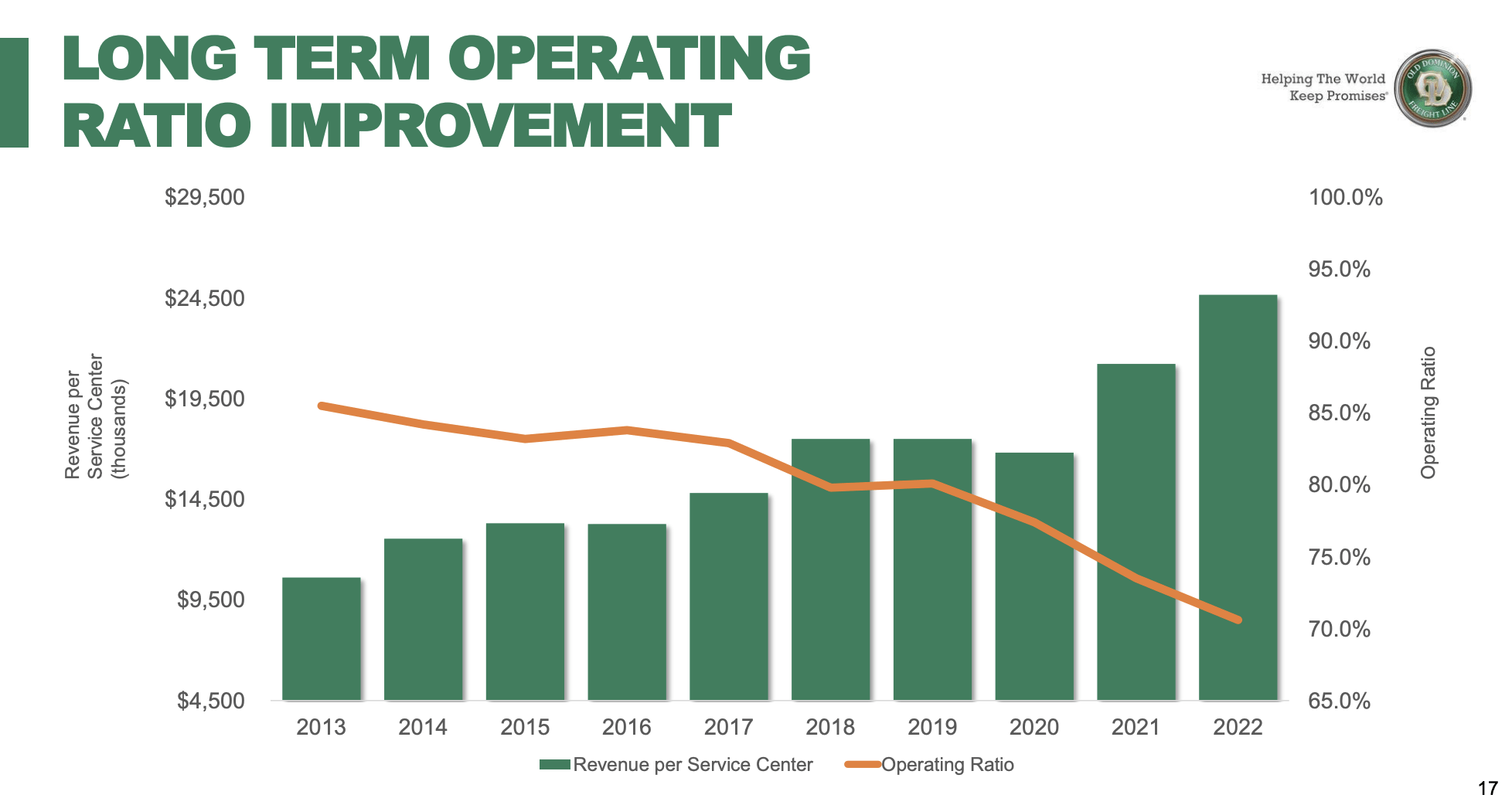

On top of that, the company has done the impossible. It has lowered its operating ratio from more than 85% in 2013 (which was already a great result!) to roughly 70%.

The operating ratio measures the percentage of revenues it costs to run the business - the lower, the better.

Generally speaking, railroads have the lowest ORs due to their more efficient operations. Most trucking companies are somewhere between 90% and 100%, with regular increases to more than 100% during recessions.

{kind=link}

Old Dominion Freight Line

At this point, ODFL is as efficient as a very inefficient railroad, which is, for the lack of a better word, mind-blowing.

It is also financially healthy. The company is expected to end this year with more than $200 million in net cash, meaning ODFL has more cash than gross debt.

Having said that, the company's stock has run into some headwinds caused by slower economic growth.

After all, despite all the good news, the less-than-truckload ("LTL") business remains highly cyclical and dependent on industrial production.

So, let's take a closer look at current developments!

Semi-Bad News From Old Dominion Freight Line

On December 5, the company reported its most recent transportation numbers. As one can imagine, the numbers weren't that great, as this is what the leading ISM Manufacturing Index looks like:

The index has been in a steady downtrend since early 2022 and consistently below the neutral 50 level for roughly a full year.

Going back to Old Dominion, the company experienced a 2.9% decline in LTL weight per shipment for November, partially balanced by a 0.6% rise in LTL shipments per day.

The good news is that for the quarter-to-date period, there was a noteworthy uptick in LTL revenue metrics.

Specifically, LTL revenue per hundredweight increased by 3.1%, and when excluding fuel surcharges, there was a substantial 7.6% surge compared to the same period last year.

Marty Freeman, the President and CEO of Old Dominion, acknowledged the revenue decline, attributing it to the persistent softness in the domestic economy (no surprises here).

However, Freeman expressed satisfaction with the ongoing improvement in yield metrics and a slight increase in LTL shipments per day.

He emphasized the company's commitment to delivering superior service at a fair price and highlighted the strategic approach to yield management as a fundamental element of their long-term plan.

In other words, the company is doing what it is doing best, offering a great service, regardless of the economy. That's the best way to grow the business while others may struggle.

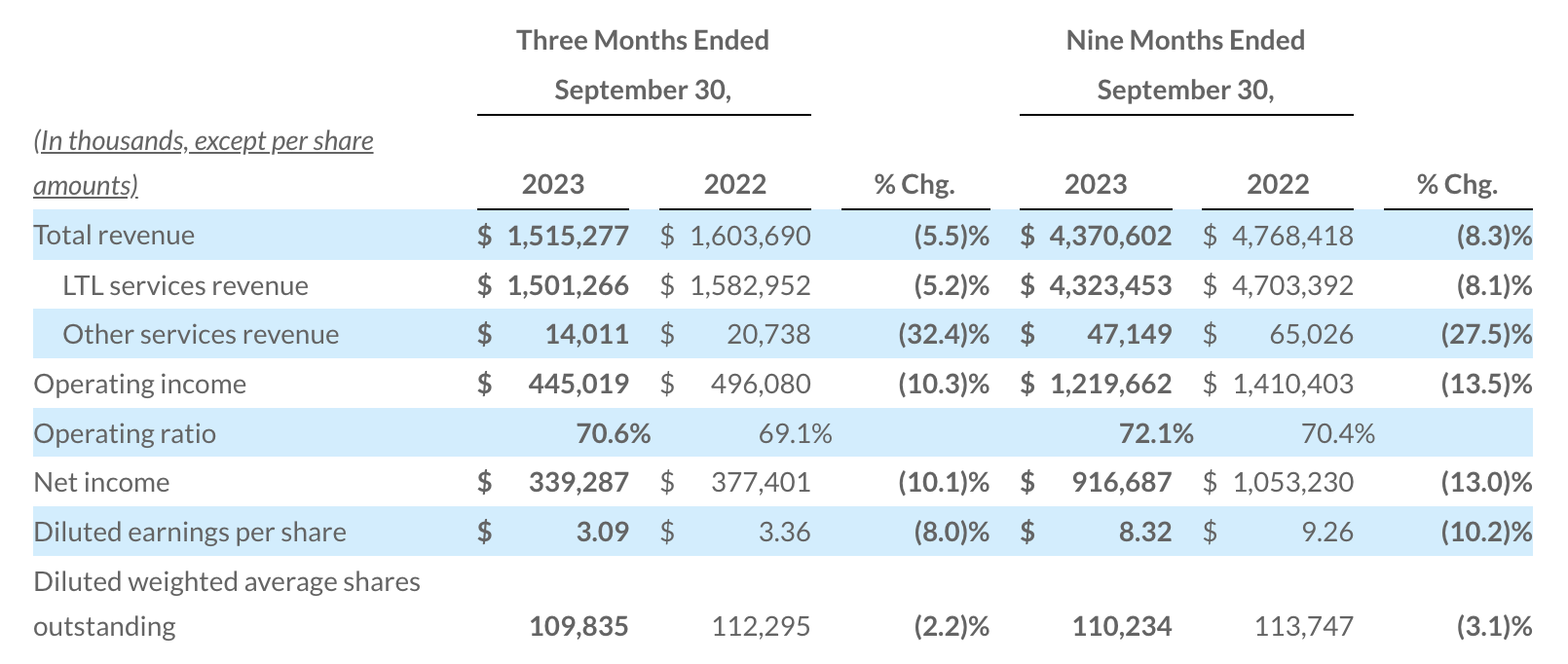

In the third quarter, the company saw a 5.5% decrease in its revenue, attributed to a 6.9% decrease in LTL tons per day, partially offset by a 3.1% increase in LTL revenue per hundredweight.

{kind=link}

Old Dominion Freight Line

However, on a sequential basis, revenue per day for the third quarter increased 8.9%, with LTL tons per day and LTL shipments per day showing positive growth compared to the second quarter of 2023.

Meanwhile, the operating ratio increased to 70.6%, driven by an increase in overhead costs as a percentage of revenue. Operating efficiencies partially offset this increase, and efforts were made to control discretionary spending.

Although the operating ratio increased, 70.6% is a phenomenal number.

So far, these numbers are mixed.

On the one hand, they are somewhat bad, as we're clearly in a different growth environment.

On the other hand, ODFL still has strong pricing power and sequential improvements.

Now, it's up to the industry.

In the most recent Logistics Managers Index ("LMI") report , for the month of November, a mixed picture was painted.

Despite a slight contraction in the overall LMI (-7.1), the North American economy remains resilient.

Logistics Managers' Index

Corporate earnings rebounded in 3Q23, marking the end of the "earnings recession."

However, global economic variations persist, with challenges in the Panama Canal impacting fuel prices in Asia. China faces economic challenges, while India sees positive growth trends. Freight distribution patterns are reverting to pre-COVID norms, with potential implications for regional costs and availability.

Moreover, inventory levels contracted (-9.1) in November, aligning with reports from major retailers like Target ( TGT ), Walmart ( WMT ), and DICK'S ( DKS ), emphasizing just-in-time strategies. Downstream retailers lean towards AI-driven inventory management, aiming for dynamic planning and disruption avoidance.

Logistics Managers' Index

With that in mind, according to the report, transportation metrics indicate a slowdown, with overall transportation utilization down (-10.7), but showing downstream expansion.

Transportation Prices show a divergence between upstream and downstream respondents. Transportation capacity is growing, especially downstream, indicating readiness for the ongoing e-commerce growth.

Unfortunately, due to weaker demand and higher capacity, transportation pricing continues to decline (it's consistently below the neutral 50 level).

Logistics Managers' Index

ODFL is in a better spot, as it has stronger pricing power.

Nonetheless, unless we get a sustainable bottom in the ISM index, I do not expect a recovery in the LMI. Nor do I expect a prolonged uptrend in transportation stocks.

But that's OK, as I'm looking to buy high-quality stocks like ODFL on weakness.

Valuation

This is where it gets tricky.

Using the data in the chart below:

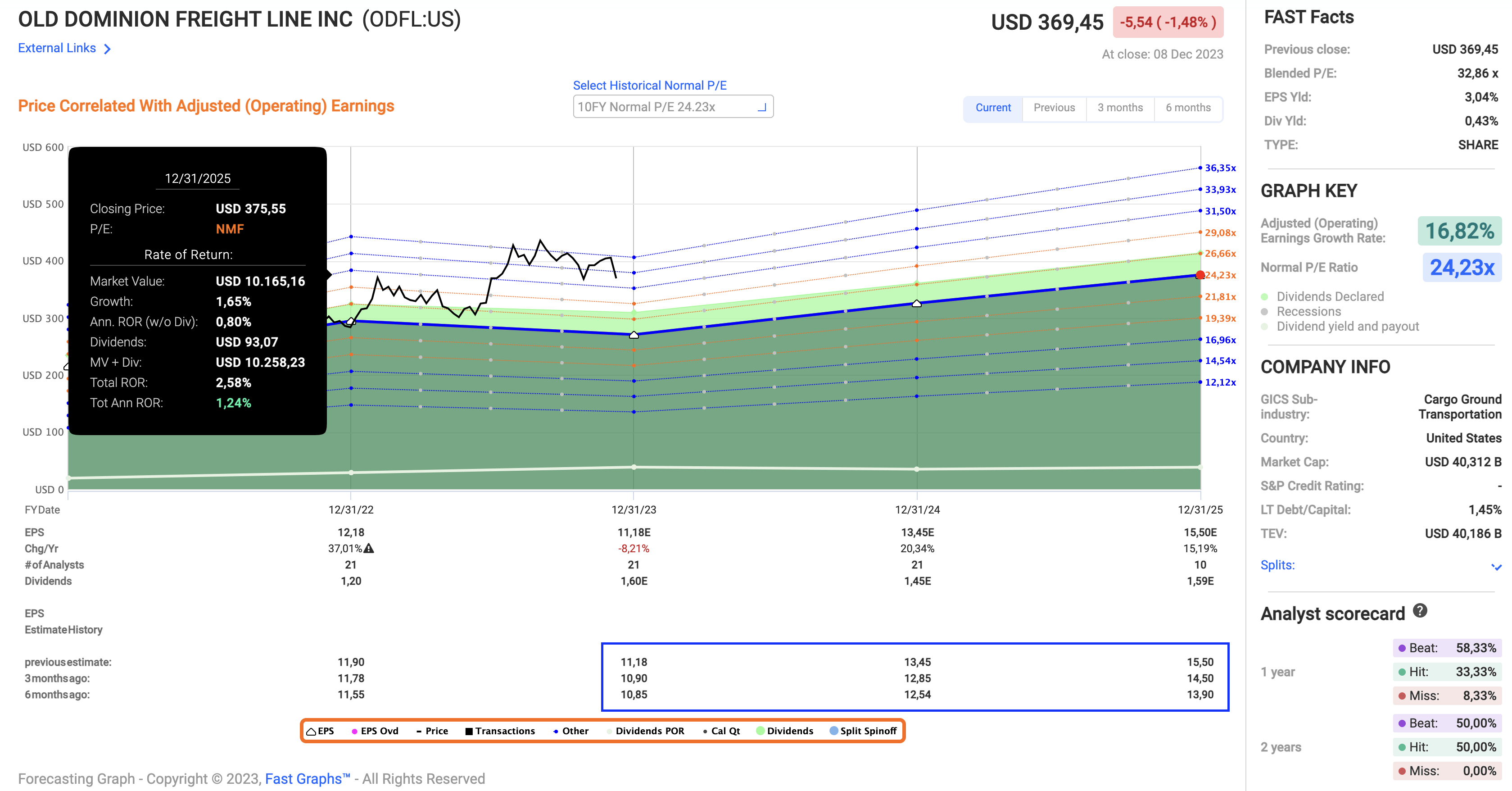

- ODFL currently trades at a blended P/E ratio of 32.9.

- The ten-year normalized P/E ratio is 24.3.

- This year, EPS is expected to fall by 8%, followed by an expected recovery of 20% in 2024 and 15% in 2025.

- Even better, all of these estimates have been hiked significantly over the past six months.

- The problem is that a return to 24.2x earnings with the incorporation of expected growth rates implies an annual return of just 1% through 2025. That's one of the worst numbers I've shown this year.

{kind=link}

FAST Graphs

Although I think the total return will likely be higher, as the market could continue to give ODFL an above-average multiple, I believe that a good buying opportunity is close to $320 per share, or 15-18% below the current price.

While waiting for weakness comes with risks, I am willing to take that risk, as economic challenges could provide us with buying opportunities in 2024.

If I get the chance, I'll likely add ODFL to my portfolio. I truly believe it would go very well with my existing railroad investments.

Takeaway

In a challenging economic landscape, Old Dominion Freight Line stands out with its resilient business model.

Despite recent declines in LTL metrics, ODFL maintains strong pricing power, sequential improvements, and an impressive track record.

The company's commitment to superior service and strategic yield management positions it for long-term success.

While facing headwinds, ODFL's efficient operations and financial health make it a compelling investment, with a potential buying opportunity at $320 per share, offering an entry point for investors seeking quality in the transportation sector.

For further details see:

Transportation Excellence: In 2024, I'm Watching Old Dominion Freight Line