BP - TravelCenters of America: BP Merger Arb Is Too Small Bonds Are A Better Deal

Summary

- BP is acquiring TravelCenters of America for $86 cash. The deal is expected to close by mid-year 2023.

- The narrow discount of only 2% to the closing price suggests the market places a high probability on the deal closing.

- TA's baby bonds offer a better return if they are called around the close date. If not called, they will yield around 8% per year until maturity in 2028-2030.

Together Again

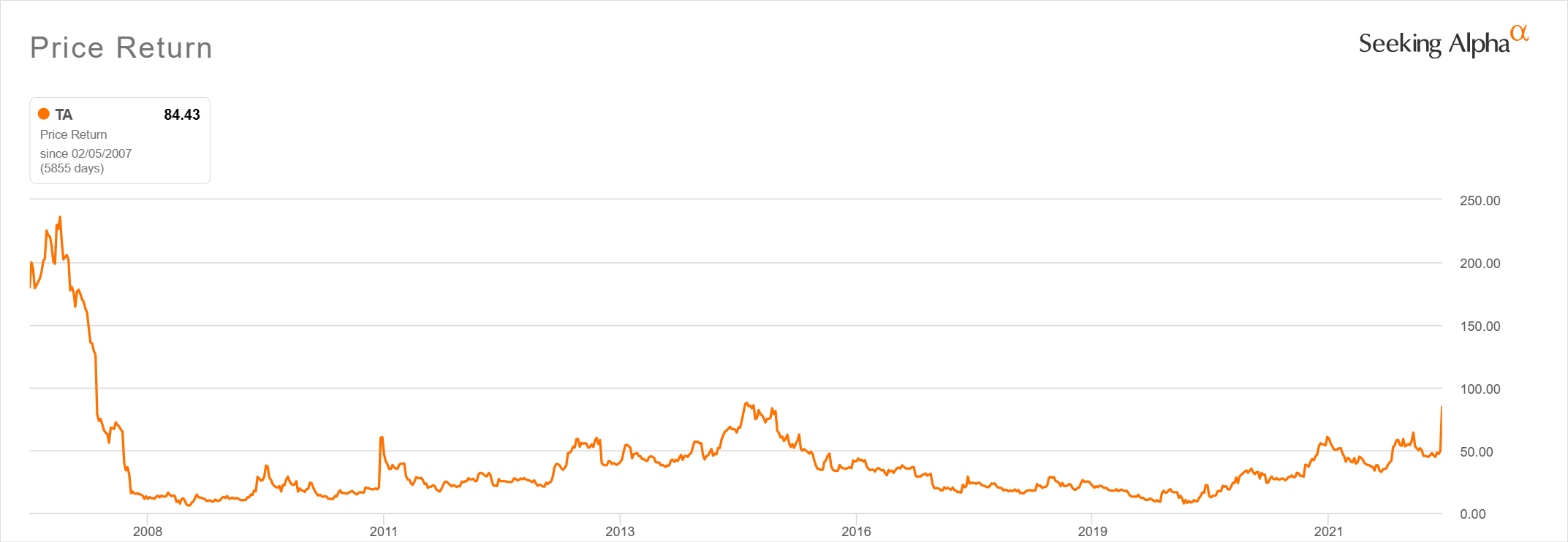

Oil major (BP) recently announced that it will acquire TravelCenters of America (TA) for $86 per share. The deal is expected to close "by mid-year 2023" according to TA's version of the announcement. This was a great windfall for TA shareholders, who saw their stock rocket up 70.8% in a single day. The stock has traded higher than the deal price only for a brief time in 2015 as well as for a few months after the IPO in 2007 (accounting for the effects of a 1:5 reverse split in 2019). Those who bought during the 2008 financial crisis or the March 2020 covid crash scored a 10-bagger, however.

{kind=link}

This deal would be BP and TA's second marriage. The first came when Standard Oil of Ohio bought Truckstops of America in 1984 when BP was still a partial owner of Sohio. BP acquired all of Sohio in 1987, and then went on to sell TA in 1992 in one of its periodic moves away from retail. Over the subsequent 28 years or so, BP engaged in a dizzying array of moves in the retail space in the US, getting rid of locally popular brands like Sohio and Amoco while keeping others like Arco. They also rolled out and rolled back several convenience store concepts like BP Connect, Split Second, and AM/PM. By 2019, most BP stations in the US were owned by third parties, retail having been considered non-strategic for most of this period.

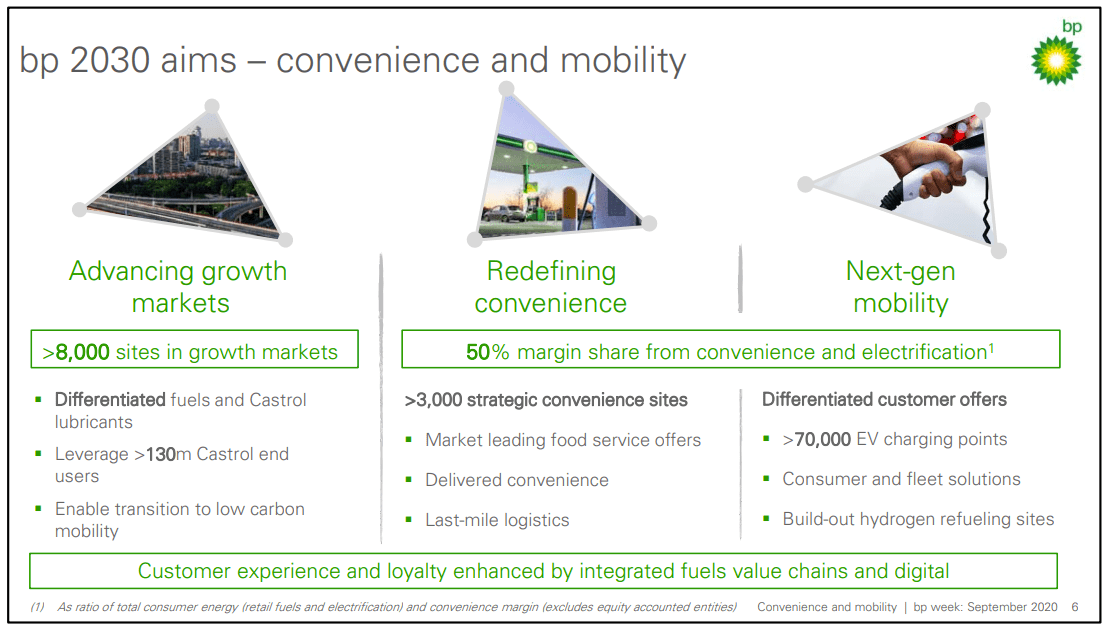

BP's attitude towards retail changed in a big way with the accession of Bernard Looney as CEO in 2020. Growing retail and convenience operations is now a key plank in BP's strategy. Assuming the electrification trend in transportation is real, the strategy makes sense. Retail sites are a prime spot for locating EV chargers. Even the fastest chargers take longer to charge a battery than a gas pump takes to fill a fuel tank. In that case, it of course makes sense to have a nice convenience store where motorists can do some shopping or dining while their vehicle charges.

{kind=link}

Since then BP has been moving slowly back into retail ownership in the US, for example with the acquisition of Thornton's in 2021. The TA acquisition offers BP instant scale in retail and also provides a platform for BP's other strategic planks such as EV charging, biofuels, and hydrogen.

Is It Worth It?

TravelCenters of America has been improving their operations in recent years, as I wrote in September 2022 . They have of course benefitted from high fuel margins but have also improved their non-fuel business, particularly truck service. Still, the biggest financial driver is fuel margins. In September, I estimated a 2023 EPS value for the company at $4.75 based on a $0.20/gallon fuel margin. In the most recent quarter , TA had a fuel margin of $0.227/gallon, and analyst consensus is close to my earnings estimate at $4.87.

A recent article by Daniel Jones recommended buying TA even after the deal announcement, with the thesis that TA still looks undervalued if the deal were to fall through. While I think there is a very low probability of the deal not closing, the existing business looks fairly valued to me.

BP's $86/share bid values TA at a P/E of 17.65. It's hard to find comps with the other US truck stop chains privately held, but if I look at Canadian convenience/fuel chain Alimentation Couche-Tard ( ATD:CA ) we see that it is valued at 16.71 times FY 2023 earnings and 17.16 times 2024. (Their fiscal year ends in April.)

These numbers suggest BP is paying about fair value, or maybe a little above, for TA's existing business. TA's merger announcement states that the $86 price was the outcome of a bidding war between several potential buyers. If the winner's curse applies, that is another indication that the bid is at or above fair value.

Following the implementation of TA's turnaround plan and several quarters of improved operating performance, TA received unsolicited interest to acquire the Company. In response, TA's Board hired financial and legal advisors as part of a formal process to consider a potential sale of the Company. This process ultimately included competitive rounds of bidding from potential buyers that resulted in the transaction announced today.

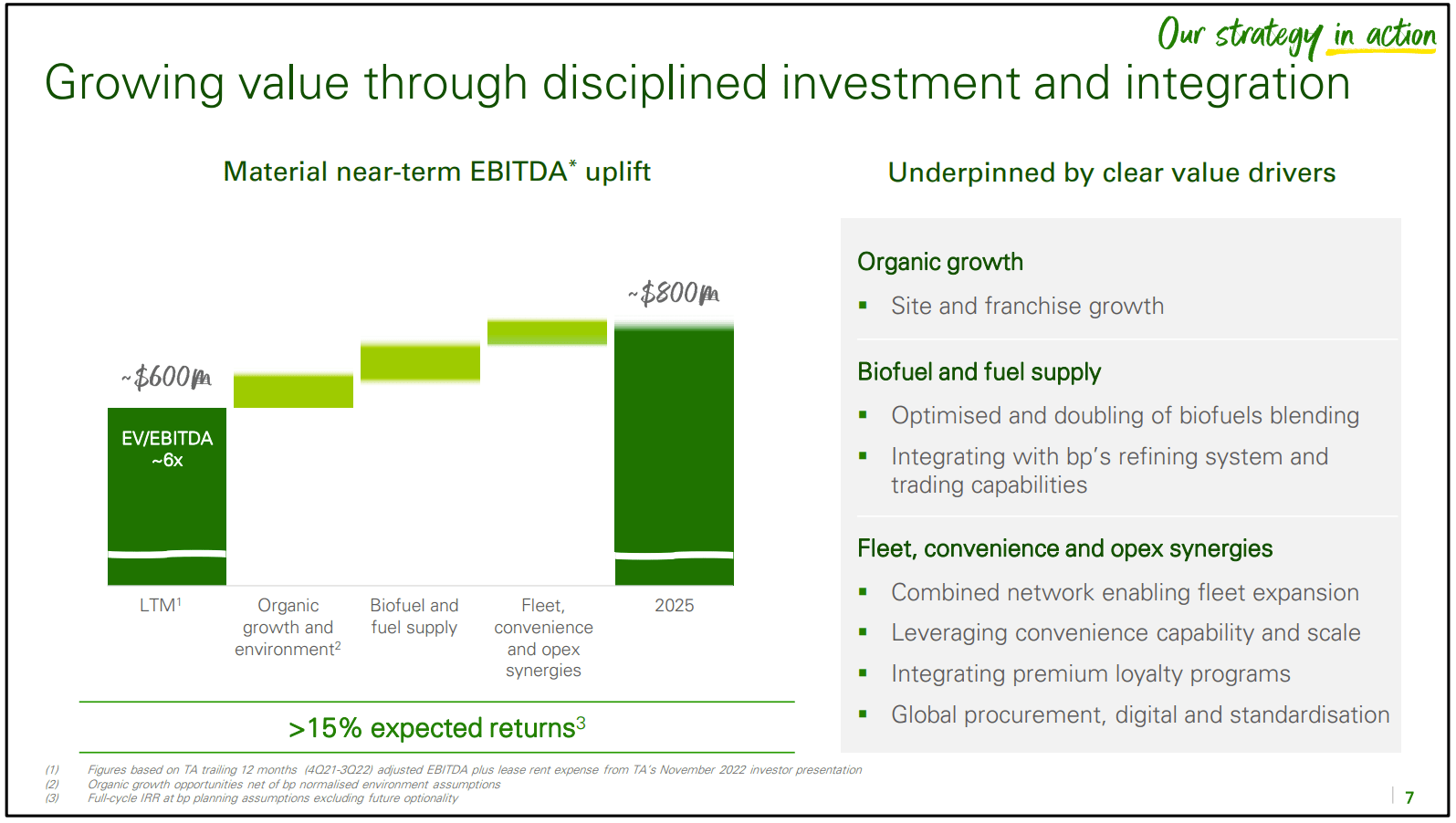

Clearly, the high price paid by BP includes some premium for the synergies BP expects to achieve with its other strategies, as stated in their merger presentation .

{kind=link}

With the stock fully valued and only a 2% arbitrage opportunity between the current share price and the deal value, I would sell TA here. The competitive bidding that already occurred makes it unlikely for higher bids to come in. If we assume closure at 6/30, the 2% translates to an annualized return of 5.6%. 6-month and 1-year T-bills now yield around 5%. Even though the risk of deal failure is very low, the 60 basis point premium over treasuries is not enough to compensate for the unexpected happening. Even a delay in closing of a month or two would make T-bills the better choice.

Look At Baby Bonds Instead

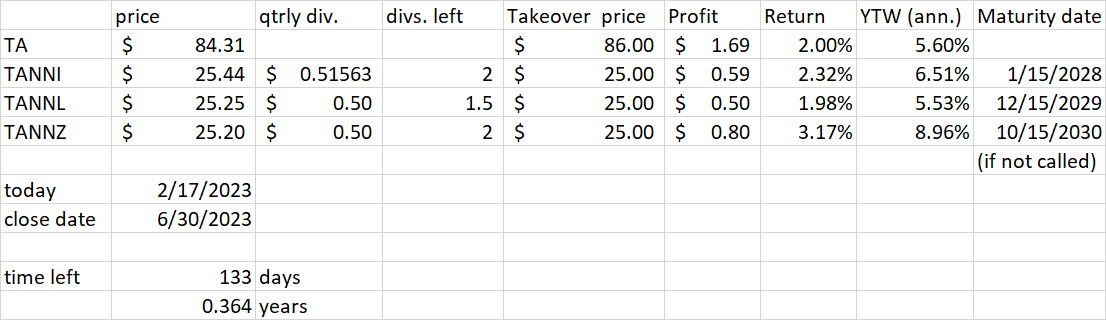

The majority of TA's long-term debt consists of three series of senior notes: the 8.25% due 1/15/2028 ( TANNI ), the 8% due 12/15/2029 ( TANNL ), and the 8% due 2030 ( TANNZ ).

These notes are considered "baby bonds" with a par value of $25. Unlike regular bonds, they trade on the stock exchange the same way as a common stock and pay interest quarterly. You also do not have to deal with accrued interest when you buy and sell them. Each series is now callable at any time at par value of $25. TA has $467 million of cash on its balance sheet and the total par value of these bonds is $330 million, yet the company has not called them despite the high coupon.

It's not clear to me if Section 6.8 of the merger agreement where the company agrees to pay off "certain indebtedness" refers to these notes. Even if it does not, I think it is likely that these notes will be called around the time of the merger. BP has a lower cost of capital and has no reason to go on paying 8% when it has already committed to use 40% of its free cash flow to reduce its own debt.

On the other hand, these notes would amount to only about 1% of BP's total debt, which may be so insignificant that they just let the notes run until maturity in 2028-2030. To find precedent for this behavior, we only have to look at the merger with BP Midstream Partners . BP let this MLP run with its double-digit yield, until 2022 when it could have bought it back a year earlier at prices around 50% lower.

The base case evaluation of these notes should assume they are called on 6/30/2023 at the time of the merger close. In that case, at least TANNI and TANNZ look like they would produce a better return than TA stock. If the notes are not called, they are easily the better deal as they continue to pay the 8% or 8.25% coupon quarterly until maturity in 2028-2030. If not called, the notes would also benefit from BP's investment grade credit rating. (The TA bonds are not currently rated but the yield suggests something around BB-)

See the table below for my return calculations. TANNI and TANNZ have two more interest payments before 6/30, going ex "dividend" on 3/30 and 6/29. TANNL goes ex "dividend" in the middle of the quarter on 5/12, meaning it has 1.5 more interest payments before 6/30. (Accrued interest is paid if the bonds are called.) As we see below, even paying above par now results in yields-to-worst for TANNI and TANNZ that exceed the expected return for TA. TANNL has a YTW that is just in-line with the TA return.

{kind=link}

Risks & Considerations

The biggest risk for the baby bonds is that they get called early, even before the deal close, as TA has the cash on its balance sheet to do so. Paying above par would result in a capital loss with less interest payments to offset it. A less likely risk is that the deal does not close and TA suffers bad business conditions before the 2028-30 maturity dates, creating a risk of default.

Investors should keep in mind that these bonds trade a low volumes and bids for even 1000 "shares" could move the price so much that the relative attractiveness goes away. Please use limit orders and consider bidding for no more than a few hundred shares at a time.

Conclusion

BP's takeover of TravelCenters of America looks likely based on the narrow arb of 2% between the current price and the deal value. This spread is too low for a trade even with the low risk of failure. Even a short delay past a 6/30 close date would give even T-Bills a higher return.

Two of the three baby bonds, TANNI and TANNZ, offer a higher return if we assume they are called on 6/30. In the slight chance they are not called, they continue paying an 8% or 8.25% coupon until maturity in 2028-30. These bonds are a better way to play the takeover.

For further details see:

TravelCenters of America: BP Merger Arb Is Too Small, Bonds Are A Better Deal