TANNI - TravelCenters of America: Watch Fuel Margins Consider The Bonds

Summary

- TravelCenters of America looks cheap at around 4-5 times 2022 earnings, but profitability depends on fuel margins, which are now unusually high.

- The company is improving its non-fuel business, but still is break-even at fuel margins around 16 cents per gallon.

- The company's debt is exchange traded as $25 par baby bonds, maturing 2028-30. Given the strong balance sheet and high yields, these securities are a safer bet.

Introduction

TravelCenters of America (TA) is one of the cheapest stocks available based on its 2022 P/E in the 4-5 range. Notably, it did not get that cheap through price contraction, as the stock is up 5.1% YTD at the time of writing, and up 73.8% from its lows on June 16. Instead, EPS has increased dramatically from $4.01 in full year 2021 to $5.41 in just the first half of 2022. If fuel margins persist, the company could earn $12.46 for the full year. Before getting too excited though, it's important to dig deeper into the fundamentals to see how sustainable these earnings are.

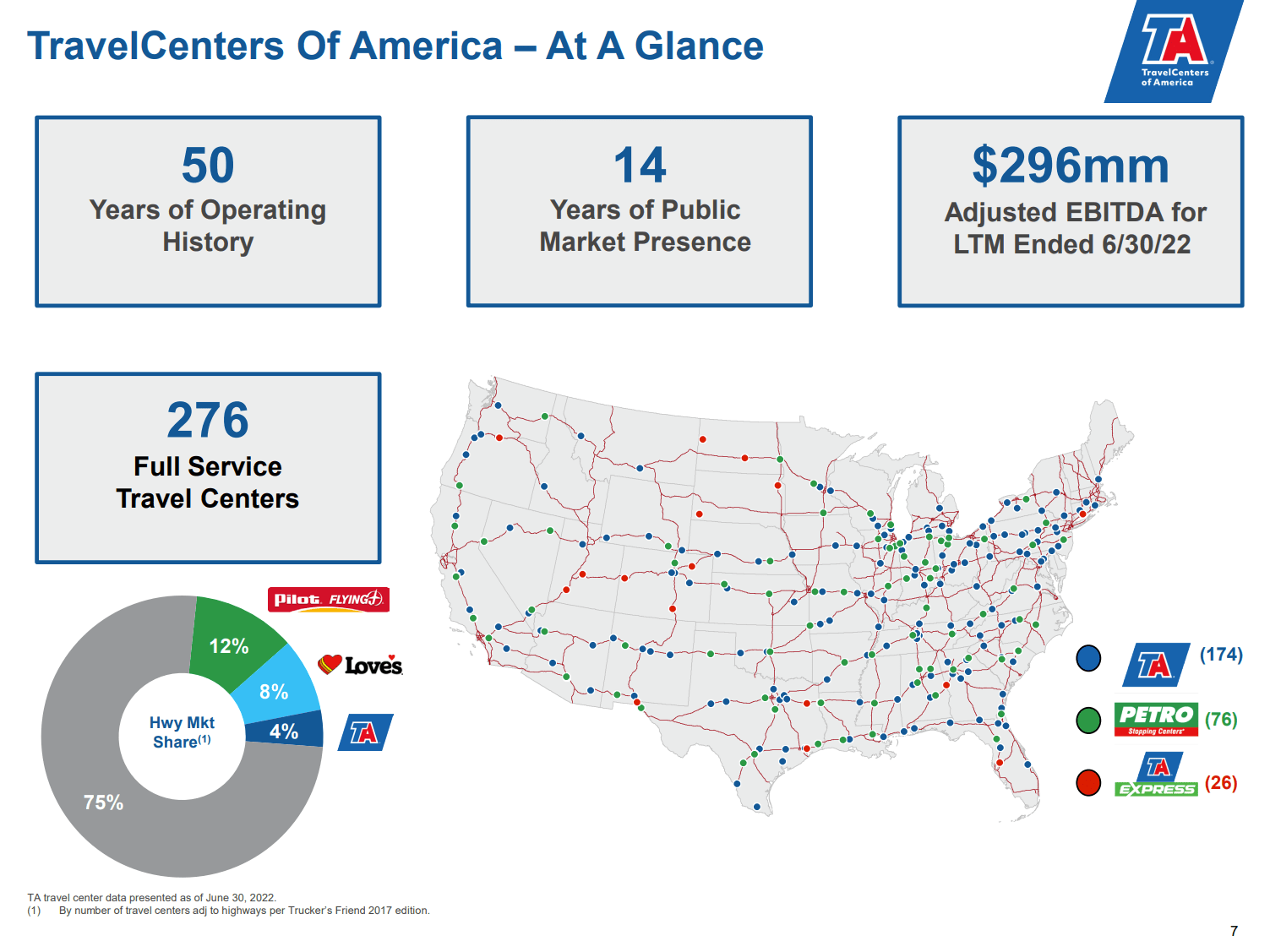

TA is the third largest company and the only publicly traded one in the highly fragmented truck stop industry where the top three companies make up only 1/4 of the total market. TA has 276 travel centers in the US, about 2/3 of which are leased from Service Properties Trust ( SVC ). Most of the remainder are either company-owned or franchised.

{kind=link}

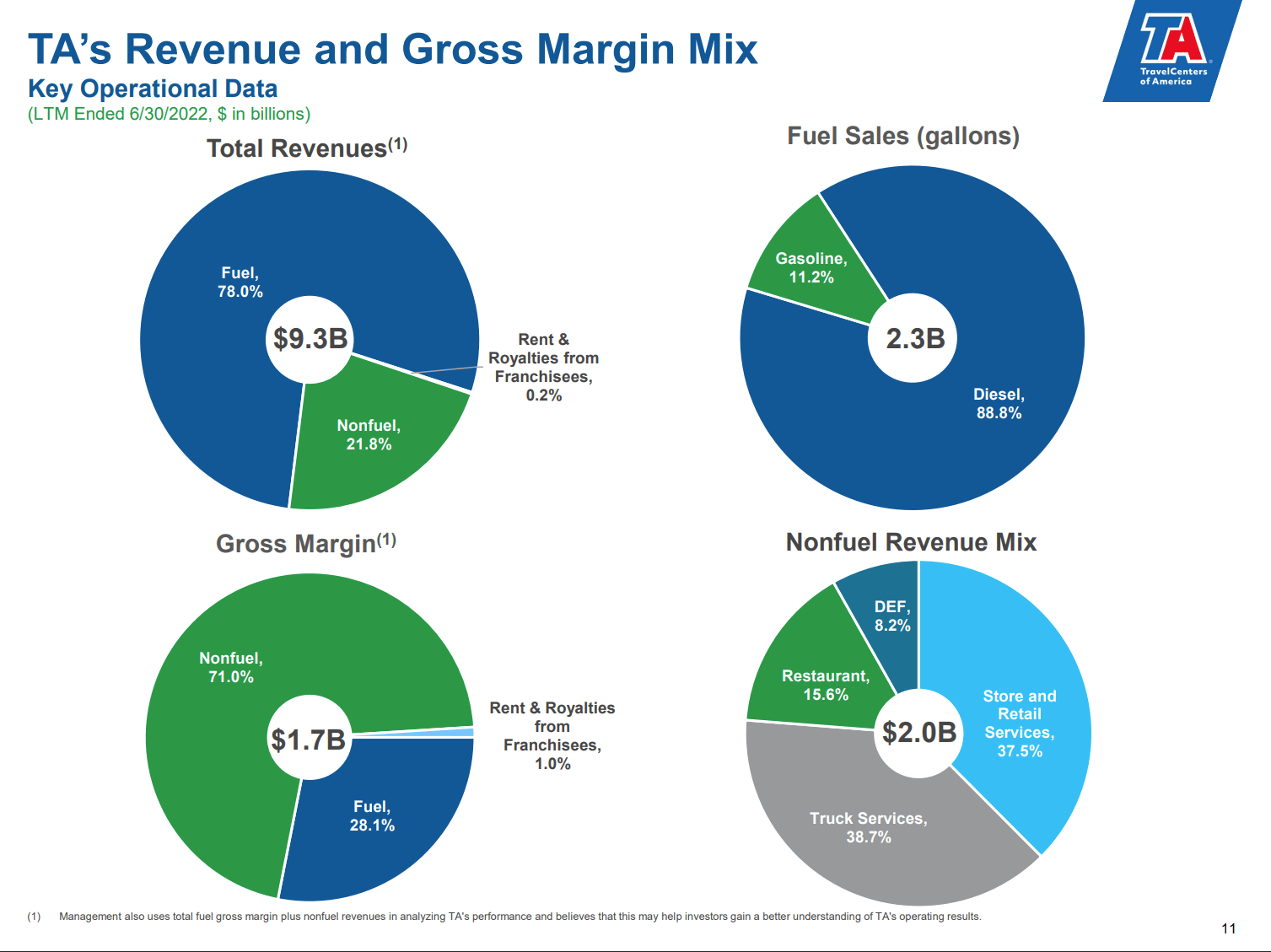

TA gets 78% of its revenue through fuel sales, the overwhelming majority of which is diesel. Because fuel margins are so thin however, the company earns 71% of its gross margin through nonfuel sales. Nonfuel sales include retail stores, restaurants, truck services, and diesel exhaust fluid.

{kind=link}

Despite nonfuel making up such a large share of the gross margin, fuel margins are more variable and a usually bigger driver of changes in financial results. This will be clear from the earnings model below.

Earnings Model

Fuel sales are TA's largest source of revenue but volume growth in gallons is near zero. The company has to rely on market forces mostly out of its control to determine fuel margins. In 2021, TA earned margins of 17.2 cents per gallon on average. This is near the company's stated long-term guidance of 15-17 cpg, reiterated in the last earnings call . In the first half of 2022 however, fuel margins averaged 23.9 cpg and were even higher in July at 26 cpg. If these margins persist for the rest of 2022, the full year average fuel margin would be 24.9 cpg and TA would earn an incremental $170 million of fuel gross margin this year.

TA is also doing a good job in nonfuel sales. Restaurant and retail sales are growing in the low single digits, but the standouts are truck services and diesel exhaust fluid sales. Under new management which took over in 2019, the company is working to gain back share in truck service and will have DEF available at all lanes by the end of this year. As a result, truck service revenues were up 10% in 2Q compared to last year and DEF sales were up 43%. Assuming similar performance in the second half of the year, nonfuel sales will grow by 9.2%. After subtracting nonfuel cost of goods, the nonfuel business adds only $103 million of incremental gross margin this year.

The company is also subject to increasing operating costs, particularly site operating expenses, SG&A, and depreciation as it increases capex to drive sales. Operating costs will be up about 7.6%, or $111 million in 2022.

After subtracting interest and taxes, we see the large change in EPS from $4.01 in 2021 to $12.46 in 2022 was driven mostly by the increase in fuel margin as the nonfuel gross margin increase was offset by higher operating costs.

Looking ahead to 2023, we can predict similar growth trends for nonfuel sales and operating expenses, but fuel margins are the big question mark. If we assume a drop-off to 20 cpg, which is still above 2021 levels and the company's long-term assumption, EPS falls back down to $4.75/share. This would value the company at 11.4 times 2023 earnings, nowhere near the screaming buy suggested by the current P/E.

Author Spreadsheet (Data Source: TA Earnings Releases and author estimates)

{kind=link}

Since the fuel margin is the most uncertain factor, we can do a sensitivity analysis of how it will affect 2023 EPS. We see that TA breaks even around a 16 cpg fuel margin. This value happens to be the midpoint of the company's current long-term expectation. I do expect them to revise the long-term plan upward, but for now it basically implies a company making zero profit over the long term unless it can achieve faster growth in nonfuel sales or market share capture in fuel sales.

Author Spreadsheet

TA common stock is still basically a leveraged bet on fuel margins. You can buy it if you believe fuel margins have taken a step change upward from prior levels, but if you believe margins will continue to be cyclical, you should wait for a pullback. TA's lack of a dividend also suggests uncertainty that current margins can be sustained. Income investors were probably already avoiding the stock, but they should consider the bonds.

A Look At TA Baby Bonds

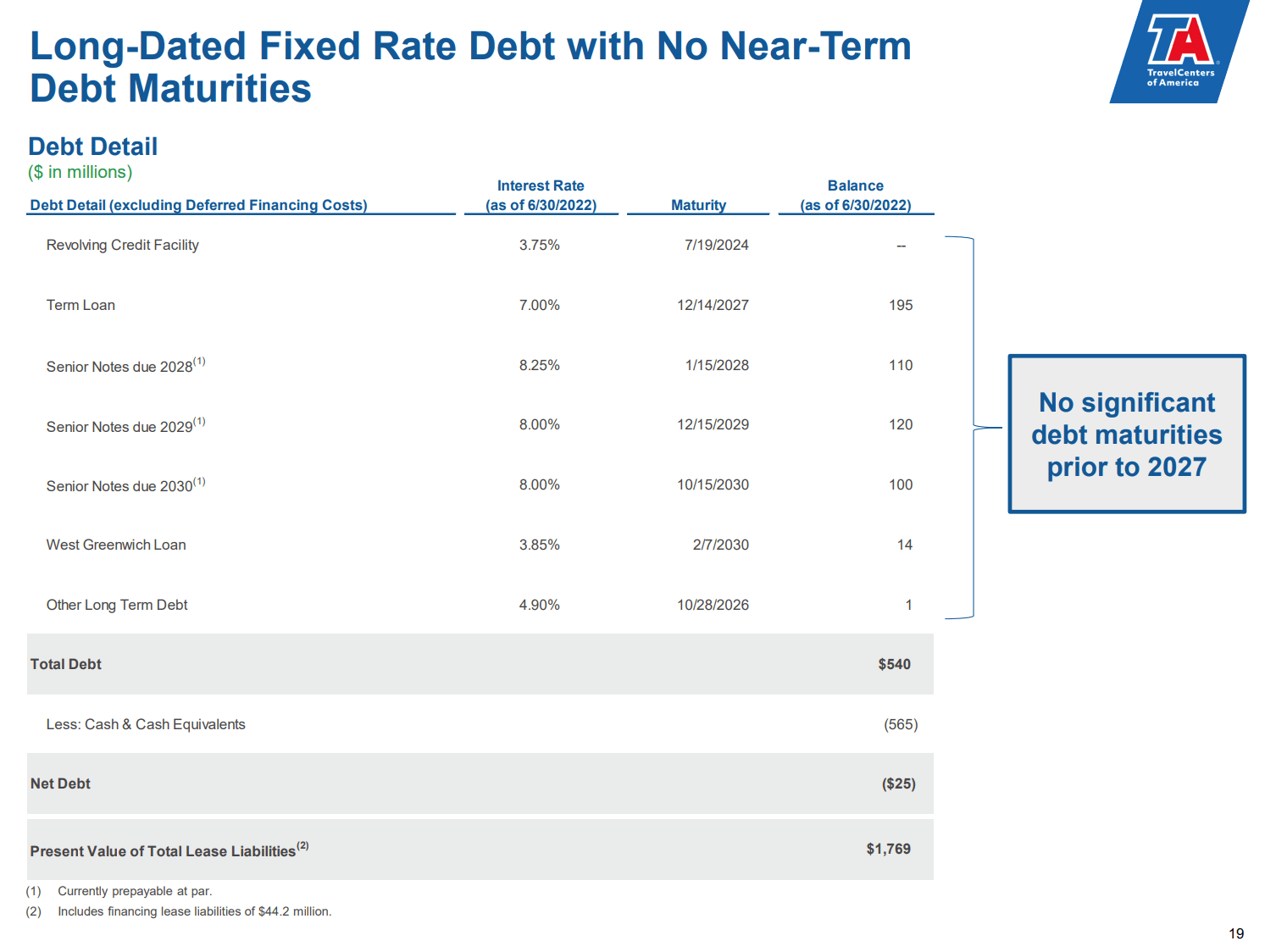

TA's debt consists primarily of a $195 million, 7% term loan due in 2027 and three series of senior notes: the 8.25% due 1/15/2028 ( TANNI ), the 8% due 12/15/2029 ( TANNL ), and the 8% due 2030 ( TANNZ ).

{kind=link}

These notes are considered "baby bonds" with a par value of $25. Unlike regular bonds, they trade on the stock exchange the same way as a common stock and pay interest quarterly. You also do not have to deal with accrued interest when you buy and sell them. However, since they are bonds, the interest payments are non-qualified and taxed at ordinary income rates.

These notes were issued from 2013-15 as 15-year maturities. Each one is now callable at any time at par value of $25. The company has left these notes outstanding despite having enough cash on the balance sheet to call them. After a couple more quarters of high fuel margins, the company could institute a common stock buyback or dividend, or they could finally call some of these bonds. Because of this, I would not pay more than $25 plus the value of one quarterly interest payment. Currently, only TANNL qualifies as buyable under this criterion.

The bonds have held up well in price except for the Covid crash of March 2020. They traded down only to the $23 area in 2018, the last time medium term interest rates were at similar levels to today.

{kind=link}

The bonds are not rated by the agencies. Interest coverage was 2.6 times in 2021 and is expected to be 6.3 times in 2022. Gross Debt/Trailing 12-month EBITDA was 1.8 times as of 6/30/2022. Of course, these values are based on unusually high fuel margins. Still, the company can afford to pay the interest and break even down to a fuel margin level of 16 cpg.

If interest rates increase from here, you may be able to pick up these bonds at a lower price, but you can still get a yield to maturity of just under 8% at current prices. Risk of default is low, barring an extended slump in fuel margins.

Conclusion

TravelCenters of America is having a great year thanks to high fuel margins. The company is better run than it was in the past and is growing its nonfuel business, but profitability is still highly levered to fuel margin. One should not get excited over the 2022 P/E in the 4-5 range with fuel margins at 25 cpg. The company looks more reasonably valued assuming fuel margins of 20 cpg and is break even at 16 cpg.

The baby bonds due from 2028-2030 are a good choice for income investors, assuming the company can at least break even until then. They are available slightly above par and have a yield to maturity just under 8%. At this point, with the company in a negative net debt position, the risk of the bonds getting called at $25 exceeds the default risk.

For further details see:

TravelCenters of America: Watch Fuel Margins, Consider The Bonds