TZOO - Travelzoo: Moderate Risk And Slightly Overvalued

2023-06-20 08:00:00 ET

Summary

- TZOO faces moderate risks, including potential liquidity issues due to its cash position and merchant payables liability, while having limited catalysts for growth.

- The company's U.S. segment, which is the core business, has seen a decline in subscribers, and its Europe business struggles to grow and scale profitably.

- I maintain a sell rating on TZOO. My target price model suggests that the stock is slightly overvalued at its current price of $9 - $10.

I first covered Travelzoo (TZOO) in 2020, when the stock was trading at ~$5 as the business struggled due to the COVID-19 travel headwinds. Obviously, the stock rallied in 2021 and reached ~$17 before seeing a gradual decline and retesting the $5 level around the beginning of this year.

Currently trading between $9 - $10 per share, the market sentiment appears to have been quite positive on TZOO this year despite the historical volatility. YTD, the share price has appreciated by ~105%.

Nonetheless, my view is that there are minimal catalysts on the stock at this time. The stock also faces moderate risks, including a potential liquidity risk due to the current cash level and merchant payables liability. My target price model also suggests that the stock is slightly overvalued today. I maintain my sell rating on TZOO.

Risk

While TZOO seems to have rebounded post-COVID, I continue to see weaknesses across its business lines.

{kind=link}

The U.S. segment, for instance, is ~68% of TZOO's business and a key growth driver, but it is facing declining subscriber growth . The number of U.S. subscribers declined from ~16.8 million in Q1 2022 to ~16.2 million in Q1 2023. If the decline continues, I believe that TZOO will likely see its overall growth runway rather limited.

{kind=link}

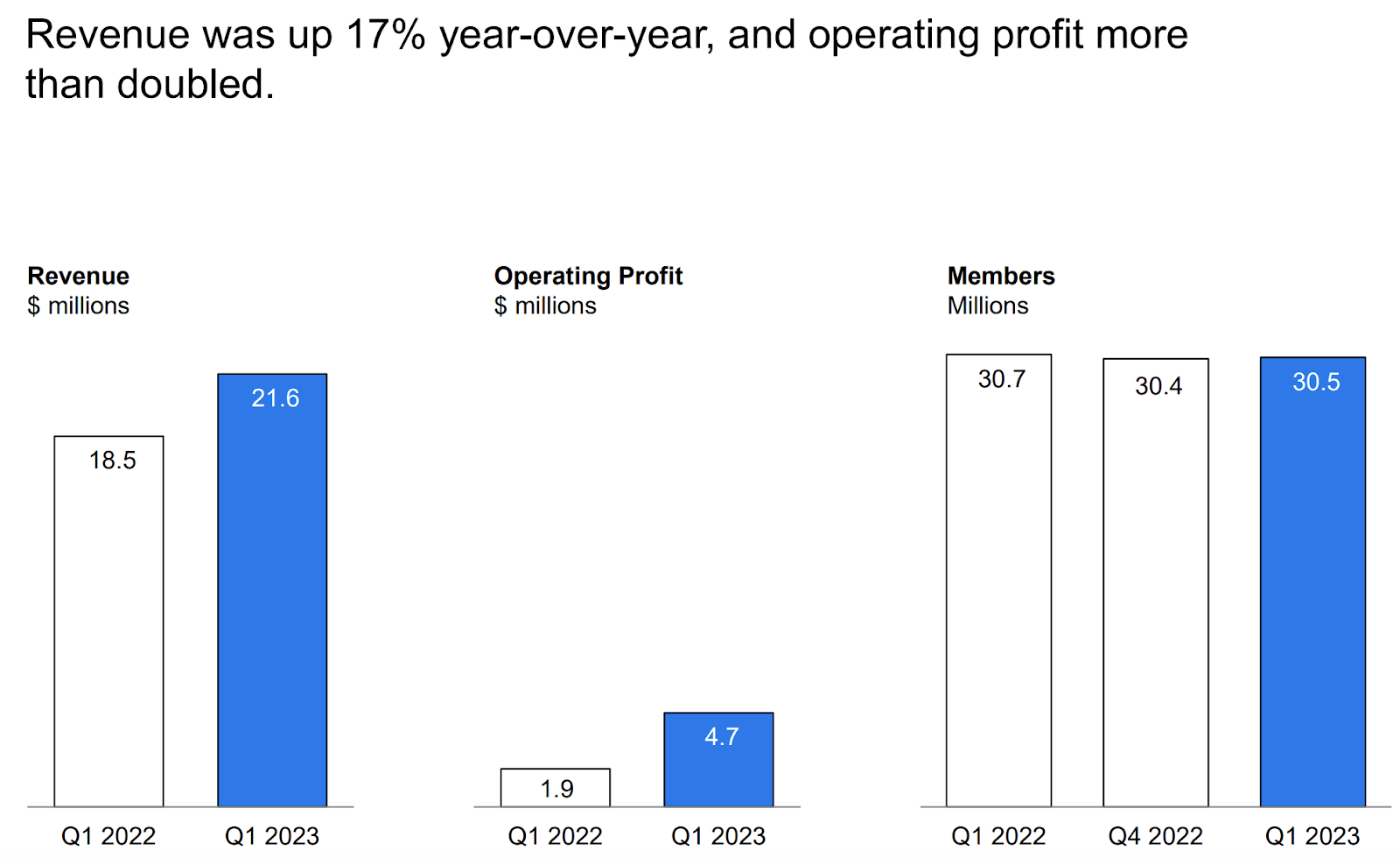

Eventually, profitability may also be negatively affected. In Q1, revenue grew by 17% and operating profit grew by ~2.5x times YoY to $4.7 million. But the US business alone contributed more than 95% of such operating profit.

{kind=link}

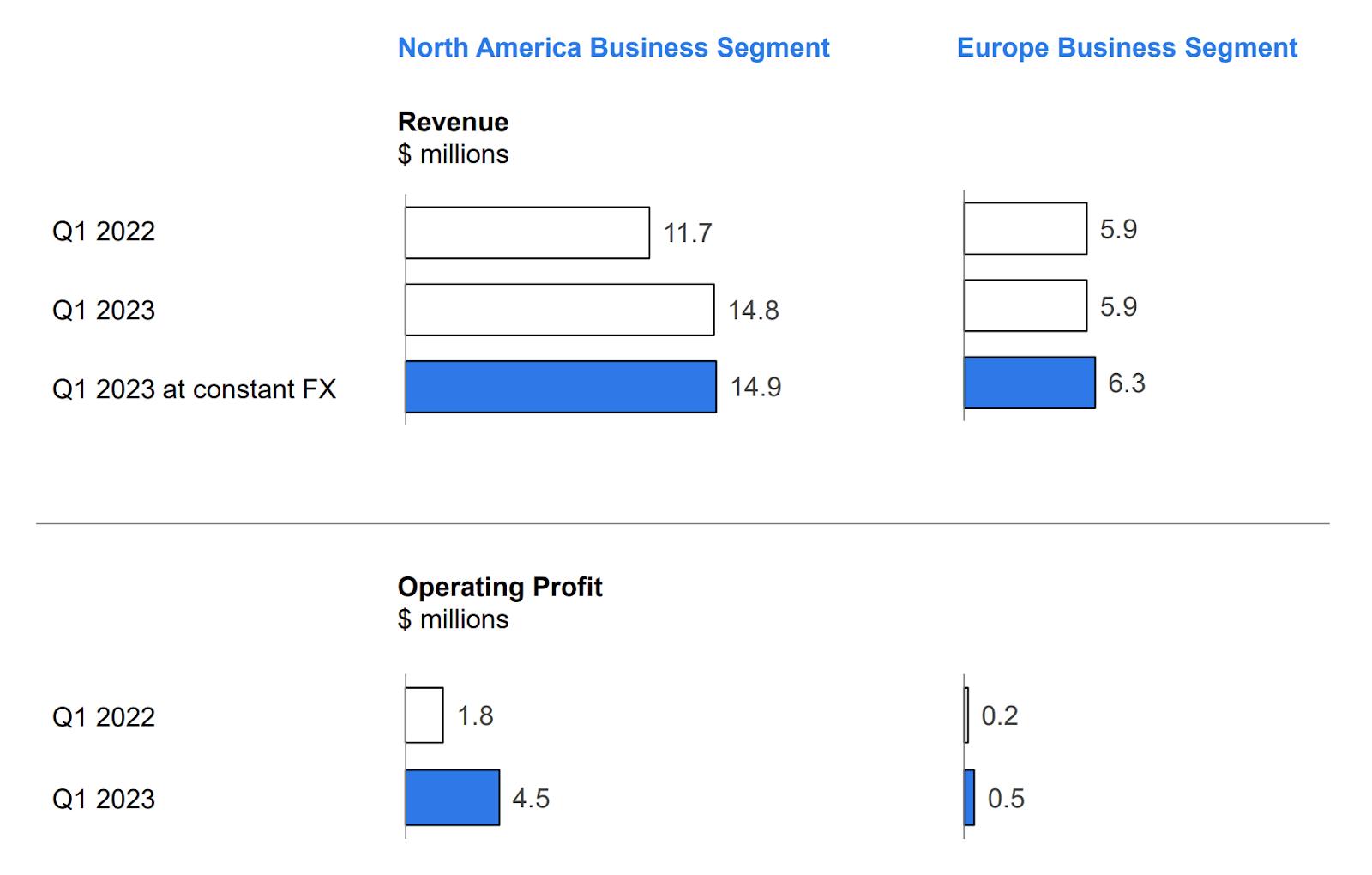

In addition, the Europe segment made up a meaningful ~27% share of the business in Q1, but it has been quite a challenging business for TZOO to grow and scale profitably. Europe remained flat YoY in terms of revenue growth in Q1, and despite turning profitable, its contribution to the overall profitability was minimal.

I continue to expect Europe to see underperformance since it appears that TZOO is still struggling to make unit economics work there. Things may even get worse, considering the ongoing macro weakness in Europe . In FY 2021 and FY 2022, for instance, Europe saw 12% to 13% YoY revenue growth, though they came with operating losses in both instances, suggesting that the growth was not sustainable. Likewise, while Europe’s operating profit turned positive in Q1 as we saw earlier, the revenue actually experienced a decline.

TZOO earnings report

Until TZOO discovers an effective strategy to enhance its unit economics, increasing marketing expenditure will not provide a solution. This is because for each dollar TZOO invests, it incurs a loss. In Q1 2023, TZOO experienced a loss of ~$1.2 for every dollar it spent on acquiring new members in Europe.

Managing acquisition costs is also just one of many areas where unit economics improvement can take place. The other important area is execution. At the same time last year, Europe actually realized an operating loss despite seeing a profit per new member acquisition, suggesting that there's room for improvements in execution.

{kind=link}

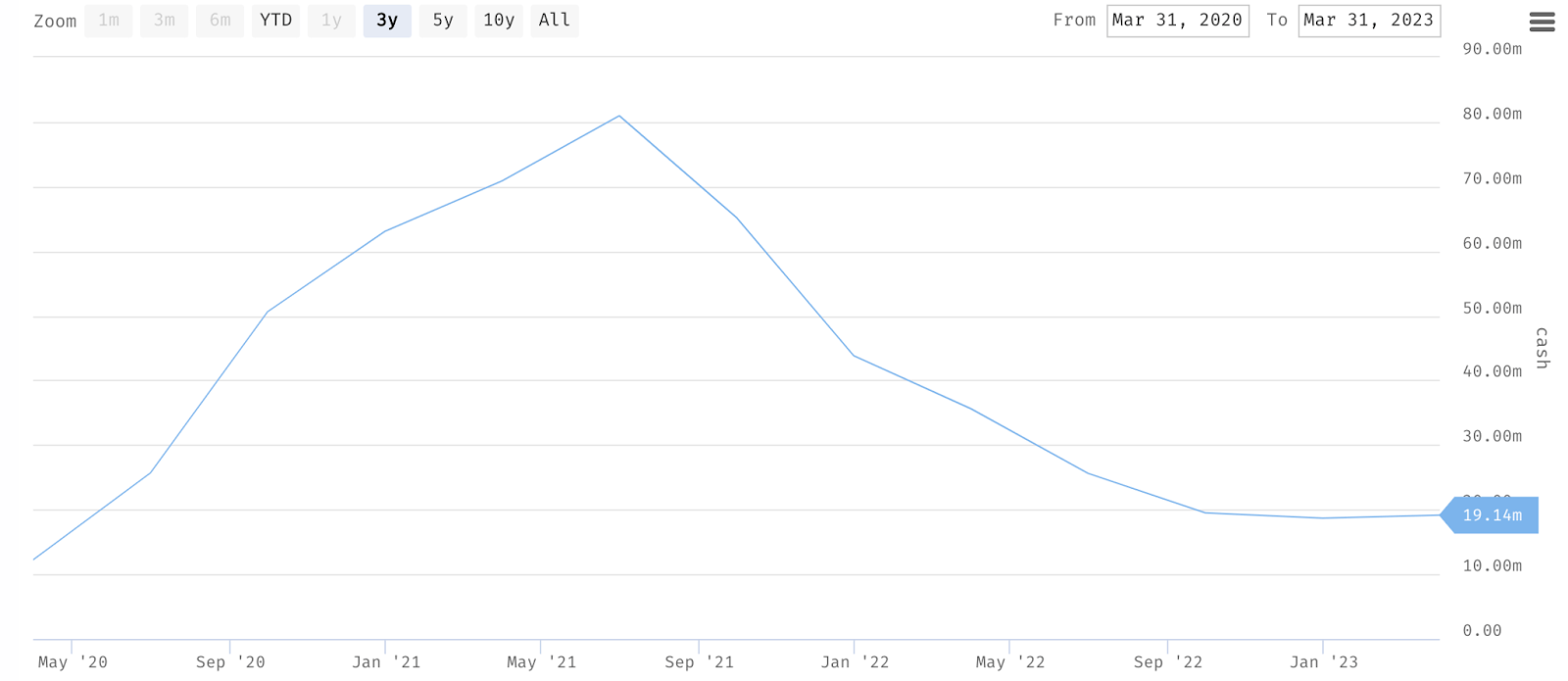

Furthermore, I think that TZOO may potentially be exposed to a near-term liquidity risk. Cash and cash equivalents / CCE stood at just ~$19 million in Q1, and despite the management suggesting a steady cash outlook for FY 2023, it appears a bit short to cover a key payable item, merchant payables. As per its 10-Q , TZOO has accumulated merchant payables as part of its business. As of Q1, merchant payables related to unredeemed deal vouchers were $28 million, and while the expiration date for the redemption varies between April 2023 through December 2025, the majority of it would expire during 2023.

Given the situation, it seems that even if TZOO can make partial payments in FY 2023 by delaying the expiration of some of the vouchers, there are two key issues. First, the ability to make the payment will also rely on TZOO’s ability to continue maintaining positive OCF generation throughout the rest of the year. Second, the limited ability to service the liabilities also suggests that TZOO will have limited ability to invest in growth and improve its operations.

Catalyst

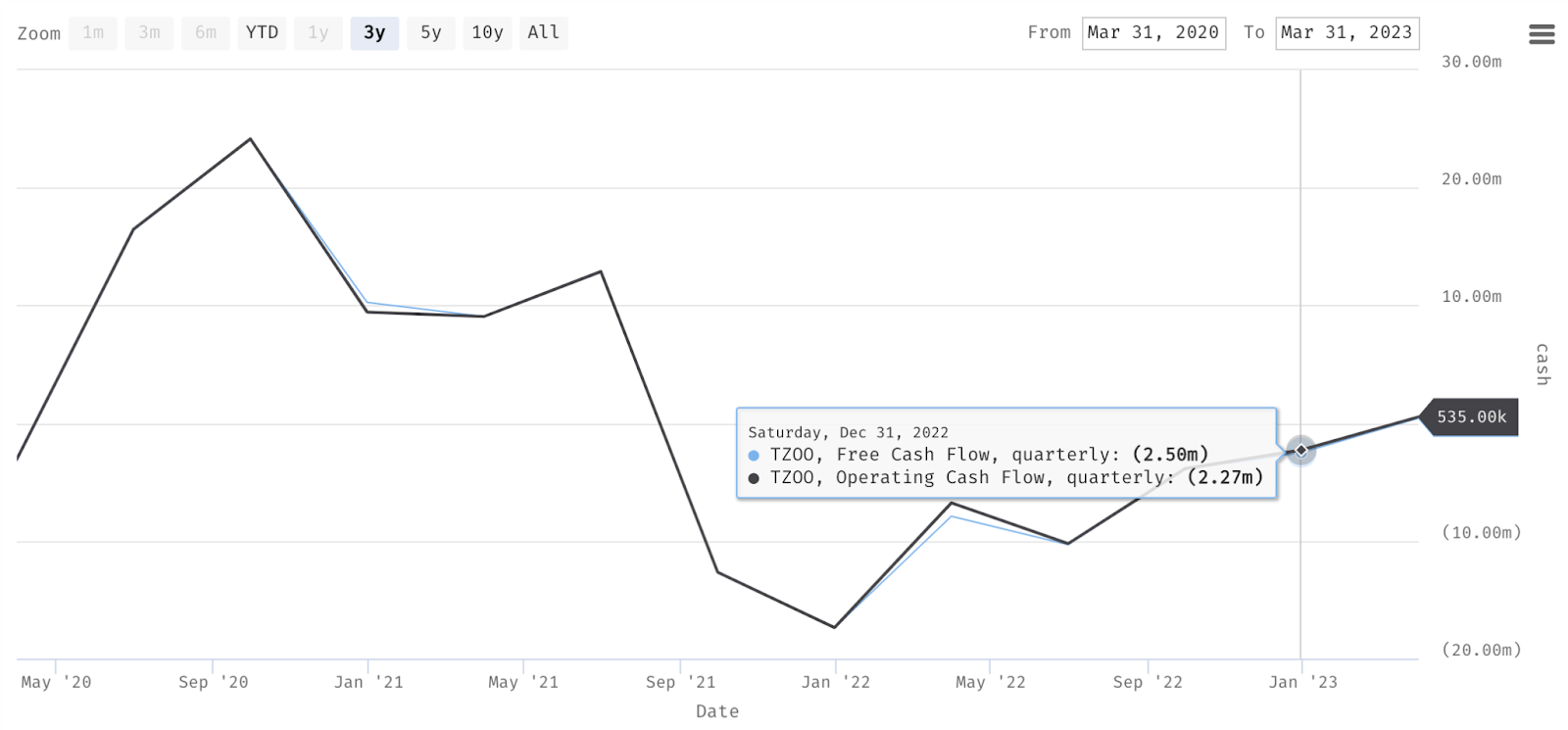

I believe that near-term catalysts remain minimal for TZOO, though I would acknowledge that there are some positives about the company. OCF generation, for instance, continued to improve. This should help improve its cash balance and effectively service its merchant payables.

{kind=link}

OCF's performance has been consistent with the management’s expectation that cash-related expenses would bottom around Q4 last year. Since January 2022, OCF has been trending up, and in Q1, TZOO had a positive OCF.

TZOO has also been a net profitable business since FY 2021. In that FY, it realized a net margin of 1.47% , which then expanded to ~9% in FY 2022.

Furthermore, given the consistently solid unit economics in the US business , it remains the key area where TZOO can continue investing in to drive the growth of the overall business profitably.

Valuation / Pricing

My target price for TZOO is driven by the following assumptions for the bull vs bear scenarios of the FY 2023 target price model:

-

Bull scenario (50% probability) assumptions - TZOO to finish FY 2023 with an EPS of $0.87, slightly lower than the midpoint of market estimates . I assign TZOO a P/E of ~16x, which is where it is trading today.

-

Bear scenario (50% probability) assumptions - TZOO to miss the market estimate and finish FY 2023 with an EPS of $0.53. Since I expect EPS to not see any improvement, I assign TZOO a P/E of 8x, a low point in FY 2023 seen sometime towards the beginning of the year.

author's own analysis

Consolidating all the information above into my model, I arrived at an FY 2023 weighted target price of $9.08 per share. With TZOO trading between $9 - $10 per share most recently, I conclude that the stock remains slightly overvalued by ~3.5%.

It is important to note that my target price does not assume potential share repurchases for FY 2023 , which may increase EPS. I also continue to view TZOO’s share repurchases as a suboptimal use of cash. Given the minimal catalyst and relatively moderate risk, I maintain my sell rating on the stock.

Conclusion

Despite showing signs of recovery after the COVID-19 pandemic, TZOO still exhibits weaknesses in its various business lines. Currently, there are limited factors that could positively impact the stock, while it faces moderate risks, including potential liquidity issues stemming from its cash position and merchant payables liability. Considering TZOO's recent trading range of $9 - $10 per share, I believe the stock is slightly overvalued. Given the limited catalysts and moderate risk, I maintain my sell rating for TZOO stock.

For further details see:

Travelzoo: Moderate Risk And Slightly Overvalued