TG - Tredegar: A Corporate Restructuring And Downcycle Mask A Great Opportunity

2024-01-19 17:35:28 ET

Summary

- Tredegar is an undervalued stock with low investor interest due to poor performance and lackluster results.

- The company has implemented corporate initiatives to improve its financials in the near term.

- The sale of a business division and the potential for a return to normal results make this an attractive investment opportunity.

Tredegar ( TG ) is an unloved and underfollowed stock where investors lost all hope of better days ahead. The company current problems are mainly due to a downcycle in all of their divisions, and consequently lackluster results. The company enacted several corporate initiatives that will show better financials in the near term, but even a valuation at the current situation shows a stock that is fairly value. The sale of a business division and the high probability of a return to normal results put the odds on our side in this investment.

Current situation and stock price

Tredegar currently operates three divisions, Aluminum extrusion, PE films and Flexible films. This last one was sold in the 4Q of 2023 and in the near future the company will operate only two divisions. The company stock price history paints a bleak picture with the performance of the last five years at around minus 70%, but it should be mentioned that the company paid a $5.97 special dividend per share in December 2020, so the return would be a lot better if we consider that current stock price is $5.26.

The company has been an steady operator of their divisions, in fact 2020 was very good year for the company. In that year TG sold their Personal Care films division for $55 million and paid a special dividend of $200 million, going from a net debt negative company in the 3Q2020 to $122 million in net debt at the end of 2020. Between 2021 and 2022 the company sold another investment, Kaleo, for $47 million and made a contribution to their unfunded pension plan of $50 million in order to retire this obligation from their balance sheet. After another contribution of $27.7 million in 2023 the company was able to pass their defined benefit pension plan to Massachusetts Mutual Life Insurance Company. The company net debt stood at around $105 million in 3Q2023. The year and half has been difficult and the light is hard to see at the moment as the CEO put it :

“We recognized another loss for the quarter as our businesses continued to suffer from severe down cycles in their markets that we believe are residual impacts of the pandemic. The timing of a recovery remains uncertain as we move into the seasonally low winter months for Bonnell.”

Divisions

Aluminum Extrusions

Tredegar operates two divisions at the moment. The Aluminum extrusions division under the name Bonnell Aluminum is the biggest division and historically has accounted for around 80% of the sales of both divisions but 67% of the of the EBITDA. This division is mainly exposed to construction, representing 63% of 2022 sales but also to the automotive, machinery and other consumer durables specialty segments and as such Bonnell is a cyclical company specially influenced by the credit cycle.

{kind=link}

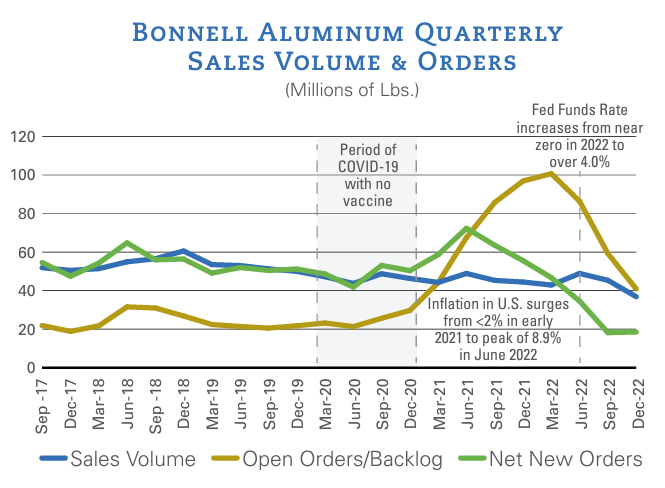

Sales and Backlog (Company annual report)

The impact of the increase in the Fed Funds Rate from 0% to over 4% in 2022 is clear on the graph, with the backlog orders went from over 100 million lbs in the end of 2021 to around 40lbs at the end of 2022. While the backlog is still above the 20 million lbs average, the net new orders are below their historical levels or around 50 million lbs.

{kind=link}

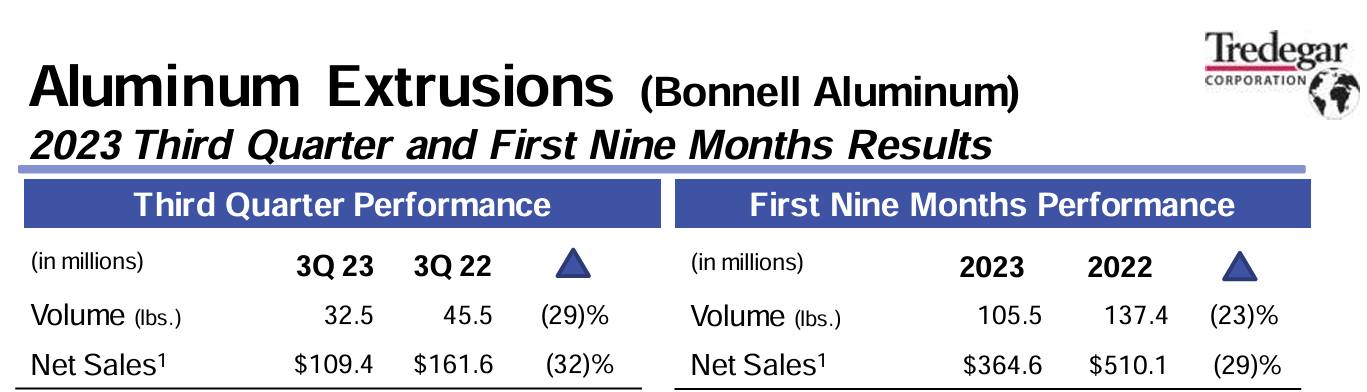

3Q2023 Results (Company website)

The weak net new orders at the end of 2022 were a sign of what would happen in 2023, with sales down 29% and 23% in dollars and lbs, respectively. Open orders at the end of the third quarter of 2023 were 17 million pounds (vs. 20 million pounds at the end of the second quarter of 2023 and 59 million pounds at the end of the third quarter 2022). The sluggish demand continues in most of the markets where Bonnell is present.

PE Films

The PE films produces surface protection films, polyethylene overwrap films and films for other markets and represents 20% of the sales but around 33% of the EBITDA. It's a division with EBITDA margins of 25% on average in the last five years vs. Bonnell which had EBITDA margins of 11%. Nevertheless, this division also is facing its own problems. One of the biggest declines in demand on record of the display industry in the second half of 2022 impacted severely the profitability of the PE division, with EBITDA levels close to breakeven.

{kind=link}

3Q2023 Results (Company website)

While Bonnell is more of a commodity type of product and depends more on phase of the industry cycle, the PE films division has more levers to pull to increase profitability. In 2H2022 the management enacted some measures to adjust the cost structure to the current environment and that is already visible in 3Q2023 results, with EBITDA Margin recovering to 20% due to lower costs and operating efficiencies.

Market Expectations and Valuation

Market expectations for Tredegar are very depressed with the current share price reflecting investors' expectations of the severe downcycle to continue for eternity. All this negativity stacks the odds in our favor because eventually things will get back to normal, company profitability will be restored, the outlook will seem less grim and stock price will go back to higher levels.

| Earnings Power Value ($ thousands) |

| Aluminum Extrusion |

| Worst Case |

| Base Case |

| Best Case |

| Sales (lbs) |

| 140,681 |

| 188,675 |

| 208,249 |

| Net Price per lbs |

| 3.46 |

| 2.92 |

| 2.92 |

| Net Sales |

| 486,143 |

| 550,424 |

| 607,528 |

| EBITDA per lbs |

| 0.28 |

| 0.33 |

| 0.33 |

| EBITDA |

| 39,957 |

| 61,966 |

| 68,395 |

| EBITDA Margin |

| 8.2% |

| 11.3% |

| 11.3% |

| Operating Income |

| 21,957 |

| 43,966 |

| 50,395 |

| Operating Margin |

| 4.5% |

| 8.0% |

| 8.3% |

| Corporate expenses, net |

| 14,721 |

| 14,721 |

| 14,721 |

| EBT |

| 7,236 |

| 29,245 |

| 35,673 |

| Taxes @ 21% |

| 1,520 |

| 6,141 |

| 7,491 |

| Maintenance Capex |

| 10,000 |

| 10,000 |

| 10,000 |

| Depreciation |

| 18,000 |

| 18,000 |

| 18,000 |

| Earnings Power |

| 13,716 |

| 31,103 |

| 36,182 |

| EPV Multiple |

| 11 |

| 11 |

| 11 |

| EPV |

| 150,880 |

| 342,135 |

| 398,001 |

| PE Films |

| Worst Case |

| Base Case |

| Best Case |

| Sales (lbs) |

| 27,783 |

| 41,786 |

| 45,175 |

| Net Price per lbs |

| 2.69 |

| 2.96 |

| 2.96 |

| Net Sales |

| 74,715 |

| 123,783 |

| 133,824 |

| EBITDA per lbs |

| 0.36 |

| 0.74 |

| 0.74 |

| EBITDA |

| 10,099 |

| 30,773 |

| 33,269 |

| EBITDA Margin |

| 13.5% |

| 24.9% |

| 24.9% |

| Operating Income |

| 3,099 |

| 23,773 |

| 26,269 |

| Operating Margin |

| 4.1% |

| 19.2% |

| 19.6% |

| Corporate expenses, net |

| 2,907 |

| 2,907 |

| 2,907 |

| EBT |

| 191 |

| 20,865 |

| 23,362 |

| Taxes @ 21% |

| 40 |

| 4,382 |

| 4,906 |

| Maintenance Capex |

| 2,000 |

| 2,000 |

| 2,000 |

| Depreciation |

| 7,000 |

| 7,000 |

| 7,000 |

| Earnings Power |

| 5,151 |

| 21,484 |

| 23,456 |

| EPV Multiple |

| 13 |

| 13 |

| 13 |

| EPV |

| 66,966 |

| 279,288 |

| 304,923 |

| EPV SOTP |

| 217,846 |

| 621,423 |

| 702,924 |

| Debt |

| 155,000 |

| 155,000 |

| 155,000 |

| Loan on Terphane |

| 20,000 |

| 20,000 |

| 20,000 |

| Cash from Terphane, net of taxes |

| 85,000 |

| 85,000 |

| 85,000 |

| Cash |

| 48,600 |

| 48,600 |

| 48,600 |

| Intrinsic Value |

| 176,446 |

| 580,023 |

| 661,524 |

| Shares outstanding (millions) |

| 34 |

| 34 |

| 34 |

| Intrinsic value per share |

| 5.1 |

| 16.9 |

| 19.2 |

| Upside |

| 9% |

| 259% |

| 309% |

The valuation idea is calculating the Earnings Power Value for Tredegar in a normal level of earnings, meaning that no growth is considered to find the intrinsic price of the company. In the case of Tredegar, it makes sense to value both of divisions normal earnings separately since they have different economic characteristics. On both case sales were found by averaging the last five years of quantity sold (lbs) and multiplying by the average net sales price of the last five years. Additionally, the EBITDA was calculated using the EBITDA margin average of the last five years. Another item that deserves to be mentioned is the corporate expenses which was divided by both divisions proportionally to their sales contribution for Tredegar. The capex considered is the maintenance capex only since growth calculations are not included in this approach. The multiples for both divisions are 11 and 13, with PE films being higher but conservative due to higher historical operational margins. In the base scenario the Aluminum division EPV is $342 million, and PE Films is worth $279 million which leads to a EPV of $621 million for Tredegar. To find the intrinsic value we have to consider the company net debt. The company net debt on 3Q2023 was $106 million but in the 4Q2023 the company asked for a $20 million loan through Terphane that will be paid with the completion of the sale for $85 million. The intrinsic value of TG is somewhere between $5 and $19 per share depending on the scenario but the base case scenario points to a value of $16.9 per share. The stock is slightly undervalued even on the worst-case scenario that considers the lowest net sales in the company history and one of the lowest profitability on record. There's a clear upside in this opportunity even without accounting for future growth.

Risks and Catalysts

The main thesis in this opportunity is that a reverse to the mean will occur in the future, the business will stabilize, and the stock will recover, but for that to happen Tredegar needs to have the financial resources to wait for better days. Total net debt is $126 million but the sale of Terphane will generate $85 million so the company total exposure is $41 million, a very manageable amount, even in the worst-case scenario. Nevertheless, they had the need to negotiate less restrictive covenants and new ABL lending facility with the banks until the end of 2023. So the company will have the resources to wait for the rebound in the market cycle while it works to improve its profitability. Additionally, part of the debt piled up by the company in 2022 and 2023 was related with the termination of the pension plan and not due to bad results and from 2024 onwards will not have to present pension expenses anymore which will lead to better financials. While waiting for better results is one of the catalysts, another catalyst is the possible reinstatement of the dividend after 2024. Moreover, the average dividend per share in the last five years was $0.46 per share, and if in the future the company reinstate that dividend and a dividend yield of 2.5% is considered that implies a share price of around $18.

The setup on this opportunity seems a very good one, a lot of elements that stack the odds in our favor. An unloved company with a depressed stock price on a market downcycle with a temporary decline in earnings, but at the same time with the capacity and resources to solve the problem and near-term catalyst to accelerate the recovery of the stock price. Let's go!

For further details see:

Tredegar: A Corporate Restructuring And Downcycle Mask A Great Opportunity