FREEW - TreeHouse Foods: Recent Strength And Cheap Shares Warrant Upside

2024-01-14 08:20:56 ET

Summary

- TreeHouse Foods has experienced a decline in stock performance despite positive revenue growth and improved cash flows.

- A lot of recent strength can be chalked up to higher prices, which has improved bottom line performance substantially.

- Management has also been active in buying and selling assets as necessary to keep the firm's offerings relevant and to grow over time.

- Add in how cheap shares are, and the company makes for a decent prospect at this time.

As much as I wish I could say that I had a perfect track record when it came to pointing out attractive investment opportunities, that would be a lie. Nobody, not even the great Warren Buffett, has a perfect track record. One firm that I came out bullish on back in late 2022 was TreeHouse Foods ( THS ), a company that focuses on a variety of packaged foods and beverages, with examples of the former being hot cereals, jams, crackers, cookies, and more. At the time, I acknowledged that financial performance had been somewhat mixed. The bottom line is where a lot of the pain at the time was. However, I was enthusiastic about some asset sales that management had engaged in and I believed that the added clarity from those sales would propel shares higher.

Since then, things have not gone exactly as I would have hoped. Even though I rated the company a ‘buy’ to reflect my view that the stock should outperform the broader market, shares are down 16.5% at a time when the S&P 500 is up 16.6%. Given this awful outcome so far, you might think that I was here to downgrade the stock to something more bearish. Despite some bottom line pain that definitely makes me regret my previous rating, I have been impressed with continued revenue growth achieved by management. On top of that, cash flows are growing nicely and it looks as though the 2023 fiscal year in its entirety will end up looking quite positive. Add on top of this how cheap the stock has become, and I cannot in good conscience rate the company anything worse than the ‘buy’ I had it rated previously.

Growing pains

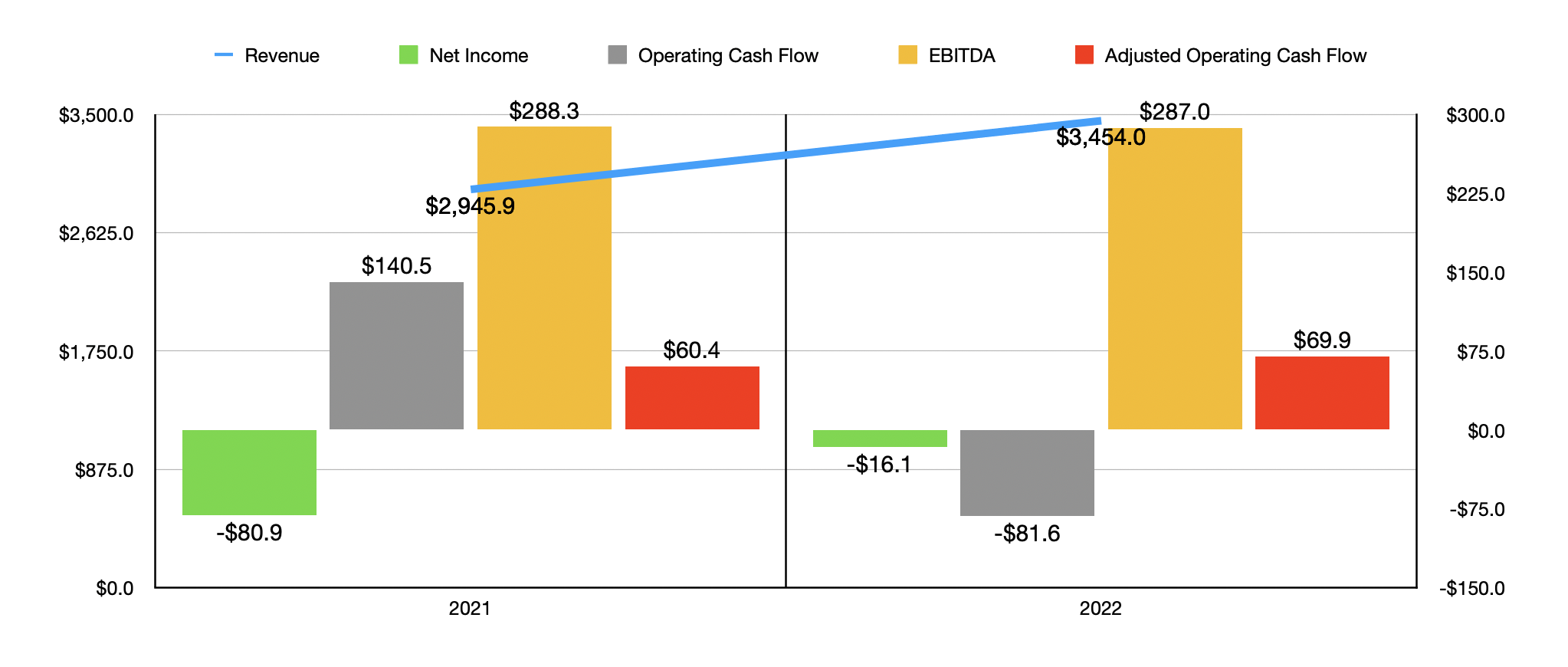

When I last wrote about TreeHouse Foods in late 2022, we only had data covering through the third quarter of that fiscal year. Today, we now have data covering not only all of 2022, but also through the first three quarters of 2023. To start with, we might want to touch briefly on how 2022 ended up looking. Although most of the focus of this article will be on the 2023 data. Revenue for the year came in at $3.45 billion. That's comfortably above the $2.95 billion reported one year earlier. In addition to seeing some attractive revenue growth, the firm went from generating a net loss of $80.9 million in 2021 to generating a net loss of only $16.1 million in 2022. But beyond that, the picture looks somewhat mixed. For instance, operating cash flow actually went from $140.5 million to negative $81.6 million. Though if we adjust for changes in working capital, we would get an increase from $60.4 million to $69.9 million. On the other hand, EBITDA for 2022 came in slightly lower than it did in 2021, inching down from $288.3 million to $287 million.

{kind=link}

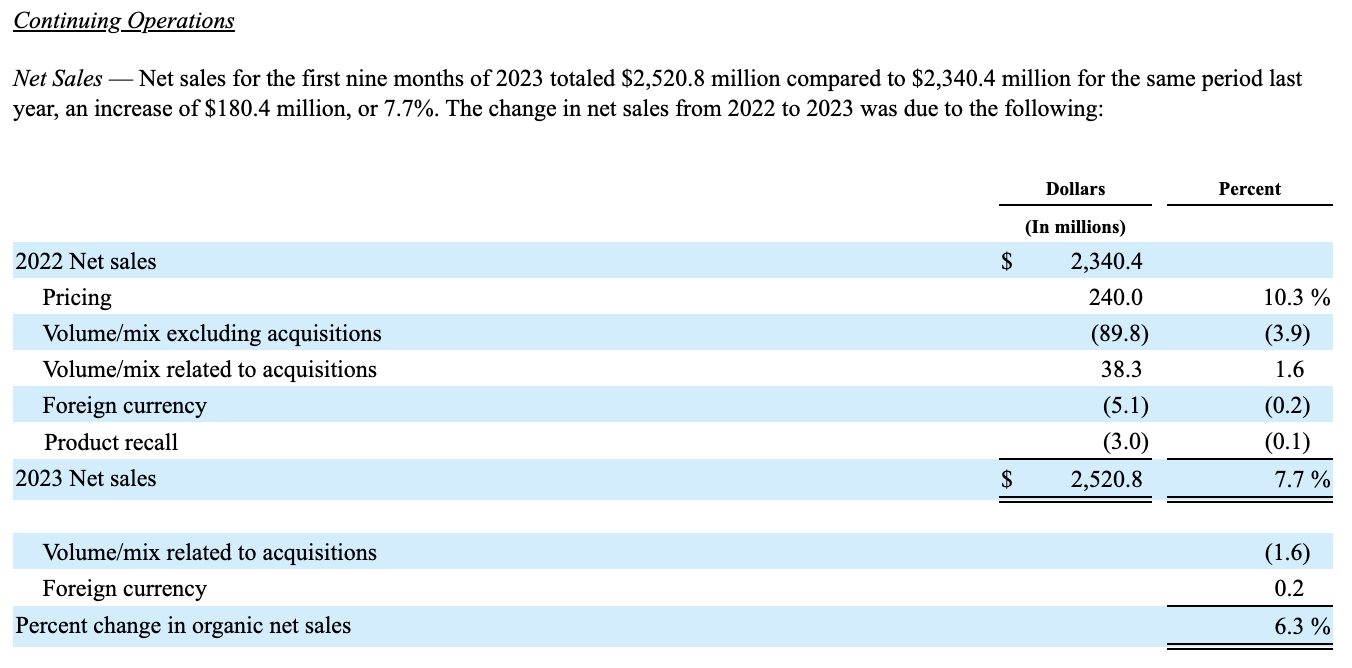

Shifting our focus now to 2023, we can see that revenue growth for the enterprise remained intact. Revenue for the first nine months of the year totaled $2.52 billion. That's 7.7% above the 2.34 billion dollars reported one year earlier. The vast majority of the sales increase that the company saw during this window of time was attributable to higher pricing on its products. This alone added $240 million to the firm's top line. But this was not the only change that the business saw. Acquisitions added another $38.3 million associated with higher volumes of products sold. However, some of this all was offset by weakness elsewhere. For instance, volumes associated with organic operations managed to drop sales to the tune of $89.8 million. The firm suffered another $3 million hit associated with recalling products. And foreign currency fluctuations hit sales to the tune of $5.1 million.

{kind=link}

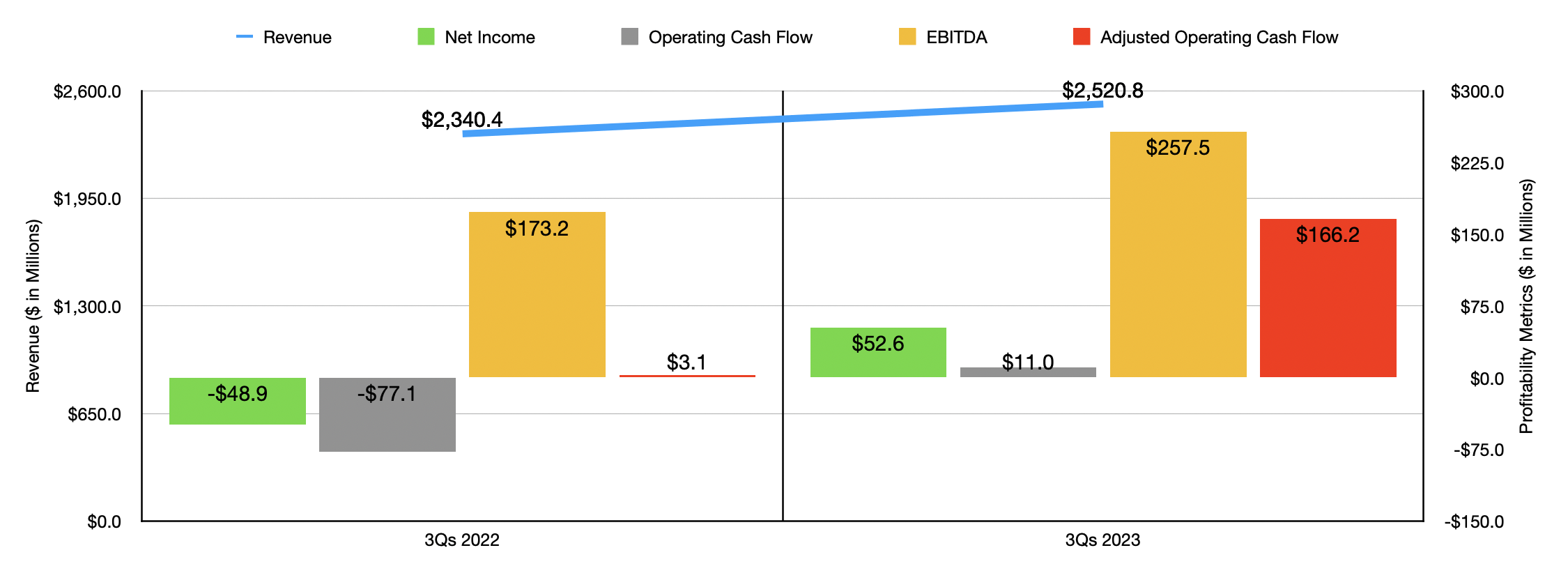

The increase in sales, particularly because it was driven largely by higher pricing, resulted in a meaningful improvement to the company's bottom line. For the first nine months of 2023, TreeHouse Foods generated a net profit of $52.6 million. That's a massive improvement over the $48.9 million loss reported the same time one year earlier. Operating cash flow went from negative $77.1 million to positive $11 million. The adjusted figure for this, which ignores changes in working capital, went from $3.1 million to $166.2 million. And lastly, EBITDA for the company expanded from $173.2 million to $257.5 million.

{kind=link}

When it comes to the 2023 fiscal year in its entirety, management has not provided that much guidance. They did say, however, that adjusted revenue should be somewhere between $3.435 billion and $3.465 billion for the year. That should drive EBITDA to between $360 million and $370 million. Based on my own estimates, at the midpoint, this should translate to adjusted operating cash flow of somewhere around $267.8 million.

{kind=link}

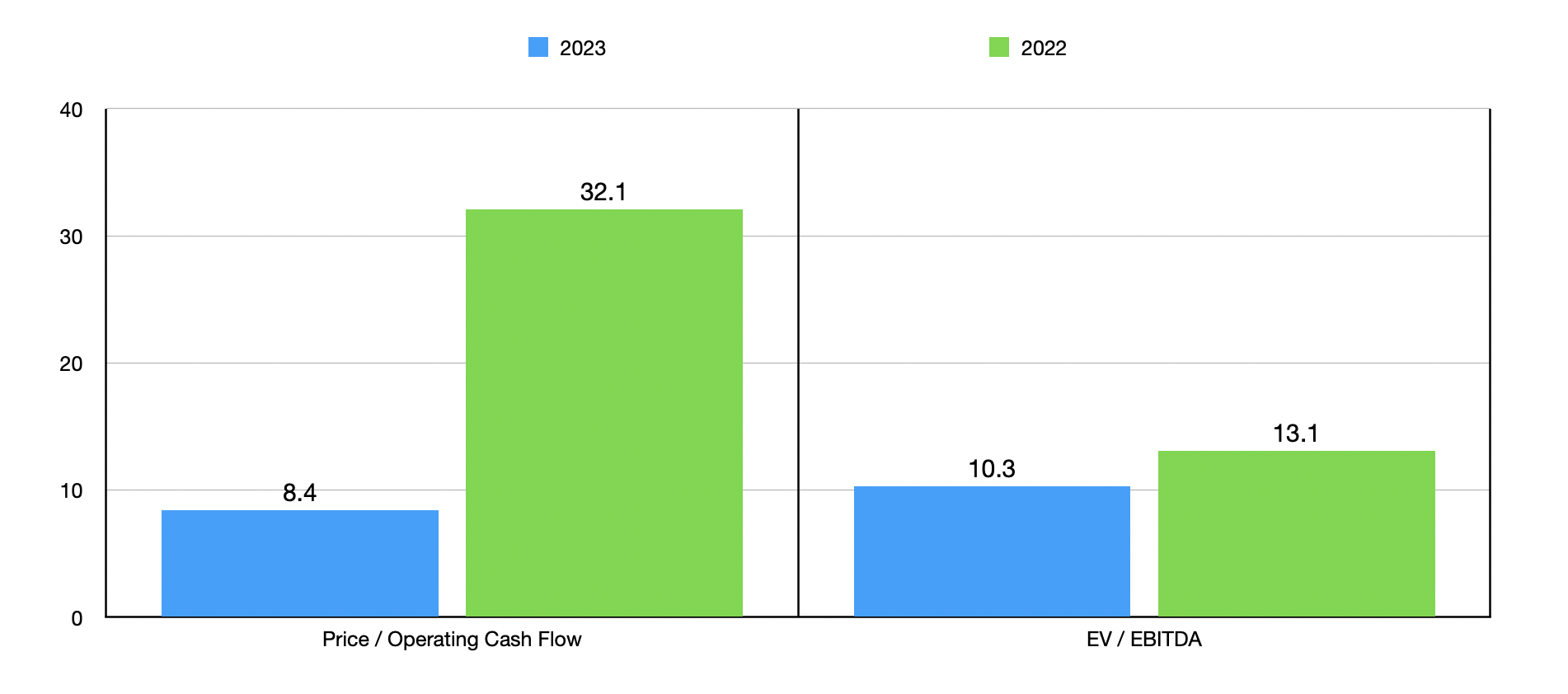

Using these estimates, as an able to value the company as shown in the chart above. On a forward basis, shares do look substantially cheaper than if we were to use the official results from 2022. I then, as part of my analysis, decided to compare the company to five similar companies as shown in the table below. When it came to the price to operating cash flow approach, two of the five businesses ended up being cheaper than TreeHouse Foods. This number drops to one of the five if we look at the picture through the lens of the EV to EBITDA multiple.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| TreeHouse Foods |

| 8.4 |

| 10.3 |

| Utz Brands ( UTZ ) |

| 15.6 |

| 27.9 |

| J&J Snack Foods ( JJSF ) |

| 18.0 |

| 17.5 |

| The Simply Good Foods Co. ( SMPL ) |

| 19.7 |

| 18.2 |

| Cal-Maine Foods ( CALM ) |

| 4.6 |

| 3.1 |

| Whole Earth Brands ( FREE ) |

| 6.6 |

| 228.2 |

In addition to shares being cheap on both an absolute basis and relative to similar enterprises, there's also the fact that management continues to grow the company. While organic growth does exist, a lot of growth recently has come from various acquisitions. The latest such purchase occurred last October. That was of the pickle-branded assets that, at the time, were owned by The J.M. Smucker Co. ( SJM ) and that cost the company $20 million. Those assets should bring in around $60 million in sales annually to TreeHouse Foods. But not everything is about achieving growth. Management is not afraid to sell certain assets. In September, management closed on the sale of its Lakeville, Minnesota manufacturing facility and snack bars business, receiving $61 million in cash.

Takeaway

As things stand, I believe that TreeHouse Foods is a decent business with decent potential to it. Shares are fundamentally cheap at this time and management continues to grow the company’s top line. Despite a mixed 2022 showing from a profit and cash flow perspective, 2023 was far better and management continues to make interesting moves aimed at creating value for shareholders. All of this, combined, makes the company a ‘buy’ candidate in my book despite the poor showing that rating has achieved for me up to this point.

For further details see:

TreeHouse Foods: Recent Strength And Cheap Shares Warrant Upside