TREX - Trex Company: Buyers Beware

2023-05-20 03:36:24 ET

Summary

- Trex Company is too richly valued and now trades above the price target set by analysts.

- The company is not immune to a slump in demand due to a weakening economy.

- Long-term investors should look to buy this stock at a much lower valuation.

- There may not be much upside for short-term investors.

Despite an upgrade from Bank of America analysts, Trex Company (TREX) is richly valued and faces a slowing economy. Any missteps by the company could lead to a steep markdown in the stock. The company has good margins and the potential to outperform the S&P 500 Index ( SP500 ) over the long term if acquired at a lower multiple. From a margin perspective, comparable companies such as Simpson Manufacturing (SSD) trade at a forward PE of 17x and an EV to EBITDA multiple of 11.7x. Investors may have to apply similar multiples on Trex. Given these facts, investors may have to wait for a much lower valuation before buying Trex.

Stalling revenue growth but stellar margins

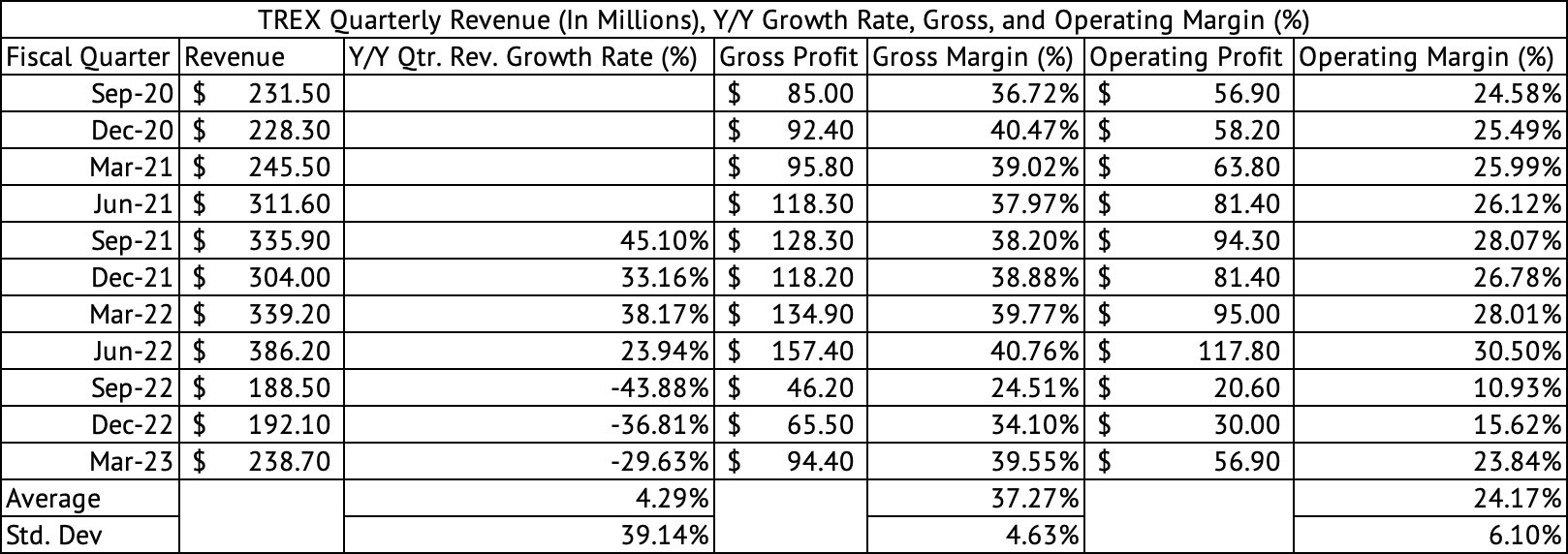

The upcoming quarter, Q2 2023, faces tough comparisons to Q2 2022, when it recorded $386.2 million in revenue and a record gross margin of 40.7%. The company registered sales of $238.7 million in Q1 2023 compared to $339.2 million in Q1 2022 (Exhibit 1) . Analysts expect the company to report $317.18 million in revenue in Q2, representing a y/y drop but a q/q growth. The company has averaged 37.2% in quarterly gross margins since September 2020 and an annual gross margin of 38% since 2013.

Exhibit 1:

Trex Company Quarterly Revenue, Gross, Operating Profits, and Margins (%) (Seeking Alpha, Author Compilation)

{kind=link}

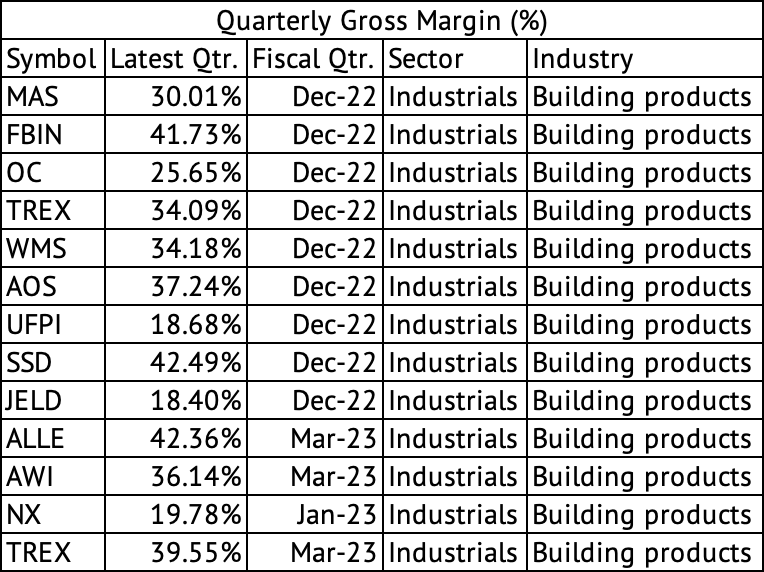

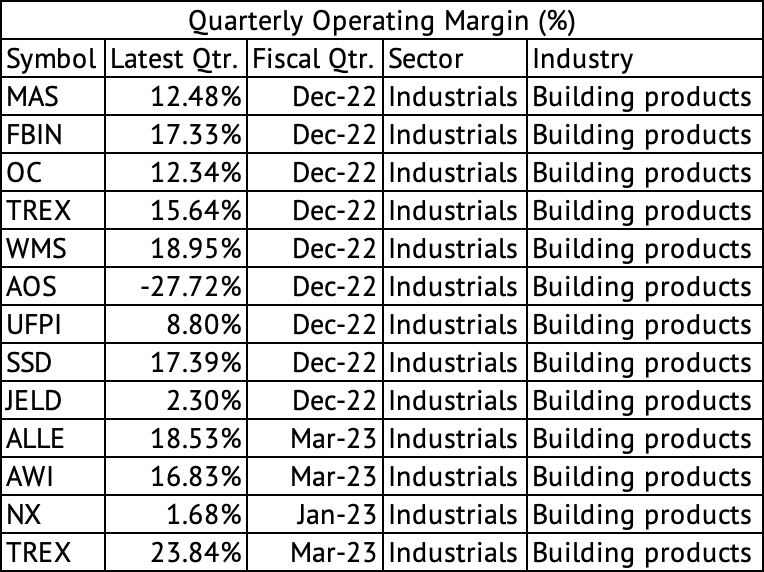

The company has registered significant operating margins with a quarterly average of 24.1% since September 2020. The company's operating margin is the best in the building products industry (Exhibit 3) . It is rare to see a building products company register nearly 40% in gross margins. Trex's gross margin of 39.5% is close to it. Fortune Brands ( FBIN ), Simpson Manufacturing ( SSD ), and Allegion ( ALLE ) are some companies that have achieved 40% or higher gross margins (Exhibit 2) .

Exhibit 2:

Quarterly Gross Margin of Building Products Companies (Seeking Alpha, Author Compilation)

{kind=link}

Exhibit 3:

Quarterly Operating Margin of Building Products Companies. (Seeking Alpha, Author Compilation)

{kind=link}

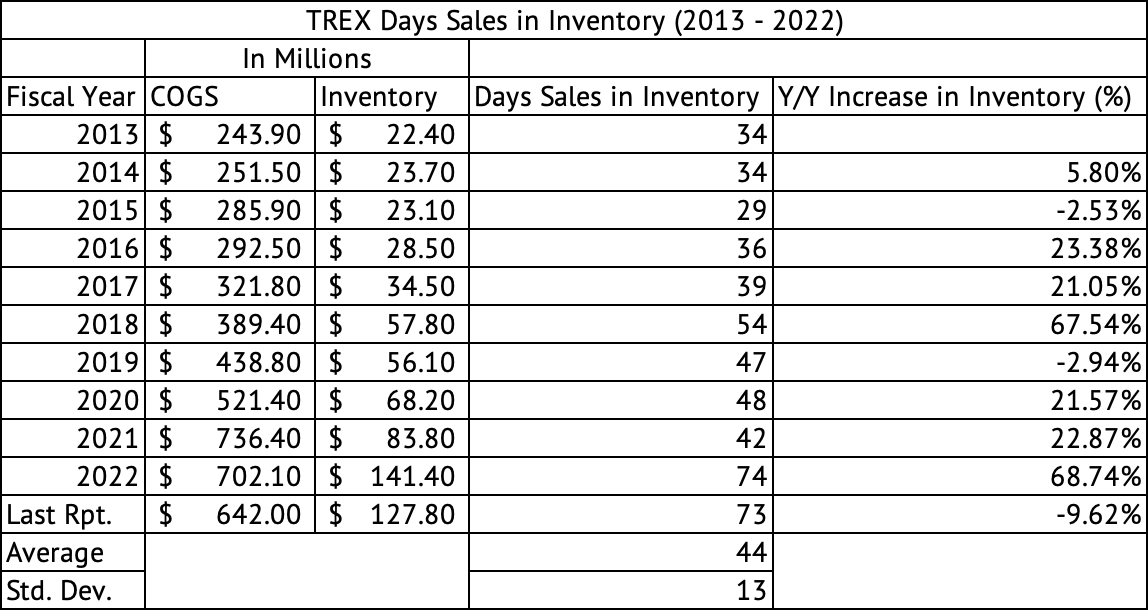

Increase in inventory carrying costs

The company's inventory costs have increased dramatically in 2022. As of the last financial report, the company carried 73 days of sales in inventory compared to its average of 44 and a standard deviation of 13 (Exhibit 4) . The company's inventory cost is one standard deviation above the mean, an extraordinary increase in inventory costs. An increase in accounts receivables and inventory led to a steep decline in operating cash to $26.9 million over the trailing twelve months. Instead of generating cash from its operations, the company used cash of $28.2 million and $115.5 million in the December 2022 and March 2023 quarters.

Exhibit 4:

Trex Annual Inventory Costs (Seeking Alpha, Author Compilation)

{kind=link}

The good news may be that the company's inventory costs have peaked, and as it sells this inventory, its cash flows should improve in the coming quarters. The company's receivables increased in the March quarter as it sold products into its channels in preparation for the spring selling season. The company's cash flows should improve in Q2 as it reduces its accounts receivables. But the company may never attain the operating cash flows it achieved in 2021 and 2022, when it recorded $258.1 million and $216.2 million, respectively. Its operating cash flows revert closer to its 2019 $156.4 million.

High valuation

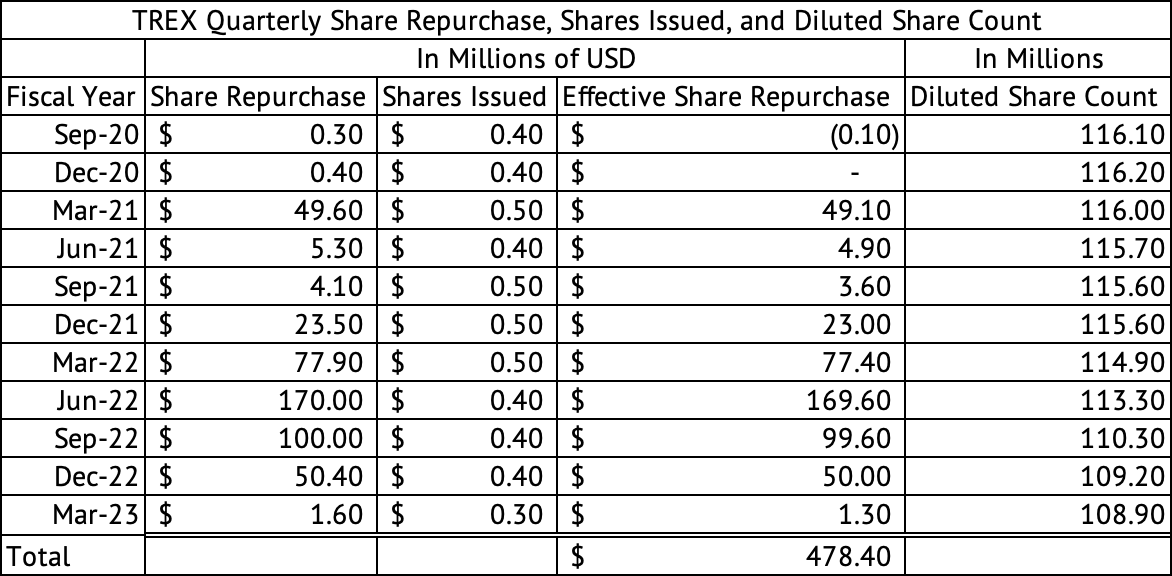

Trex Company looks overvalued on every measure. Trex trades at a forward GAAP PE of 36x and a non-GAAP forward PEG ratio of 2.9x. It sells at a forward EV-to-Sales multiple of 6.3x. Besides, the stock offers no dividend income, but the company does many buybacks. Since September 2020, the company has spent a net amount (after shares were issued) of $478.4 million, reducing its share count from 116.1 million to 108.9, a reduction of 7.2 million or 6.2% (Exhibit 5) .

Exhibit 5:

Trex Quarterly Share Buybacks (Seeking Alpha, Author Compilation)

{kind=link}

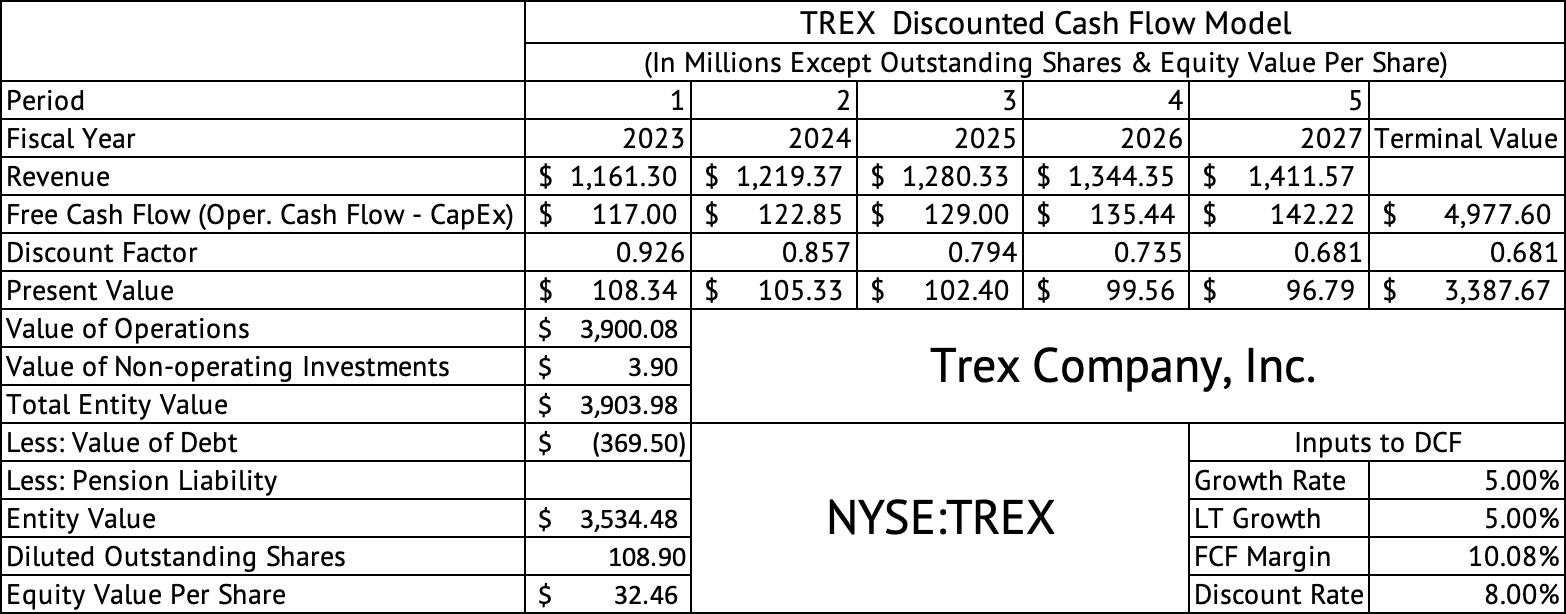

A discounted cash flow model estimates the per-share equity value for Trex at $32 (Exhibit 6) . This model assumes an optimistic growth rate of 5% over the long term. It assumes a 10% free cash flow margin and an 8% discount rate. The company's cost of capital may fall between 8% and 10%. The company's cost of capital may be at 8%, given its low debt levels. As of the quarter ending March 2023, Trex is carrying a short-term debt of $369.5 million and net debt (after cash and short-term investments) of $365.6 million. Its debt-to-EBITDA ratio is 0.36x.

Exhibit 6:

Trex Discounted Cash Flow Model (Seeking Alpha, Author Compilation)

{kind=link}

Given its high valuation, Trex may not be the company to own in a long-term portfolio. The company has no room for error in its execution and cannot afford an economic slowdown or recession. Consumers must continue spending on discretionary items such as a deck for the company to benefit. But consumer debt reached an all-time high of $17 trillion , and consumer spending, which was already slowing in Q1 2023, will slow further. The revenue miss reported by Home Depot (HD) during its earnings released on May 16 may be further proof of a slowing demand or "moderation," as the company's CEO, Ted Decker, called it. According to Mr. Decker, Home Depot predicts a broad weakness in average unit retail across their business, with deflation in lumber prices and unfavorable weather in California affecting its sales.

Trex does not have a competitive moat to protect its revenues and profit margins. Its biggest competition comes from pressure-treated lumber. After a historic increase in lumber prices due to a pandemic-driven supply shortage and stimulus-driven demand, lumber prices have now regressed to the mean (Exhibit 7) . The company also faces competition from other wood-alternative product manufacturers, such as the AZEK Company (AZEK) and Fiberon (part of Fortune Brands (FBIN)). The company's low raw material costs and scale of operations may confer some cost advantages. But, even with these lower cost advantages, the Trex composite decking products may be 35% more expensive than wood.

Exhibit 7:

{kind=link}

Recently, Trex and Azek caught upgrades from analysts at Bank of America. The bank set a price target of $54 for Trex; the stock is trading at $56. Even by Bank of America's price targets, the stock looks overvalued. Composite decking has many advantages compared to lumber, and that may be the reason for the positive comment from Mr. Rafe Jadrosich, an analyst at Bank of America, that composite decking continues taking market share from lumber even as lumber prices have declined in the past year. The analyst also noted that they prefer the Azek Company over Trex due to relative valuation.

The stock has done exceedingly well on a 10-year and 5-year basis, with a total return of 714% and 109%, respectively, compared to 201% and 66% for the S&P 500 ( SP500 ) (Exhibit 8) . But, the company has hit a ceiling on its valuation; it has underperformed on a 3-year and 1-year basis. Trex has returned 0.08% over the past three years compared to 51% for the S&P 500 Index. The company trades 11%, 12%, and 16% above its 50-day, 100-day, and 200-day simple moving average. The stock had good momentum over the past three, six, and nine months, but the stock has dropped 4% over the past year while the Vanguard S&P 500 Index ETF has returned 6.8%. This stock may have more downside given the weakening U.S. economic environment and high valuation.

Exhibit 8:

{kind=link}

Trex has performed exceedingly well over the long term. But, it now trades at a stratospheric valuation. Long-term investors should proceed with caution when considering this stock. The company has a long runway of growth ahead of it but is not immune to an impending economic slowdown or recession in 2023. The stock will take a beating if the U.S. economy enters a recession. Investors may have to wait to own this stock. Once acquired at a fair valuation, investors can hold the stock long-term.

For further details see:

Trex Company: Buyers Beware