TREX - Trex Q4 Results: Inventory Recalibration Mostly Complete Stock Remains Cheap

Summary

- Trex appears to have mostly completed its inventory recalibration efforts.

- Q4 and FY2022 brought decent results given the headwinds. The company profited off the weakness in its share price to buy back record amounts of shares.

- Shares remain cheap, trading with EV/Revenues and EV/EBITDA multiples below the ten year averages.

Trex ( TREX ) has been working very hard in re-calibrating its channel inventory, which is why it was great to hear the company say that they are entering the year with inventory levels that align with market expectations. The company started working on tackling the excess inventory in the channel in July of last year, and it is now more or less where they want it to be. Trex plans to continue decreasing its balance sheet inventory to more normalized levels throughout 2023, which will improve cash flow, as it continues to run its facilities with the assumption of a ~$1 billion revenue run-rate for the year.

There were some other interesting pieces of information shared during the earnings call , including that in Q4 the company completed the sale of Trex Commercial. The company wants to focus on its high-growth and profitable Trex Residential segment. The good news is that this less attractive part of the business will no longer take attention from management, and they will now be able to completely focus on the residential segment.

Unfortunately Trex continues operating at a level below its total capacity, and that will weigh on margins. This is prudent, given that the company expects a mid-single digit decline in demand, measured in volumes. If demand proves higher than expected, that should significantly help margins. The company shared that for every ~$100 million in net sales that they add to production they would be expecting to see about 100 bps to 150 bps of gross margin improvement.

Q4 and FY2022 Results

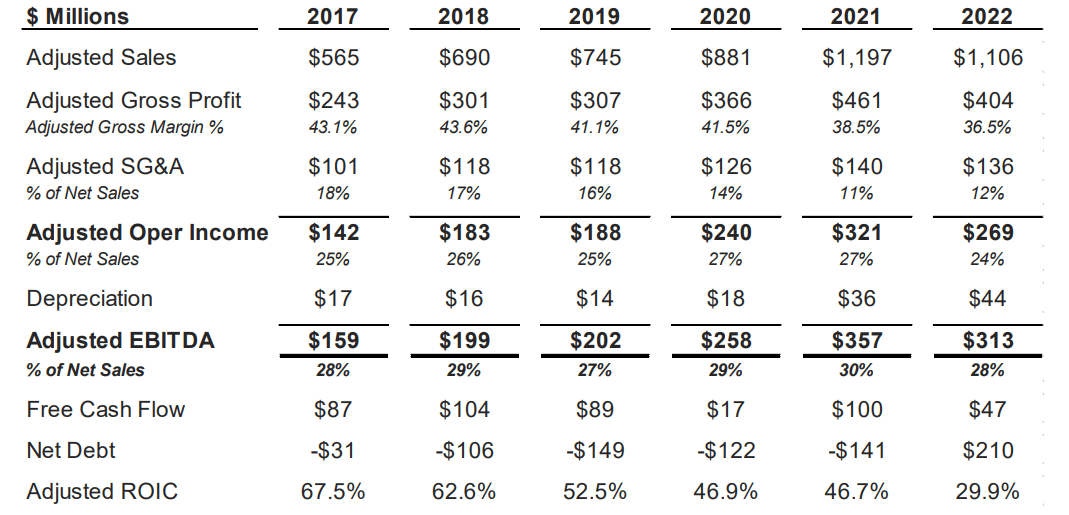

The headline for the fourth quarter was that operating results came in ahead of expectations. Consolidated net sales were $192 million and for the full year were $1.1 billion, a decline when compared to the $1.2 billion in 2021. The company generated operating cash flow of $216 million in 2022 and invested $176 million in CapEx, mostly directed to the new Arkansas manufacturing facility.

In Q4 adjusted net income, which ignores the loss from selling Trex Commercial, was $25 million or $0.23 per diluted share. Full year 2022 net income was $185 million or $1.65 per diluted share, a decline when compared to the $209 million or $1.80 per diluted share in the previous year. The company ended the year with net debt of $210 million.

{kind=link}

Growth

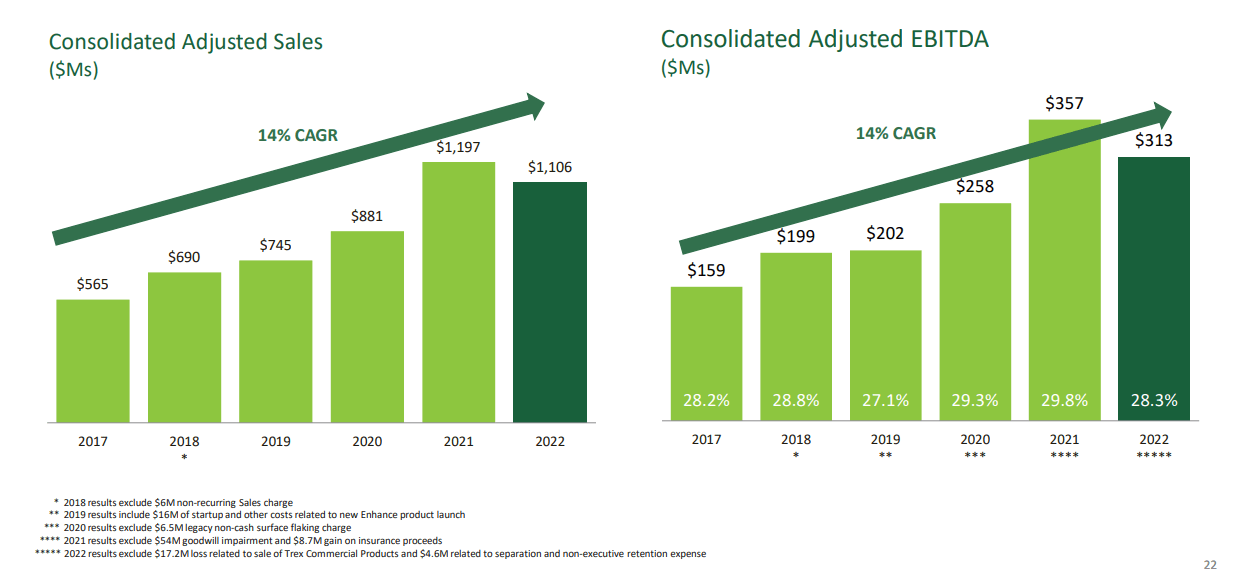

While 2022 was a disappointing year, and 2023 looks complicated as well, it is worth looking at the big picture. Zooming-out it is clear that this is a growth company, that has increased sales and earnings at a very solid pace. If analysts are correct, the company should be posting sales records again by FY2025. We think there is a good possibility it might even happen in FY2024.

{kind=link}

Buybacks

Trex returned a record amount to shareholders in the form of buybacks in 2022. It spent roughly $395 million to repurchase ~6.5 million shares, which comes to an average of ~$60 per share. It still has ~1.5 million shares remaining under its share repurchase program. Just in the fourth quarter the company bought ~1.1 million of its shares for $50 million, meaning it paid only about ~$45 per share. Thanks to the significant share repurchases, the number of diluted shares outstanding has been decreasing significantly.

Arkansas Facility

Trex's existing facilities don’t have much room for additional buildings or additional capacity, which is why it decided to build a third site. This third production location is going to be in Arkansas. Total investment is planned at ~$400 million. This investment was originally planned to occur through late 2024, but the company has updated its plans so that the investment will be made through 2025 and into 2026. In other words, the company is in no hurry to complete this new facility, as demand for the next couple of years is still expected to be relatively soft.

Still, the new manufacturing facility in Arkansas will give the company the capacity to take full advantage of future demand growth. The facility is expected to have a gradual manufacturing ramp, starting with processing of recycled materials, and then moving to decking manufacturing by early 2026.

Guidance

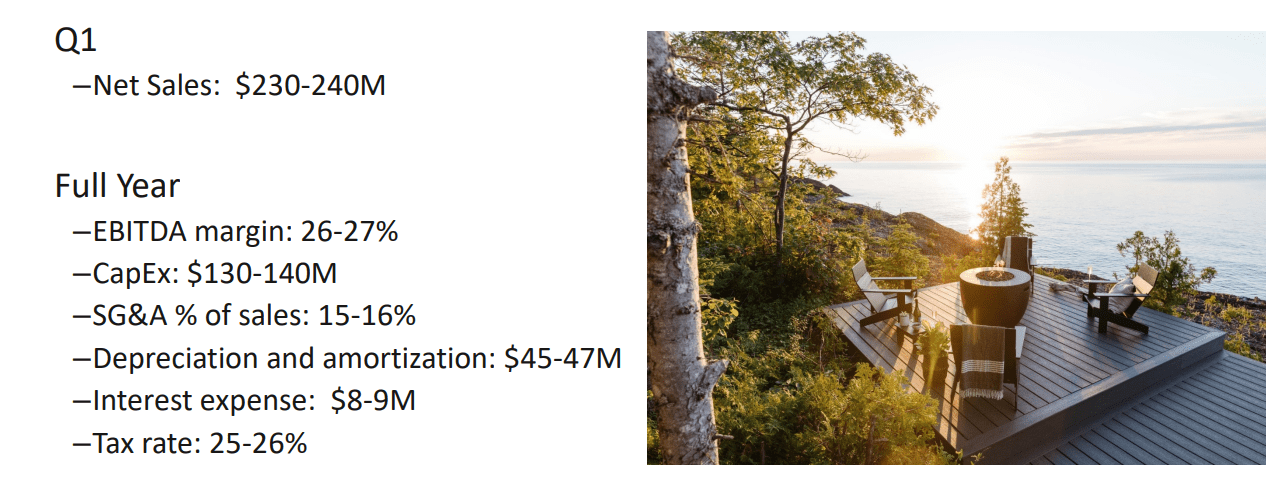

Trex expects Q1 of 2023 net sales to be in the range of $230 million to $240 million. For the full year it expects an EBITDA margin between 26% and 27%, and CapEx of $130 million to $140 million, most of it directed towards the build-out of the Arkansas facility. While the company did not provide full year sales guidance, we think the average analyst estimate of ~$1 billion is reasonable.

{kind=link}

Valuation

We believe shares remain cheap, trading with an EV/Revenues multiple below the ten year average of ~5.7x. There is still a lot of pessimism that this year will be a tough year for the company, which we believe is creating this opportunity to buy shares at a below average valuation.

Similarly, shares are trading with an EV/EBITDA multiple below their ten year average. This includes the forward EV/EBITDA, which is higher than the trailing twelve months multiple, given the expectation that earnings will be lower in 2023.

Analysts expect earnings to have mostly recovered by FY2024/FY2025. We view the FY2025 p/e ratio of ~24x as attractive, given the company's history of growth and attractive profit margins.

Seeking Alpha

Risks

The main risk we currently see for investors is that a potential recession could make things even more difficult for the company. Trex is already dealing with a significant slowdown in the construction industry, in large part as a result of rising interest rates. A recession would make this complicated macro environment much worse. This risk is mitigated by the company's very strong balance sheet and high profit margins. This is reflected in Trex's off-the-charts Altman Z-score. It is also worth mentioning that shares are very volatile with a high Beta.

Seeking Alpha

Conclusion

We believe that the current valuation does not give Trex enough credit as the world’s largest manufacturer and market leader of wood alternative composite decking. Despite the tough macro conditions, Trex still managed to deliver very decent results. It is likely that 2023 will remain a difficult year for the company, but headwinds should start dissipating next year. The current pessimism offers the opportunity to buy shares in a very high quality growth company at a very reasonable valuation. After reviewing the Q4 and FY2022 results, and seeing that the valuation remains attractive, we are maintaining our 'Strong Buy' rating.

For further details see:

Trex Q4 Results: Inventory Recalibration Mostly Complete, Stock Remains Cheap