TY - Tri-Continental Corp: Thank You For Delivering A Solid 2023

2023-12-03 08:43:39 ET

Summary

- Tri-Continental Corporation is a well-managed closed-end fund with strong long-term performance and a sustainable distribution yield.

- TY is well positioned in the current equity markets, with top holdings in leading growth stocks like Microsoft, Apple, Alphabet, Meta, and Nvidia.

- TY has consistently delivered impressive returns over the long-term and pays distributions based on earnings, unlike "return of principal" funds.

A year ago, I wrote an initiating article on the Tri-Continental Corporation ( TY ), calling it a hidden gem of a closed-end fund ("CEF"). In my opinion, TY is what every CEF should aspire to be: solidly managed with strong long-term performance while paying a sustainable distribution yield.

As we near the end of 2023, let us review Tri-Continental's performance in the past year and see if there are any developments worth highlighting.

Brief Fund Overview

The Tri-Continental Corporation is a long-term capital appreciation focused CEF. The TY fund primarily invests in equities, but has the flexibility to invest across a company's capital structure. The TY fund has $1.7 billion in assets and charges a relatively low 0.62% annual expense ratio.

Tri-Continental was established in 1929 and is one of the longest-operating closed-end fund in the market. The fund is currently managed by Columbia Management Investment Advisers, LLC ("Columbia Management"), a subsidiary of Ameriprise Financial ( AMP ).

As mentioned above, Tri-Continental has the flexibility to invest in all types of securities including common stocks, bonds, preferred stocks, and any other securities the investment manager deems suitable to achieve its investment objectives. As of October 31, 2023, the TY fund is 68.6% invested in equities, 18.6% invested in bonds, and 7.3% invested in other securities (Figure 1).

{kind=link}

Portfolio Well Positioned For Current Markets

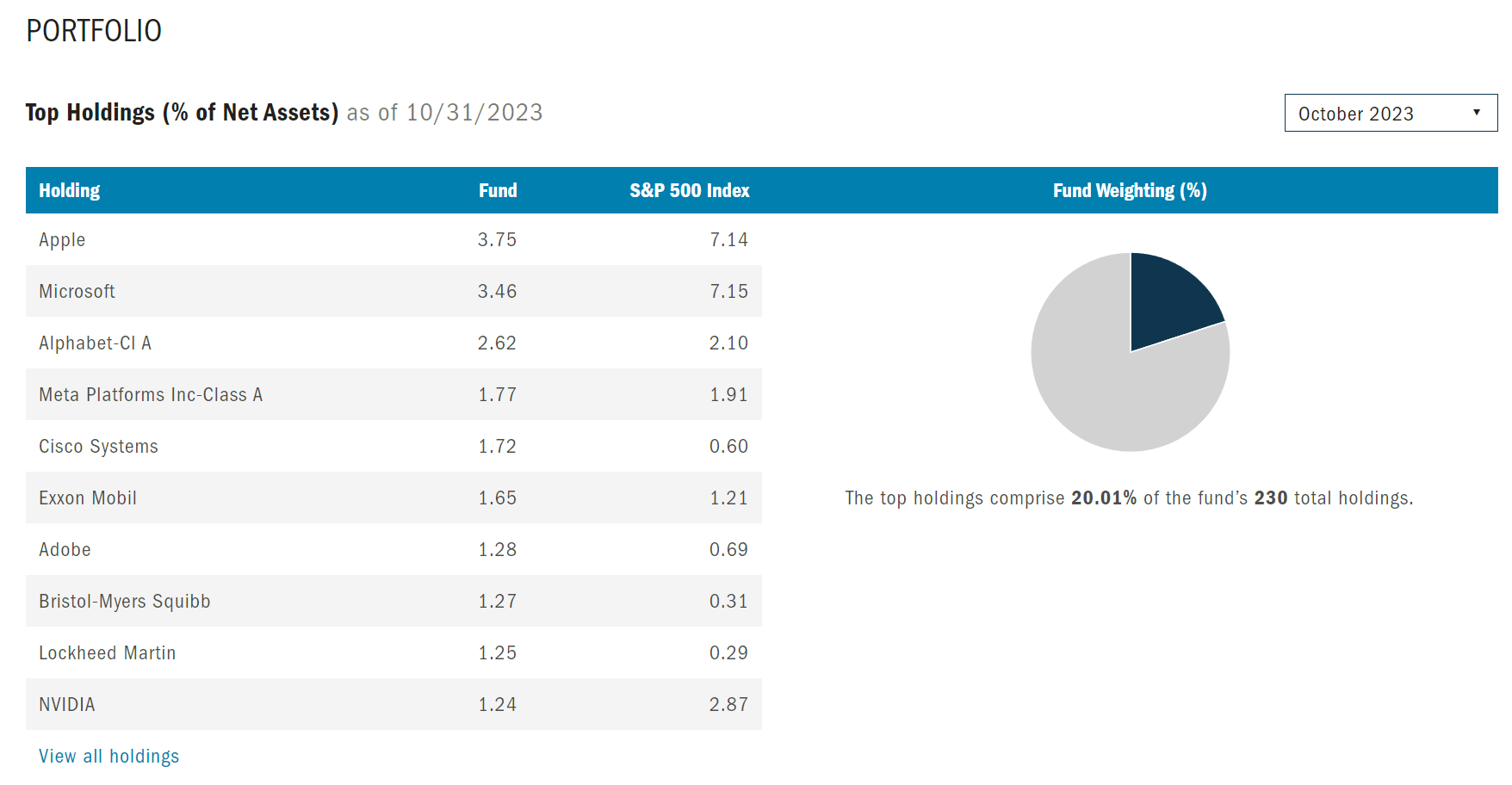

As of October 31, 2023, the TY fund held 230 positions with the top 10 holdings accounting for 20% of the fund (Figure 2).

{kind=link}

Looking at Tri-Continental's current portfolio in detail, it appears the TY fund is well positioned for the current tough equity markets, as the fund's top holdings are concentrated in leading growth stocks like Microsoft, Apple, Alphabet, Meta, and Nvidia that are collectively called the Magnificent 7 .

This has allowed the TY fund to return 11.2% YTD to November 30, 2023, a strong performance for 'balanced' funds with fixed income allocations.

Consistent Performance Over The Long-Term

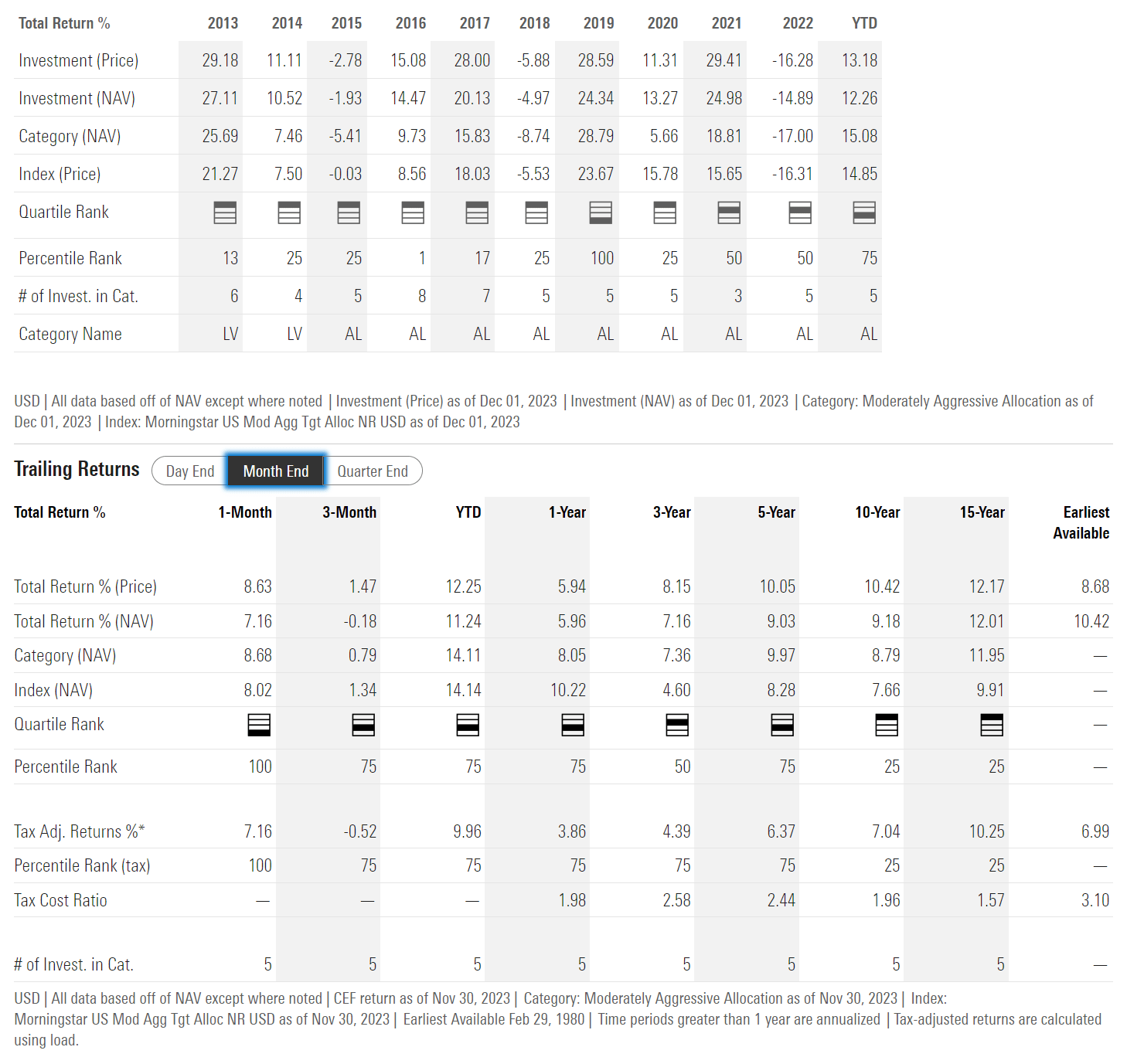

In fact, one of the features I find most impressive with Tri-Continental is its remarkably consistent historical performance. Over the trailing 3/5/10/15-year timeframes to November 30, 2023, the TY fund has returned 7.2%/9.0%/9.2%/12.0% respectively (Figure 3).

{kind=link}

Furthermore, in terms of risk-adjusted returns, the Tri-Continental has been able to deliver returns comparable to its Moderately Aggressive Allocation peers with significantly lower volatility (Figure 4).

Figure 4 - TY delivers similar returns compared to peers with less volatility (morningstar.com)

{kind=link}

Model Of How CEF Should Pay Distributions

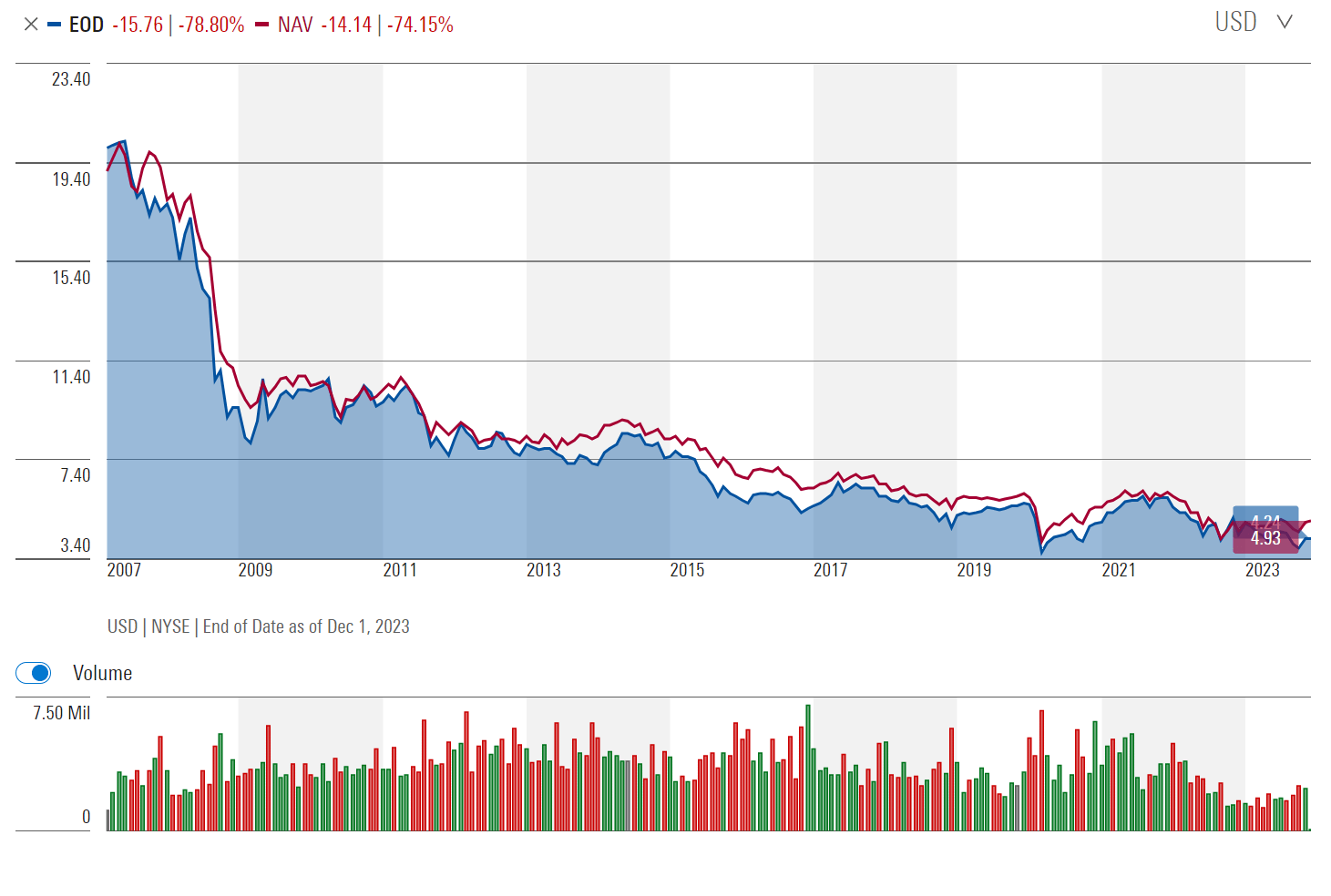

Long-term readers will note that I have been very critical of closed-end funds that pay distribution yields far higher than what the funds can earn. I call these 'return of principal' funds, and they are characterized by amortizing NAVs. The Allspring Global Dividend Opportunity Fund ( EOD ) is a 'return of principal' fund that I have recently written about. Its NAV profile is shown in Figure 5.

{kind=link}

The reason 'return of principal' funds should be avoided is very simple. First, as we can see from Figure 5 above, the market price of closed-end funds typically tracks their NAVs. As NAV gets amortized, the market price declines. So, investors who buy these amortizing 'return of principal' funds will see the market value of their holdings decline over time.

Furthermore, the liquidation of NAV to pay distributions is a sign that the fund does not earn sufficient returns. As NAV gets sold off, there are less assets to earn income to fund future distributions, so more assets need to be sold off, a deadly negative spiral. Over time, we find these 'return of principal' funds tend to shrink their distributions in line with their declines in NAV (Figure 6).

Figure 6 - EOD has a shrinking distribution (Seeking Alpha)

In contrast, Tri-Continental pays a quarterly distribution that is variable and dependent on the earnings of the fund. The TY fund also pays periodic special distributions funded by capital gains.

For 2023, Tri-Continental has declared or paid $1.11 in regular distributions, or a ~4.0% yield. It has also declared or paid $0.1444 / share in special distributions (Figure 7).

{kind=link}

In good years like 2021, Tri-Continental's special distributions can be quite substantial, as the fund paid a total of $4.6901/ share in distributions ($1.0549 in income and $3.6352 in capital gains) or a 14.3% year-end yield.

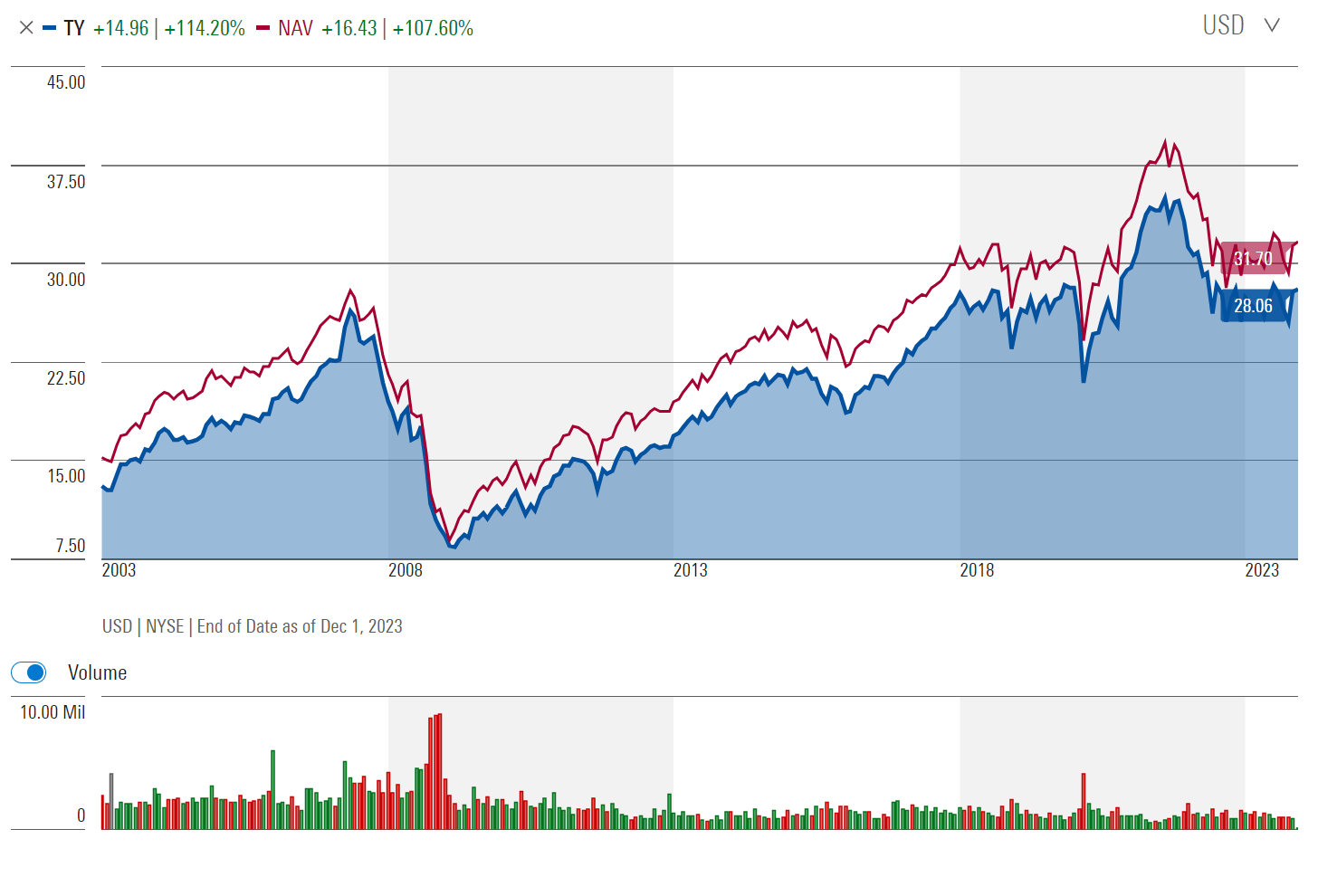

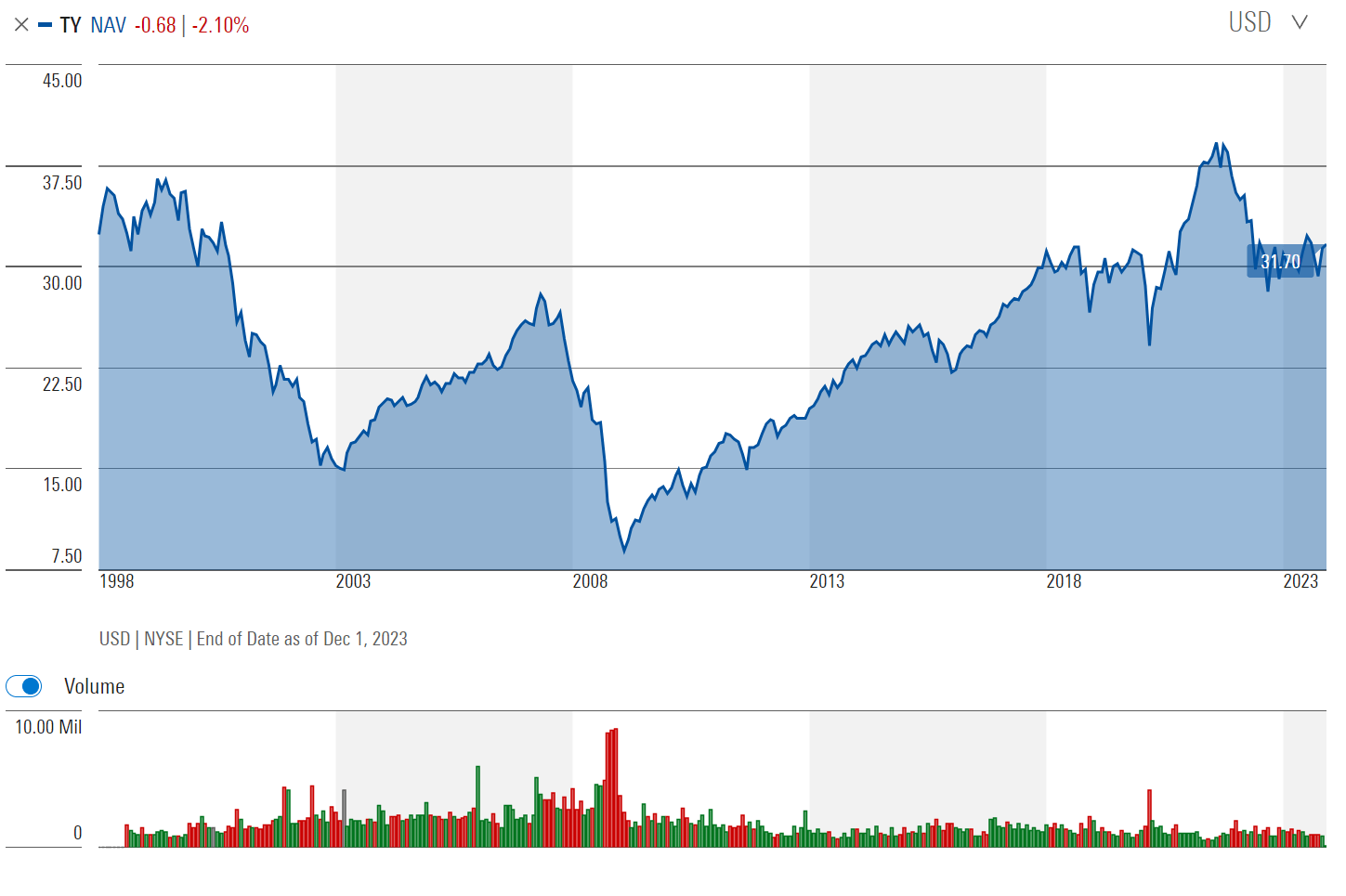

Despite paying over $23 in distributions over the past 20 years, Tri-Continental's NAV has actually doubled, from $15 in 2003 to over $31 recently (Figure 8).

{kind=link}

So, investors in accretive funds like Tri-Continental saw growth in both principal and income, contrary to 'return of principal' funds.

Risks To Tri-Continental

While I like Tri-Continental's long-term performance, that does not mean the fund is riskless. For example, as we showed in Figure 2 above, the Tri-Continental has relatively large weights to the Magnificent 7 stocks. If the Magnificent 7 were to underperform, then the TY fund could also be negatively affected.

This risk has been nagging at me in recent months, as the current 'AI bubble' has striking similarities to the 'dotcom' bubble from 2000. For example, leading AI stocks like Nvidia is currently trading at a ridiculous 20x forward sales. Investors should be wary any time they see stocks trade over 10x sales.

In the words of Scott McNealy, former CEO of Sun Microsystems, one of the darlings of the dot-com bubble:

“…2 years ago we were selling at 10 times revenues when we were at $64. At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

Following the dotcom bubble, the TY fund suffered a peak-to-trough decline of 59% in its NAV, and the fund's NAV did not exceed its pre-2000 peak until 2021 (Figure 9).

Figure 9 - TY suffered a large drawdown following dot-com bubble (morningstar.com)

{kind=link}

If a similar scenario were to occur, funds like TY with large exposures to the AI darlings (MSFT, META, NVDA) could be vulnerable.

For now, I am keeping a close eye on the Federal Reserve's monetary policies. If we look at history, the dot-com bubble and the 2008 housing bubble did not burst until the Fed started cutting Fed Funds rate (Figure 10). As long as the economy performs well and the Fed remains on hold, growth stocks may yet reaccelerate into year-end and beyond.

Figure 10 - Historical overlay of Fed Funds rate and Nasdaq 100 performance (Author created with charts from St. Louis Fed)

Conclusion

The Tri-Continental remains one of my favorite closed-end fund holdings, as it has delivered strong long-term performance that has allowed me to sleep well at night. My only concern with Tri-Continental is its exposures to leading 'AI' stocks like Microsoft and Nvidia that could make the fund vulnerable if the 'AI bubble' were to burst.

I continue to recommend the TY fund as a buy for growth-oriented investors looking for income.

For further details see:

Tri-Continental Corp: Thank You For Delivering A Solid 2023