TOLWF - Trican Well Service: 3 Reasons To Own The Stock

2023-07-18 09:07:36 ET

Summary

- Trican Well Service has managed its business effectively through industry downturns, maintaining a clean balance sheet and bouncing back well in the last two years.

- Despite a bearish energy sector, Trican trades at a price-to-earnings multiple of 7.6x and has seen a 35% growth in revenues, indicating a potential good long-term investment.

- The company's management is confident in the strong global demand for oil and natural gas, and the construction of additional export capacities in Canada creates a favorable environment for Trican's services.

Reason 1: Managing the business

Trican Well Service ([[TOLWF]], [[TCW:CA]]), based in Canada is a leading provider of oil and natural gas well servicing equipment and solutions offering a comprehensive range of services throughout the drilling, completion, and production processes. Their offerings include hydraulic fracturing, cementing, coiled tubing, nitrogen services, and chemical sales, primarily serving the oil and gas industry in Western Canada.

What I am most impressed about is how well they have managed their business through the downturns of this industry. In the last 15 years, the oil industry has had three prominent downturns and many companies got completely decimated.

- More than 100 oil and gas companies declared bankruptcy in 2020

- Almost 150 bankruptcies during the oil bust of 2015-2016

- The great recession had rolling effects on the industry much after 2010

Through all these downturns the company managed to stay nimble and survive. Through a combination of acquisitions , divestitures , debt management, stock buyback, and dividend management the company has been able to react and adapt as required. The end result is even with inconsistent profitability, the company has a clean balance sheet.

Coming out of a bad 2020, the business bounced back really well over the last two years. In the latest quarter, the management committed to a dividend of $0.04 per share and for the first three months of the year, the Company also purchased 9.8M of its own stock funded through operating cash flow. All in all, this speaks to the sound management of the business in good times and bad.

The above chart shows a net reduction in share count over the last five years due to stock buybacks implemented by the company.

Reason 2: Discount valuation

The company trades at a Price to earnings multiple of 7.6x which is in alignment with the sector as a whole (The energy sector's median is 7.1x) This reflects the current environment of energy stocks, especially the oil and gas industry. After experiencing a roaring 2021; 2022 and 2023 have been quite muted . There have been repeated cuts on the supply side but a pessimistic economic outlook has not helped much. All of this has contributed to bearishness in the energy sector, resulting in a depressed valuation for the industry as a whole. In my opinion, this is a good time to pick up quality companies and hold for the long term.

A dark economic forecast did not mean much for Trican. For the latest quarter, the company grew 35% in revenues, and diluted EPS improved 300%. This results in an extremely low PEG ratio of 0.02. This may not mean much if earnings do not continue to grow but management is quite confident of 2023 as discussed in their outlook.

Reason 3: Outlook

Management thinks that the global demand for oil and natural gas will be strong due to their widespread use in various products and industries. Ongoing geopolitical tensions have led countries to prioritize secure of environmentally sustainable energy sources. Canada, with its high environmental and regulatory standards, is an important supplier of choice for oil and natural gas. The construction of additional export capacities, such as the Trans Mountain pipeline, Coastal GasLink Pipeline, and LNG export facilities ensures a sustainable long-term supply. These factors create a favorable environment for oil and natural gas development in Western Canada and the associated oilfield services for which Tristan acts as a key supplier.

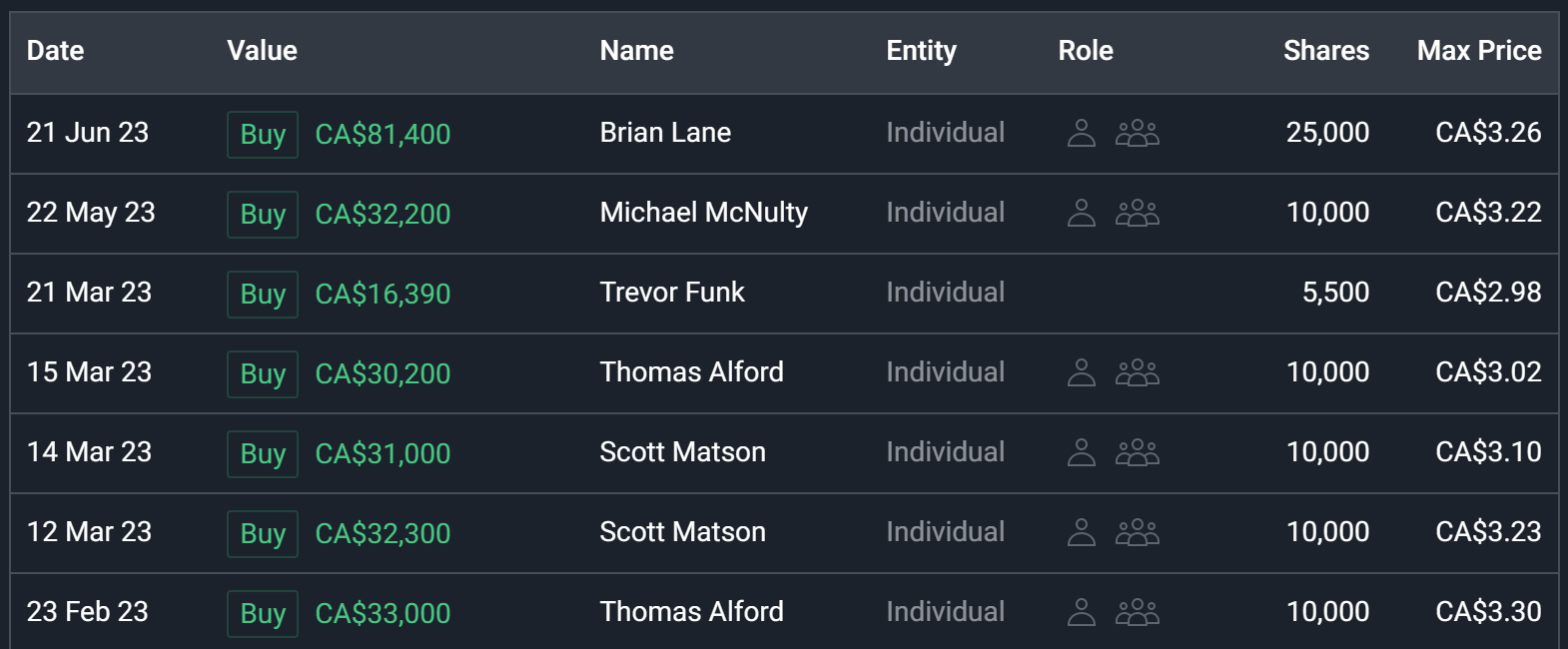

There is no greater proof of the management's confidence than when you see them actively buying their own stock. This year alone there have been seven total instances of insider buys by the CFO, director, and chairman.

{kind=link}

Final Call

I rate this company as a buy. Oil and Gas businesses are inherently risky due to the nature of the business undergoing boom and bust every few years. But the management in this business has proven themselves beyond doubt that they are able to navigate and survive as a company during bad times and get back to growth during good times. The company has fallen far from its all-time highs but the clean balance sheet and expected growth seem like a good entry point into the company at this point in time.

For further details see:

Trican Well Service: 3 Reasons To Own The Stock