TCN - Tricon Residential Is Cheap Relative To Its Growth

Summary

- TCN has greater opacity than its peers and is getting punished for it.

- While that makes it more work to study and own, the fundamentals look good.

- Thus, I think the discount represents opportunity.

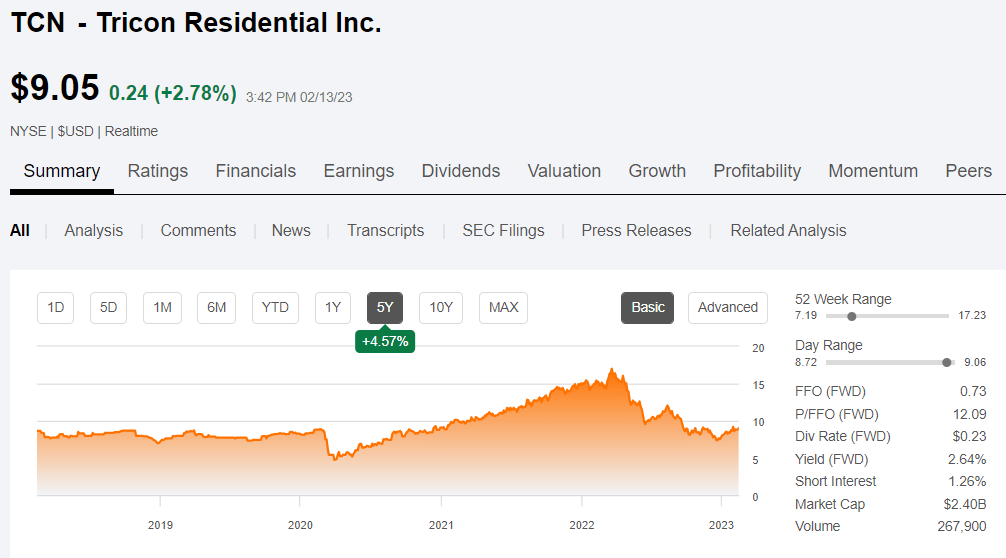

I am always scanning the real estate universe for mispricing and one of the most reliable ways to find it is wild price swings in the presence of stable fundamentals. Based on recent market action, Tricon Residential ( TCN ) is likely to be mispriced.

{kind=link}

Single family rental fundamentals have been strong and quite steady with moderate to fast paced organic growth. Despite this steadiness, TCN stock has fluctuated from the low $5s to above $16 and now sits back at about $9.

With price deviating so extremely from fundamentals we can say with a high degree of certainty that this stock has been wildly mispriced. Through fundamental analysis we intend to uncover whether it was overpriced at $16 or underpriced now at $9.

In brief, fair value is somewhere in the middle, I think in the $11 to $12 range. Following is the analysis that led to this judgement.

Company overview and strategy

Tricon is a relatively small single family rental company in terms of market cap, sitting at about $2.4 billion, but it is involved in over $30B of assets. This discrepancy is a result of extensive use of joint ventures in which Tricon has a minority stake. Thus, its financial commitment is only a fraction of the asset value.

I dislike joint ventures in general for 2 reasons:

- It adds a great deal of opacity.

- The waterfall is usually unfair. An 80/20 joint venture usually does not pay out 80% and 20% of profits, respectively.

The market also seems to dislike joint ventures as companies that rely heavily on joint ventures tend to trade at a discount to peers. TCN is no exception with a significantly lower multiple than the SFR REITs.

However, in this case, the unfair waterfall seems to fall in Tricon’s favor with their overall share of profitability generally surpassing their financial investment in the property. Tricon is usually the managing partner and collects a fee for managing the properties and this fee results in their earnings from the JV exceeding their pro-rata share.

Fees earned by TCN accrue to shareholders in the same way that earnings from a property would. So while I don’t like the murkiness that comes with joint ventures, this is an instance in which the structure is well utilized on behalf of shareholders.

Both fee income and property income are related to the property performance. Thus, Tricon’s fundamentals can be analyzed in the same way as a REIT directly and fully owning its properties.

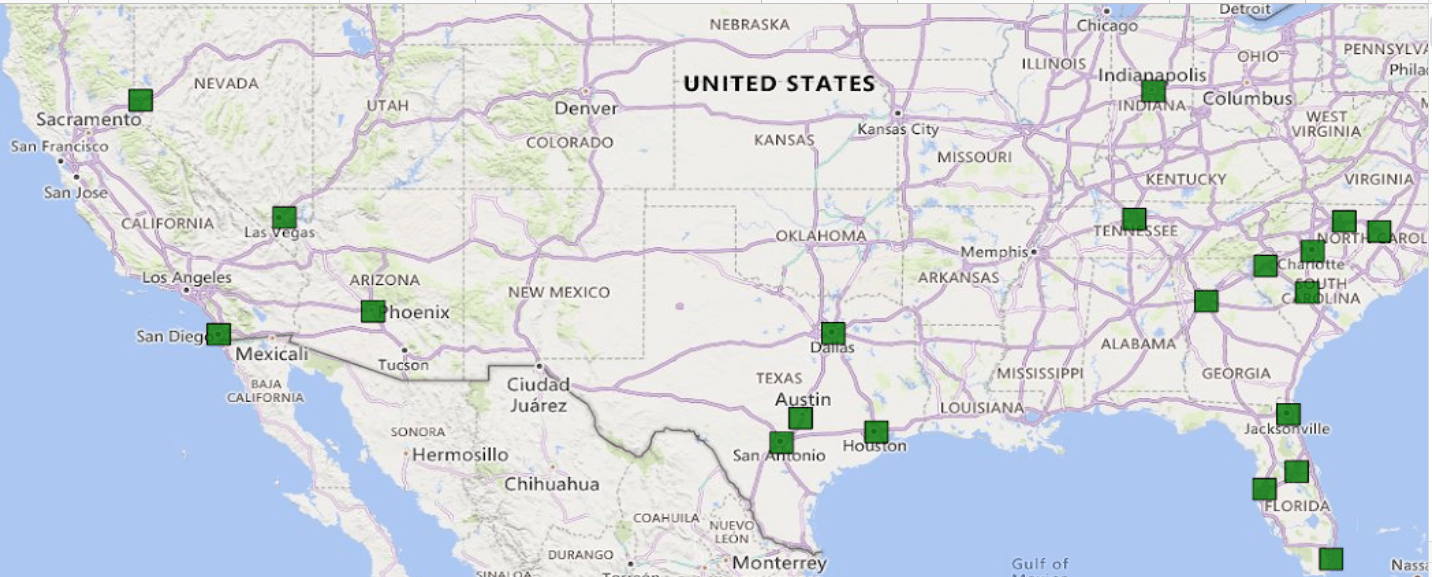

Property Portfolio

Despite being a Canadian domiciled company with headquarters in Toronto, the bulk of its portfolio is in the U.S.

{kind=link}

The U.S. properties are single family rental with a few apartment complexes in Toronto.

These are what I would call typical middle class homes – about 1700 square feet and the rent is fairly affordable at just over $1700 per month. Price wise, that puts them in competition with Class B apartments but it tends to appeal to a different demographic. More families, less single people. This means more stability and much longer length of stay.

For apartments, annual tenant turnover is about 40%+ while TCN has turnover under 20%. Longer stay means less capex and generally high profit margins which sat at 68.5% in 3Q22.

Growth outlook

Single Family rental was one of the biggest beneficiaries of rapidly rising mortgage rates for 2 reasons:

- Substantially reduced pace of new home construction which is keeping competing supply low.

- Improved relative affordability.

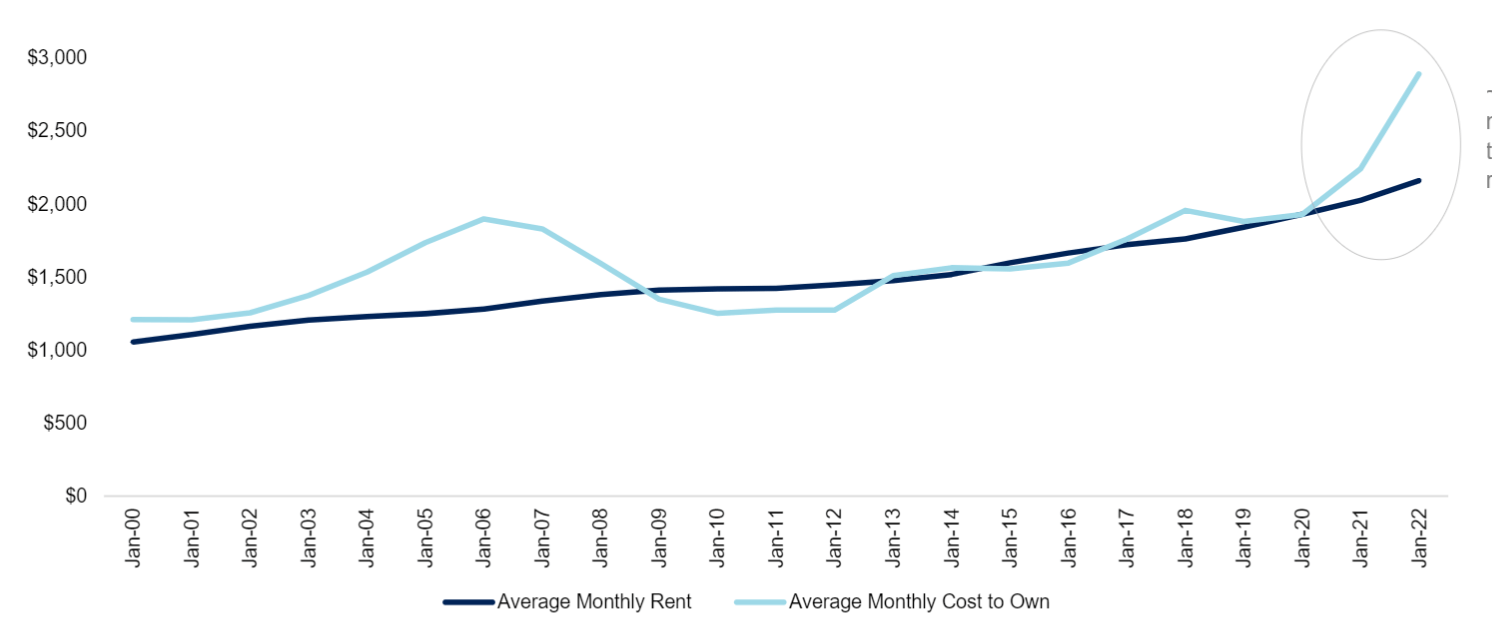

Higher mortgage rates increase the monthly cost of owning a home which has made renting attractive as an alternative.

{kind=link}

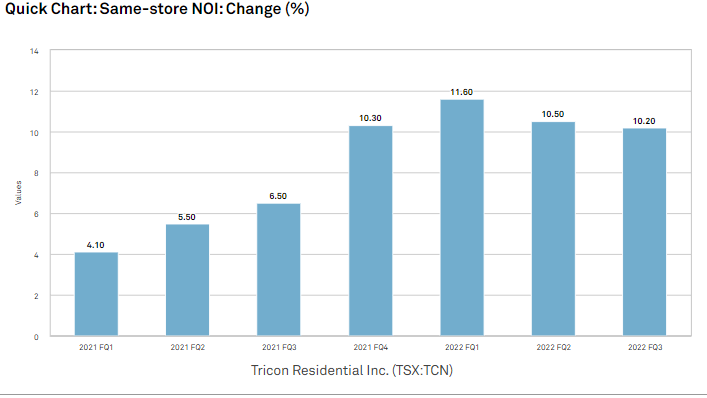

This means that families considering buying a home may spend the next few years in SFR instead. Organic growth has been quite strong from a combination of occupancy increases and rental rate growth.

{kind=link}

Given the increased demand from higher mortgage rates I think there is significant upside to rental rates. Occupancy has likely peaked as it is already at about 98%. Thus, I think same store NOI growth will likely slow to about 7% but that is still a phenomenal number.

Why Tricon’s market price collapsed

$16 down to $7.50 is quite the fall. It has since recovered to about $9 but that is still a dramatic downdraft which I don’t think lines up with Tricon’s individual business or SFR fundamentals.

I think the fall comes down to 2 data points which have been misinterpreted as a much gloomier outlook than what I view as the realistic range of outcomes.

Data point 1) Tricon’s 3Q22 call prominently featured a discussion of Tricon pulling back on growth.

Gary Berman on the 3Q22 call:

“We plan to decelerate our acquisition pace to 850 homes in Q4 and 7,300 homes for the full year, which is still a record for Tricon. While this falls short of our previous guidance of 8,000 homes, we feel this is prudent given today's capital markets environment, where financing rates have climbed much faster than acquisition cap rates and where the securitization market is going through a period of price discovery.”

Data point 2) FFO/share is forecast to drop significantly in 2023.

Consensus estimates show FFO/share at $0.60 for 2023.

{kind=link}

That appears to be significantly negative growth as consensus for 2022 is $0.72. Tricon’s guidance for 2022 is even higher with Core FFO of $0.75 to $0.77.

{kind=link}

So, the 2 data points the market is working with are the CEO talking about pulling back on growth and FFO/share dropping significantly.

I can understand why that looks rough and why that would cause the huge drop in market price.

However, if we dig deeper I think it becomes clear that nothing is actually wrong here. Recall that as a Canadian company TCN uses IFRS instead of GAAP. Well, the IFRS reconciliation from net income to FFO is not quite as clean as the GAAP reconciliation from net income to FFO.

We are going to get in the weeds a bit here but basically what I am getting at is that there is no drop in FFO/share. FFO/share was never actually at $0.72 or the guided $0.75-$0.77. That is just an artifact of IFRS not being particularly compatible with FFO.

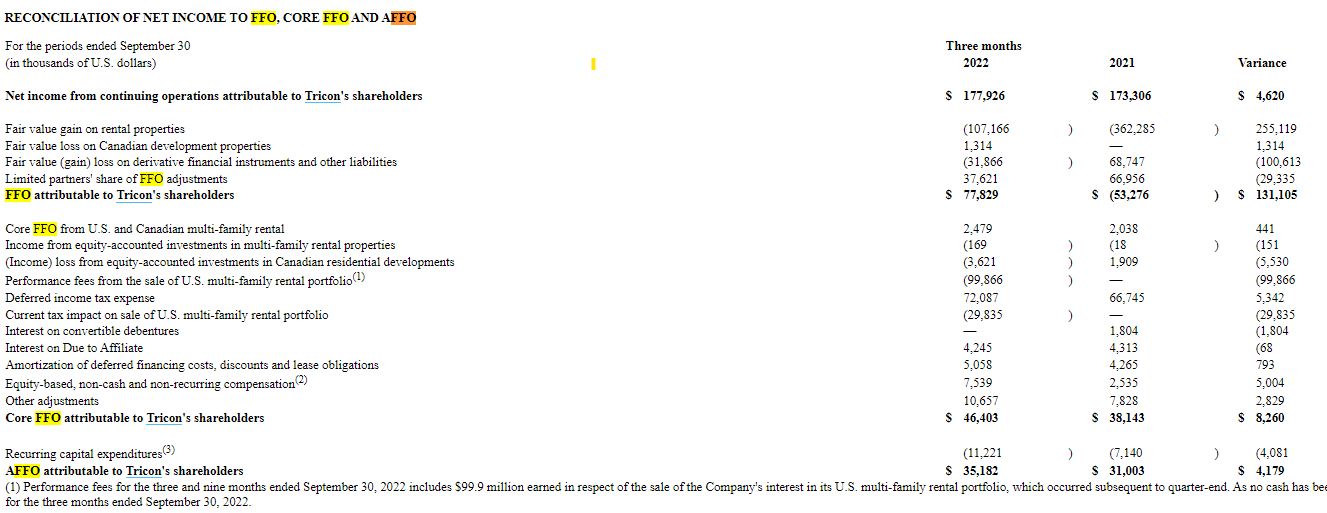

The reconciliation is below as per TCN’s earnings release.

{kind=link}

The big line item of interest here is the $99.866 million performance fee from the sale of a U.S. multifamily property portfolio.

This is a very real gain resulting from selling properties for drastically more than TCN bought them for which resulted in a big payout from one of their joint ventures. Yet, it is a onetime gain and gains from sale of property are taken out of FFO which is meant to be more reflective of run rate earnings.

As seen above, TCN correctly deducted this gain from net income in their reconciliation to FFO. Unfortunately, it appears they did so for the wrong reason. They were removing it for timing reasons as the gain happened subsequent to quarter end. It looks as though TCN will be counting it to 4 th quarter FFO. In their guidance upping from $0.60-$0.64 to $0.75-$0.77 they specifically note that the change is to account for performance fee recognized in 4Q related to multifamily portfolio sale.

Therefore, I posit that FFO never was in the $0.70s.

It will be about $0.60 in 2022 and still about $0.60 in 2023. There is no negative growth here. 2023 will be a year in which strong organic growth will largely balance out increased interest expense. The organic growth will continue after 2023 while the interest expense growth is a largely one-time thing unless the Fed really goes aggressive.

With that misinterpretation in mind, I also want to reinterpret Berman’s statement about growth. The market response to the call was quite negative which indicates they thought the pullback on growth was a bad thing.

I think it is just responsible management. Real estate investing is a combination of real estate acumen and financial spreads. The massive value gains achieved in TCN’s portfolio suggest they have the real estate acumen, but right now the spreads just aren’t there.

Cost of debt has risen dramatically while cap rates have remained quite low. When cost of borrowing is in the 5s, it really doesn’t make sense to buy at cap rates also in the 5s. That is taking on risk with insufficient reward.

As such, I fully support the decision to pull back on growth - Save the dry powder for when spreads make more sense. There is no reason TCN needs to be in a rush to grow. Its existing portfolio is cash-flowing and growing nicely.

The opportunity to acquire SFR in the private market has largely dried up for now, but the organic growth from ownership of SFR is still in its early innings.

Valuation – relative and absolute

The aforementioned $0.60 of FFO consensus estimate for 2023 places TCN at about a 15X multiple on forward FFO which makes it look quite cheap on a relative basis. Peer SFR REITs Invitation Homes ( INVH ) and American Homes 4 Rent ( AMH ) trade at 18X and 20X 2023 FFO, respectively.

{kind=link}

At these multiples, I would be buying up shares of the whole sector, but as is often the case, consensus metrics are missing some key bits of information. In particular, I think adjustments need to be made for maintenance capex and stock-based compensation.

Valuation adjustments to true FFO numbers

I say this frequently but because it is so often reported the wrong way I’ll say it again.

Stock based compensation is a real expense.

TCN’s annual stock comp has a run rate of about $10 million. It was slightly higher in 2022 as a result of the $99 million gain on sale but forward I think $10 million is about where it is trending.

Maintenance capex cycles at about $44 million annually. Thus, I would deduct $54 million from reported FFO to get to true FFO. With 311.9 million diluted shares outstanding that is $0.17 per share which takes 2023 true FFO to about $0.43 per share and TCN to a 21X multiple.

If similar adjustments are made to peers, they would be in the mid 20s so TCN still looks cheap on a relative basis.

Absolute valuation

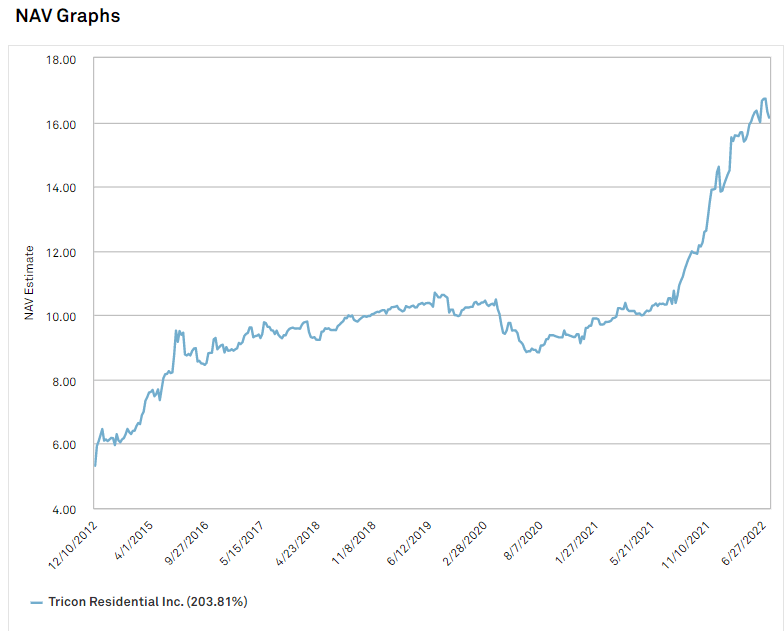

The real draw for me is the asset value. Tricon’s stock price has gone down while its assets have appreciated substantially. Since 2012, TCN’s net asset value has grown from about $5 per share to just over $16 per share.

{kind=link}

If one wants to go out and buy single family homes, they would be buying them at very close to NAV, but if one buys shares of TCN, they can get the same assets at 62 cents on the dollar.

That is compelling.

TCN’s cost structure is a little bit high for my liking but it is really good real estate and that is a fantastic discount.

Final note

While Canadian domiciled, Tricon is listed on U.S. exchanges via the ticker TCN. Revenues come in U.S. dollars and the dividend is paid in U.S. dollars but that might not stop custodians from doing some tax withholding. In my experience, the withholding can be clawed back for no net loss, but it can be a bit of a headache so check with your custodian as to how they handle it before buying.

For further details see:

Tricon Residential Is Cheap Relative To Its Growth