TCN - Tricon Residential's Performance Revenue Is Not Priced Into The Stock

2023-09-20 08:54:48 ET

Summary

- Tricon Residential, with its ownership of 37,000 single-family rental homes, offers outsized exposure to the space relative to dollars invested.

- The discount at which Tricon trades compared to its net asset value is clear, presenting an opportunity for investors.

- Tricon's potential pathways for realizing value include the realization of performance bonus revenue and a potential buyout by a private equity firm like Pretium.

The buy thesis

Tricon Residential (TCN) owns roughly 37,000 single family rental homes ((SFR)) with a market cap of just $2.26B making it the most exposure to the space one can get for their investment dollar. The amplification comes from the joint venture structure through which TCN owns/manages the properties as well as a moderate amount of leverage (standard loan to value ratios). Usually, amplification of this sort is equal parts upside and downside, but due to the timings of purchase, TCN's managed entities have built in appreciation. The 20%-50% appreciation already experienced at the asset level is amplified with respect to the common shares resulting in a share price that is drastically below the value of the underlying real estate.

As single family home prices are readily available on a current basis, the discount at which TCN trades is quite clear. There are 2 paths for realization of this value:

- The individual managed entities reaching an exit at which point TCN receives a fee based on the appreciation (much of which has already happened). This fee is on top of the gains TCN gets on its equity share in the venture.

- TCN as a whole gets bought out. Given the discount at which it is trading it becomes an acquisition target for peers which are trading much closer to asset value. A specific private equity company focused on SFR could be the ideal buyer.

Let me begin by discussing the SFR market and follow with the TCN specific analysis.

SFR fundamentals and outlook

Single family rental properties have been performing well with gains to occupancy and rental rates. The sector has appealed to consumers as it allows them to have the experience of having their own home, but without the prohibitive up-front cost of home ownership. When interest rates were low it was mostly about having enough for the down payment, but as mortgage rates soared, the monthly cost of home ownership increased as well. These high mortgage rates have resulted in renting a single family property being a better value than buying.

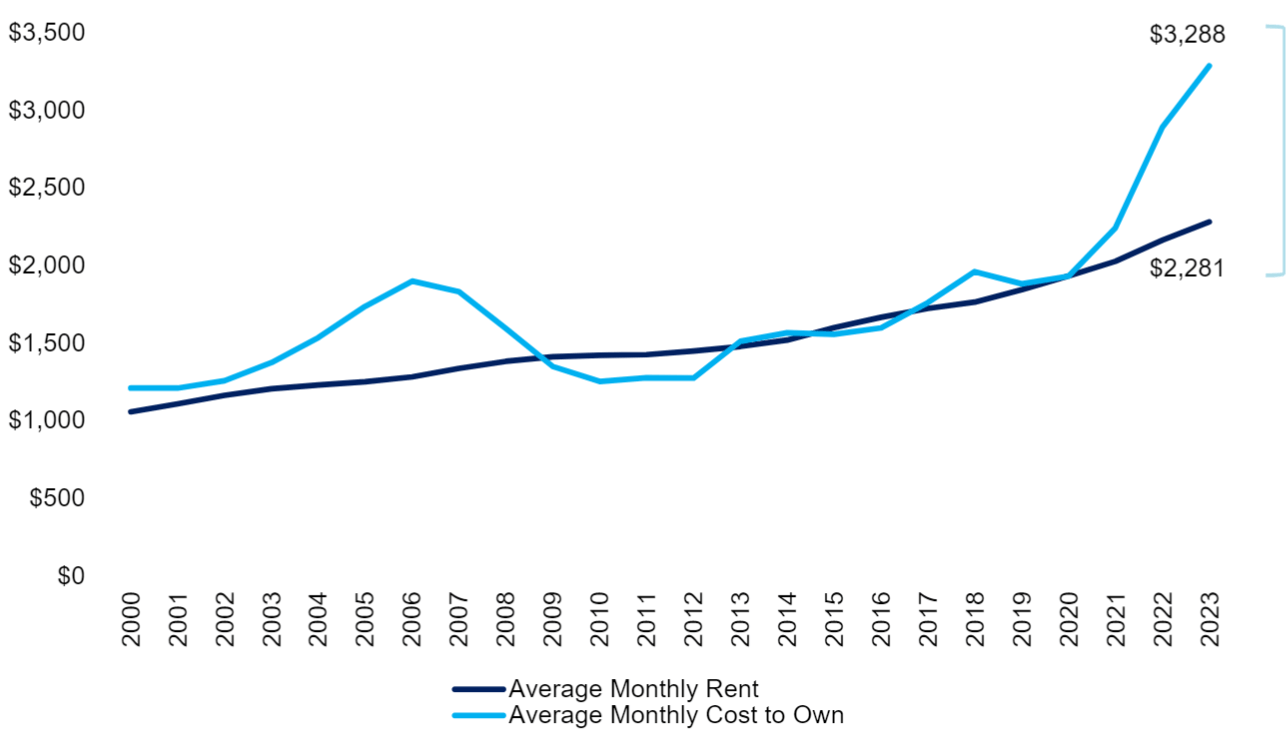

Historically, the cost of renting tends to be approximately equal to the monthly cost of owning.

{kind=link}

Yet the mortgage rate driven spike in the cost of owning makes renting far cheaper today.

In a very rational way, this has driven demand for renting both apartments and single family homes. Apartment development has largely kept up with the demand surge which looks to moderate growth going forward, but single family homes are still significantly undersupplied.

As such, I anticipate further rent growth for the sector while maintaining strong mid-to-high 90s occupancy.

Given that the demand is being fueled by a financial decision of the consumer, I suspect the renter by necessity cohort will be the primary incremental demand whereas higher end buyers may be able to just buy their homes in cash and forgo the high mortgage rates.

Data from a recent Yardi Matrix report confirms the idea that renter by choice is the stronger segment.

"Year-over-year rent growth has turned negative in the Lifestyle segment, at -0.4% as of August, while Renter-by-Necessity rents have increased by 2.9%. The same dynamic holds in occupancy. Year-over-year through July, Lifestyle occupancy rates have declined 100 basis points to 95.3%, while RBN occupancy rates have increased 290 basis points to 97.7%"

This bodes well for Tricon Residential as their portfolio is priced for the renter-by-necessity market with an average rental rate of $1,792.

TCN

In theory, rental rates will track toward parity with the monthly cost of home ownership. It could either be rental rates continuing to rise or cost of ownership declining. I think it will be a bit of both as my base case for mortgage rates is stabilization around 6%.

Geographically, I like the sunbelt focus of TCN's single family rentals.

{kind=link}

These are the job growth markets and population follows jobs.

Tricon's amplified exposure to SFR

There are 3 aspects of TCN that multiply its exposure to SFR fundamentals

- Valuation

- Joint ventures

- Performance bonuses

Technically there would be a 4th in leverage, but the leverage is not unique to TCN as its peers, American Homes 4 Rent ( AMH ) and Invitation Homes (INVH), also have access to leverage.

Discount to net asset value ((NAV)) makes each invested dollar go further.

- AMH is trading at 97.5% of NAV

- INVH is trading at 92.7% of NAV

So for each dollar one invests in these REITs you get slightly more than a dollar of real estate (ignoring leverage for now).

Tricon is trading at 61% of book value which due to IFRS accounting is basically NAV. Thus, each dollar invested in TCN buys $1.63 of real estate.

Discounted valuation is the best way to amplify one's exposure because unlike other forms of amplification, there is no downside to buying cheaply. In fact, the margin of safety introduced by the value actually reduces the risk.

Beyond valuation, an investment in TCN amplifies exposure to SFR through its joint ventures. In these JVs TCN typically has a roughly 1/3 equity stake with the counterparties owning the other 2/3. 1/3 ownership of 3 houses is roughly the same financially as fully owning 1 house, so the reduced capital contribution in itself does not amplify returns.

However, TCN manages the entirety of these JVs which provides fees and performance bonuses. The fees are counterbalanced against that actual cost of managing large property portfolios so there isn't all that much upside there. It is the performance bonuses where the opportunity lies.

If the managed entities generate a return beyond a certain threshold, TCN collects a performance bonus equal to a percentage of the returns beyond that watermark. At the time of underwriting, these bonuses were fair and typical of this sort of managed entity. Going forward, I would expect only a normal level of return from this structure.

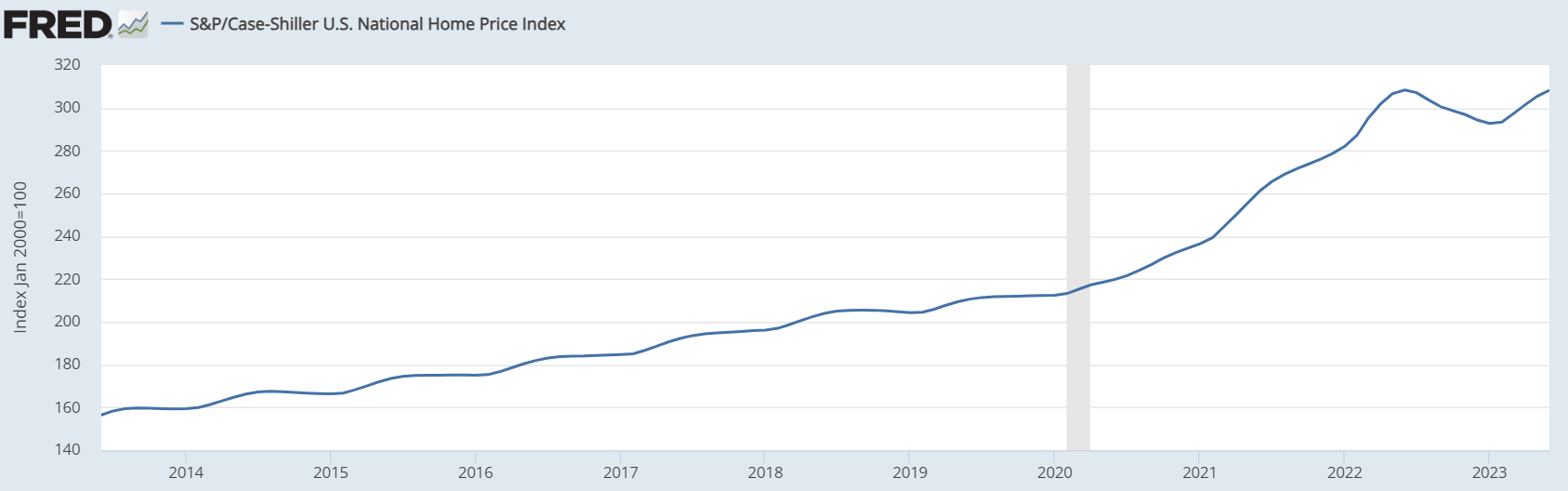

However, we have the benefit of knowing what has already happened and some rather enormous performance fees have already accrued (although not yet recorded). The single family rental joint ventures raised capital many years ago and invested that capital in SFR at much lower prices. This is what has happened to home prices nationally:

{kind=link}

TCN's assets are in the epicenters of population and job growth so their appreciation has likely come in above national averages.

Depending on the JV, TCN is sitting on asset appreciation of anywhere from 20% to 50%. Additionally, rental rates and occupancy have improved dramatically from initial purchase. As such, I suspect the returns on these JVs has greatly exceeded the threshold and is well into the territory of performance fee generation. While TCN gets to record the benefit of asset appreciation and NOI growth in real time on its equity portion, the performance bonus is only recognized at some predetermined date of maturity.

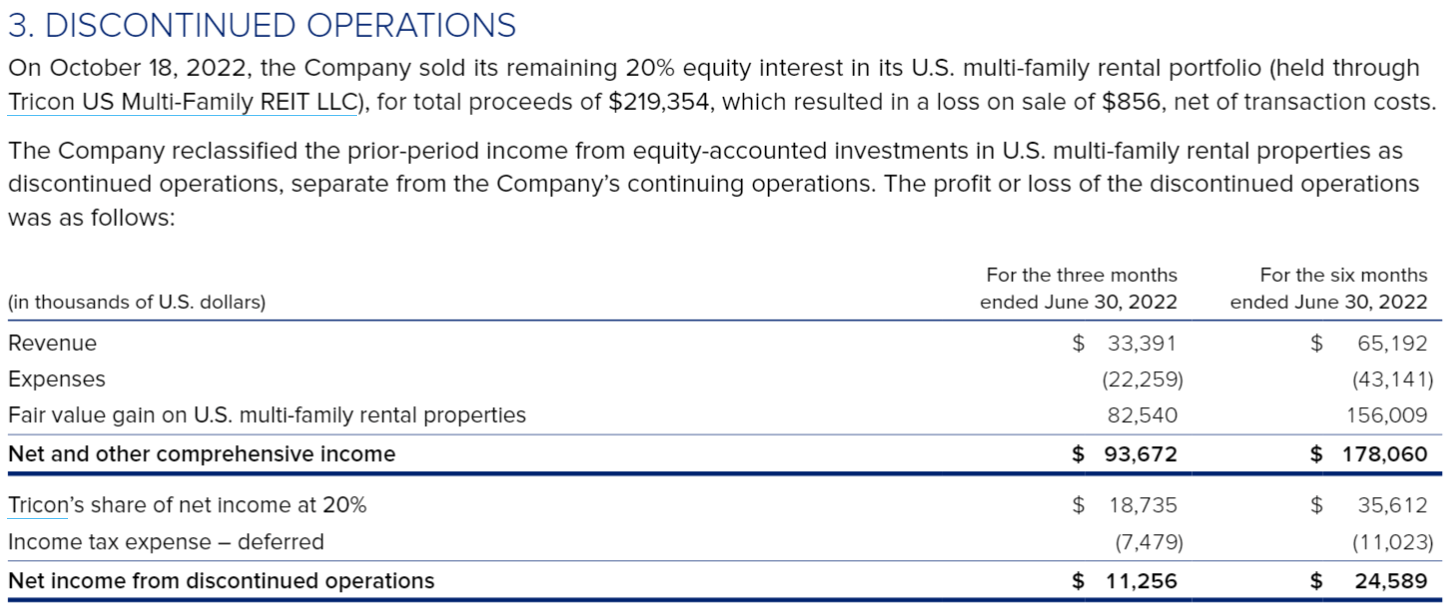

As an example, we can look at the U.S. multifamily sale.

{kind=link}

TCN sold its 20% stake for $219 million. This was a large gain over their invested capital but in-line with the fair value of the assets on the balance sheet which got marked up over time (due to IFRS accounting).

That equity gain on JVs is already in the books and already in the NAV that makes it discounted at 61%.

The aspect that is not in the books yet is the performance fee component which I think will be quite large. In the case of the multifamily sale, the performance fee revenue was $100 million.

From the 10-K

"Performance fee revenue of $99.9 million was recognized upon the sale of the U.S. multi-family rental portfolio in the third quarter of 2022"

The multifamily portfolio was a relatively small asset in comparison to the SFR JVs. As such, I think there will be many hundreds of millions of performance fee revenue coming as the SFR JVs hit their maturity dates starting in 2025.

Recall that TCN has a market cap of $2.26 billion so a few hundred million is a big chunk of assets that is not yet being reflected in the NAV.

I think the recognition of these performance bonuses will be a good catalyst for the stock price in addition to being a large cash infusion.

Forward growth prospects

Growth looks to be a combination of organic in the form of continued rental rate growth on SFR and external through new investments.

TCN is working on capitalizing a new joint venture of similar structure which will presumably be called SFR JV3. I don't see this as being as wildly successful as the previous ones simply due to timing in the cycle. The asset appreciation of single family homes of the last 4 years was astounding and probably unlikely to repeat. That said, SFR seems to be fairly priced and TCN is acquiring at pricing that makes it accretive on a cap rate versus WACC spread.

Thus, I would anticipate a positive yet modest FFO/share accretion from the new venture. Another investment that looks more accretive to me is the development deal with the Arizona State Retirement System in which TCN will develop 2227 units over the next few years.

{kind=link}

TCN's capital commitment here is rather small, but they have an amplified payoff upon successful completion.

Valuation

We have already discussed the substantial discount at which TCN trades on an NAV basis, but I like to look at valuation from multiple angles. TCN also appears to be cheaper than peers on an FFO and AFFO basis.

Using the closing market price of $8.54 on 9/14/23 and sell side consensus estimates, TCN is trading at 13.7X forward FFO and 17.4X forward AFFO.

{kind=link}

These multiples strike me as rather opportunistic given the fast growth rate.

It is also a cheap multiple for the sector.

- INVH trades at 19X and 24X FFO and AFFO, respectively.

- AMH trades at 21X and 24X FFO and AFFO, respectively.

Pathways for shareholders to realize the value

I am a firm believer that stock prices will gravitate toward intrinsic value over the long run, but most investors are not as patient as I am. They want a catalyst to realize the value sooner. With TCN I see 2 potential catalysts.

- The aforementioned realization of performance bonus revenue as entities hit their maturity date

- A buyout of the company

The deep discount at which TCN trades makes it an attractive target for the private equity that is scooping up SFR. Specifically, I think Pretium is a potential buyer.

Pretium is a $50+ billion private equity giant focusing on the single family rental space, already owning over 100,000 homes. They recently hired Johnathan Pruzan who is known for leading large acquisitions and that is his stated purpose at the company.

TCN would be a bite size acquisition for them and due to the discount, it would be immediately accretive even if bought at a large premium to current share price.

Risks of investment

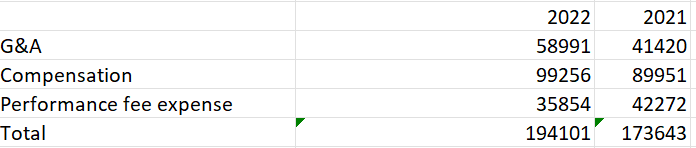

While I am strongly bullish on TCN, there are some risks here. Some are related to the macroeconomic exposure inherent to the sector, but a more TCN specific risk is its high G&A cost. Between the multiple buckets of expense, I calculate total G&A at $194.1 million in 2022 and $173.6 million in 2021.

{kind=link}

There are expenses associated with managing a large portfolio of third party and partially owned assets so it should be somewhat high, but this is more than I would anticipate given the size.

G&A expense for TCN is significantly higher than for AMH or INVH.

Note that FFO and AFFO are measured AFTER G&A expense, so even factoring in the high cost, the valuation looks cheap, but I think it is a factor on which to keep an eye.

It can also be a little bit challenging to own TCN due to its Canadian domicile. In fact, we think this could be one of the aspects causing it to trade at such a discount. While the U.S. and Canada have a tax treaty, some custodians will still put withholding on the dividends from TCN. In our experience, the withholding can be clawed back come tax time, but it is an extra hassle and it may be keeping some investors from owning the stock.

Wrapping it up

Single family rental fundamentals look strong, particularly in the sunbelt where TCN is located. The deep discount at which TCN trades, along with the subtleties of accrued bonus revenue, suggest TCN could deliver an outsized total return to shareholders.

For further details see:

Tricon Residential's Performance Revenue Is Not Priced Into The Stock