TRLEF - Trillion Energy: Headwinds Ahead (Rating Downgrade)

2023-06-20 00:36:14 ET

Summary

- Trillion Energy, a natural gas producer in Turkey, has experienced both positive and negative developments, including increased reserves and production, but also falling gas prices eventually need for additional financing.

- The company's Q1'23 exit rate production was below expectations, and management has been vague about the need for further financing, adding uncertainty.

- My calculations indicate that the company won't be able to self-fund its expansion in the current environment and dilution is likely, so I'm changing my rating to a Hold.

Back in March, I wrote an article about Trillion Energy ( TRLEF ) – an emerging natural gas producer in Turkey. Since then, some important events, related to the company have happened. While some of them like the increase in reserves and putting another well into production are positive, some negative developments have also unfolded. The price of natural gas in Turkey has fallen, the Q1’23 exit rate production came below my expectations and unfortunately the company had to resort to additional financing, which could increase the share count further. In recent interviews, management has been pretty vague about the need of additional financing, which adds uncertainty. Looking through Trillion’s Q1’23 performance, the current gas price environment and additional wells costs guidance, I think that further financing looks very likely. For these reasons, I’m changing the rating to Hold.

New developments

In the beginning of April, Trillion released an updated reserves data, indicating 30.2% increase of 2P reserves, attributable to the company, to 63.3Bcf of natural gas. However, this press release was accompanied by other, not so positive information – Trillion placed CAD$15M of convertible notes with 12% interest rate, convertible into 25M shares, which translates into conversion price of CAD0.60/share. The notes were also complimented by 25M warrants with an exercise price of CAD$0.50 each. The notes will mature on 30 April 2025, while interest payments will begin at the end of Oct’23. For reference as of 31 March 2023, Trillion has approximately 386M shares while the market price as of 16 June is CAD$0.365/share.

Reserves (Trillion Energy)

On one hand, the potential conversion of those instruments into shares if exercised, will be done at a considerably higher than current market prices. But the financing itself reveals a deeper problem – Trillion is unable to self-fund its growth as inflation has hit the anticipated cost of new wells, while lower gas prices have hurt revenues. To make matters worse, The company reported exit production rate of its 4 operation wells of 12.6MMcf/day, which puts the average rate/well at 3.15MMcf/day – well below the guided range of 3.5-4MMcf/day. The company explains the inferior result with pressure variances between the wells, which should be temporary.

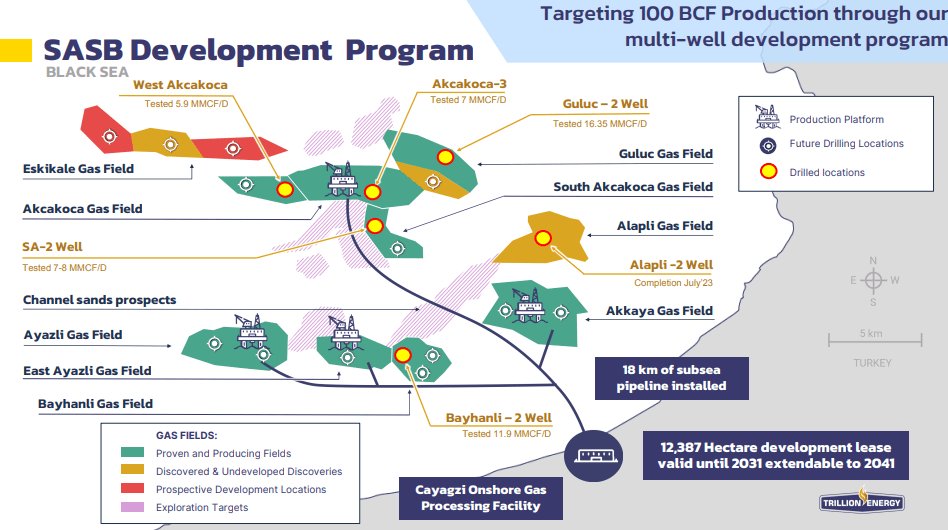

The SASB program (Trillion Energy)

{kind=link}

On the positive side, Trillion was able to complete and put into operation its fifth well – Bayhanli-2, which according to a recent interview of the company’s CEO is producing around 8Mcf/day alone, making it the best performer so far.

Brace for dilution

Despite having 5 producing wells, I’m not optimistic about Trillion being able to self-fund the development of the remaining part of the SASB program. The CEO – Art Halleran revealed that wells cost between CAD8-13M each, depending on their depth. At the same time, natural gas prices in Europe and Turkey have been falling and the company is currently getting around US$14.14/Mcf. Looking at the company’s balance sheet it finished Q1’23 with close to CAD$2.4M of cash, which gives it pretty much no breathing room. Note that at that time, the fifth well was not developed, so large part of the CAD$15M of financing likely was spent on that.

I tried to simulate the Q2’23 cash flow, without considering CAPEX. For the calculations I assumed average production for the quarter of 16MMcf/day, gas price of US$14.14/mcf, oil production of 80 barrels/day, oil price of US$75/barrel, exchange rate of USD/CAD of 1.33 and incremental OPEX of CAD$2.26/mcf, extrapolated by the Q1’23 results. As Trillion has quite large tax pool, I didn’t consider corporate tax expenses.

| Unit |

| 16MMcf/day scenario |

| 28MMcf/day scenario |

| oil revenue |

| CAD |

| 0.7 |

| 0.7 |

| gas revenue |

| CAD |

| 13.3 |

| 23.2 |

| total revenue |

| CAD |

| 14.0 |

| 23.9 |

| royalties |

| CAD |

| 1.7 |

| 3.0 |

| net revenue |

| CAD |

| 12.2 |

| 20.9 |

| OPEX |

| CAD |

| 2.2 |

| 3.4 |

| G&A |

| CAD |

| 2.5 |

| 3 |

| interest expense |

| CAD |

| 0.1 |

| 0.5 |

| FCF |

| CAD |

| 7.5 |

| 14.1 |

*Author's own assumptions and calculations

My calculations indicate that Trillion should generate only CAD7.5M of FCF in Q2’23, before accounting for CAPEX spending. The simulation also included a scenario where the company completes the first phase of the SASB program and has 7 producing wells with assumed total production rate of 28MMcf/day. Even in the 7 well scenario, in the current natural gas price environment, the example indicates quarterly FCF of CAD$14.1M, which is not sufficient to cover the expenses for 2 wells (approximately CAD$20M), assuming that the initial guidance of putting one well every 45 days is followed. Unfortunately, additional dilution looks very likely if Trillion wants to continue its development program. When asked about dilution in the interview , the CEO didn’t give a firm answer, but instead pointed out that there will be more clarity after Q2’23 ends. In my opinion, given the calculations that I carried out, additional financing seems almost inevitable.

Natural gas prices risk

The biggest risk factor for Trillion is related to natural gas prices. If they continue the freefall, the future of Trillion is not bright. Even the current price environment doesn’t support self-funding future CAPEX, so additional financing will be needed. The best case for the company will be some sort of a repeat of the energy crisis of 2022 with significant jump in gas prices. This scenario is not to be excluded, as a repeat of the warm winter in Europe is not likely. If energy prices reverse their decline, Trillion should be able to obtain additional funds at more favorable terms, as the sector as a whole will gather wider investors’ interest again.

Conclusion

Since my last article about Trillion Energy, the situation had changed for the worse – natural gas prices are falling, development costs are hit by inflation and operations are experiencing some technical problems, resulting into lower average production rates. While the increased reserves base and the news about the fifth producing well are positive, they seem to be offset by the negative developments. Dilution seems very likely if the company wants to continue its SASB development program as scheduled. For these reasons, I’m changing my rating from Buy to Hold.

For further details see:

Trillion Energy: Headwinds Ahead (Rating Downgrade)