HRZN - Trinity Capital: A 14.5%-Yielding 'Higher-For-Longer' Buy

2023-10-10 08:30:31 ET

Summary

- Trinity Capital is a self-managed BDC that offers exposure to growth-stage companies backed by venture capital.

- The company's diversified portfolio, focus on floating-rate loans, and impressive dividend yield make it an attractive investment.

- TRIN appears to be undervalued and trades at a discount compared to its peers, all while paying a well-covered 14.5% yield.

Variety is the spice of life, and the same goes for investments, too. While it may be hard to go wrong with so-called 'sleep well at night' stocks like Main Street Capital (MAIN) in the BDC space, some investors may find it appealing to reach for higher yield while also getting the peace of mind of not having all their eggs in one basket.

This brings me to Trinity Capital (TRIN), which is a relative newcomer in the BDC space. Like many of TRIN's peers, it's seen decent share price performance over the past 12 months, but the past 30 days have proved challenging with the broader market downturn. In this piece, I discuss what makes now a good buy-the-dip opportunity, so let's get started!

{kind=link}

Why TRIN?

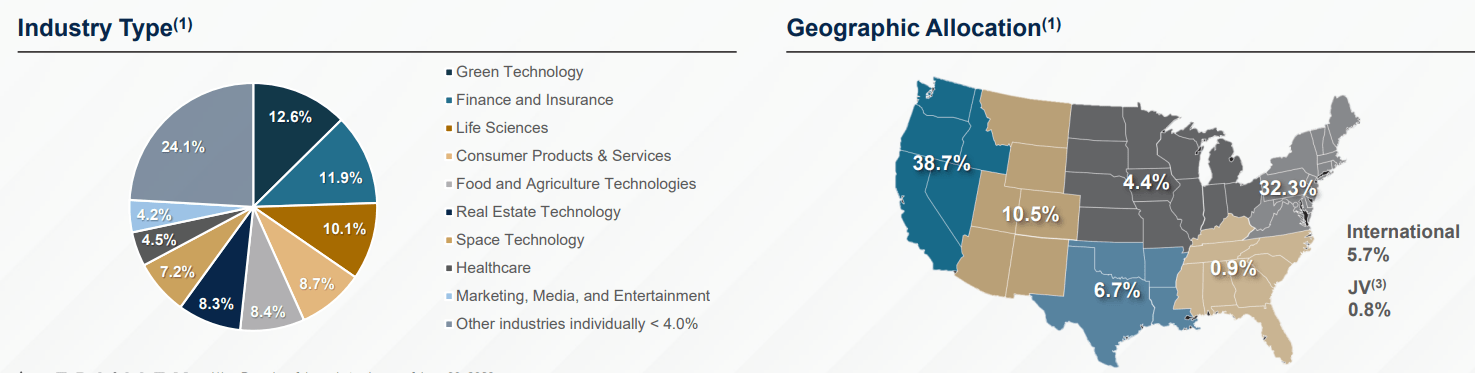

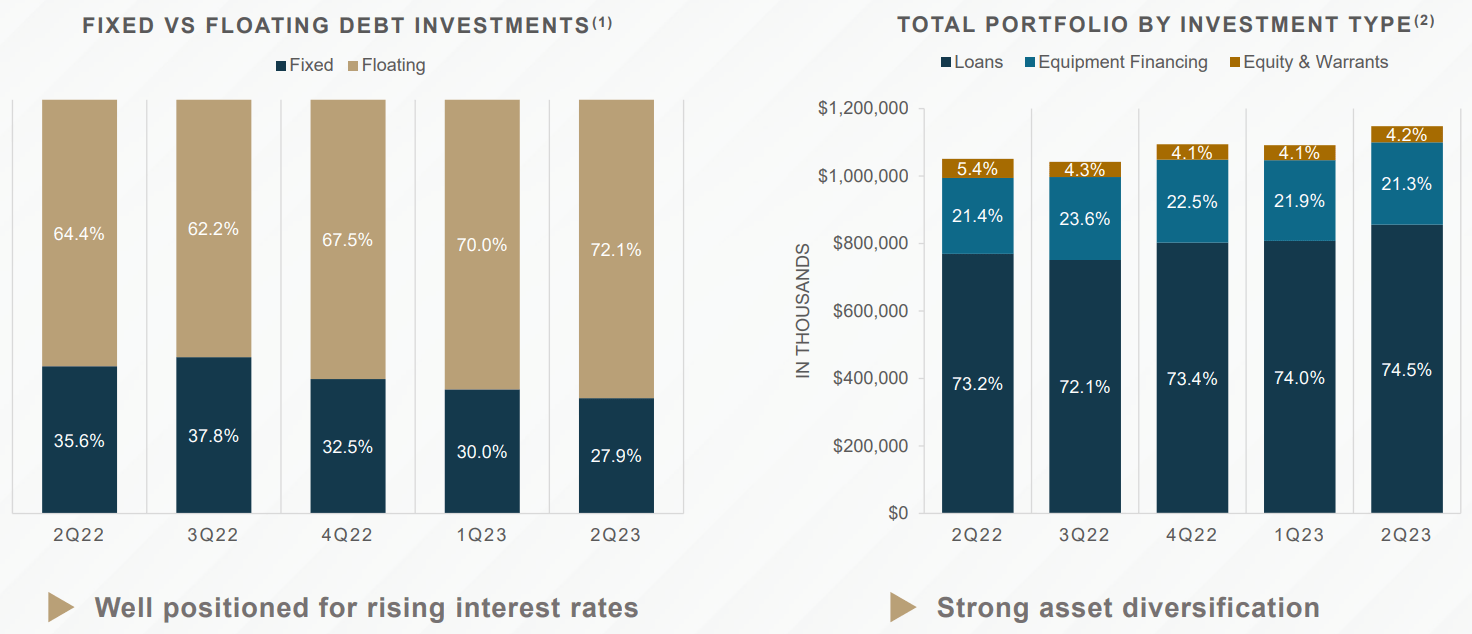

Trinity Capital is one of a handful of internally managed BDCs and focuses on growth-stage companies that are often backed by venture capital. At present, it carries a $1.15 billion portfolio that's composed primarily of secured loans (75% of the portfolio), followed by equipment financing (21%), and equity and warrant investments (4%).

TRIN's portfolio resembles that of growth-oriented peer, Hercules Capital (HTGC), with a tilt toward technology and life science. It also has a bit of bread and butter industries like that of Main Street Capital with consumer products and finance, insurance, and healthcare in the mix.

As shown below, Green Technology, Finance & Insurance, Life Science, Consumer Products & Services, and Food Technologies make up TRIN's 5 industries, comprising just over half of its portfolio, and TRIN is diversified by geography with higher concentrations along the West Coast and Northeast, where growth industries are primarily located.

{kind=link}

Like other BDCs, TRIN is benefitting from higher interest rates, which has resulted in TRIN's effective yield on investments rising by 240 basis points over the past 12 reported months to 16.2%. This has helped TRIN achieve a $0.61 NII per share during the second quarter, which is up $0.06 on a sequential basis from the Q1 rate of $0.55. TRIN is also well-positioned to benefit from a ' higher-for-longer ' rate environment that the market now widely expects after the Federal Reserve's meeting in September.

TRIN is well-positioned for this type of rate environment, as it has shifted the portfolio more toward floating-rate loans. Management estimates that annualized NII per share increases by $0.15 for every 100 basis point rise in interest rates. As shown below, the percentage of floating-rate debt investments has risen materially by 7.7% over the past 12 reported months, from 64.4% to 72.1%.

{kind=link}

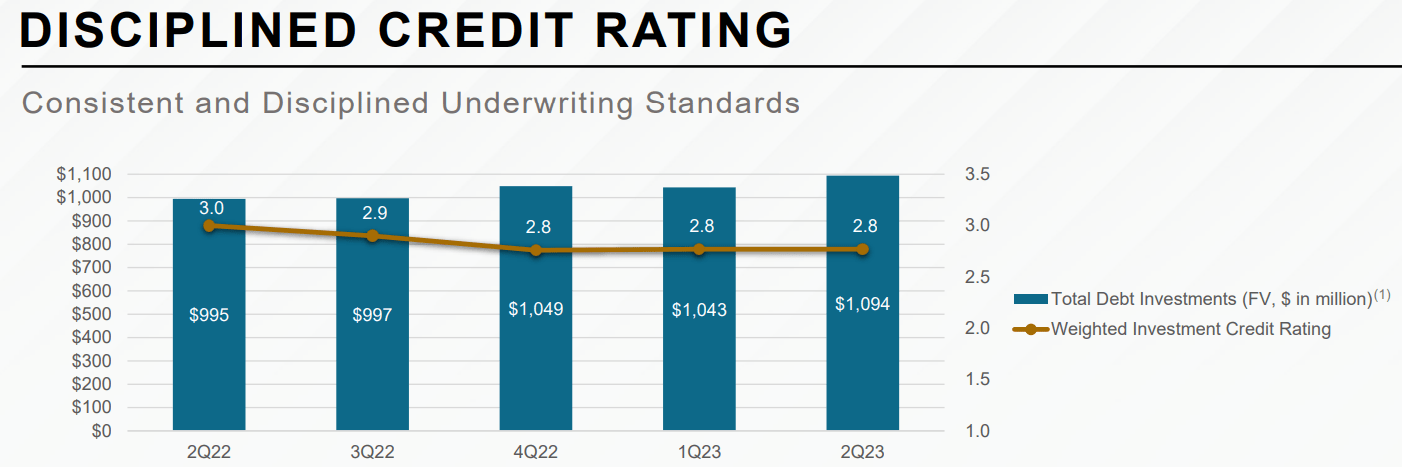

Risks to TRIN include the cyclical nature of the tech industry and the headwinds they face from higher interest rates. This means that portfolio exits through IPO or M&A are less commonplace given the higher cost of capital that these companies face, and as such, TRIN won't be able to grow its NAV/share through its equity investments as much compared to a healthy IPO environment.

Also, lower interest rates would mean a lower NII/share, but that scenario does not seem likely in the foreseeable future. As shown below, TRIN's portfolio credit score slightly declined last year from 3.0 to 2.8 (on a scale from 1 to 5, with 5 being the highest performing), but has held steady so far this year.

{kind=link}

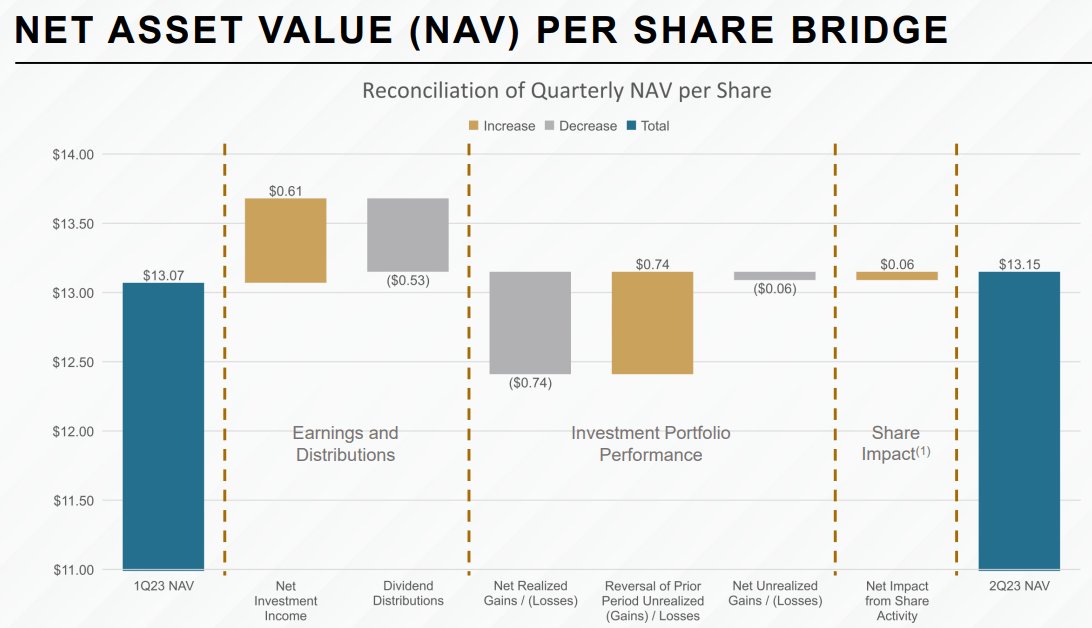

Nonetheless, TRIN's investments in non-accrual declined since earlier this year and sit at a modest 2% of portfolio value. That's worth monitoring, as I'd like to see that decline down to the 1-1.5% range over time. In addition, TRIN has seen an improvement in its NAV per share on a sequential basis, driven by higher net investment income, reversal of earlier mark to market (unrealized) loss, and accretive equity issuances.

{kind=link}

Importantly for income investors, TRIN currently yields an impressive 14.5% based on the regular dividend alone, with the potential for a higher yield through special dividends. The regular dividend is well-protected by an 80% payout ratio. TRIN has recently been paying out about half of its NII to regular dividend overage with $0.05 special dividends, leaving plenty of retained capital to fund growth. TRIN also carries a reasonable amount of leverage with a 138% debt to equity ratio, sitting below the 200% statutory limit.

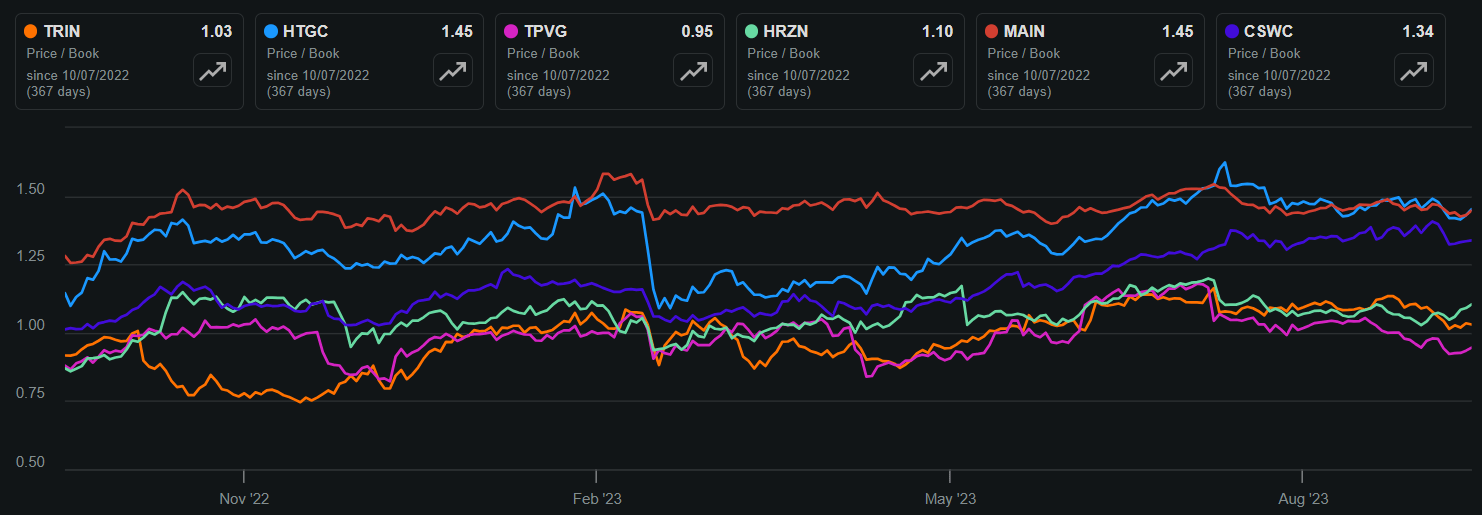

Lastly, I see value in TRIN at the current price of $13.54 with a price to book value of 1.03x. As shown below, this sits just above that of peer TriplePoint Venture Growth (TPVG), while sitting materially below that of Horizon Technology Finance (HRZN) and internally managed peers Main Street Capital, Hercules Capital, and Capital Southwest (CSWC).

TRIN & Peers Price-to-Book (Seeking Alpha)

{kind=link}

Using the following NPV analysis, I came up with a fair value price of $15.93, which sits slightly above the analyst consensus average price target of $15.50 . This is based on the current year's EPS estimate of $2.23, a conservative 0% growth rate, since TRIN pays out most of its earnings, and a 10% discount rate to account for the higher risk nature of TRIN due to exposure to emerging growth industries. This fair price sits meaningfully above the $13.54 current share price.

NPV Analysis (Produced By Author)

{kind=link}

Investor Takeaway

All in all, Trinity Capital appears to be a well-managed internally managed BDC that offers exposure to attractive growth-stage companies backed by venture capital. It's set to benefit from a higher for longer interest rate environment.

With its diversified portfolio of industries and geography, focus on floating rate loans, impressive dividend yield, and potential for NAV/share growth through equity investments, I see value in TRIN at the current price. Lastly, TRIN appears to be undervalued based on my valuation analysis and trades at a discount to most of its peers.

For further details see:

Trinity Capital: A 14.5%-Yielding 'Higher-For-Longer' Buy