TCOM - Trip.com: Betting Big On Chinese Demand

2023-05-18 13:39:21 ET

Summary

- Trip.com Group Limited is a travel service provider that offers various travel-related services, primarily in the Chinese market.

- China recently ditched its zero-COVID policy. With things dying down, our view is that travel should begin to pick up in the coming months.

- Economic weakening will impact international expansion and demand in the near term but the company should naturally bounce from its current depressed state.

- The company can be highly profitable and grow quickly, as evidenced by its pre-FY20 performance. Our view is that they can replicate this.

- Based on our valuation of the business, we see an upside of 20%.

Investment thesis

Most of the company's exposure is to the Chinese market, which has been hurt by the COVID-19 pandemic. With things beginning to look up, we have the potential to see a bounce back from Trip.

The purpose of this paper is to assess just that, whether the industry will in fact improve and whether Trip is positioned to take advantage of this. This will involve an analysis of the company's financial profile, current conditions in its key markets, and whether the travel and tourism industry as a whole is attractive.

Company description

Trip.com Group Limited ( TCOM ) is a travel service provider that offers various travel-related services, including accommodation reservation, transportation ticketing (predominantly flights), packaged holidays, and in-destination services. The company also provides ancillary services such as travel insurance, cancellation protections, online advertising, etc.

Trip's target audience is low-cost travel, with the company seeking to aggregate the cheapest options for consumers and supplement its income by upselling services.

Share price

The company's share price has performed poorly in the last decade, on the back of what have been difficult trading conditions. The industry has become more competitive and prices have been driven down, squeezing the players in the market.

China's COVID problems

China initially responded well to the COVID-19 pandemic, locking down the whole country extremely effectively and minimizing deaths / cases. The problem partially began due to poor vaccine uptake compared to the West and so when the lockdowns eased, cases increased substantially. Unlike the West, China remained steadfast in its zero-COVID policy, contributing to constant lockdowns. This has decimated the tourism and travel industry, as the majority of flights in and out of the country have ceased. As of Mar23, it does not seem possible to get to China from the UK on a non-stop flight in less than 24hrs.

UK > China (Google Flights)

For a company like Trip, this has been a disaster. The company has seen declining revenue and has had to rely on domestic Chinese tourism, which has shown strength when not in lockdown but has been materially interrupted. There is reason to be upbeat, however, China has ditched its zero-COVID policy and following a few months of very high case numbers, the country has declared victory over COVID . Although the current quarter's numbers will be impacted, our view is that the company will likely see a rapid acceleration in demand. This will be driven by pent-up demand from the restrictions, with consumers saving money given the lack of spending options.

Economic conditions in China

As the graph above shows, lockdowns have contributed to the slowest growth rate China has experienced in several years. Unlike much of the West, however, China has not seen rising inflation. There is the risk that China does become a victim of this as a rapid expansion of demand can destabilize the supply side, however, it is far too early to suggest this. Inflation in Western nations is impacting China as it is contributing to slowing demand for goods, as consumers see their discretionary income decline. When coupled with high interest rates, it is not surprising to see consumers focus only on essentials. With many discretionary industries, such as tech hardware and retail, having supply chains in China, we are likely to see a knock-on effect. Chinese exports have been trending down for the last year partially supporting this western decline. This impacts domestic tourism more so, as if businesses struggle with exports, we will see a negative impact on income and employment, reducing the demand for domestic travel.

Another impact on Trip in particular is the risk of declining demand for travel in the West, which it services as part of its international operations. Travel has been surprisingly strong given the current conditions, with companies like AAL and RYAAY achieving revenues in excess of pre-COVID levels. Having said this, the industry remains fragile and with very little notice could see demand rapidly decline. We have already seen consumers preferring staycations, suggesting consumers are looking for cheaper options. Trip has seen its domestic hotel bookings already return to pre-COVID levels.

Our overall outlook for 2023 is a rapid improvement in demand from China from Q2-23 onwards, but not necessarily to a level where it breezes past pre-COVID levels. The western market will likely weaken but its resilience so far suggests it is possible that we will not see a dramatic decline. Net of all, the company should be up.

Financials

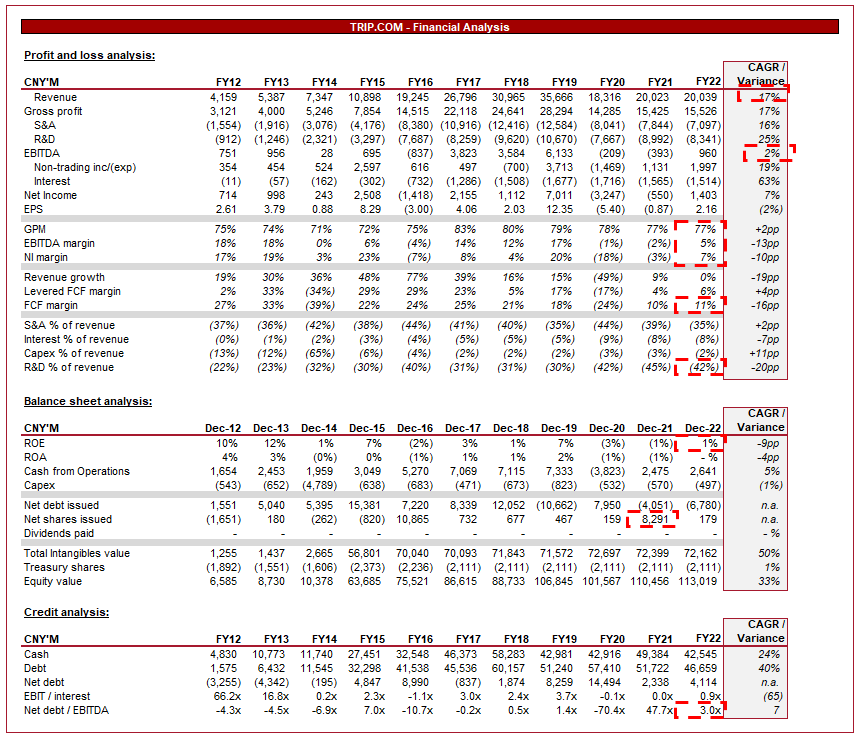

{kind=link}

TRIP.COM Financials (Tikr Terminal)

Presented above is Trip's financial performance across the last decade. It is a story of two parts, firstly from FY12 to FY19, which has been nothing short of fantastic. And then the post-COVID part, which is less good.

In the last decade, Trip has grown at a CAGR of 17%, driven by its technology-first approach to what is a historically unsophisticated industry. Trip offers an easy-to-use app with everything travel related in one place, creating convenience and speed for consumers. Trip was named the 10th most downloaded OTA app in 2022 , a year in which the number of services the company can offer is far lower than usual. As with most industries, the technological revolution is a structural change rather than a short-term trend, positioning Trip to continue this growth going forward. The industry is forecast to grow at 14.8% in the next 5 years.

In the most recent period, performance has picked up. This does not reflect the incredible jump in China's COVID numbers but is more a reflection of consumer sentiment.

CEO message on recent performance (Trip)

The company has maintained strop controls over its cost of revenues, which primarily includes payroll compensation for customer service support. With the west experiencing wage inflation, this impact has not translated across to Trip.

S&A expenses, which primarily include compensation and advertising, have grown in line with revenue. This is unsurprising as although the business considers itself to be global, the majority of revenue is derived from China. The company has a way to go in expanding into other countries and further increasing its presence in China.

R&D relates to product development as Trip maintains and expands its current platform. This expense has been increasing as a % of revenue for several periods now and looks unusual, as one would expect some economies of scale, even though they are launching new products. Management has commented on this, seeking to run lean and reduce the impact of this expense. We can see it ticking down in the coming periods.

Taking a step back, the company's "go-forward" margins are difficult to assess as we do not know how the company will shake out once things in China return to normal. If we take FY19 as a proxy, a 17% EBITDA margin and a 20% NI / FCF margin are very attractive. The question will be how S&A and R&D respond to revenue picking up, will they return to FY16 levels and destroy margins, or FY19 where the company was running far more efficiently? Our view based on LTM Nov22 is that costs will marginally tick up, likely showing margins closer to FY17 in FY23 and then moving towards FY23 levels.

Moving onto the balance sheet, the company has needed to raise debt in order to finance its operations. Debt in the last decade has increased quickly, but most of this was in FY14, with the subsequent period being more balanced. This does look slightly concerning, but for now, we are content. What we must remember is that EBITDA is likely to increase substantially in the coming year and once this is factored in, the level of debt is less concerning. From a net debt perspective, if Trip was to return to its FY18 level, its Net debt / EBITDA ratio would be 1.2x which is very comfortable.

The company also holds a substantial amount of long-term investments and goodwill, which has the scope to muddy net income with positive or negative below-the-line charges.

Peer comparison:

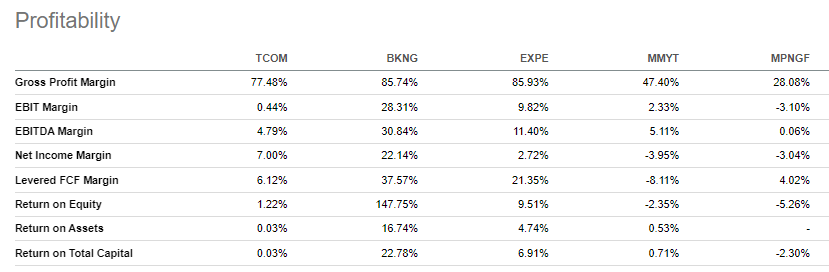

{kind=link}

Profitability (Seeking Alpha)

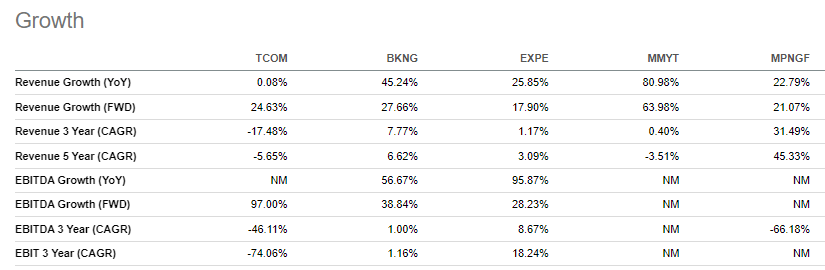

{kind=link}

Growth (Seeking Alpha)

Presented above is a cohort of companies that operate in the online travel industry. We have presented a mix of both faster-growing businesses, such as MMYT , and traditional players like BKNG . The US travel businesses have benefited from much of the West reopening completely, which is why they are so superior.

Our intention in presenting this is to illustrate where Trip can reach relative to its current position. In FY19 the company achieved an EBITDA margin of 17%, which is in the ballpark of both Expedia and BKNG. Both BKNG and EXPE levels suggest that TRIP can reach a maturity level where both EBITDA and FCF margins are in the region of 20-30%, which is incredibly attractive. For now, investors can get pretty good results while the company focuses on growth, with this likely being in excess of its fast-growing competitors.

Valuation

Valuation (Tikr Terminal)

Valuing Trip is not an easy thing to do. As the above shows, valuations are a mess currently for businesses that are facing disruptions.

Our view is that once growth slows to single digits, Trip will reach the 15-20x level, similar to our established players. For now, however, the company will trade at a premium as the Chinese market continues to grow in wealth and the business expands internationally.

We have derived a fair value NTM EBITDA multiple of 25x, which sounds high relative to its key peers but looks justifiable. Firstly, we have assumed the travel industry will accelerate from Q2/Q3-23 onwards and allow the business to exceed FY19 levels. Our 25x multiple is based on how we think Trip's EBITDA will grow in the coming 5 years (c.15% after the FY23 bump) relative to its peers who are growing at a slower rate. We should see noticeable multiple contractions towards the 20-30x range in the years following FY23.

Final thoughts

Trip has done a fantastic job of growing market share quickly while continuing to innovate its product offering. The company was on an amazing trajectory until COVID hit, with the business losing 3 years. Things are looking up, however, with China seemingly kicking COVID to the curb. Our view is that demand should pick up quickly, similar to what occurred in the West, as travel opens up to China. All the while, Trip will continue to expand internationally, diversifying away from China. We do not see FY23 being a blowout year objectively, as we are in a cyclical downturn economically, but our view is that medium-term demand will be robust.

The company's profitability profile is very attractive historically and the big risk is whether the company can return to this. Our rating suggests they can but investors should keep a keen eye on financial performance in the coming quarters to see if this is a reality or not.

Based on the valuation of the business, our view is that the company has an upside of around 20%, below analysts' forecast of 35%. We also believe there is a chance that the stock immediately pops on improving performance once things improve and management can provide semi-reliable guidance on what is achievable.

For further details see:

Trip.com: Betting Big On Chinese Demand