TCOM - Trip.com: Favorable Tailwinds In Play Initiate A Buy

2023-10-05 00:20:01 ET

Summary

- Trip.com has benefited from travel recovery after the reopening of the lockdown restrictions in China last year.

- Domestic travel in China is expected to log strong growth, recovering to 80% of its pre-COVID levels.

- TCOM reported strong Q2 earnings as a result of robust travel recovery along with strong market share gains.

- We believe the recent price correction offers an attractive entry point for long-term investors and initiate a Buy.

Investment Thesis

Trip.com ( TCOM ) shares have outperformed the KraneShares China Internet ETF ( KWEB ) having rebounded over 75% since it bottomed in Oct 2022 compared to KWEB's jump shade below 50% amidst Chinese recovery. TCOM is also one of the most favored sell side analysts' stock recommendations with 30 out of 31 ascribing a Strong Buy or Buy rating with the exception of one rating as a Hold.

Seeking Alpha

We believe despite the apparent crowding and recent profit booking, the strong earnings momentum driven by industry recovery and market share gains as a result of its strong positioning within the overall Chinese travel market provides an attractive entry point for long term investors. We initiate with a Buy rating and assign a target price of $42 (at 21x Fwd P/E in line with the global peer Booking.com).

Company Background

Trip.com is a leading one-stop travel platform for users globally offering accommodation, transportation, package tours and corporate travel reservations. It operates through several brands including Ctrip and Qunar (primarily for domestic customers), and Trip.com and Skyscanner (mainly for international customers). It generates majority of its revenues from China with accommodations and ticketing being the key revenue contributors.

Robust Travel Demand

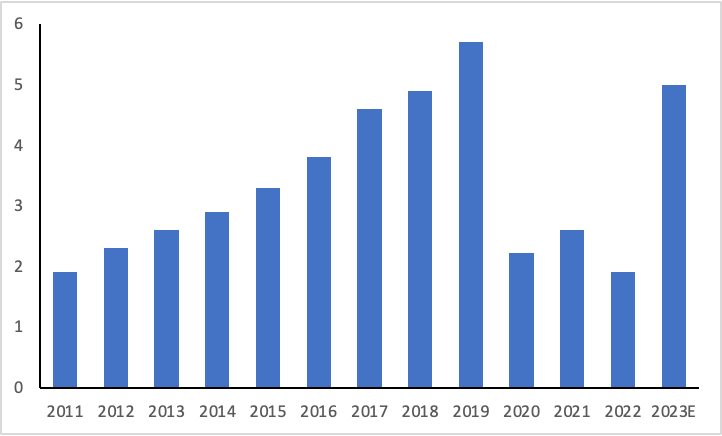

According to China Tourism Academy, domestic travel revenue increased at a strong 14.7% growth between the 2011-2019 period driven by increasing number of tourists which more than doubled during the period along with higher spending. It declined 61% YoY in 2020 as a result of COVID-19 and remained around the 2 trillion mark for 2021 and 2022 amidst the country's aggressive lockdown strategy. However, post lifting of the COVID-19 restrictions, travel demand has soared and domestic travel revenue is expected to reach 5 RMB trillion in 2023, 80% of the pre-covid levels with an estimated 5.5 bn trips.

Domestic Travel Revenue (RMB tn)

{kind=link}

While there are concerns about the overall macro scenario, Chinese have saved significantly during the COVID-19 pandemic with household deposits totalling 132 trillion yuan (US$18.3 trillion), an increase of 12 trillion yuan in H1, highest increase in a decade which may enable them to fend off any macroeconomic shock.

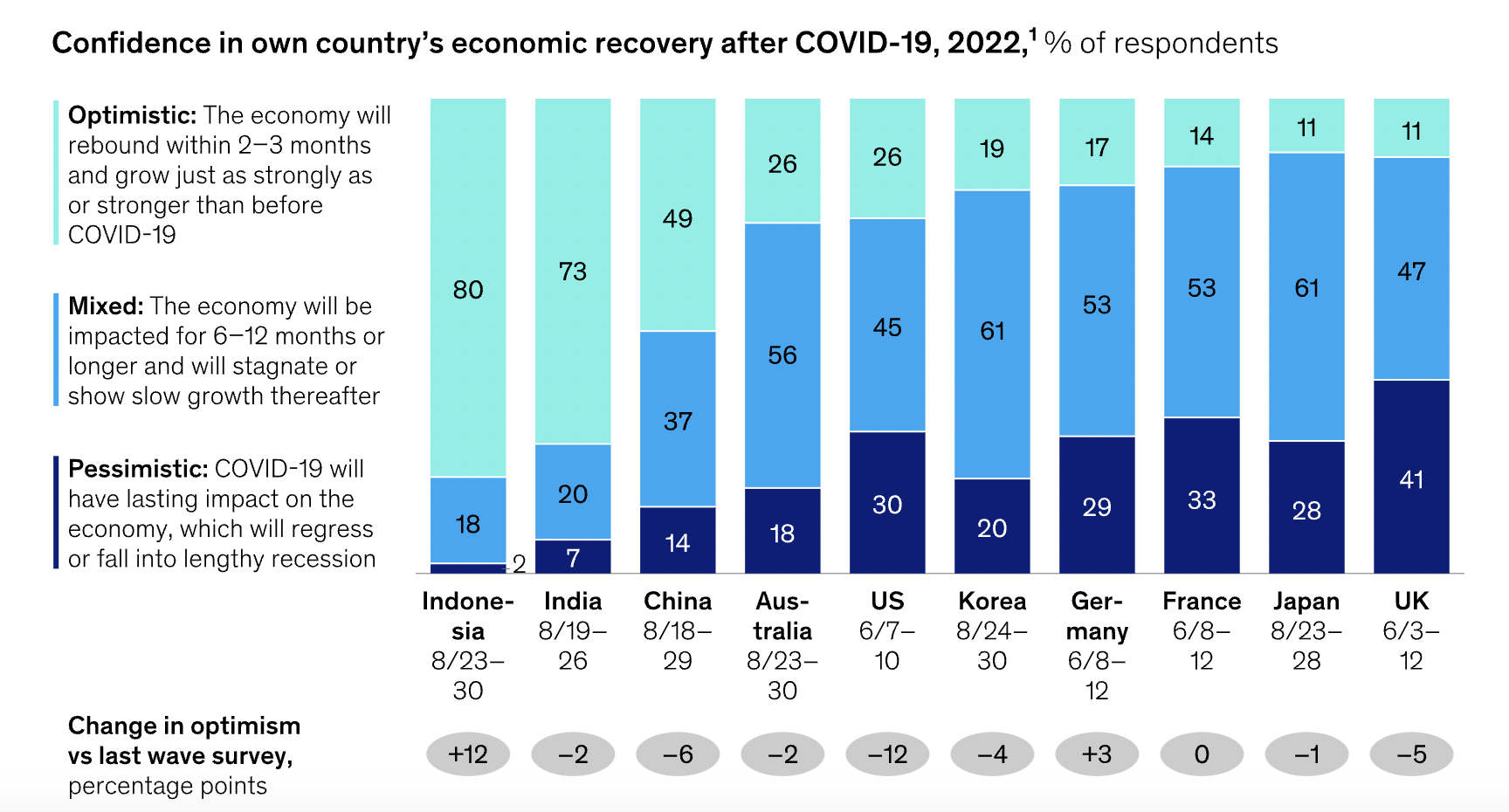

According to a McKinsey report , optimism regarding the economic growth has fallen significantly for several major economies, however, Chinese people are still among the most optimistic among other countries expecting that the economy will rebound strongly - only lower than Indonesia and India.

{kind=link}

Strong Q2 Earnings

TCOM reported a strong 180% YoY growth in revenues and 22% sequentially in Q2 ahead of the consensus expectations. The solid growth came from business recovery across all segments driven by robust recovery in domestic and international travel markets. It reported domestic hotel bookings growing over 170% YoY in the quarter, 60% higher than pre-COVID level. Outbound hotel and air reservations grew to over 60% over 2019 levels, significantly surpassing the industry at 37% demonstrating strong market share gains as a result of its strong brand resonance. Air ticket bookings also grew 120% YoY and doubled compared to pre-COVID levels driven by industry tailwinds and market share gains. In addition, packaged tour revenues grew 492% YoY and 87% sequentially while corporate travel revenue jumped 178% YoY and 31% sequentially.

Gross margins improved over 6 percentage points YoY to 82.2% driven by outsized growth in revenue and significant improvement in utilization. Gross margins remain above the pre-COVID levels as a result of the continued market share gains and its shift towards higher take rates.

Selling and Marketing expenses deleveraged by 30 bps driven by an increase in promotions and marketing activities while G&A expenses as % of revenue improved by over 650 bps primarily as a result of fixed cost leverage due to strong growth in revenue. Product expenses as % of sales improved 18 percentage points as strong revenue growth outpaced the increase in personnel expenses and related development. In all, it reported an Adj. EBITDA margin of 33%, improvement of 24 percentage points over the previous year along with over 2 percentage points sequentially.

Balance sheet position continues to improve as the company ended with cash balance of ~$7.3bn with total debt outstanding of ~$7.1bn driven by strong cash generation over the past few quarters.

Management maintained that TCOM's outbound hotel and air bookings have recovered to 80% of Pre-COVID levels in Q3 2023 QTD with outbound flight capacity at 50% of 2019 levels. We expect strong demand for leisure travel during the summer holidays and long national holidays in September / October which could drive continued recovery in domestic travel market. We estimate 2023 revenues to be ~28% above 2019 levels largely driven by robust domestic travel which we expect to grow by 60% along with sequential recovery in international outbound travel which is expected to be about 50-60% of pre-COVID levels with a gradual increase in flight capacity. We expect 2024 revenues to further grow by high teens driven by a double digit revenue growth in domestic travel along with 40% growth in international travel which is expected to recover to pre-COVID levels by 2024.

| Particulars |

| 2019 Revenues |

| 2023E Change vs 2019 |

| 2023E Revenues |

| Total Revenue |

| 4,768 |

| 28% |

| 6,080 |

| Domestic Travel |

| 3,100 |

| 60% |

| 4,960 |

| International Travel |

| 1,668 |

| (40%) |

| 1,120 |

| Outbound |

| 1,192 |

| (30%) |

| 835 |

| Inbound |

| 476 |

| (40%) |

| 286 |

We expect non-GAAP operating margins to climb to 28%, up 9 percentage points from 2019 levels driven by robust travel recovery and strong gross margins along with efficiency improvements. The strong operating margins are driven by a 15 percentage point improvement in domestic travel while expecting a 14 percentage point decline in international travel. We expect overall operating margins to stabilize at 28% in 2024 as higher sales and promotion activities can lead to a slight decline in operating margins for domestic travel offset by a swift recovery in margins for international travel.

Valuation

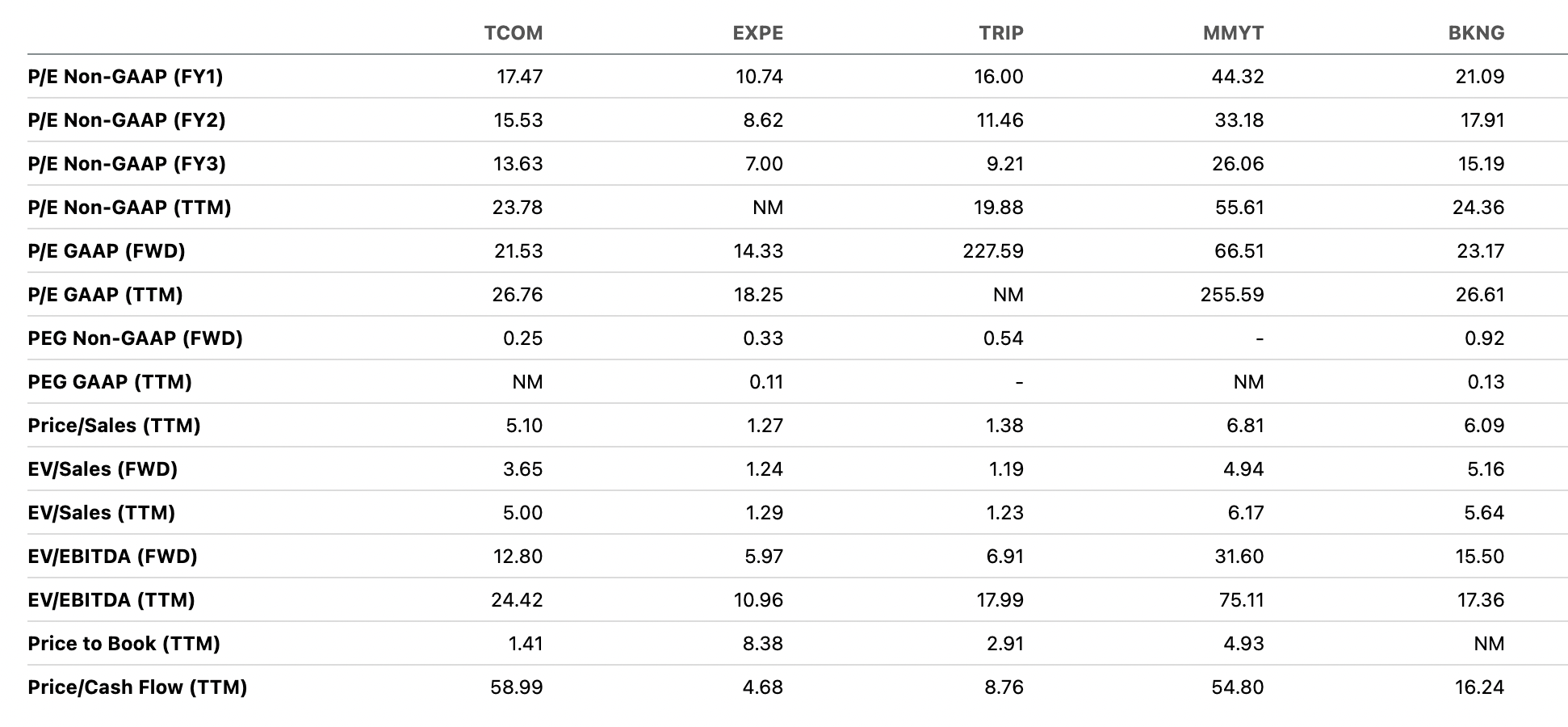

TCOM trades at 17.5x Fwd P/E and is stacked in the middle compared to other peers. However, Expedia ( EXPE ), Tripadvisor ( TRIP ) and Booking ( BKNG ) generate the bulk of the revenues in mature markets within North America and Europe which are undergoing significant macro uncertainty while TCOM is still significantly cheaper than MMYT with exposure in fast growing markets such as India and China which seems to be relatively better off. We value TCOM at 21x Fwd P/E (in line with the global peer, Booking.com) and ascribe a target price of $42.

{kind=link}

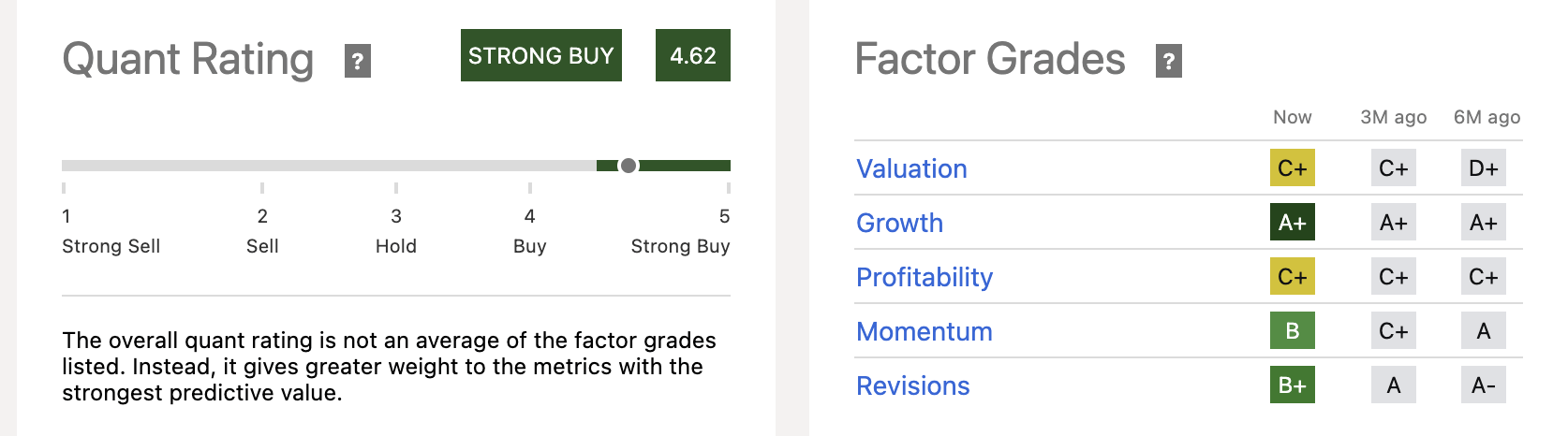

Seeking Alpha's Quant rating ascribes a "Strong Buy" to TCOM driven by upward revisions to its earnings profile and strong growth momentum.

{kind=link}

Risks to Rating

Risks to rating include

1) Potential slowdown in China's economy can negatively impact the overall travel demand

2) Geopolitical tensions can have an adverse impact on the tourism industry

3) Natural calamities and any spread of contagious diseases such as COVID-19 can significantly hamper the travel market as witnessed during 2020-2022 period

4) Recovery in China's international travel demand may be slower than anticipated heading into 2024 due to macro concerns and slower ramp up in capacity additions by airlines and hotels

4) Competitive pressure may intensify and TCOM may have to reduce commission rates or aggressively spend on sales and promotional activities which can significantly impact its operating margins

Final Thoughts

TCOM has reported strong growth in recent quarters driven by a robust recovery in the Chinese travel industry along with market share gains. It has a strong momentum entering H2 2023 as a result of pent up demand for travel, in particular, during the holiday season of September/ October. We believe from valuation perspective TCOM still appears undervalued looking from PEG perspective (TCOM is currently trading at 0.25x compared to peer average of 0.6x) and strong cash generation over the coming quarters. Initiate a Buy with a target price of $42.

For further details see:

Trip.com: Favorable Tailwinds In Play, Initiate A Buy