TCOM - Trip.com: Positioned To Recover As China Actively Attempts To Boost Tourism

2023-12-25 11:44:37 ET

Summary

- Investor confidence in China has been shaken, but there are still opportunities for traders in the equity market.

- Trip.com is a promising long-term investment in China's online travel industry, and is likely heading higher within 12 months.

- The normalization of the travel industry in China is expected in 2024, and Trip.com is well-positioned to benefit from the rebound.

Investor Confidence in China takes a hit but we remain bullish on a messy bottoming phase for their economy

If you are an investor with a traditional long-term approach in China, no doubt there has been disappointment and even frustration in the outcomes from the past 2 years. I do believe the investing landscape for China will improve in the future.

If you are a trader with a defined return target and have spent the time to develop the skillset of knowing what levels are likely to cause a bounce reaction and which regions are levels where the market-makers are ready to dump (reset) the stock, China's equity environment is still tough but continuously offers opportunity.

Case in point, I wrote a positive opinion piece on NetEase (NTES) and a Black Swan Event essentially eviscerated the stock. That said, as a Trader in the China sector, we found an opportunity to buy (and later close) long-dated calls on NTES at Friday's open for a 30% intraday gain.

Survivors in the China investing landscape have learned to focus and trade on price action and while macro policy from the Mainland is almost impossible to predict, there will be Alpha at the right levels.

Trading Calls on NetEase (Interactive Brokers - My Position)

{kind=link}

Despite the harsh investing environment, China as a sector is my specialty and I cannot abandon it. I am regularly invited to conferences to talk about investing in China, and I routinely share my conclusion that rapidly changing sentiment is part of the game. There is a high degree of mental adaptability that is required.

There also continues to be names that will work on long-term timeframes, and one of them I believe is Trip.com (TCOM). We believe that the stock is going higher and that investors who already own the stock should Hold for further recovery. I've been an investor in this name since the mid-20s and I continue to have a favorable long-term outlook on it.

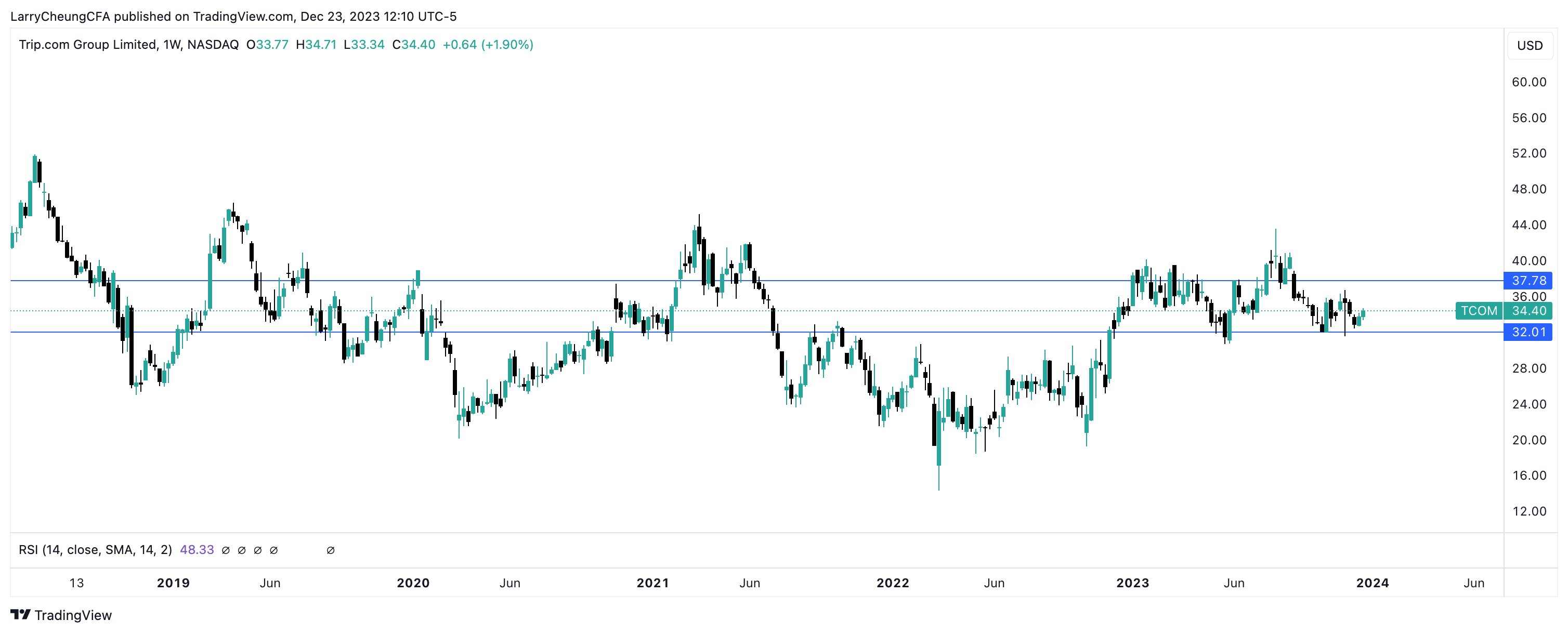

TCOM Technical Structure (YCharts)

{kind=link}

The Catalysts for Trip.com and Fundamental Outlook

Trip.com is China's leading online travel and hotel accommodation booking agencies. With over 1.4 million hotels on its platform, it is by far the leader in China's Online Travel Agent ((OTA)) industry. The next closest competitors include Meituan (360K listings) and Fliggy (200K listings).

As of the latest quarter, the company did 13.74B Yuan in revenue and held an operating margin of 29% which beat expectations by nearly 2% in a challenging spending environment in China. The travel industry in China is expected to normalize in 2024 as international outbound travel becomes a greater focus point for the OTA industry and TCOM in particular. As of now, TCOM's international travel business has recouped approximately 80% of pre-pandemic revenue. While volumes are down, airplane tickets have skyrocketed 20-30% from pre-pandemic levels which have offset fewer people traveling abroad.

Geopolitics between Mainland China and the EU and U.S. do play a role as visa applications are key to having TCOM's international travel business remove the current bottleneck that it is experiencing. Long visa wait times are a major key factor holding back a rebound from mainland Chinese citizens looking to travel internationally, and the U.S. Travel Association estimates the following industry observation :

As U.S. Commerce Secretary Gina M. Raimondo makes an official visit to China, new U.S. Travel Association analysis shows that a complete rebound in Chinese visitation (to 2019 levels)—which is currently substantially trailing other nations—would boost the U.S. economy with an additional 2 million visitors a year and more than $11 billion in export spending.

The U.S. Travel Association also estimated that China was the third largest source of overseas travelers to the U.S. and that Chinese visitors typically spend more than $5K per trip so there is economic incentive for visa wait times to be accelerated.

The positive aspect about this is that tourism travel to the U.S. is unlikely to face the myriad of roadblocks that current exist in the Semiconductor and Tech Chip cold war that the U.S. and China are currently encountering.

Right now, according to the U.S. Travel Association , the wait times on visa to travel from China to the U.S. is about 164 days. In addition, the weekly flights from China to the U.S. is less than 10% of pre-pandemic capacity.

There is large opportunity for these bottlenecks to resolve over time and that will greatly help Trip.com outperform next year's revenue estimates.

In the meantime, investors will focus on China's domestic travel fundamentals which are currently solid in today's consumer spending slowdown. China's Tourism Academy (reported from Ministry of Culture and Tourism on ChinaDaily) estimates that the figure of tourism related revenue will increase 114% in the first 9 months of 2023 compared to last year, which then re-captures 90% of the pre-pandemic level. This feat is quite impressive given the deep macroeconomic slowdown happening across China. TCOM's competitive pricing and scale as the leading OTA will help it bounce back faster than other competitors such as Meituan and Fliggy.

Ministry of Culture and Tourism Industry Commentary (China Daily)

{kind=link}

The company is also focused on cost structure management, which is top of mind for all investors in this environment. The Sell Side expects to see net margins improve to the 16-17% region from 7% in 2022 primarily due to reduced headcount, a more efficient back-end IT system that will result in productivity gains, and optimized advertising and customer acquisition spending.

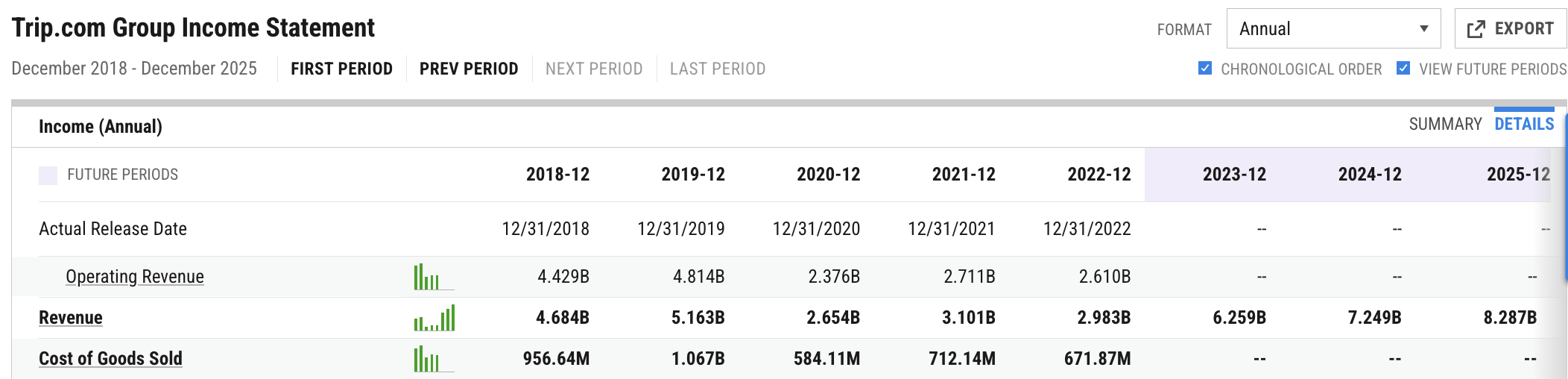

We can see from the below tables that the Street is expecting revenue and EBITDA to grow in the 10-20% growth profile, which is currently a rarity in the Hang Seng H-Shares market where most names are struggling to achieve more than 7-9% top line growth.

Table 1: Revenue Expectations of Trip.com (Expected to grow 10% in 2023-2025)

TCOM Revenue Expectations (YCHARTS)

{kind=link}

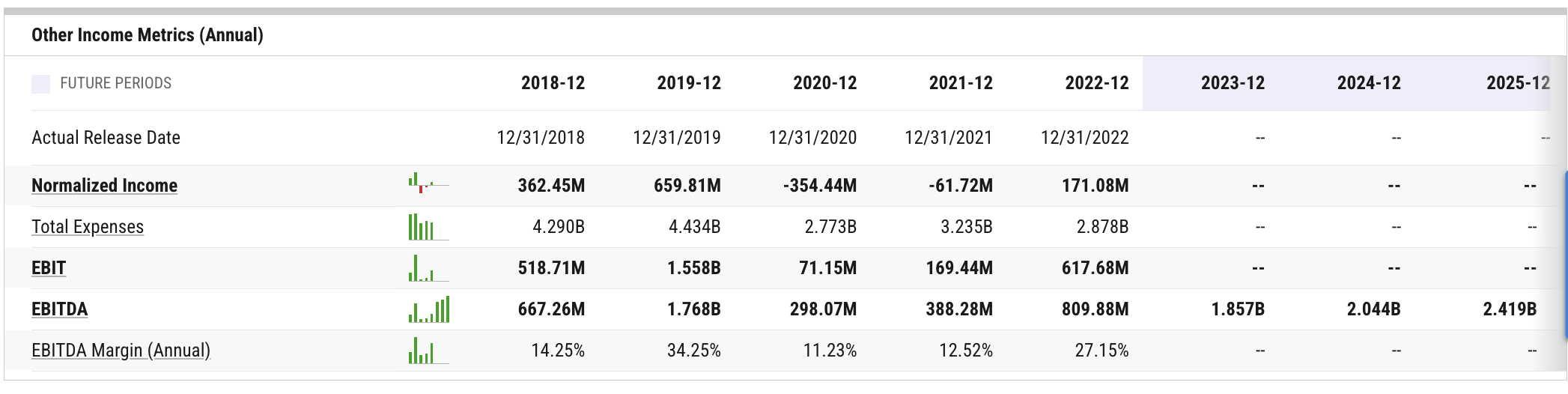

Table 2: EBITDA Expectations of Trip.com (Expected to grow 12-18% in 2023-2025)

TCOM EBITDA EXPECTATIONS (YCHARTS)

{kind=link}

Risks, thoughts on Entry & Valuation

Given that the current valuation on TCOM using its sales multiple (cannot use historical Earnings or EBITDA because previous years were lumpy due to pandemic) is near historic troughs, there is reasonable room for valuation expansion once Visa wait times are lowered, and capacity for flights from China to the U.S. is increased.

There are a number of macro and company-specific risks we will want to keep on our radar. The obvious big picture risk that investors should pay attention to is that China's consumer consumption weakness still persists, is clearly reflected in indirect proxies such as e-commerce spending BABA/JD's earnings outcomes, and also shows from the latest Golden Week results which showed a 10% increase over 2019 in air travelers (Analysts had been expecting more). Another key over-arching risk that may prevent TCOM from reaching its potential is if U.S. and China relations deteriorate further and the U.S. delays wait times for Visas for Chinese travelers as well as any lowering in flight capacity from China to the U.S. If that happens, it will take longer than expected for TCOM's international business segment to rebound, and that is where most of the upside potential comes in for 2024's revenue, EBITDA, and EPS estimates come in to outperform the Street's expectations. Before 2019, the international business segment was nearly 25% of its business mix but due to travel restrictions, it is currently less than 5% of the mix. We would need to see the international business segment grow again for the stock to gain strong favor among investors.

Investors looking for opportunities in China may want to focus on areas that are least likely to be impacted by sudden regulatory changes. NetEase and Tencent will likely see a technical bounce from its pre-Christmas selloff, but the gaming industry has structurally changed so any bounces in NTES is likely an opportunity to reduce exposure. Tencent is a bit more diversified, so its fundamentals should be somewhat more shielded but in the short-term sentiment drives price action in China stocks.

I personally view the travel industry to be a bit more insulated from the regulatory landscape as China is actually actively looking to boost its domestic tourism industry . I also believe that if U.S. and China relations stabilize, one of the more "negotiable" areas of an improved relationship is greater travel access between the two countries. That is my opinion, but of course, the landscape can change adversely as we know and the ongoing geopolitical developments remain as macro risks.

That being said, I believe that once the China market domestic travel industry and international travel segment recovers (and it has a high likelihood of doing so on long timeframes), Trip.com will continue its gradual ascent higher on investment timeframes.

For further details see:

Trip.com: Positioned To Recover As China Actively Attempts To Boost Tourism