TCOM - Trip.com: Short-Term Margin Headwinds Long-Term Resilience In Sight

2023-11-22 00:11:14 ET

Summary

- Trip.com Group reported strong Q3 earnings, beating analyst estimates for both earnings per share and revenue.

- Despite the positive earnings, the stock price fell 8% as investors had already priced in future growth expectations and potential margin contraction risk short term.

- The company's international travel business is expected to grow, and its valuation multiples are relatively low compared to historical levels.

- Despite short-term risks, TCOM maintains leadership in China's online travel industry and stable profit margins.

Q3 Earnings and Stock Performance

Trip.com Group Limited (TCOM) reported its third-quarter earnings on November 20th, 2023. Even though the company surpassed the analyst estimates for both earnings per share and revenue for the third quarter, the stock price fell 10% after the earnings report was released. One potential explanation for the stock drop, despite the earnings beat, is that investors had already priced significant future growth expectations into TCOM's stock price over the past year. Given that the stock price has increased 33% over the last 12 months leading up to the earnings announcement, some of the future potential tailwinds and growth prospects were likely already reflected in the company's valuation. As a result, even a strong third-quarter earnings beat was not enough motivation for investors to further bid up the stock price.

{kind=link}

Investment Thesis Highlight

TCOM is facing some short-term risks due to management's comments about potential margin compression during the third quarter earnings call. However, the company still maintains a leadership position in the online travel industry in China and has demonstrated the ability to produce strong and stable profit margins over time. We believe TCOM has more room to grow its international business moving forward through its strong partnerships with travel suppliers, which will allow it to effectively compete with other Chinese online travel agencies.

Additionally, TCOM's valuation multiples continue to trade at a relatively low level compared to its historical range. As a result, we view the downside risk for the stock as limited at the current valuation. Our focus remains on the long-term growth potential for TCOM's business, and we believe the stock has more upside from current levels. We rate the stock as a Buy.

Financial Review

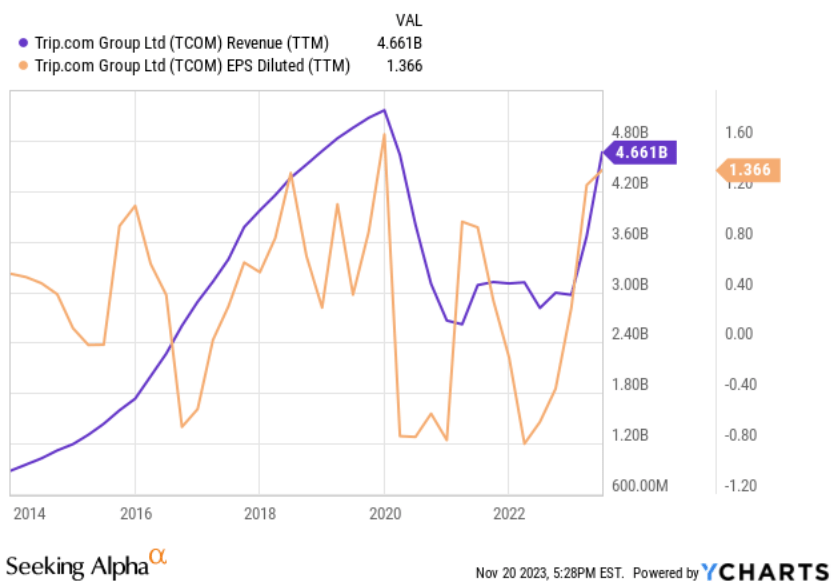

The company's revenues increased by 99% in Q3, and its adjusted EBITDA margin improved to 34% from 21% in Q2 or 33% last year. China lagged behind in the lockdown schedule, so the country's robust growth rate is likely a reflection of the lockdown's comparatively subpar performance the previous year. Nonetheless, the business's profits and revenues for the previous 12 months were both getting close to surpassing their all-time high.

{kind=link}

Specifically, TCOM's domestic travel business within China has already passed pre-COVID financial levels, while its international travel bookings have recovered to around 80% of 2019 volumes. Given the significant room for further international travel demand recovery, we believe TCOM could grow both revenues and earnings to exceed historical peak levels in the coming years as COVID impacts continue to subside globally.

- Domestic hotel bookings grew by 170% year over year and by over 60% compared to the pre-COVID level for the same period in 2019.- Outbound hotel and air reservations recovered to over 60% of the pre-COVID level for the same period in 2019, surpassing the industry-wide recovery rate of 37% in terms of international air passenger volume for the same period.

During the earnings call, TCOM's management mentioned that the current recovery in international travel demand has been driven by increased travel within Asia and the Middle East regions.

APAC regions such as Hong Kong, Macau, Thailand, Singapore, Korea, Japan remained top outbound destinations due to the higher recovery in flight capacity and easy visa application......In particular, hotels in more than 15 popular destinations, including Dubai, Paris, Kuala Lumpur have offered tailored services such as Chinese language support and payment.

Additionally, they noted that demand and search volumes for outbound travel from China have already exceeded 2019 levels. However, actual outbound bookings have been restricted due to supply constraints like limited flights and hotel room capacity.

If you look at our demand and supply side, the demand already exceeded 2019 level....The first one is the visa application process takes a little bit longer for certain regions, such as Europe, United States, et cetera. However, after the APAC meeting, I think there will be improvements on the visa application side. The second one is the flight capacity. As of Q2 -- as of Q3, the flight capacity only recovered 50%

Given that China has started to ease more restrictions on overseas travel to the United States after the APEC summit meeting concluded in November, it is expected that TCOM's international travel business, especially to North America, will gain additional momentum in the following quarters after this regulatory change.

Our business has consistently performed well, breaking previous records in hotel and air bookings. Additionally, outbound travel is rapidly recovering, thanks to improvements in international airlift and travelers’ robust desire for international experience. So, we anticipate a continuously strong demand for outbound travel in the coming year and are committed to enhancing our partner offerings to meet this demand.

Risks

Domestic Competition Risks

TCOM currently faces increased competition in the China online travel industry from strong peers such as Meituan and Douyin.

Given Meituan and Douyin's high frequency consumer platforms in other sectors like food delivery, their traffic acquisition costs are much lower than TCOM's. As a result, these two companies have aggressively grown their presence in the online travel booking space in recent years.

TCOM's current strategy to compete is to leverage its core capabilities in supply chain technology and booking system algorithms to deeply partner with travel suppliers. For example, TCOM purchases hotel room and flight ticket inventory directly from suppliers in advance and provides end-to-end customer service to simplify the workflow for its partners. As a result, even though Douyin drives significant consumer traffic, it lacks the dedicated customer service teams to handle complex travel-related issues. Consequently, airlines and hotels still prefer to closely collaborate with TCOM over alternative platforms.

And I think OTA and content platform have totally different core competence. Content platform excel at producing creative content and sharing information, make them effective at promoting trending products. However, most of the content platform, they lack very strong back-end system to fulfill the booking capabilities, while OTA’s core competence in the -- firstly, in the supplier chain -- standard supplier chain and also, more importantly, the capabilities to provide reliable services.

We believe there is more serious competitive pressure from Meituan compared to Douyin, as Meituan has demonstrated the capability to handle travel bookings and customer support at scale - directly competing with TCOM's core strengths. However, Meituan's key advantage remains the sheer size of its domestic user base.

In contrast, TCOM has cultivated a strong market presence, specifically in international travel, over the past decade and has forged close partnerships with overseas travel suppliers. As a result, we think TCOM should still retain significant competitive advantages in serving outbound Chinese travelers and cross-border travel booking needs compared to Meituan. While Meituan's desktop and app traffic is massive domestically, TCOM continues building out its global supply chains. Hence, TCOM and Meituan may ultimately carve out a duopoly in China's online travel industry with more delineation between domestic and international focus.

Margin Risks

During the earnings call, TCOM's management noted that the company's current high-profit margins are likely not sustainable. They explained that travel demand has rebounded much faster than anticipated post-COVID, and TCOM will need to increase spending on sales and marketing to support this growth.

Specifically, management expects long-term adjusted EBITDA margins of 20-30% to be more sustainable compared to the 34% margin delivered this past quarter.

So, in the longer period , we think we will definitely achieve -- previously, we have -- give guidance to our shareholders that to achieve the margin level toward like -- to the 20% to 30% level.

This lower margin outlook is a risk factor that could cause TCOM's valuation multiples to contract. Investors seem to have reacted negatively to the peak margin commentary, leading to the post-earnings stock price decline despite the company beating revenue and earnings expectations in the third quarter.

Valuation

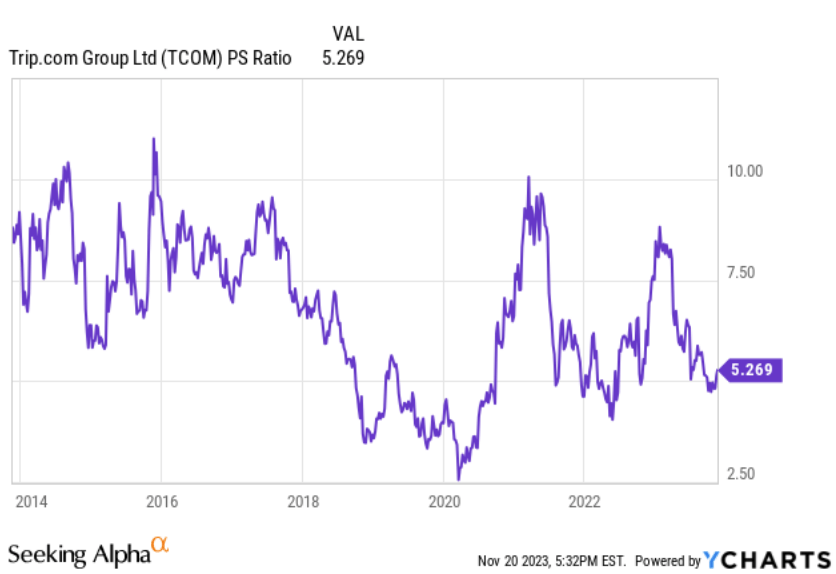

TCOM currently trades at a P/S ratio of 5.2x, which is near the bottom of its historical valuation range.

{kind=link}

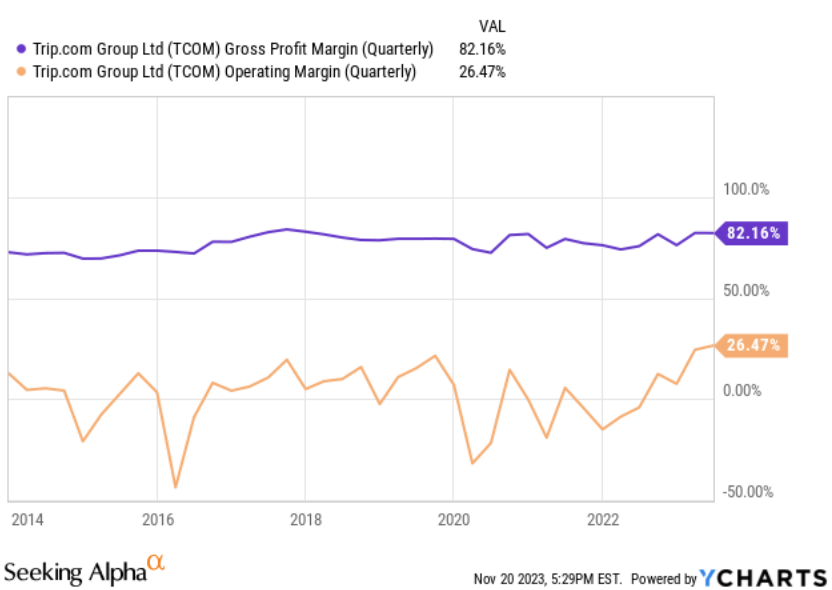

The management's outlook for increased spending on marketing and customer service to support a lowered 20-30% adjusted EBITDA margin poses some downside risk factors for profitability. However, TCOM has been able to consistently maintain strong gross margins historically even through competitive challenges. This suggests the company continues maintaining a competitive position in China's online travel industry, despite the rising competition from Meituan and Douyin.

We believe as TCOM expands its international travel business and corporate travel offerings, it can further strengthen partnerships with overseas and domestic suppliers that will help secure its market leadership in the long run. If TCOM proves it can maintain sector leadership, the short-term margin compression risk seems an acceptable trade-off to us.

Given the current low valuation multiple against the backdrop of TCOM's growth recovery momentum in international markets, we see attractive risk-reward at current levels for long-term investors.

{kind=link}

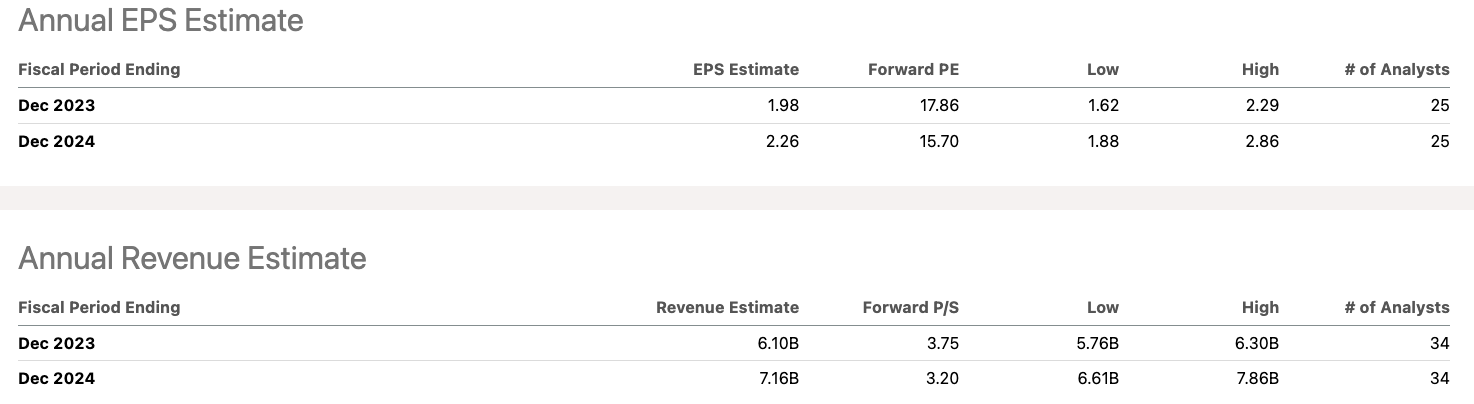

Sell-side analysts currently estimate TCOM trading at a forward price-to-sales ratio of 3.75x for 2023 and 3.2x for 2024. Both of these forward valuation estimates remain below the company's long-term historical median price-to-sales ratio. The discounts to TCOM's normal valuation range make the stock attractively priced for long-term investors.

{kind=link}

Conclusion

TCOM has maintained its leadership position in China's online travel industry through its strong booking system capabilities and customer service offerings. Despite rising competition from companies like Meituan, TCOM has continued to produce healthy profit margins over time. Its current valuation multiples are at the bottom of historical ranges, limiting further downside risk, in our view.

Although margin compression concerns contributed to the post-earnings stock price sell-off, we believe this presents a buying opportunity for long-term investors. TCOM is nearing an inflection point where both revenue and earnings surpass pre-COVID peaks amid a broader travel demand recovery. Once supply bottlenecks ease and restrictions further relax, TCOM’s growth trajectory remains very positive.

Given the company’s competitive strengths in technology and partnerships, leadership position sustenance, and low historical valuation, we rate the stock as a Buy for long-term investors willing to look through near-term margin shifts. We would be buyers on additional stock price weakness driven by short-term margin fears.

For further details see:

Trip.com: Short-Term Margin Headwinds, Long-Term Resilience In Sight