TCOM - Trip.com: Strong Top Line Growth Driven By Recovering Travel Demand

2023-10-05 10:59:11 ET

Summary

- Trip.com's Q2 2023 earnings report shows remarkable growth, with revenue surging by 180% YoY.

- The Chinese travel industry is in a recovery phase, providing favourable conditions for Trip.com's expansion.

- Trip.com's stock has an appealing forward price-to-earnings ratio relative to its online travel industry peers.

Trip.com ( TCOM ) stands as China's leading travel platform. In its recent Q2 2023 Earnings report, the company showcased remarkable growth, with revenue surging by 180% YoY, primarily fueled by the robust domestic and international travel demand. Nevertheless, the stock has experienced a decline following the earnings release, partly attributed to a significant YoY expense increase. Additionally, uncertainty looms regarding the complete recovery of the outbound travel market, which presently stands at 60% of pre-pandemic levels.

Stock trend year to date (SeekingAlpha.com)

{kind=link}

However, the Chinese travel industry is in a recovery phase compared to the past three financial years. It enjoys favourable conditions that can expand the company's addressable market, including an extended Golden Week holiday and a growing customer base in an industry rebounding to pre-pandemic demand levels. Additionally, the stock boasts an appealing forward price-to-earnings ratio of 20.47, relative to its peers, suggesting further upside potential. Consequently, investors might consider adopting a bullish outlook on this stock.

Company overview

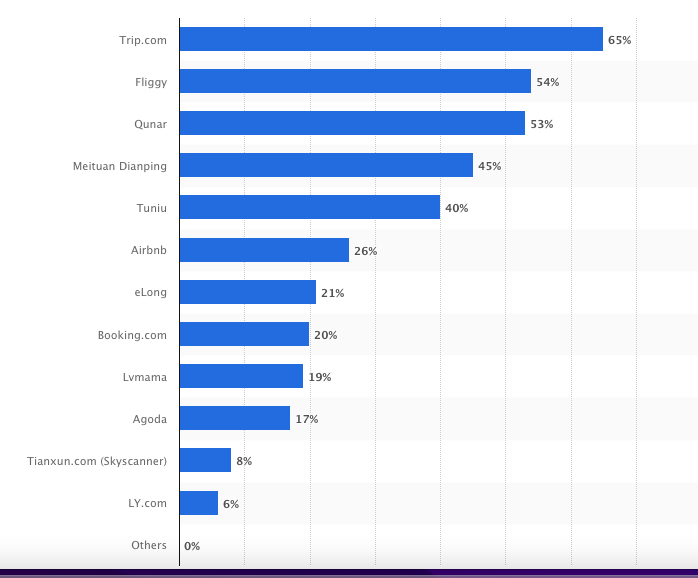

Trip.com is a leading online travel provider in China, experiencing significant revenue growth, especially in Q2 2023. Founded in 1999, it's been publicly traded on NASDAQ since 2003 and on HKEX since 2021. They manage well-known brands like Ctrip, Qunar, Trip.com, and Skyscanner. A recent survey shows that 65% of Chinese individuals prefer Trip.com for travel planning.

Most popular online travel agencies among consumers in China as of June 2023 (Statista.com)

{kind=link}

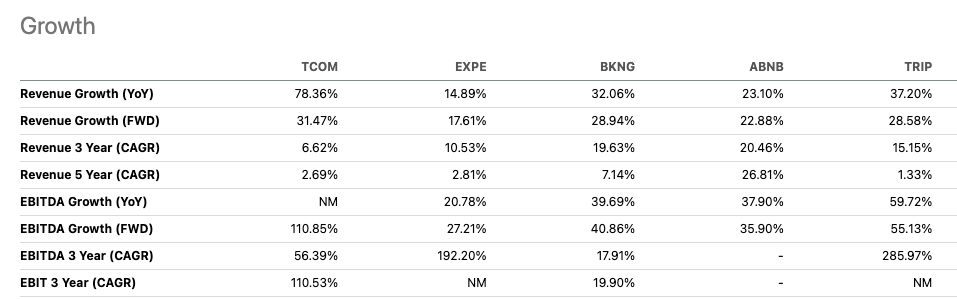

Trip.com is a travel platform that uses technology and innovation to keep up with the changing travel landscape. They provide unique experiences to travellers and make money through commission fees from bookings like hotels, flights, car rentals, and vacation packages. They partner with travel providers such as hotels, airlines, and transport companies and earn a share of the booking cost for connecting them with travellers. Additionally, they generate income from premium services and targeted advertising. Trip.com provides innovative tools such as virtual travel guides and personalised recommendations to enhance their revenue. Compared to competitors like Expedia Group ( EXPE ), Booking ( BKNG ), Airbnb ( ABNB ), and Tripadvisor ( TRIP ), Trip.com has achieved a year-over-year growth rate of 78.36%.

Growth versus peers (SeekingAlpha.com)

{kind=link}

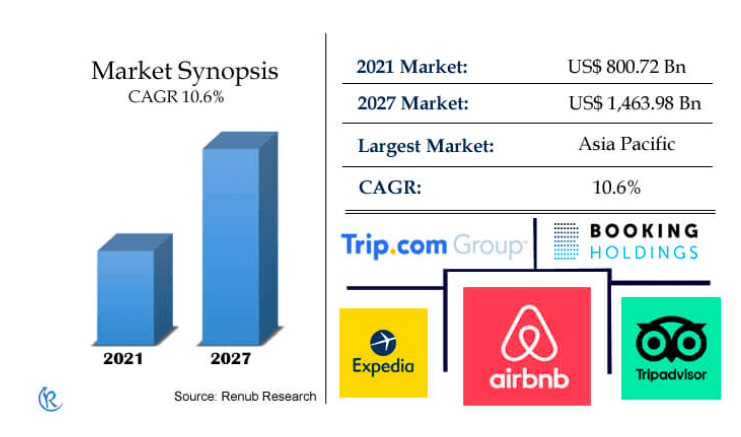

Moreover, the online travel industry is forecasted to grow at a steady rate of 10.6%. Trip.com, with its solid position in the rebounding Chinese market, has an opportunity to extend its global reach further. This can be achieved by focusing on the burgeoning online markets in Southeast Asia, Latin America, and Africa. These regions are experiencing significant growth in tourism and e-commerce. By expanding into these markets, Trip.com can access emerging sectors such as eco-tourism, adventure travel, and cultural experiences, catering to niche traveller segments and bolstering its revenue streams.

Online travel market (Renub.com)

{kind=link}

Financials and valuation

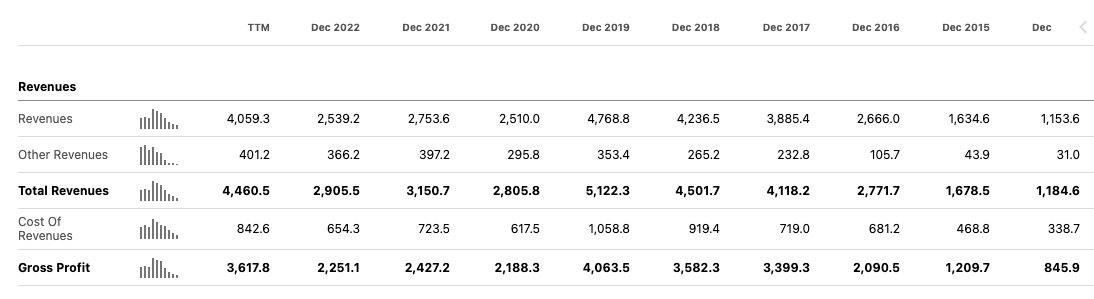

In the recent quarter, Trip.com reported strong revenue figures and its TTM revenue of $4.06 billion indicates a promising return to pre-COVID-19 performance levels. Additionally, the TTM gross profit exceeds the figures from the three previous financial years, which were significantly impacted by pandemic-related regulations.

Annual revenue and gross profit growth (SeekingAlpha.com)

{kind=link}

When examining the TTM net income of the company, which amounts to $872.3 million, it becomes evident that this represents a substantial improvement compared to the performance in the three preceding financial years.

Annual net income (SeekingAlpha.com)

{kind=link}

The company's leveraged free cash flow has shown a consistent upward trend over the past three years, although we can see the pandemic's negative impact on its cash flow. Moreover, their financial strength is underscored by a substantial balance of $10.3 billion in cash and equivalents, restricted cash, short-term investments, held-to-maturity time deposits, and financial products. Furthermore, the current ratio is a healthy 1.10, signifying the company's capacity to meet its short-term obligations.

Annual levered free cash flow (SeekingAlpha.com)

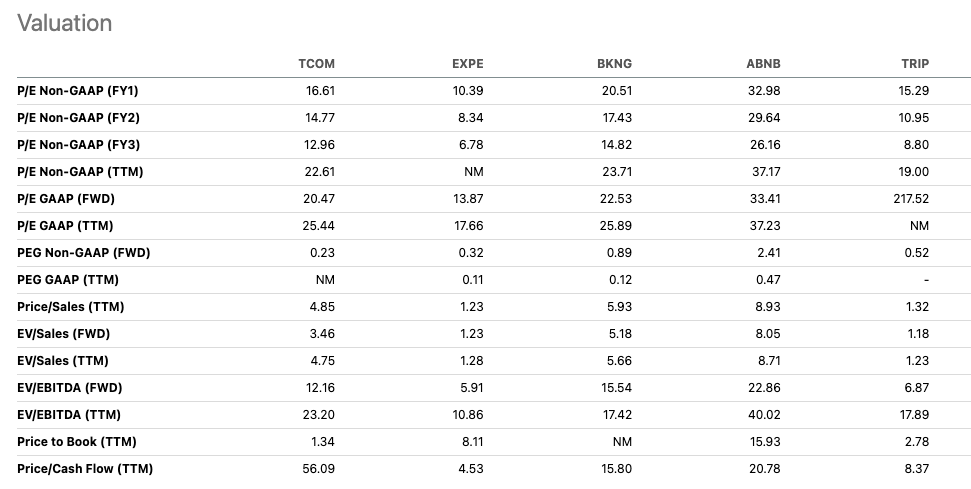

The stock is trading below its average price target of $50.22, offering a potential upside of 51.68%. Despite an 11.23% drop in value over the past month, Wall Street analysts maintain a bullish sentiment with a strong buy rating of 4.7. When comparing its valuation to other online travel platforms, Trip.com appears favourable. It boasts an FWD price-to-earnings ratio of 20.47, which is lower than most peers, excluding Expedia at 13.87. Additionally, factoring in the growth rate yields a low FWD PEG ratio of 0.23, the most attractive among its peers. Considering the recovery of the Chinese tourism market and Trip.com's advantageous position, the stock may be an appealing buy at its current price point. Furthermore, the price-to-book ratio is lower than its peers, suggesting the stock might be undervalued.

Relative peer valuation (SeekingAlpha.com)

{kind=link}

Risks

Trip.com operates within the fiercely competitive online travel agency market, competing against peers like Expedia, Booking and Airbnb. While it maintains its stronghold position, these companies could pose challenges within the Chinese market and impact its potential future growth. Furthermore, we should be cautious of the economic uncertainty and its potential impact on a recovering travel industry. Lastly, Trip.com heavily relies on third-party service providers, and any disruption or failure in their services could have detrimental consequences for Trip.com's operations and customer satisfaction, ultimately impacting the business negatively.

Final thoughts

Trip.com has demonstrated impressive top-line growth in the past two quarters, primarily fueled by the rebounding Chinese travel market and rising domestic and international travel demand. Despite operating in a fiercely competitive landscape, the company boasts diverse offerings and agile technologies to respond to evolving customer preferences swiftly. While pre-pandemic figures have yet to be surpassed, Trip.com indicates robust top-line growth in a thriving industry with untapped potential in new markets and customer segments. Consequently, investors might consider adopting a bullish outlook on this prominent online travel platform.

For further details see:

Trip.com: Strong Top Line Growth Driven By Recovering Travel Demand