TRIP - Tripadvisor: What I Will Be Watching In Q4

2024-01-20 00:24:10 ET

Summary

- Tripadvisor has continued to see significant revenue growth.

- The stock's EV to EBITDA continues to trade near a 10-year low.

- Should we see a reduction in selling and marketing costs as a proportion of overall revenue in Q4, this would prompt me to revise my rating from Hold to Buy.

Investment Thesis: I take the view that Tripadvisor could have the capacity for upside if revenue continues to see growth and selling and marketing costs as a proportion of overall revenue decline from here.

In a previous article back in February 2023, I made the argument that Tripadvisor ( TRIP ) could see low growth in the short to medium-term, on the basis of rising costs despite encouraging growth in revenue.

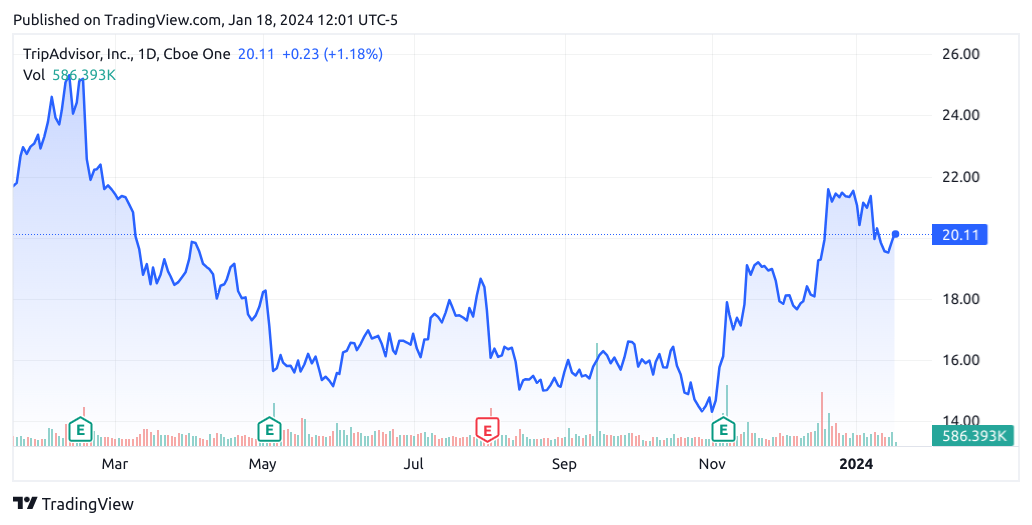

Since then, the stock has descended to a price of $20.11 at the time of writing:

{kind=link}

The purpose of this article is to assess whether Tripadvisor has the ability to see continued growth from here taking recent performance into consideration.

Performance

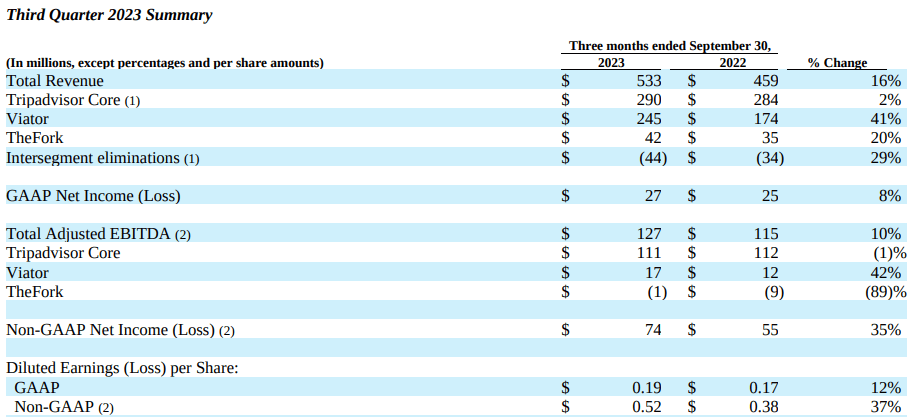

When looking at Q3 2023 earnings results for Tripadvisor as released on November 6, we can see that total revenue continued to see growth of 16% as compared to the prior year quarter, while diluted earnings per share was up by 12% on a GAAP basis.

{kind=link}

When looking at a breakdown of total revenue by quarter on a heatmap, we can see that Tripadvisor has comfortably exceeded 2019 revenue levels - with each quarter for 2023 having shown significant growth as compared to the prior year quarter.

Figures sourced from historical TripAdvisor quarterly earnings reports. Heatmap generated by author using Python's seaborn visualisation library.

While I had previously expressed the concern that rising costs had been holding down the stock - it is notable that revenue growth has largely kept pace with that of costs.

For instance, selling and marketing costs saw an increase of 16% from the prior year quarter to $272 million - but this cost represented 51% of revenue for both periods. Technology and content costs - which represent the second-largest segment of total operating expenses - saw an increase of 20% to $66 million from the prior year quarter, but represented 12% of revenue in both periods.

I had previously commended Tripadvisor on its short-term liquidity, as the company has continued to maintain a quick ratio significantly higher than 1 - indicating that it is in a good position to meet its current liabilities using existing liquid assets. The quick ratio below is calculated as (cash and cash equivalents + short-term marketable securities + accounts receivable)/current liabilities.

| Sep 2019 |

| Sep 2022 |

| Sep 2023 |

| Cash and cash equivalents |

| 838 |

| 1066 |

| 1124 |

| Short-term marketable securities |

| 95 |

| 0 |

| 0 |

| Accounts receivable |

| 218 |

| 205 |

| 234 |

| Current liabilities |

| 468 |

| 573 |

| 719 |

| Quick ratio |

| 2.46 |

| 2.22 |

| 1.89 |

Source: Figures sourced from Tripadvisor Q3 2019, Q3 2022 and Q3 2023 Financial Results. Figures provided in USD millions, except the quick ratio. Quick ratio calculated by author.

Additionally, Tripadvisor's long-term debt to total assets ratio has remained virtually constant from last year. While one would ideally like to see a reduction in long-term debt - the fact that the company has not had to boost long-term debt levels to grow revenue further has been encouraging.

| Sep 22 |

| Sep 23 |

| Long-term debt |

| 836 |

| 839 |

| Total assets |

| 2565 |

| 2636 |

| Long-term debt to total assets ratio (%) |

| 32.59% |

| 31.83% |

Source: Figures sourced from Tripadvisor Q3 2023 Financial Results. Long-term debt to total assets ratio calculated by author.

My Perspective and Looking Forward

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, we can see that Tripadvisor's EV/EBITDA ratio is trading near a 10-year low. With that being said, we see that growth in EBITDA per share has been plateauing - remaining below highs seen pre-2020.

ycharts.com

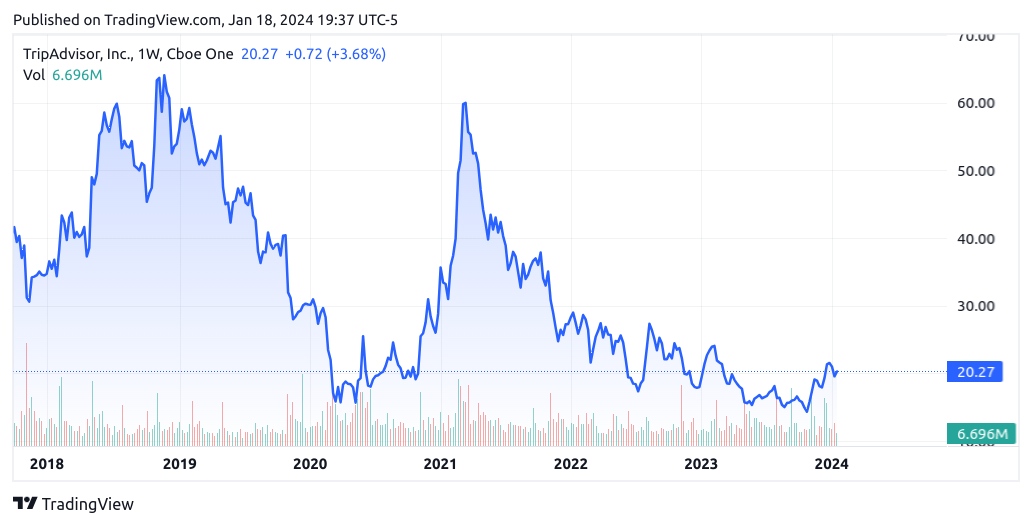

When looking at stock price from a longer-term standpoint, we can see that the stock had been trading largely within the $30-50 range in 2018 and 2019, with a high of just over $60.

{kind=link}

In this regard, I take the view that if earnings growth can rebound to the $2.00-2.40 range as seen pre-2020 - then the stock could stand to see upside back to the $30-50 price range once again.

To judge whether earnings growth can ultimately grow to this range from here - I will be paying attention to see whether costs as a percentage of revenue can ultimately decrease. While I expect that revenue will see a decline in Q4 owing to a dip in seasonal demand - I would ideally like to see selling and marketing costs as a percentage of total revenue come down. For reference, selling and marketing costs of $176 million in Q3 2019 accounted for 41% of total revenue of $428 million during the period.

In my view, if we see indications that S&M costs start to come down to a similar level - then this would be a significant sign that earnings growth has the capacity to see a significant boost later this year.

Risks

In terms of the potential risks to Tripadvisor at this time, there is the possibility that we might start to see a plateau in revenue growth for 2024. While pent-up demand on the part of consumers and the "revenge travel" phase following COVID-19 had allowed Tripadvisor to see a substantial recovery in revenue growth - there is the risk that continued inflationary pressures and high hotel prices may mean in plateau in travel demand for this year.

However, it is forecasted that demand will remain vibrant - with IATA estimating that 4.7 billion people are set to travel this year - which would break the pre-pandemic record. From this standpoint, I am cautiously optimistic that Tripadvisor can continue to boost revenue going forward.

The other risk is in relation to inflationary pressures more generally - we have seen that rising costs have accounted for a higher proportion of overall revenue than in pre-pandemic times. However, should we see inflation start to level off this year, then I take the view that Tripadvisor has the capacity to lower costs while continuing to grow revenue on the basis of continued travel demand.

Conclusion

To conclude, Tripadvisor has seen encouraging growth in revenue and the stock looks to be trading at attractive value from an EV/EBITDA standpoint. For Q4, should we see continued revenue growth and a reduction in selling and marketing costs as a percentage of revenue (ideally near the 2019 level of 41%), then this would prompt me to revise my rating on Tripadvisor from Hold to Buy.

For further details see:

Tripadvisor: What I Will Be Watching In Q4