TPVG - TriplePoint Venture Growth: A Potential Opportunity

Summary

- Shares of TPVG had fallen sharply after providing notice that a position in its portfolio would be filing for bankruptcy.

- While the hit will be significant, as they expect no recovery, this could still create an opportunity.

- This news overshadowed the other generally positive news of a special dividend.

Written by Nick Ackerman. This article was originally published to members of Cash Builder Opportunities on December 14th, 2022.

TriplePoint Venture Growth ( TPVG ) is the latest venture lending-focused business development company to succumb to a tumble after a large position in its portfolio filed for bankruptcy. This comes after Trinity Capital ( TRIN ) also had its own issues with Core Scientific ( CORZ ) coming to light last month.

TPVG is an "externally managed, closed-end, non-diversified management investment company regulated as a business development company under the Investment Company Act of 1940." It focuses on lending to venture growth stage companies.

{kind=link}

A Frank Discussion Of BDCs

I'm not sure if this is what we are starting to see now or if it is just some unfortunate luck. However, we do know that the current economic conditions are very uncertain. If I was guessing, we could start to see a bit more of these big announcements of bankruptcies leading to non-accruals in the BDC space pick up over the next year. Non-accruals and BDCs are a fact of life for those that invest in these securities. The idea is that you get more good loans/equity positions than bad; managers play a role in this as well as the style of BDC.

I think this is a good reminder that BDCs are riskier investments overall. They invest in companies that are on the smaller end. They then leverage up their portfolios, so any move to the downside is amplified. Of course, that's also their attractiveness. It is the leverage that can really juice up the yields these instruments pay out to investors.

In particular, these venture or startup growth-oriented BDCs invest in businesses that often don't have any profits. At the end of the day, no business really wants to take a loan at 6 to 10% interest rates that also are floating. If they could get financing at better terms elsewhere, I think it would be fairly obvious that they would.

Again, this is one of the upsides for BDCs as well, that floating rate exposure. They are seen as a hedge against interest rates because their income generated should go up due to the floating rate loans. That's why we've seen many BDCs raising their regular dividends and even declaring specials. It is worth mentioning that there is a point where higher interest rates break things, though.

On a YTD basis, TPVG was holding up relatively in line with its peers in terms of performance. However, with this latest move, it now joins TRIN as a significant laggard. That's precisely where an opportunity could be made.

YCharts

On a personal note, I was considering swapping Horizon Technology Finance ( HRZN ) for TPVG due to valuation. However, I now think it highlights the fact that if you are messing with BDC fire, you will get burned. You don't collect 12%+ yields because it is easy money!

Perhaps increasing diversification in this space could be seen as beneficial. So I'm not giving up on BDCs, but looking at it as an opportunity to expand to more positions in the space. Spread the love around so each one of these big hits within each BDC is reduced. Ideally, keeping the big hits to a minimum would also be a goal.

The Medly Speed Bump

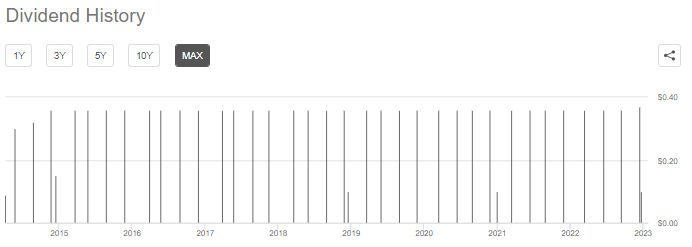

TPVG itself declared a special of $0.10 and last quarter raised its regular quarterly from $0.36 to $0.37. One of the things that drew me to TPVG to put it on my watchlist in the first place was the stable dividend that they've been able to deliver. This has been a dividend they've been able to cover as well. The latest earnings reported a net investment income or NII of $0.51. Plenty more than the $0.37 that they just raised.

TPVG Dividend History (Seeking Alpha)

{kind=link}

This is by no means a new development either, as they've consistently covered the dividend over time .

TPVG Cumulative NII To Distributions (TPVG Investor Presentation)

This news of the special was overshadowed by Medly Health Inc filing for bankruptcy. This was announced in a recent 8-K from TPVG. More importantly for TPVG was this part of the announcement where they expect the recovery to be nothing and have the entire position as a write-off.

As a result of the filings, the Company has placed its investments in Medly on non-accrual status effective October 1, 2022. Although the amount of recovery of the Company’s investments in Medly is not yet determinable, the Company expects to assign its investments in Medly a rating of 5 under its credit watch list and fully write-down the fair value of its investments in Medly, excluding the debtor-in-possession credit facility, while actively monitoring Medly’s bankruptcy proceedings on an ongoing basis to evaluate its ability to recover any amounts on its investments in the future.

Upon this coming to light, TPVG fell over 7% on a day that showed an overall strong day for the market.

TPVG Price On 12/13 (Google Finance)

If this plays out similarly to TRIN, we know that further weakness and price meandering could be in store for the next month or two. One of the big differences here is that Medly should be an isolated incident. The reason TRIN could be experiencing even further weakness is that CORZ was a crypto miner, where they still have other crypto miner exposure. I would have to say it seems that while the recovery for Medly is probably zero vs. some recovery for TRIN, the two speed bumps for these BDCs are fairly different.

What might be more interesting here is that this wasn't the first mention that something might be afoot. In the prior earnings call, they noted that they were downgrading the position with more future downgrade potential on the latest development.

We downgraded one portfolio company Medly Health, an online digital pharmacy with a total principal balance of $34.3 million from category two to category three, due to reductions in its operating plan, changes in its senior team and the overall liquidity position. On November 1, we were made aware of recent preliminary negative developments and Medly, which we believe may result in a future downgrade of their outstanding loans here in Q4.

Ramifications Of This Event

Two things are of utmost importance for a BDC, in my opinion. That would be the NAV per share and the NII per share to cover the dividend. So with this news, we have to see what the hit could be to each of these metrics. After all, that's what sent the shares tumbling lower, as it definitely will cause a hit.

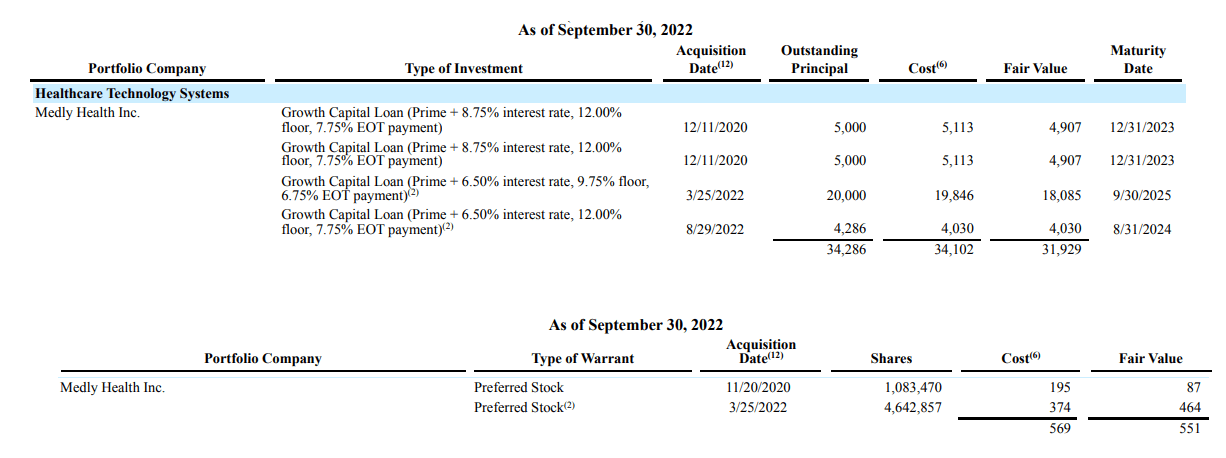

They have loans and warrants for the preferred holdings with this company.

TPVG Medly Health Exposure (TPVG Quarterly Report)

{kind=link}

As noted above, they have an outstanding principal of around $34.3 million in loans plus another $569K in costs. This worked out to a fair value of $551K for the preferred warrants and $31.929 million for the loans. They also held another $30K in fair value for preferred equity, but that position is pretty immaterial. That gives us an entire fair value at the end of their last quarter of $32.51 million.

The total shares of TPVG outstanding at the end of September 30th, 2022 came to 35.282 million. That means that we should anticipate around a $0.92 hit to NAV. At the end of last quarter, they reported a NAV per share of $12.69. We should anticipate that this will move down to $11.77. A ~7.2% to NAV hit is quite substantial. Of course, that would also require all else to stay the exact same, and we know that isn't the case. Portfolio valuations are always moving around.

That does make the last closing price of $11.79 right at that level. (Since the original publication, shares are now down to $11.13, presenting a move to a discount.) Before this news, the fund was trading right around parity with its NAV, so it's interesting that it isn't being "punished," really. Not in the same way that we saw for TRIN. That's why I suspect that it could drift a bit lower, or investors are essentially giving TPVG a pass on this news.

Now, we know the dividend coverage was strong, and this latest development will have a material hit but shouldn't completely derail the fund. When they announced the special, they knew this was also going on. Figuring out the exact hit to NII is a bit more of a guess due to interest rate fluctuations.

The Medly loans have a floor of 12% and 9.75% for the loan made in March. That loan made in March just so happens to be the largest. However, they also have the variable rate of prime + 8.75% on two of them and then 6.5% on the other two.

It looks like the prime rate today was 7% as of writing this. We would be looking at interest rates of 15.75% and 13.5%, which these loans should be paid at today. However, the prime wasn't at this level earlier this year, and as rates were rising, this was, of course, pushing up the prime rate.

YCharts

To be cautious and overestimate here, I'm just going to say that the entire exposure was paying at 12%. That overestimates because the larger loan floor was lower than 12%. Anyway, when we look at it that way, we can say that $34.3 million earned $4,116,000 for the BDC annually. That would work to around a $0.117 hit to NII the entire year. In the rolling 4 quarters, they earned $1.78 NII. That's against the annualized $1.48 payout per year.

Given that we are past the interest rate floor on most of their holdings, it can be offset by higher income elsewhere. Therefore, we could expect to see NII tick up higher in the next several quarters. So this hit doesn't seem to be too detrimental to the future survivability of the current dividend. It would be if we start seeing more non-accruals pick up elsewhere, that concern could come in.

Conclusion

TPVG is on my watchlist and is something I'm considering investing in. However, my previous buy target was around $14.50. Given the current environment and news, I think it should be dropped closer to $11.50. That puts it closer to what its NAV is expected to be once the Medly position is removed. To get an even better price with more cushion for further potential weakness, I think selling some puts at $10 could make sense. (Exactly what I have done since the original posting of this article.) This could be more tempting if we get some further sell-off related to this news or a general downturn in the broader markets.

The overall hit to TPVG is material but doesn't seem likely to derail the fund completely. At least in terms of the BDC's distribution coverage, it should still remain covered. I think this news is a good reminder to us that BDC risks are something to consider, especially as we move into more uncertain economic periods. Spreading out the exposure to several BDCs can mitigate some of these potential hits to add further diversification.

For further details see:

TriplePoint Venture Growth: A Potential Opportunity