TPVG - TriplePoint Venture Growth: High Yield Is Sustainable For Now

2023-12-07 12:10:56 ET

Summary

- TriplePoint Venture Growth is a BDC that provides financial assistance to companies in industries like e-commerce, entertainment, technology, and life sciences.

- The company has a robust financial position with a solid net asset value and total liquidity.

- The dividend yield is currently above 15% and has been well-covered, but there are concerns about the credit quality of TPVG's portfolio.

Overview

TriplePoint Venture Growth ( TPVG ) is a BDC (business development company) that focuses on supporting and investing in industries like e-commerce, entertainment, technology, and life sciences. They specialize in providing financial assistance to companies in the venture growth space, offering various types of financing such as growth capital loans, secured loans, equipment financing, revolving loans, and direct equity investments.

TPVG tailors its debt financing products to different needs, investing amounts ranging from $1 million to $50 million, depending on the type of financing. Their investments may include lines of credit, warrants, and secured loans. The company seeks returns in the range of 10% to 18% and does not actively seek board seats in the companies they invest in. The management fee is reasonable at 1.75%.

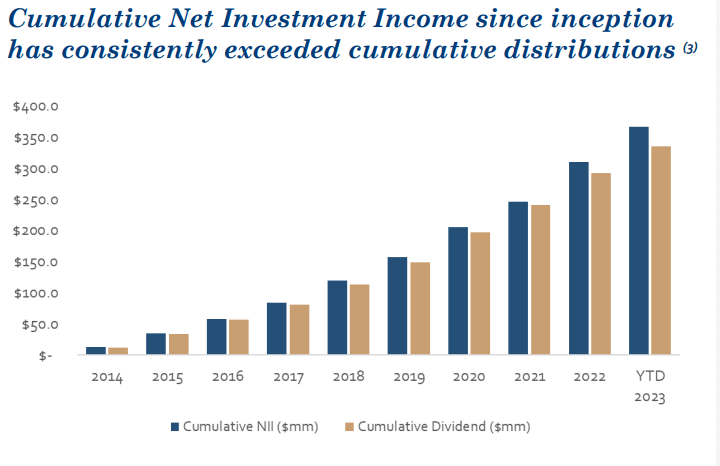

Although the dividend yield is currently above 15%, their distributions have been sustainable so far which is what originally caught my attention. Their accumulated net investment income since inception in 2014 has consistently surpassed cumulative distributions with a comfortable margin of safety. However, I don't think I will buy any additional shares of TPVG at this level as I plan to sit on the sidelines and see how the price reacts to future interest rate cuts.

Portfolio & Strategy

{kind=link}

TPVG Investor Presentation

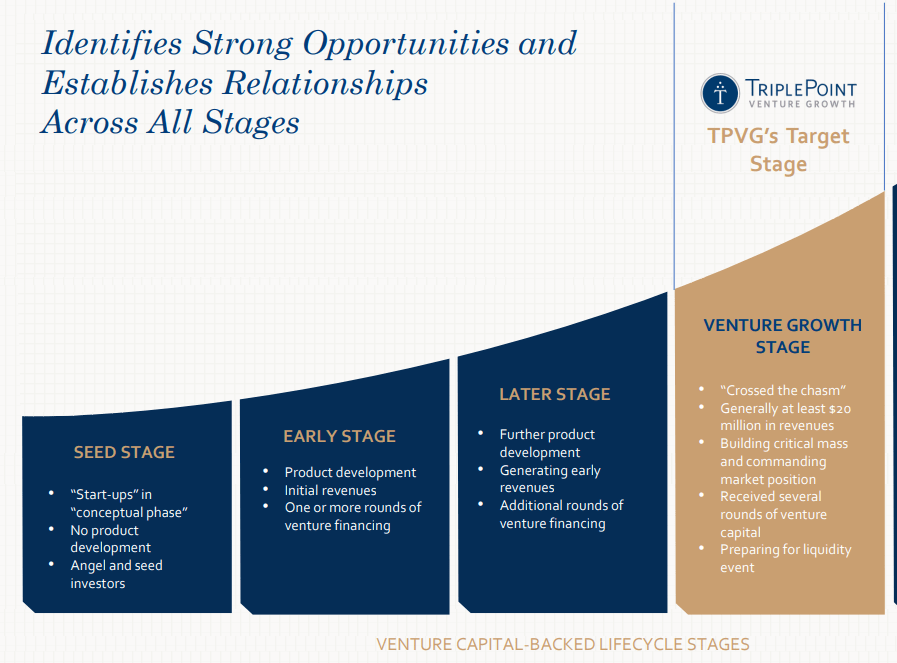

TPVG looks to invest in companies within the venture growth stage of their journey. I like that they operate in this area of the process because it serves as a baseline safety net. They only consider companies that have at least $20M in reoccurring revenue, have received several rounds of venture capital, and are prepared for a liquidity event.

This strategy has so far delivered solid results for shareholders, delivering over 100% in total returns over the last decade. Management is continuing their expansion story as they've recently signed term sheets totaling $58.1 million with venture growth stage companies at TriplePoint Capital LLC. The deal closed $5.6 million in new debt commitments to these entities.

Notably, the company funded $12.7 million in debt investments to five portfolio companies, achieving an impressive 14.2% weighted average annualized yield at origination. The receipt of $37.3 million in loan principal prepayments and the realization of a 15.1% weighted average annualized portfolio yield on total debt investments further contribute to the solid financial performance.

New debt commitments are advantageous for BDCs as they contribute to income generation through interest payments. By actively pursuing new debt opportunities, TPVG has signaled confidence in identifying growth prospects in my opinion. As of September 30, 2023, TPVG holds debt investments in 54 portfolio companies, warrants in 106, and equity investments in 48. With a solid net asset value of $374.1 million, or $10.37 per share, and total liquidity of $262.5 million along with unfunded commitments of $141.9 million, TPVG's financial position is robust.

It seems that management recognizes that the environment has changed and are managing accordingly. While they still try to find expansion opportunities, they also recognize that cash management is priority right now. This was reinforced in the latest earnings call :

For the deals getting done in today's market, the operational investment principles have changed. The emphasis is now on managing cash burn and demonstrating a projected path to profitability. As opposed to the guiding principle just 2 or 3 years ago, where venture investors sought growth at all costs. While we don't expect any finite changes, as I will get into, we continue to find pockets of opportunity for new growth stage investments reflecting this new market reality. And we expect to be able to increase our allocation of investments to TPVG in the quarters ahead. - James Labe - Co-Founder, Chairman & CEO

In Q3, TPVG downgraded the credit ratings of several e-commerce and consumer companies. Three companies moved from category 2 to category 3, and two companies dropped from category 3 to category 4. The combined total principal balance for the downgraded companies is $28.4 million. This adjustment reflects increased risk and potential challenges for these companies. Given the upcoming holiday season's significance for retail, e-commerce, and consumer companies, the performance of Q4 will be crucial and It's something I plan to revisit. However, due to the downgraded credit ratings, I maintain caution in adding here. While a strong Q4 could potentially improve their positions for 2024, the downgrades highlight a need for caution in my opinion.

Dividend

In the recent press release , the third-quarter Net Investment Income [NII] exceeded expectations at $0.54 while surpassing estimates by $0.04. This comfortably covers the most recent declared dividend of $0.40/share. Additionally, the total investment income reached $35.74 million, marking a 20.3% year-over-year increase. Based on their financial standing, the high distributions have been well-covered.

{kind=link}

TPVG Investor Presentation

The dividend growth story is a bit mixed but that's expected from a BDC that's already yielding over 15%. The dividend CAGR over the last 5-year period is only 1.74%. TPVG reported net investment income of $19.1 million, or $0.54 per share, and generated total investment income of $35.7 million during the quarter. With a record 20.0% return on average equity based on net investment income, the company underscores its financial strength.

Additionally, the successful capital raises by three debt portfolio companies, totaling $46.8 million in private financings, reflect the attractiveness of TPVG's investment portfolio. The company's prudent leverage management is evident in its 1.62x gross leverage ratio at the end of the quarter. Importantly, TPVG's declared fourth quarter distribution of $0.40 per share, payable on December 29, 2023, reinforces the sustainability of its dividend policy, bringing the total declared distributions to $14.65 per share since its initial public offering.

Valuation & Risk

{kind=link}

CEF Data

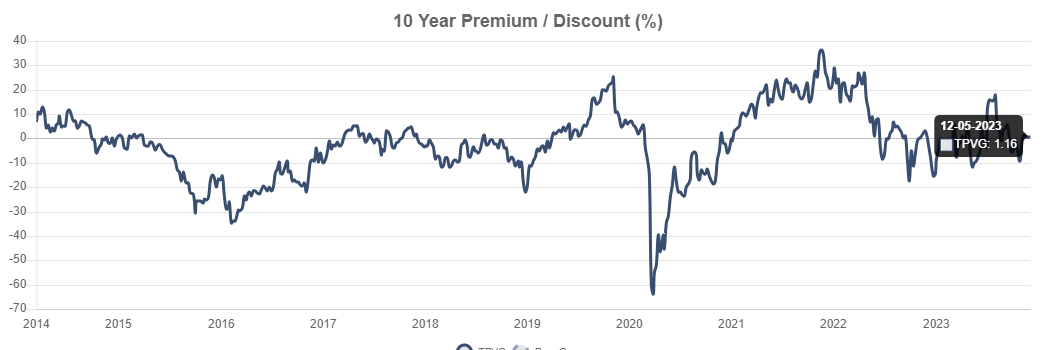

TPVG currently trades at a slight premium to NAV of 1.16%. When looking back at the 3-year average NAV premium/discount relationship, the stock has traded at an average premium closer to 8%. While this may indicate that TPVG currently trades at a slight discount to NAV, I believe this is for a reason.

As previously discussed, the credit quality of TPVG's portfolio has weakened a bit. Their most updated non-accrual ratio was 11.1%. A rising non-accrual ratio for BDCs is a cause for concern because it reflects the increasing percentage of loans in the BDC's portfolio that are not generating interest income. The concern arises from the heightened risk of loan defaults, as non-accrual loans are frequently precursors to such events.

Additionally, there's a potential threat to the sustainability of dividends, as BDCs often distribute a substantial portion of their income to shareholders. Even though the net interest income has historically covered distributions, who is to say that will always be the case? I stay observant as we head into the new year and a new rate environment. In addition, rate cuts may have an affect going into 2024. It will all depend on how aggressive the cuts are that will determine how significant of a headwind we see. The fed is expected to cut rates at least 4 times over the course of next year.

Takeaway

TriplePoint Venture Growth ((TPVG)) stands as a BDC with a strategic focus on supporting industries like e-commerce, entertainment, technology, and life sciences. Despite its recent credit rating downgrades for certain companies in its portfolio, TPVG maintains a solid financial footing, actively pursuing new debt commitments and demonstrating prudent leverage management.

The sustainability of its dividend policy is underscored by strong net investment income, successful capital raises, and a declared fourth-quarter distribution. However, caution is advised due to the non-accrual ratio's uptick and potential risks associated with a changing rate environment.

The upcoming holiday season's performance and the Federal Reserve's anticipated rate cuts in 2024 add elements of uncertainty that warrant careful observation as we approach the new year. Investors may find TPVG's current slight premium to NAV a reflection of these considerations, emphasizing the need for a discerning approach to valuation and risk management.

For further details see:

TriplePoint Venture Growth: High Yield Is Sustainable For Now