TPVG - TriplePoint Venture Growth: Why I'm Moving To The Sidelines

2023-12-07 08:05:00 ET

Summary

- TriplePoint Venture Growth is an externally-managed BDC that invests in debt financing for high-growth companies.

- It currently pays a 15% dividend yield that's well-covered by net investment income.

- TPVG's portfolio quality has declined, and its NAV/share performance lags behind its peers, making it a less attractive investment option at present.

Many investors will shy away from high yield, and this may be warranted for some companies, as an elevated yield is a sign of a company in distress. However, certain industries such as REITs, BDCs, and MLPs are designed for high yield due to tax advantages at the corporate level.

With these types of investments, a high yield speeds up the payback period, in which an investor potentially realizes the value of their principal faster than they would with low-yielding alternatives on the market.

This brings me to TriplePoint Venture Growth ( TPVG ), which I last covered here back in August with a 'Buy' rating, highlighting its high portfolio yield on investments. TPVG's stock price has slid by 9% since then, with the market pricing in more risk on the potential for a recession. While TPVG's 15% dividend yield is certainly attractive, in this article, I discuss why I'm getting more cautious around the name until the picture brightens, so let's get started.

Why TPVG?

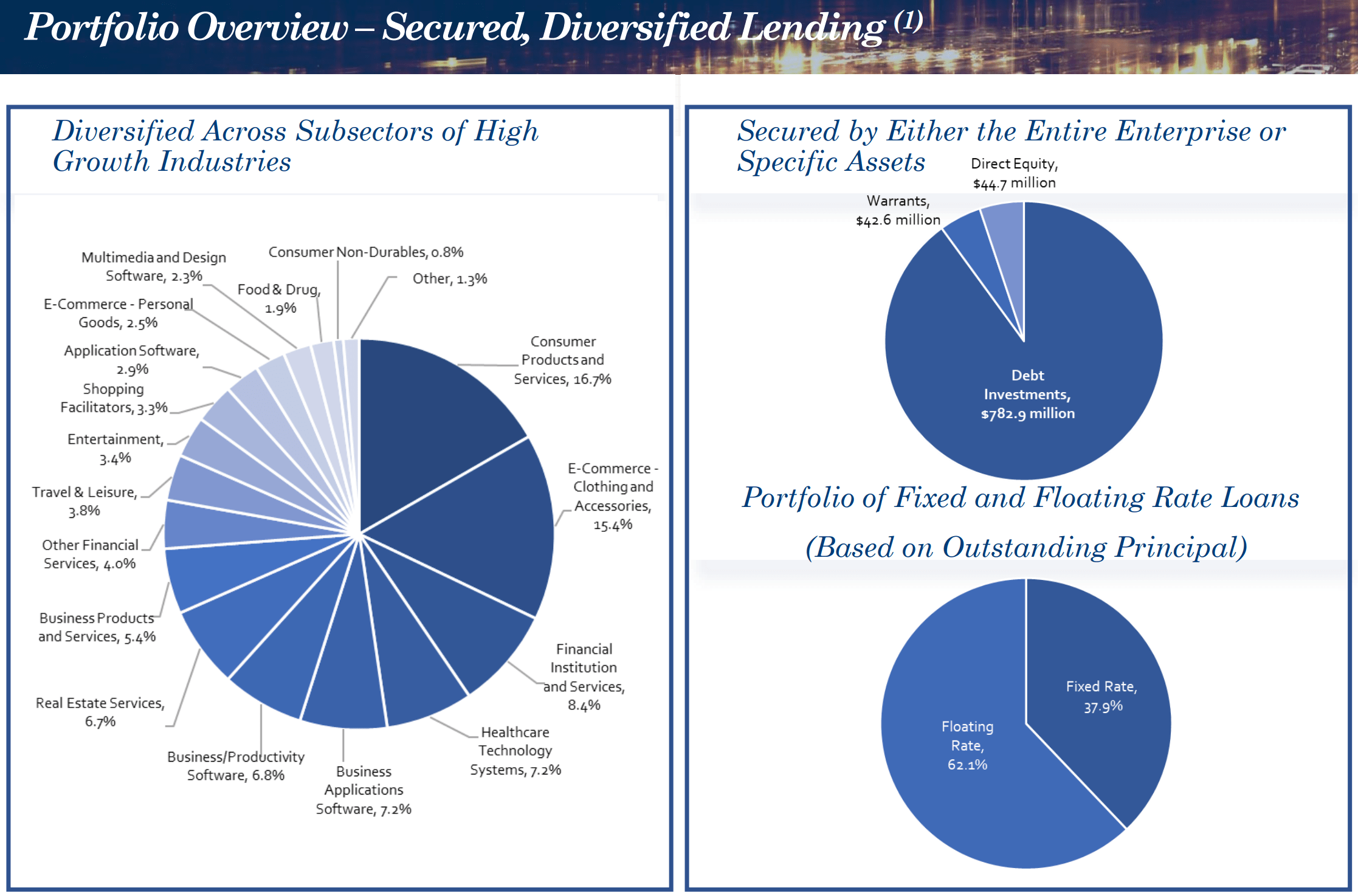

TriplePoint Venture Growth is an externally-managed BDC that invests in debt financing for venture capital-backed companies in high-growth sectors. At present, it has an investment portfolio with a fair value of $870 million consisting primarily (90%) of debt investments, followed by warrants and equity, which each comprise 5% of the portfolio.

Among TPVG's past investments include a number of companies that are either now public or have been acquired by public companies. This includes PillPack, which was bought by Amazon ( AMZN ), as well as cybersecurity firm CrowdStrike ( CRWD ), cloud infrastructure company, Nutanix ( NTNX ), and database management provider, MongoDB ( MDB ). As shown below, consumer products, e-commerce, financial institutions, healthcare technology, and business applications software comprise TPVG's top 5 segments, comprising 55% of portfolio value.

{kind=link}

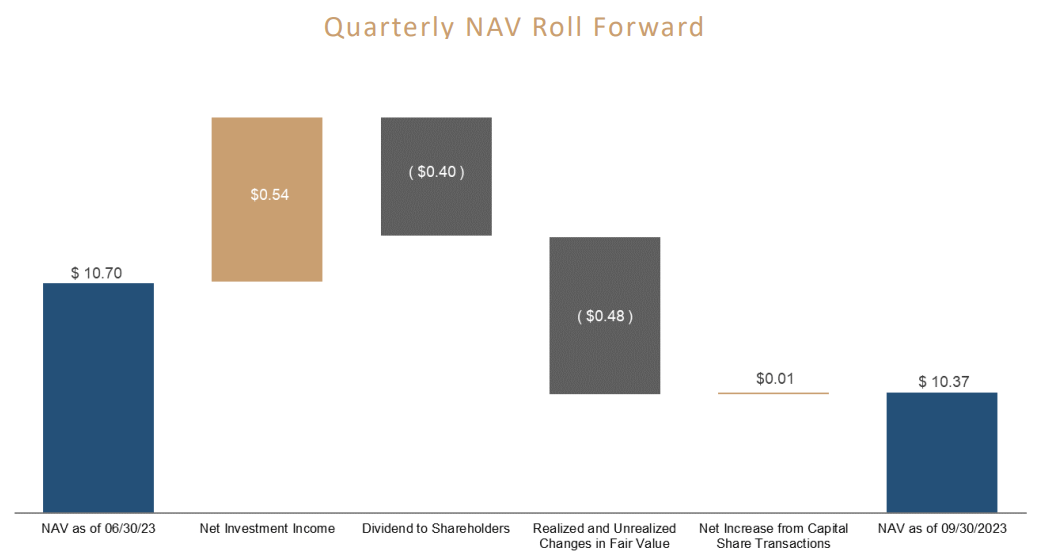

While TPVG's percentage of debt carried as floating rate (62%) sits lower than that of most other BDCs, it's still nonetheless benefitting from higher interest rates. This is reflected by TPVG's high weighted average yield on debt investments of 15.1% during the third quarter, sitting 210 basis points higher than where it was in the prior year period, before interest rates started to materially climb. This enabled TPVG to earn NII/share of $0.54, which comfortably covers the $0.40 quarterly dividend rate at a 74% payout ratio. It's also worth mentioning that NII per share during Q3 is $0.03 higher than it was in the prior year period.

Despite TPVG's decent performance from a portfolio yield and dividend coverage perspective, I see reasons to be concerned, as investments on non-accrual ticked up by 40 basis points on a sequential QoQ basis and by 4 full percentage points on a YoY basis to 5.0% during Q3. Overall portfolio quality has also taken a hit due to a number of credit downgrades on a scale from 1 to 5, with 1 being the highest quality.

{kind=link}

This contributed to a deterioration of TPVG's NAV per share on a sequential basis from $10.70 in Q2 to $10.37 in Q3. As shown below, both realized and unrealized declines in the investment fair value more than offset the retained capital of $0.14 from net investment income after paying the dividend.

{kind=link}

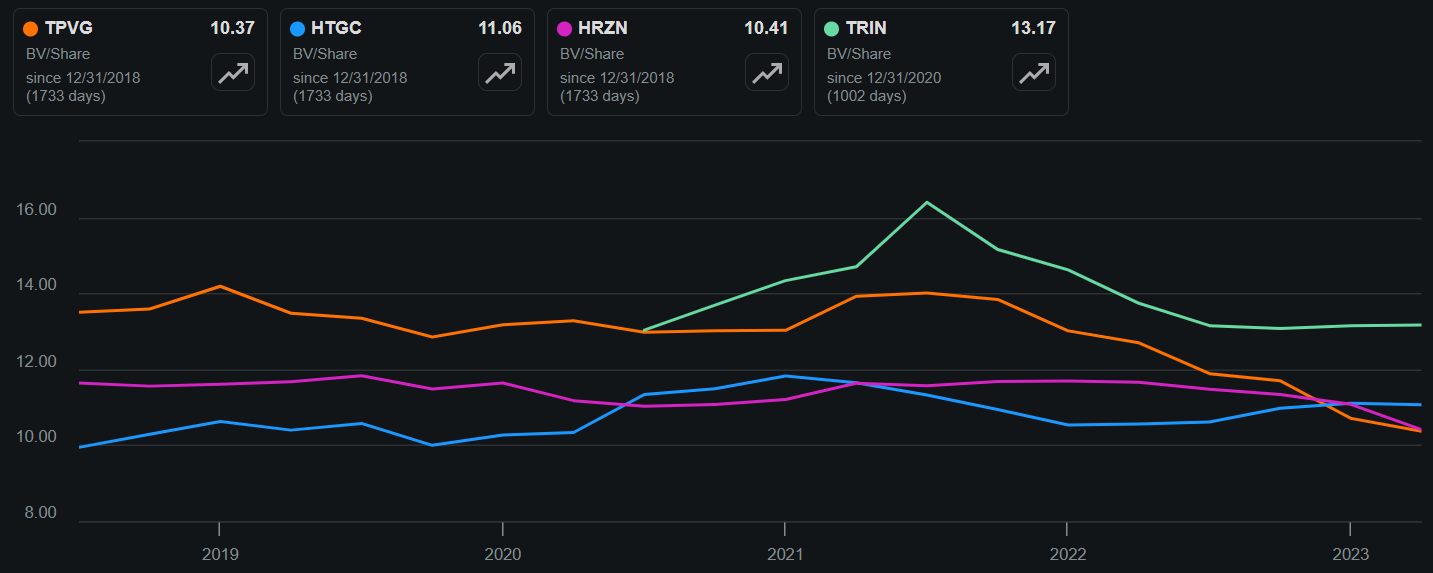

While one quarter's worth of performance doesn't make or break a BDC, it's worth comparing TPVG's NAV/share performance with that of its peers over an extended period of time. For the purposes of this exercise, I included the growth-focused BDCs, Hercules Capital ( HTGC ) and Trinity Capital ( TRIN ), both of which are internally-managed, as well as Horizon Technology Finance ( HRZN ), another externally-managed BDC.

As shown below, all 3 of TRIN's peers have seen better NAV/share performance over their comparable time periods (since Q2 2020 for TRIN) on a percentage basis, and HTGC actually increased its NAV/share over the past 5 years. At the same time, TRIN's NAV/share has declined from just under $14 in 2018 to $10.37 as of the last reported quarter.

{kind=link}

Importantly, the economic picture has changed since the last time I visited the stock in August. At that time, the economy was still firing on all cylinders, but now Wall Street, including JPMorgan Chase ( JPM ), anticipates the real possibility of a " hard landing " in the economy in 2024 rather than a previously anticipated soft landing.

In a hard landing scenario, TPVG may find itself handicapped in terms of its ability to opportunistically invest, as its shares currently trade at just a slight premium to NAV, and as it carries a debt-to-NAV ratio of 1.62x, sitting not too far from the statutory limit of 2.0x for BDCs. This also sits higher than the 0.8x to 1.3x "sweet spot" that I see for most BDCs.

Considering all the above, I would rather move to the sidelines on TPVG due to better BDC alternatives on the market today, including its aforementioned direct peers. At the current price of $10.50, TPVG trades at a slight premium to its NAV/share of $10.37, and I believe a discount is warranted considering higher non-accruals, the decline in portfolio quality, and elevated leverage heading into a potential recession.

Investor Takeaway

In conclusion, while TPVG has a high dividend yield that's well-covered by net investment income, recent performance and market conditions indicate caution for investors. There are better BDC alternatives available with stronger NAV/share performance and less credit risk. Until the economic outlook improves, it may be wise to wait on investing in TPVG. As such, I'm downgrading TPVG to a 'Hold' at present.

For further details see:

TriplePoint Venture Growth: Why I'm Moving To The Sidelines