TTBXF - Tritax Big Box REIT: Fairly Valued After The 40% Drop

Summary

- Tritax Big Box REIT is a UK-focused warehouse and distribution center REIT with an exceptionally robust balance sheet.

- The stock is trading at about 20 times the adjusted earnings.

- That's not cheap, but the REIT is working on a development pipeline of almost 1B GBP.

- The most recently calculated NTA/share is outdated. Increasing interest rates likely mean the NTA/share will fall by 30-50%.

Introduction

Tritax Big Box REIT ( OTCPK:TTBXF ) is a UK-based REIT focusing on warehouses and distribution centers . The REIT has always had a focus on running a very conservative balance sheet with a low LTV ratio, and its strong leasing profile with long-duration leases and inflation and market related rent hikes has made this a favorite of the markets.

{kind=link}

Now that interest rates are increasing, I’m afraid the REIT will have to recalculate its Net Asset Value (and Net Tangible Assets) using the new reality. While the REIT had an official NTA/share of in excess of 240 pence as of the end of June, the capitalization rate used to calculate the fair value is now too low as even the overnight lending rate is now higher than the capitalization rate used by Tritax.

Despite this, the conservative balance sheet means that even if the capitalization rate would have to increase by 50%, the LTV ratio will remain below 35% and there's no balance sheet issue. It does mean the 242 pence in NAV/share will have to be taken with a grain of salt and I think the current fair value is pretty close to the current share price of just under 250 pence.

{kind=link}

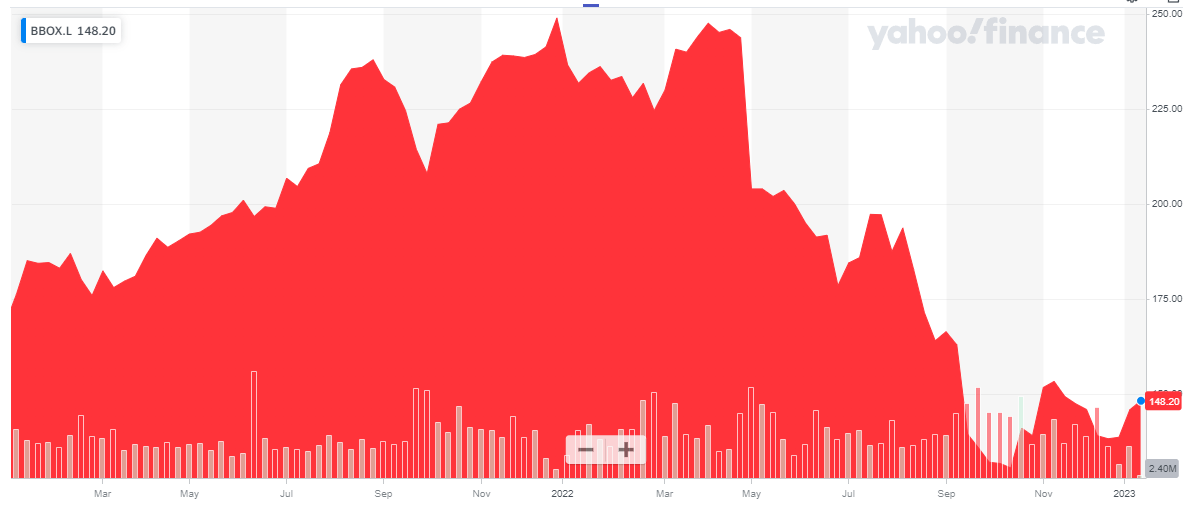

Tritax has almost 1.9 billion shares outstanding, resulting in a market cap of approximately 2.8B GBP. The REIT is part of the FTSE 250 index, and as the average daily volume in London is far superior to any of the secondary listings, I’d strongly recommend to use the London listing to trade in Tritax’ shares. The average daily volume is 7.2 million shares in London , the ticker symbol is BBOX. I will use the GBP as base currency throughout this article.

The earnings are okay, but the NAV/share should be taken with a grain of salt

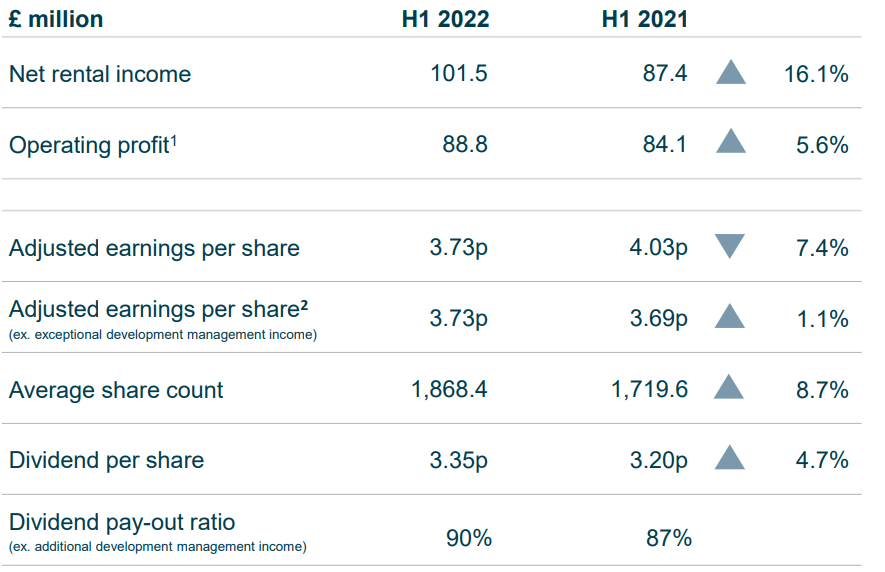

My main focus point in this article will be the valuation of the properties. The REIT performed pretty well in the first half of the year (unfortunately it does not provide detailed financial statements on a quarterly basis), and as you can see below, the adjusted earnings per share came in at 3.73 pence, an increase of 1% compared to the first half of last year, despite an increased amount of shares outstanding.

{kind=link}

The payout ratio is 90% and an interim dividend of 3.35 pence per share was paid out . Keep in mind the distributions from UK REITs are generally taxed at 20% unless it's not a property income distribution.

Tritax Big Box REIT proudly refers to its NAV per share and its recent growth evolution to show how well the REIT has done. While that's objectively a correct statement, let’s not forget a substantial portion of the NAV increase was fueled by gradually reducing the capitalization rates used to value the properties.

{kind=link}

While it’s perfectly understandable a low interest rate environment makes real estate more appealing and thereby compressing cap rates, the evolution of the capitalization rate used by Tritax is quite interesting. We ended 2014 using a capitalization rate (the EPRA Net Initial Yield) of in excess of 5.5% and ended the first semester with a capitalization rate of 3.36%. This means a very substantial portion of the value increase was caused by reducing the capitalization ratio by 40%.

Author Calculation based on Tritax Documentation

A decreasing capitalization rate is acceptable when your so-called risk-free interest rate also decreases. And during the same period, the five-year UK government bond (‘GILT’) and the SONIA (Sterling Overnight Index Average) remained pretty flat but started to increase in 2022.

Author Calculation & Chart

It's clear the capitalization rate of less than 3.5% is coming under severe pressure if even the overnight interest rates are exceeding 4%. And even if you would use a longer-term interest as your benchmark, the current five-year UK GILT is 3.44%. Which basically means the capitalization rate used by Tritax includes a negative risk premium of a few basis points.

The H1 2022 conference call discussed the borrowing cost of Tritax. Back in June, Tritax mentioned it sees a borrowing cost of 100 basis points over the three-month LIBOR (a synthetic interest rate which will continue to exist for another year) and that resulted in an approximate cost of debt of just under 2.9% (excluding hedges).

Paul May

Cool. Perfect. And on that -- sorry, on the floater the 2%. So your margin -- I mean, you're looking at LIBOR is going 1.9-ish I think, something around there, 3-month LIBOR. Is that sort of margins are basically 0 effectively in -- on bank debt?

Or should we be thinking sort of 100 basis points or so margin on top of the 1.9 plus a little bit on the fee side, all-in cost?

Frankie Whitehead

Sure. So the margins are in around the 100 basis point mark you mentioned. We're borrowing over 3 months on the flowing.

A lot has changed and the current three-month LIBOR stands at 3.93%. Applying a similar 100 basis points margin would indicate the current cost of debt (excluding hedges) would jump to almost 5%. Which would be 50% higher than the capitalization rate used to determine the value of the properties.

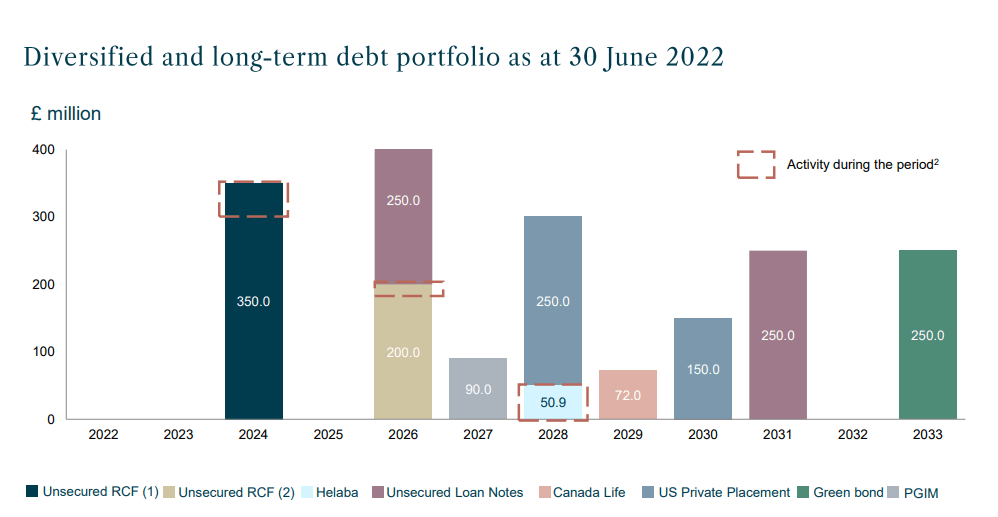

There are a few elements here that work in Tritax’ favor as well. First of all, the LTV ratio is very low which means the absolute increase in interest expenses on an annual basis will remain limited. In fact, it's not unlikely future rent hikes in 2023 and 2024 may already compensate for a higher cost of debt and considering only 350M GBP in debt will have to be refinanced between now and the end of 2025, I'm not expecting a disastrous impact on the EPRA earnings.

{kind=link}

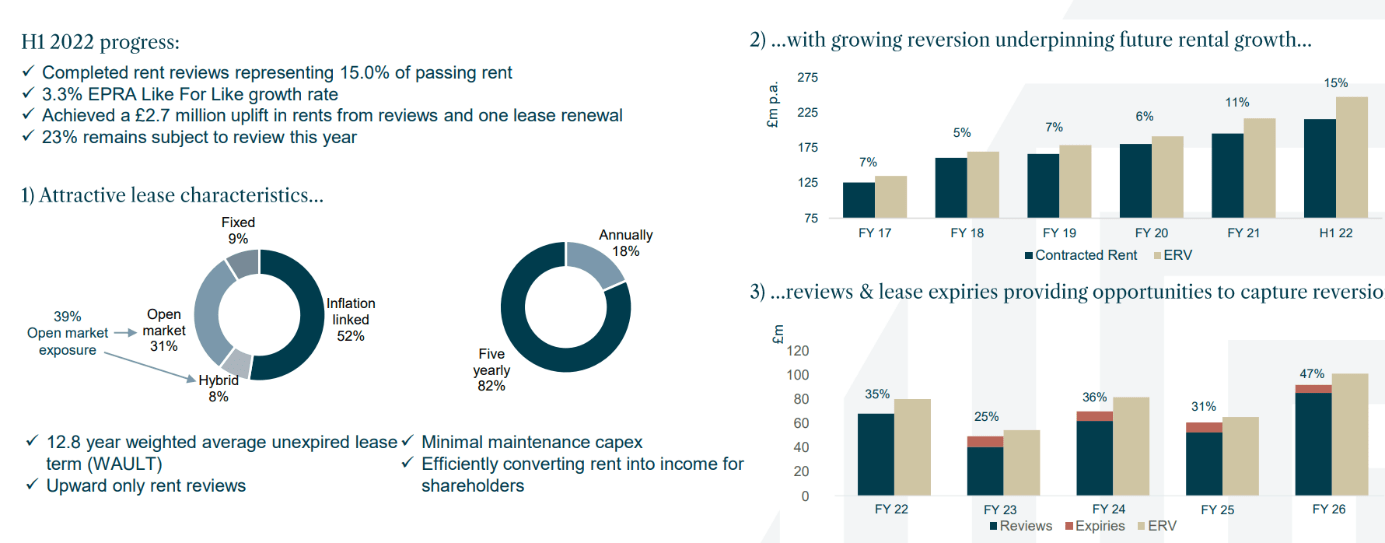

Between now and 2026, a substantial portion of the assets are up for rent reviews. The system applied by Tritax is different from other REITs in the world as about 52% of the leases are inflation linked while 39% is market-based. About 18% of the leases are up for annual rent hikes, while the vast majority is up for review on a five year basis.

{kind=link}

This means I have no beef with the EPRA earnings and anticipated earnings. If anything, I think the earnings may actually increase faster than the net interest expenses.

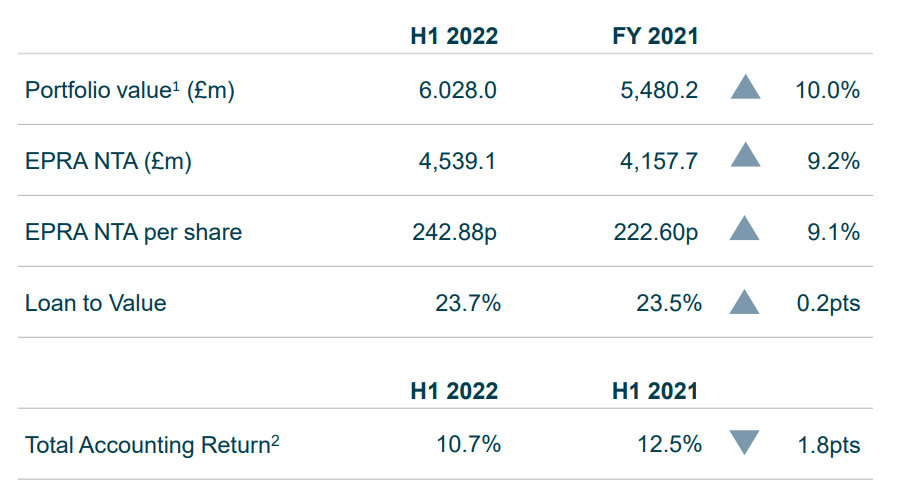

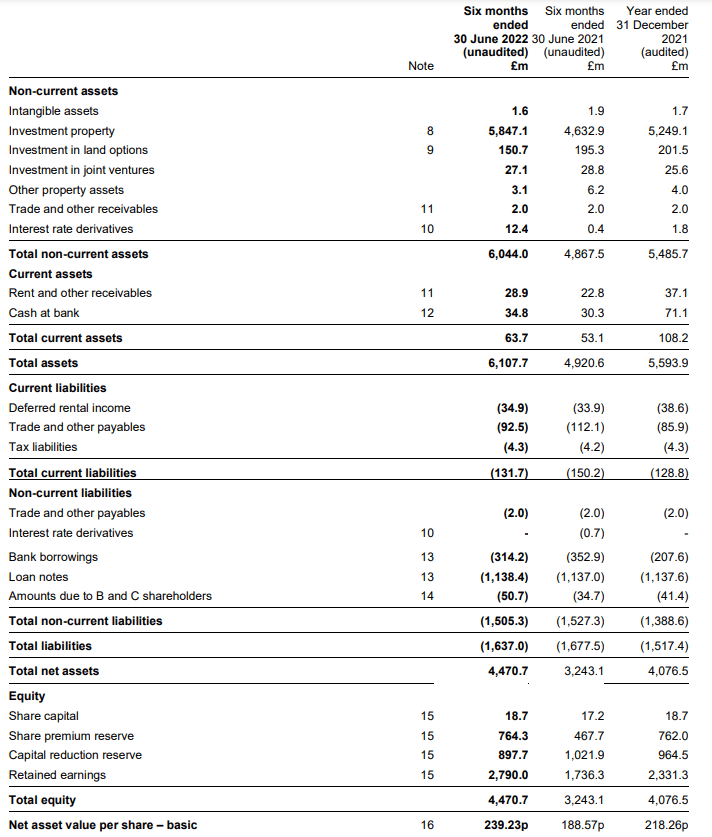

The main issue I have with Tritax is its use of a 3.36% capitalization rate to derive a Net Tangible Asset of almost 243 pence per share. We know the book value of the assets if 5.85B GBP as you can see below.

{kind=link}

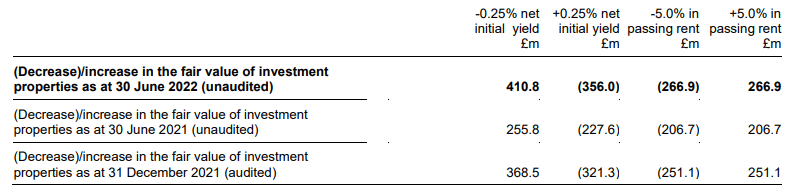

Tritax also provided a sensitivity analysis in its financial statements. For every 0.25% increase in the net initial yield, the book value will drop by 356M GBP.

{kind=link}

So if we would apply a required capitalization rate of 4.36%, about 1.42B GBP in book value would evaporate. Should Tritax be able to increase its passing rent by 10% in the next few years, the net impact on the book value would be roughly 900M GBP. Divided over 1.87B shares, that would be a hit of 48 pence per share. And I don’t think applying a 4.36% capitalization rate is outrageously conservative here. Hiking it further to 5% would result in an additional loss of 46 pence per share. Still assuming the passing rent increases by 10%, the Net Tangible Assets per share would drop to 194 pence and 148 pence per share respectively.

And although the book value per share would drop, the current LTV ratio is low enough to make sure Tritax stays out of trouble. Even after applying a 5% capitalization rate, the LTV ratio should remain below 35% so I do not expect any balance sheet issues.

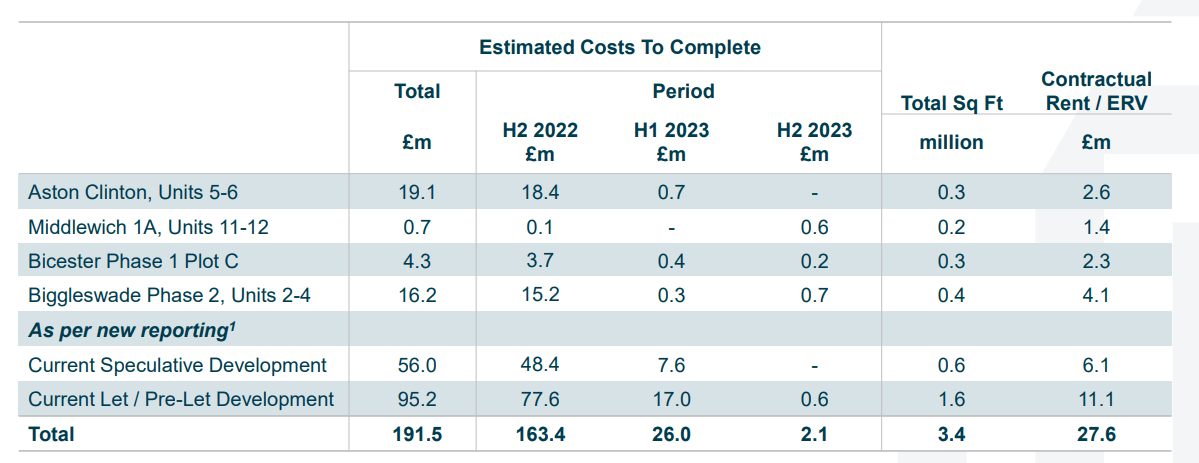

There are also things to look forward to. The near-term development pipeline will start to throw off cash flow as well while I think the REIT’s strategic land bank could be valuable.

{kind=link}

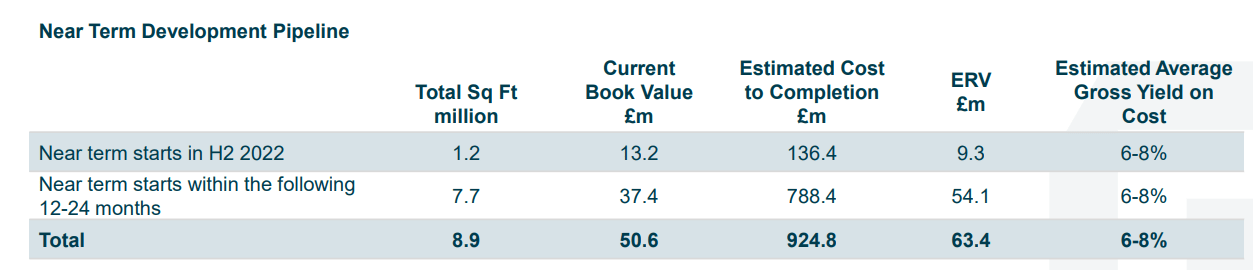

Meanwhile, the 788M GBP near-term development pipeline will also boost the rental income. Considering the implied average gross yield on cost is 6-8%, re-rating these new developments at a 5% capitalization rate should provide a welcome boost to the book value as this could create almost 300M GBP or just over 15 pence per share upon completion.

{kind=link}

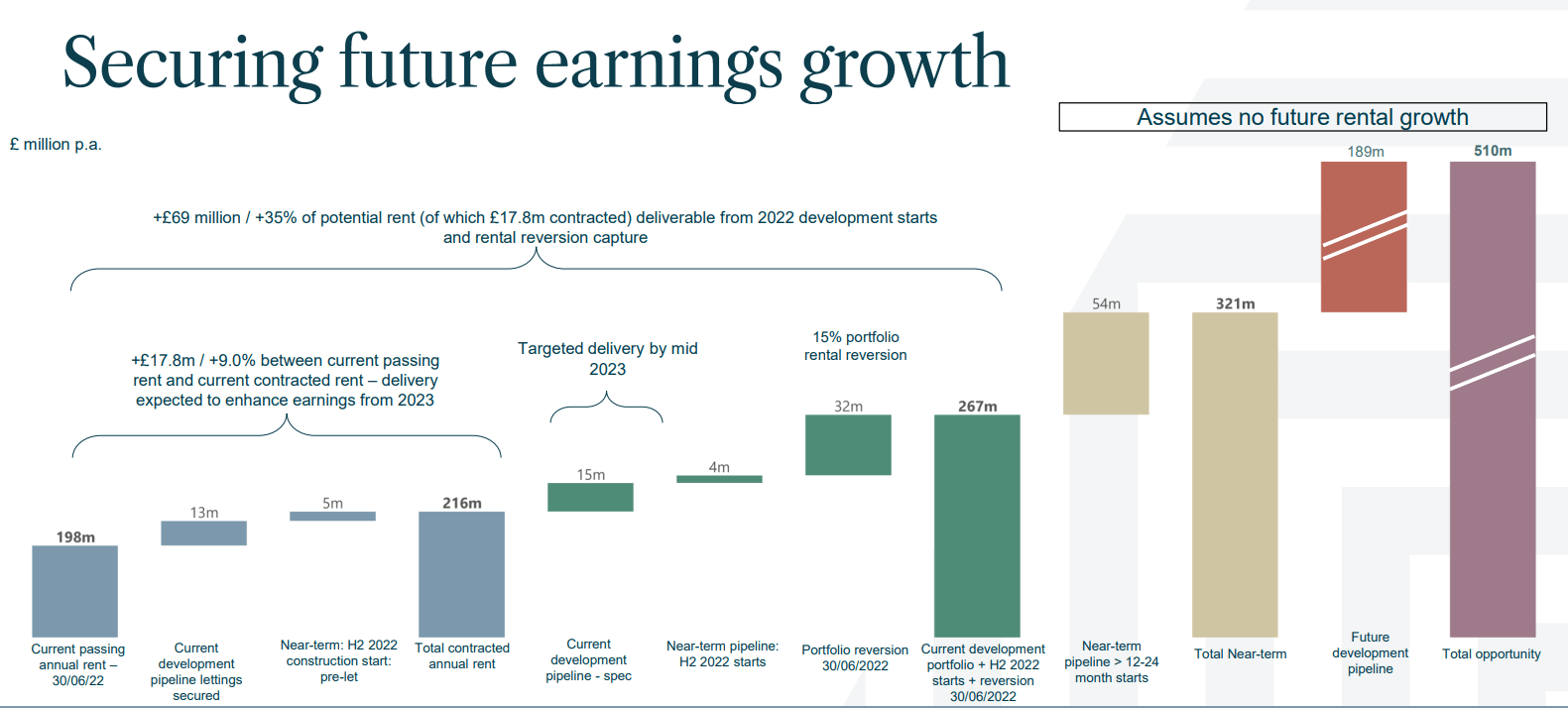

This near-term pipeline should provide a platform to Tritax to grow its annual rental income to just over 320M GBP

{kind=link}

This now allows us to calculate the potential adjusted earnings increase. We know the pipeline consists of 925M GBP and I will assume no new shares will be issued, and I will assume an average of 3.5 years to complete these investments. Applying a 90% payout ratio on the earnings, I expect Tritax to retain about 55M GBP in earnings, which means it would have to borrow 880M GBP to complete the development pipeline (I’m cutting a few corners here, but I want to show that even borrowing almost the entire amount would still increase the adjusted earnings per share).

Let’s assume the cost of debt will be 5% (long-term debt is slightly more expensive than the floating rate debt at this point, see later). This means the interest expenses will increase by 44M GBP per year, but as Tritax expects to generate 63M GBP in rental revenue, even borrowing almost 100% of the required investment would result in an increase in the adjusted earnings of 19M GBP. Other expenses will likely also increase (management fees etc), so let’s say borrowing 880M GBP to fund the 935M GBP development would increase the annualized earnings from 7.5 pence per share to almost 8.5 pence per share. And that excludes rent hikes on the existing portfolio which will also hit the top (and bottom) line and should result in a lower external financing need than the 880M GBP I used. Based on the development pipeline and despite a higher interest rate, I do see a clear path forward to adjusted earnings of 9-10 pence per share from FY 2025 on.

{kind=link}

I also would argue the bonds could be an interesting option for income-oriented investors that aren’t necessarily looking for capital gains. The 2.625% December 2026 bonds are trading at just over 90 pence on the Pound for a YTM of 5.5%. The 2031 and 2033 bonds have YTMs of respectively 5.4% and 5.5% respectively.

Investment thesis

I’m between a rock and a hard place when it comes to Tritax Big Box REIT. The official book value is outdated and using more conservative capitalization rates the book value of the assets and the NTA/NAV per share will drop by double digit percentages. The market appears to be very well aware of that, and the current share price of 148 pence already implies a capitalization rate of close to 5% as I don’t think anyone expects the 3.36% used in H1 2022 to be credible in the current interest rate environment.

I do like the REIT’s robust balance sheet and even a revaluation of the assets should not put the balance sheet in any danger.

In a case like this, the 5.4-5.5% yielding bonds would be the no brainer, but as the minimum order size is 100,000 GBP I’m also not too keen on investing that much in a starter position. As such, I am on the side lines and will keep an eye on how Tritax Big Box REIT advances its pipeline, and how it will deal with the revaluation of its properties.

For further details see:

Tritax Big Box REIT: Fairly Valued After The 40% Drop