TTBXF - Tritax Big Box REIT: The Worst Is Behind Us

2023-04-04 14:11:13 ET

Summary

- Tritax Big Box REIT is a warehouse and distribution center REIT in the UK.

- Three months ago, I warned for a massive drop in the REIT's book value per share as the capitalization rates used by Tritax were no longer justified.

- Most of the bad news should be in the share price. New and upcoming rent increases should be helpful to mitigate the impact of higher interest rates.

- Income-focused investors may also look at the bonds. The 2026 and 2033 bonds both have a yield to maturity of approximately 5.5%.

- The REIT is paying 7 pence per share on its FY2022 results. 6.775 pence is PID (and subject to the 20% dividend tax rate), 0.225 pence is ordinary income.

Introduction

In January, I discussed Tritax Big Box REIT ( OTCPK:TTBXF ), a UK-based REIT focusing on warehouses and distribution centers with a wide variety of tenants. I did like the low LTV ratio on the balance sheet, which means there likely won’t be any pressure on the capital structure even if (or better, "when") interest rates increase further. That being said, I was expecting the REIT to report a substantial decrease in its NAV/share due to sharply increasing capitalization rates.

{kind=link}

Yahoo Finance

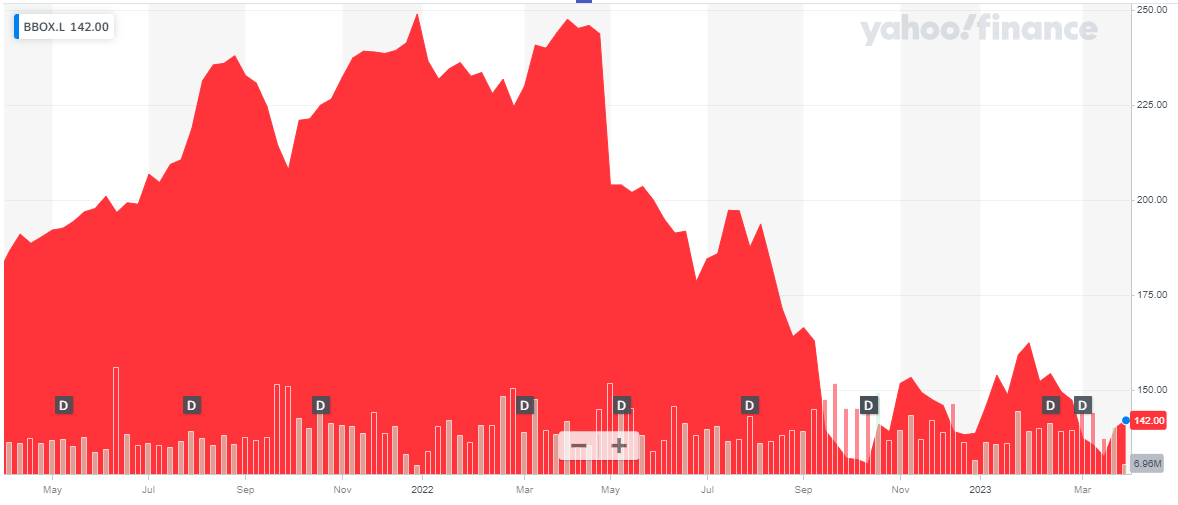

Tritax has approximately 1.87B shares outstanding, resulting in a market cap of approximately 2.65B GBP based on the current share price in the low-140 pence range. The REIT is part of the FTSE 250 index, and as the average daily volume in London is far superior to any of the secondary listings, I’d strongly recommend to use the London listing to trade in Tritax’ shares. The average daily volume is 6.6M shares in London, the ticker symbol is BBOX . I will use the GBP as base currency throughout this article as that’s the currency Tritax trades in and reports its financial results in.

The full-year results are in and don't contain any surprises

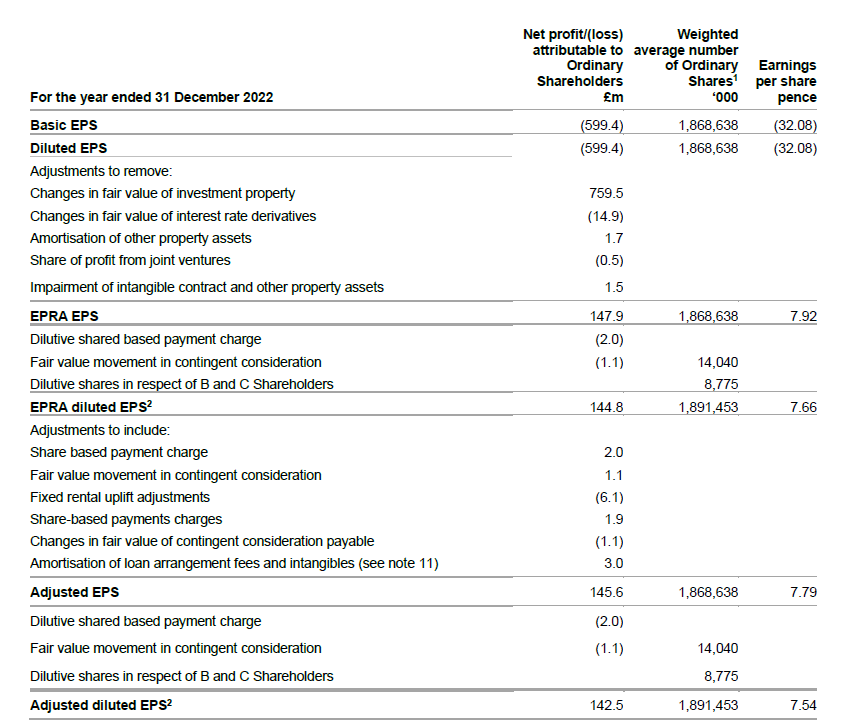

As explained in the January article, Tritax has seen its adjusted earnings per share decrease due to a higher share count after a recent share issue. In the first half of the year, the adjusted earnings per share came in at 3.73 pence while the company posted a full-year result of 7.79 pence per share including the development management income. Looking at the recurring earnings, the 7.51 pence per share indicates the underlying adjusted earnings in the second semester came in at approximately 3.78 pence, an increase of just over 1% versus the H1 result.

{kind=link}

Tritax Big Box REIT Investor Relations

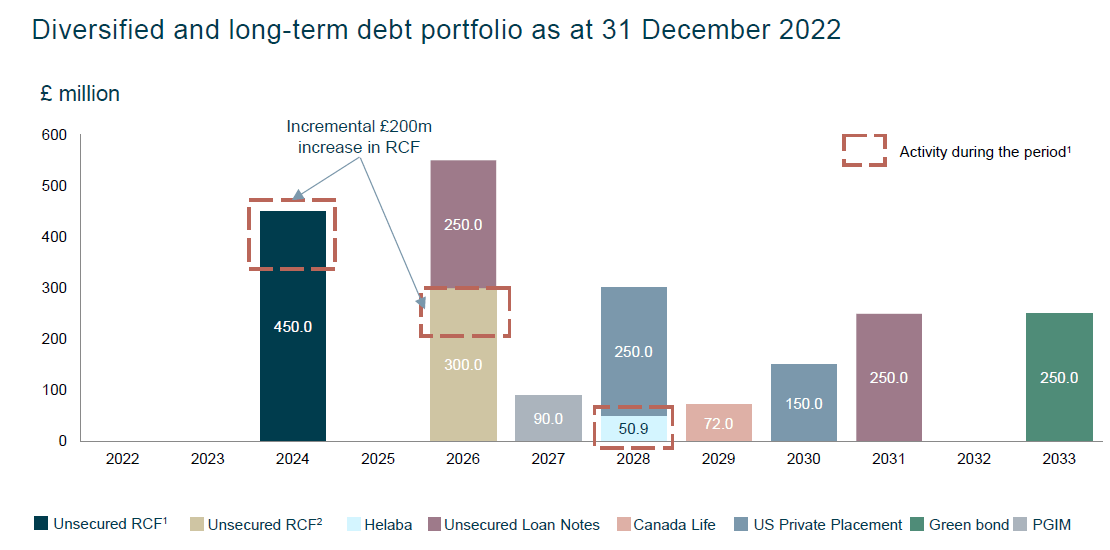

That sounds great, but keep in mind Tritax still has to deal with increasing interest rates. As of the end of last year, the average cost of debt was just 2.6% and fortunately 99% of the debt either has a fixed interest rate or is hedged and that will be a big help in keeping the current situation under control.

This will likely change later this decade as existing debt will start to roll off. Some of the bank debt will have to be refinanced as the bank debt is mainly related to credit facilities and the first real litmus test will be the repayment of a 250M GBP bond maturing in 2026 .

{kind=link}

Tritax Big Box REIT Investor Relations

As you can see above, Tritax will have to refinance a 250M GBP bond which currently has a 2.625% coupon. Assuming the cost of debt will increase to 4.5% (the cost of debt to issue new debt right now would be higher but I would expect the debt markets to normalize between now and 2026 and I expect the cost of debt for low-LTV REITs to come down), the REIT will have to pay an additional 4.75 million per year in interest expenses. That’s a quarter of a pence and represents about 3% of the current earnings profile.

{kind=link}

Tritax Big Box REIT Investor Relations

Fortunately there's one thing working in Tritax’s favor: Time. Thanks to the fact its debt maturities are very well spread out in time and considering it only has to refinance credit facilities between now and 2026, I like the odds of seeing Tritax being able to hike its rental income first before being really hit by the higher interest rates.

But let’s also not kid ourselves. Based on the gross debt level of just over 1.6B GBP, a 200 basis point increase in the average cost of debt will result in an additional 32M GBP in interest expenses. Divided over the almost 1.9B shares outstanding, the total impact would be about 1.7 pence per share per year. This excludes the impact from rent hikes and Tritax will likely be able to mitigate the impact from increasing interest rates along the way by increasing its rental income.

I remain confident in Tritax’s ability to increase the rent. As mentioned on the conference call :

[…]the rent secured within our development pipeline means that our contracted position rests 9% above today's passing rent, whilst the ERV of the portfolio sits a further 19% ahead of today's contracted rental position, providing us with good visibility over the future growth in our income, and I'll come back to this later

Throw in the interesting development pipeline and I expect Tritax to be able to cover the increasing interest expenses further down the road.

I was right in my January update

Back in January I argued the 3.36% capitalization rate used by the REIT wasn’t a valid multiple anymore considering the cost of debt already was exceeding the capitalization rate at that point. The existing bonds had a yield to maturity of north of 5% in January which definitely indicated the capitalization rates were way too optimistic as they were still based on the zero interest rate policy.

Upon running the numbers, I argued a 4.36% capitalization rate would reduce the NAV by about 1.42B GBP and even if it would be able to hike the rent by 10% in the next 2-3 years, the book value of the assets would still drop by approximately 900M GBP. A further increase to a 5% capitalization rate would result in a NAV/share of 148 pence excluding any rent hikes and about 190 pence including a cumulative 10% increase in the rental income.

{kind=link}

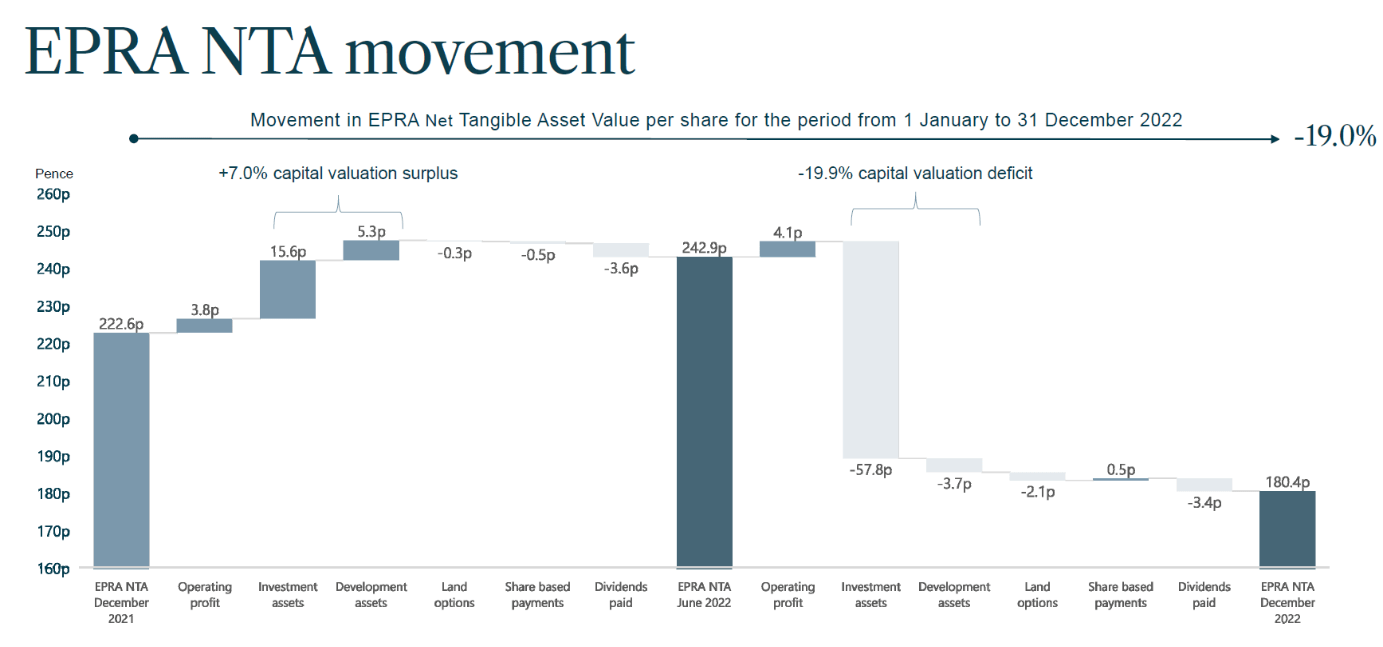

Tritax Big Box REIT Investor Relations

I was right. As you can see above, the REIT had to use higher capitalization rates to calculate the fair value of its real estate assets and the Net Tangible Asset result fell from almost 243 pence per share to just 180.4 pence per share. A dramatic 25% decrease in just one semester as the 4.1 pence in operating profit was almost entirely used to cover the interim dividend (3.4 pence per share) while there was a 61.5 pence per share hit due to the revaluation of the assets. The existing portfolio accounted for the bulk of this decrease while the fair value of the development projects also had to be written down.

Unfortunately I don’t think the pain is over. As of the end of 2022, Tritax Big Box REIT used a net initial yield of 4.19% and a topped-up Net Initial Yield of 4.39%. Considering the Tritax bonds on the secondary market are yielding 5.5% for the December 2026 bond (the 2033 bond has a similar yield to maturity), I still think the 4.39% used by Tritax is sufficient.

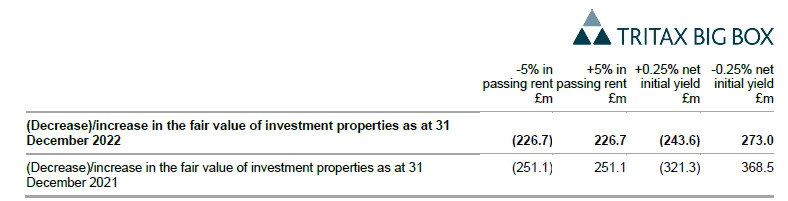

Fortunately the REIT once again provided a sensitivity analysis. As you can see below, a 25% increase in the net initial yield will reduce the fair value by 246M GBP. Which means an increase of the capitalization rate to 5.2% (which I really don’t think is too conservative given the current circumstances on the world markets) would thus reduce the fair value by almost 750M GBP.

{kind=link}

Tritax Big Box REIT Investor Relations

However, I also expect Tritax to be able to hike its rent in the next few years. Perhaps not to the same extent as originally anticipated as there are pricing pressures everywhere, but a 5% increase in passing rent would increase the value of the portfolio by 227M GBP. So if I would use a combination of a 75 basis point increase in the capitalization rate in combination with a 5% increase in the rental income, the net impact would be just over 500M GBP or 27 pence per share resulting in an adjusted NTA of just over 150 pence.

Investment thesis

I think Tritax will have to reduce the fair value of its assets even more, but I do think the worst is now behind us. The revaluation hardly came as a surprise as the market has been discounting Tritax’s book value for quite a while now as the stock has been trading at a double digit discount for about a year now.

That being said, I do think the current share price is much more reasonable and offers a better risk/reward ratio based on its discount to the Net Tangible Assets and the pro forma discount vs. the adjusted NTA if I would use a higher capitalization rate. Despite this, I’m still on the sidelines for now as I would like to see how the REIT’s earnings will develop from here. I’m not too keen on paying 20 times the EPRA earnings but I also realize Tritax will be able to increase its rental income and it’s not unlikely the increasing rental income will compensate the higher interest expenses.

Tritax’s main feature is the low LTV ratio, which stood at 31.2% as of the end of last year, based on the official Net Tangible Assets calculation. This was further reduced to less than 30% subsequent to the end of the financial year as the REIT sold four assets at valuations "in line with the year-end 2022 value." Add the average unexpired lease term of in excess of 12.5 years (with 35% of the portfolio having lease terms exceeding 15 years) and the current valuation of Tritax Big Box makes sense.

I currently have no position in Tritax Big Box but the stock is getting increasingly interesting at the current levels.

For further details see:

Tritax Big Box REIT: The Worst Is Behind Us