HYMPF - Tritium DCFC Is Very Interesting But Reflexivity Is Alarming

Summary

- Tritium DCFC Limited is very interesting, and we believe their claims that their technology is desirable among marquee customers hold water.

- Also, their economics could stand to improve a lot as maintenance economics improve with greater network density.

- Furthermore, Australia is fallow land for more infrastructure investment, and the government support for EV is undeniable.

- However, the low Tritium share price is a major problem for current shareholders, as dilution is going to be extreme if they have to do an equity raise.

- With cash balances likely to be burned in a year's time, major revaluation would be necessary to limit dilution and reverse reflexivity effects. Tritium DCFC Limited is a bad bet.

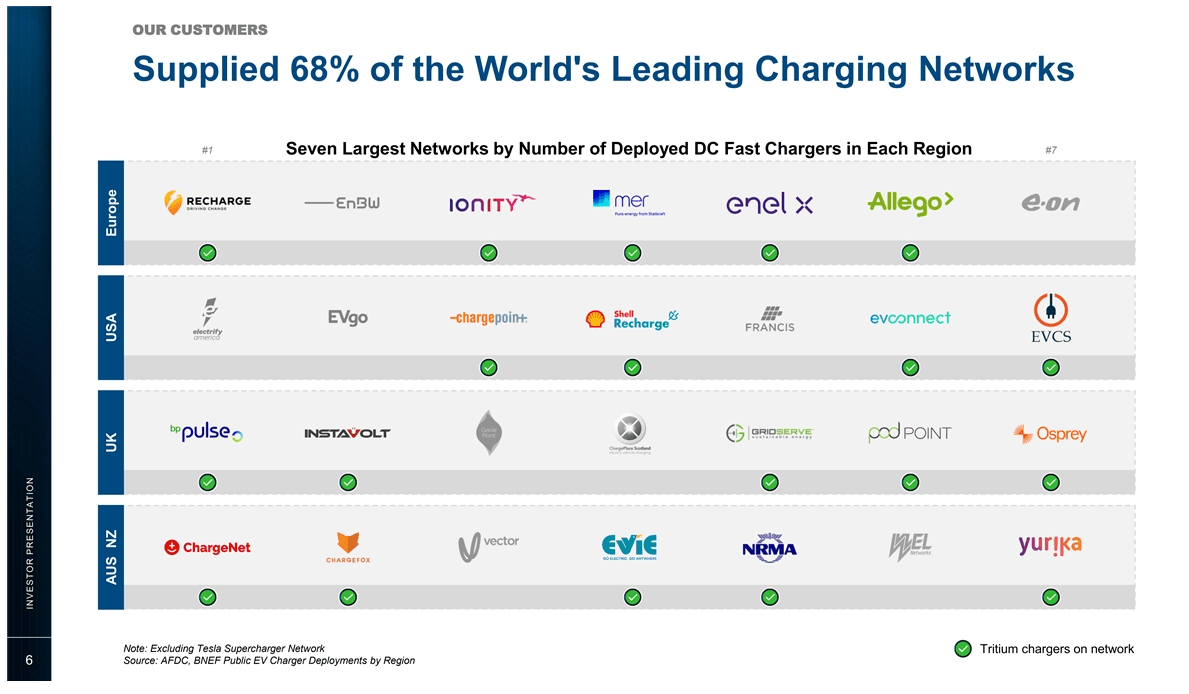

Tritium DCFC Limited ( DCFC ) makes charging units for electric vehicles ("EVs") that charge very fast. Its charging units have been used in networks such as Ionity . That network was created as a JV between Hyundai ( HYMLF ), Mercedes ( MBGAF ), BMW ( BMWYY ), Ford Motor Company ( F ), and Volkswagen ( VWAGY ). Other major networks use DCFC's chargers, too, like Enel's ( ENLAY ) Enel X and those in the U.S. like DC-America.

{kind=link}

There is fallow ground in Australia to expand, and the commitments to reducing emissions from transportation will continue to support DCFC's top line, with orders coming in at massive rates . This is doubling backlogs and rocketing the stock, too, by 30% two days ago. We also believe that the gross margins can improve substantially on the service and maintenance line. However, they have to burn cash, and at this rate, they are going to have to raise equity at very low valuations. Without a revaluation of the stock price, current investors are going to be heavily diluted, perhaps close to 50%. Reflexivity is a huge danger for DCFC, and in markets that are stubbornly low, this bet is much riskier than just the prospects of the energy transition.

What does DCFC Do?

DCFC makes and sells sophisticated EV chargers based on DC technology. Long story short, AC regular charging isn't going to cut it for the EV market since charging takes too long, and rapid charging is essential for the economics of charging stations to make sense and to be able to sustain a population of EV users, which is the plan of most governments. They sell chargers of different power levels that can be used for different tiers of EV charging infrastructure, and the higher the power, the more sophisticated the charger needs to be, with things like internal cooling systems, etc. to make them safe and functional. They are a leader in this field, with 10% in Europe and 20% in the U.S. These two geographies are where almost 90% of their sales and backlog come from.

The emerging segment with the company is going to be maintenance and hardware revenues, and this is going to be a nice recurring revenue stream that comes from the fact that a DC charger can be expected to last around 8-10 years.

The Investment Argument

Pros

- With DC chargers being relatively long-lived, we can expect positive margin contribution as the maintenance and service revenue line starts to scale. Invariably, service revenues are higher margin than the sales of the assets themselves. If EVs are truly the future, density of the coverage of charging networks will also contribute to scale economies through route economics of the service and maintenance business.

- The backing of EVs is undeniably by governments, with EVs representing a way to tackle the 20% of carbon emissions coming from ground transport. Scale in the sale of the chargers as large sums of money, billions in the U.S. and in the EU each, are being earmarked for charging infrastructure should do a lot to create stronger industrial economics in the sale of the chargers.

- Australia is still a very nascent but fallow market for infrastructure as the Albanese government commits to double the rate of carbon emission reduction than the previous Morrison administration. This is home territory for DCFC.

- EV technology needs to compete a little with hydrogen for viability as a green energy solution. EV is way ahead of hydrogen in actual penetration.

Cons

- The business argument against EVs is that markets may think every type of transport can be electrified. Trucks probably won't be a success and neither will aviation. Don't count on these markets.

- There is a sustainability debate around batteries, and there are also sourcing and resource issues in the West. With geopolitics becoming increasingly important and the amount of resources for batteries existing in unreliable nations like the DRC and China being quite substantial. EV batteries also don't last very long, there will need to be recycling infrastructure on top of everything else that has been subsidized to keep EVs as a relatively sustainable option. Lots of challenges ahead.

- Specific to DCFC, they have around $70 million in cash balances and burned almost $90 million in 2022. They are likely to have to raise equity to keep liquidity reserve requirements as per their debt facility agreements, and their current market cap is $244 million, which means that as they are still in relatively early stages of scaling, they may need to raise a lot of equity, perhaps enough to dilute current shareholders close to 50% if they need another $100 million. Debt raising doesn't look likely given the current DCM environment and DCFC's cash flow profile, which is very much cash-burning and loss-producing. They are also scaling their facilities in the U.S. , which will cost investing cash flows.

Bottom Line: A Definite Pass

The problem is that Tritium DCFC Limited is going to need to talk to capital markets for more financing, and with already a good degree of leverage, these discussions are going to be around equity raisings. Dilution is going to be substantial unless the stock's price rises and the company can get more bang for their buck with a new wave of investors. This becomes a binary play around whether the stock can revalue in time, but there's no option value from having the time limit either, so it's a disadvantaged bet.

There are so many companies on markets these days that can benefit from the EV revolution, such as Matthews International Corporation ( MATW ), which lies at one of the top positions in our exclusive Value Lab portfolio . Why take the risk here when other options dominate Tritium DCFC Limited in terms of risk-reward. Pass.

For further details see:

Tritium DCFC Is Very Interesting, But Reflexivity Is Alarming