TRTN - Triton International And Brookfield Infrastructure Tie The Knot

2023-04-13 08:14:56 ET

Summary

- Triton International agreed to sell itself to Brookfield Infrastructure in a massive, multi-billion-dollar deal.

- This move created a significant upside for investors in Triton International, but the transaction doesn't make sense to me.

- Shares of Triton International still look undervalued, even with this massive premium.

April 12th proved to be a massive day for shareholders of Triton International Limited ( TRTN ). After news broke that the company had agreed to be acquired by Brookfield Infrastructure Partners ( BIP ) in a multi-billion dollar transaction, shares of the enterprise skyrocketed, closing up 32.3% for the day. Although this is a great premium for investors to enjoy, it does strike me as a rather unappealing deal for shareholders of Triton International. Based on my assessment of the company, shares look undervalued at this point. But unless there is some way for the deal to be scrapped, I don't see much in the way of opportunity for the picture to change for the better other than for investors to look elsewhere for upside. Of course, for those who think that Brookfield Infrastructure Corporation ( BIPC ), the subsidiary of Brookfield Infrastructure Partners that will be absorbing Triton International, is undervalued, there could be an interesting avenue to explore.

An interesting deal

According to the terms of the agreement between Brookfield Infrastructure Partners and Triton International, the former will be acquiring, using its subsidiary, Brookfield Infrastructure Corporation, in a cash and stock deal that values the equity of Triton International at about $4.70 billion and places an enterprise value on the transaction of roughly $13.32 billion. On the equity side of things, this transaction translates to a 35% premium over where Triton International was trading at just one day earlier.

In many instances, cash and stock deals are pretty straightforward. You get a certain amount of cash per share, as well as a fixed amount of stock. But this transaction is a bit different. On the cash side of things, investors in Triton International will receive $16.50 per share for each unit of the business they currently own. In addition to this, they will receive what is currently estimated to be $68.50 per share of stock compensation for each unit that they own as well. However, there is a stipulation here. After all, one of the dangers of bringing stock into the equation is that a fluctuation from the acquirer can ultimately impact, sometimes positively, and sometimes negatively, the ultimate price that investors receive by the time a deal closes. As a hypothetical, if shares of Brookfield Infrastructure Corporation were to plummet by 20% between now and the time the deal closes, offering a fixed amount of stock would mean a sizable haircut for investors in Triton International. If, on the other hand, Brookfield Infrastructure Corporation guaranteed a certain value per share, a drop in its stock price between now and closing could result in significantly more dilution for the acquirer than management and shareholders anticipated.

{kind=link}

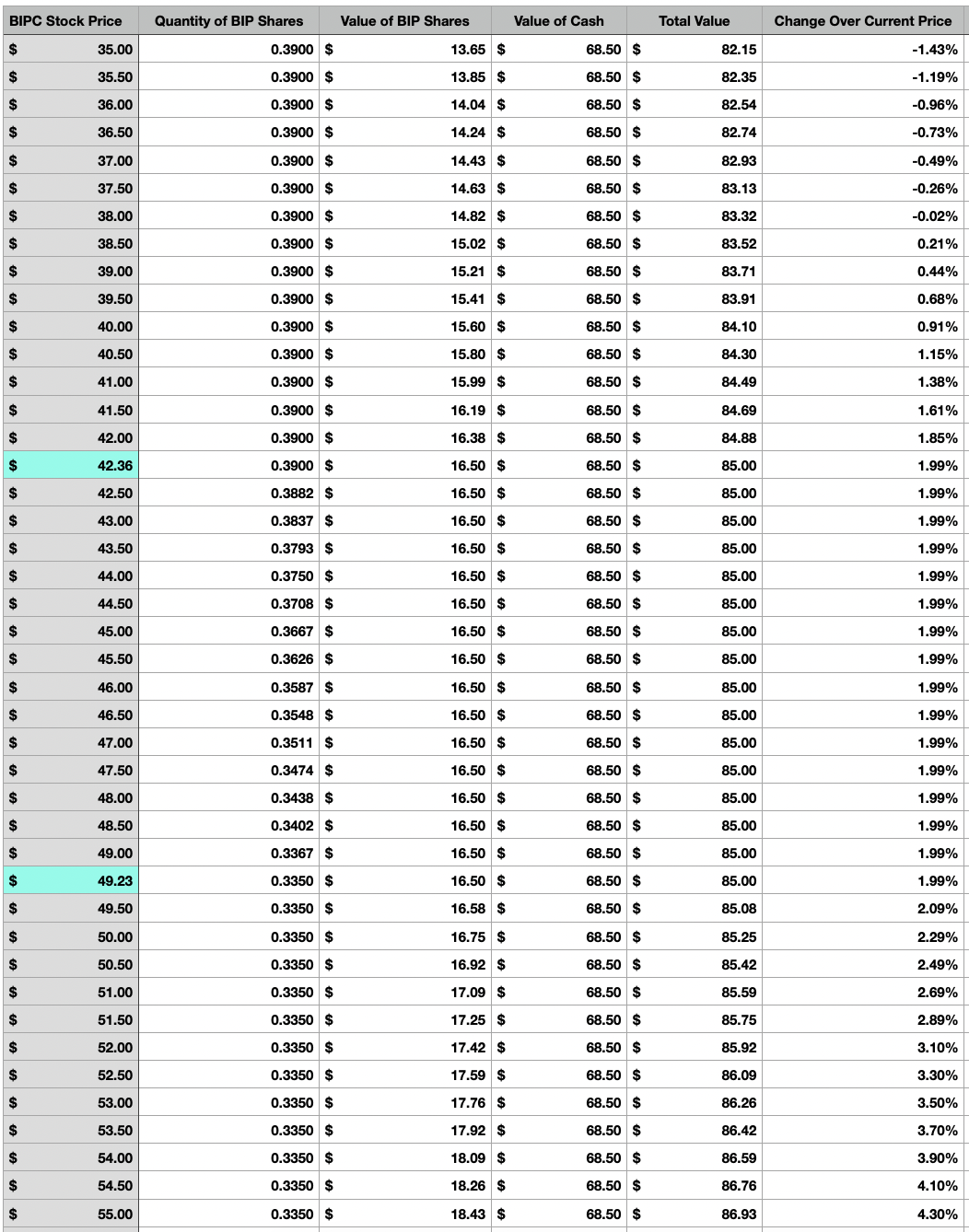

To reduce the risk of this occurring, the deal adjusts the quantity of Brookfield Infrastructure Corporation units that investors in Triton International will receive, depending on the price that the stock ultimately trades at immediately prior to the deal closing. If shares of Brookfield Infrastructure Corporation are between $42.36 and $49.23 at that time, investors in Triton International will see the number of shares of that business that they will receive fluctuate, with a lower point of 0.3350 units per each share of Triton International and an upper point of 0.3900 units. Below $42.36 per share, the number of units received will be fixed at 0.3900, while any point above $49.23 will see the exchange ratio fixed at 0.3350. The table above shows a significant number of different ways this could play out. In the event that shares of Brookfield Infrastructure Corporation drop to, say, $35, then investors in Triton International would receive total consideration that would result in a 1.43% loss compared to the $83.34 that the stock closed on April 12th. If, on the other hand, shares rise to $55 per share, they would experience upside of 4.30% compared to the implied 2% rise at a fixed consideration amount of $85 per unit.

This deal undervalues Triton International

Over the past few years, I have not followed Triton International nearly as close as I should have. The only article that I wrote about the company was published in December of 2020. In that article, I said that strong cash flows and a low trading multiple made the company an appealing opportunity. This ultimately led me to rate the business a 'buy' to reflect my view that shares should outperform the broader market for the foreseeable future. And outperform the market, shares did. While the S&P 500 is up 11.8% since the publication of that article, shares of Triton International have generated upside for investors, inclusive of distributions, of 90.5%.

For those who don't know much about Triton International, a bit of a refresher would be appropriate. According to management, the company serves as the largest lessor of intermodal containers across the globe. These are standardized containers that are used for the purpose of transporting goods and materials, often ones that are being shipped internationally. While this is the bulk of the company's business, it does also lease chassis, which are used for the transportation of containers.

{kind=link}

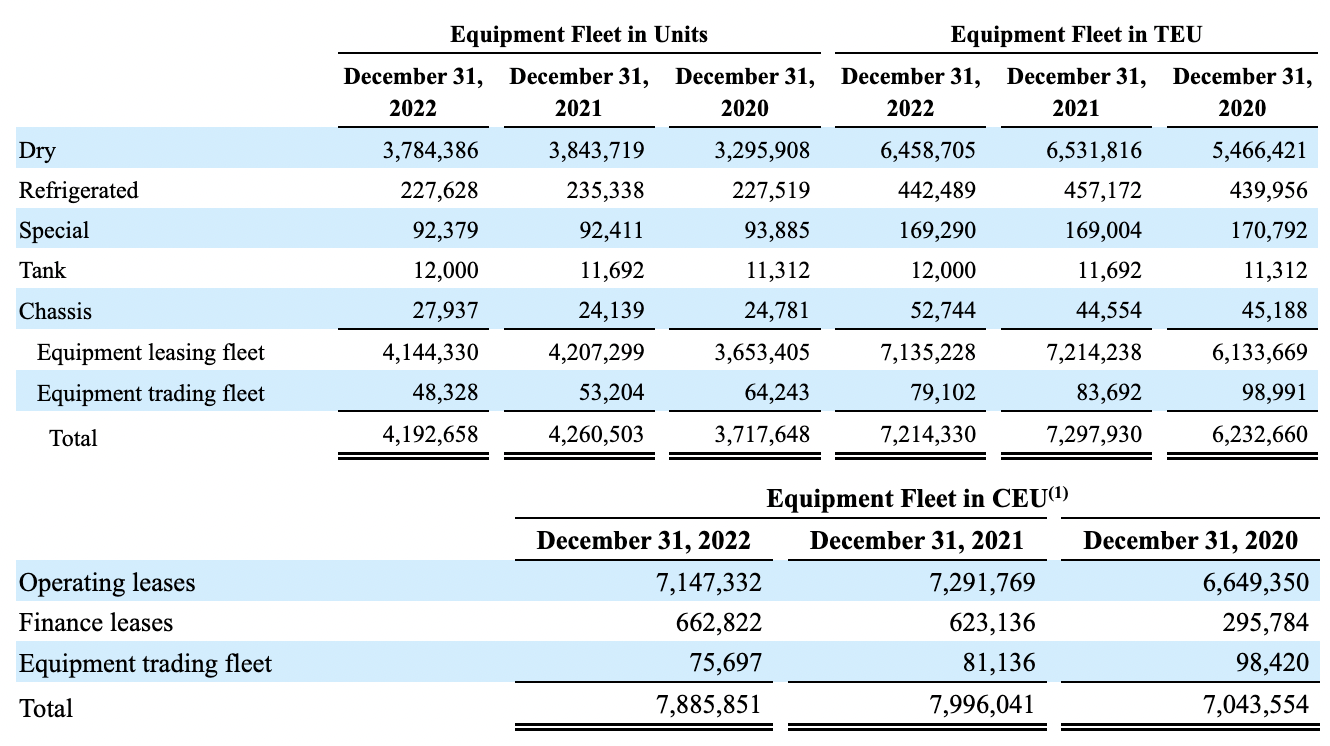

This is a rather simple business at the end of the day. But it is an incredibly vital business for the global economy to function. In all, at the end of the 2022 fiscal year, the company boasted 4.2 million containers and chassis in its portfolio, which translated to about 7.2 million twenty-foot equivalent units, or TEUs. To handle all of these, the company has grown to operate a global network of offices. On top of this, they also use third-party container depots spread across 46 different countries.

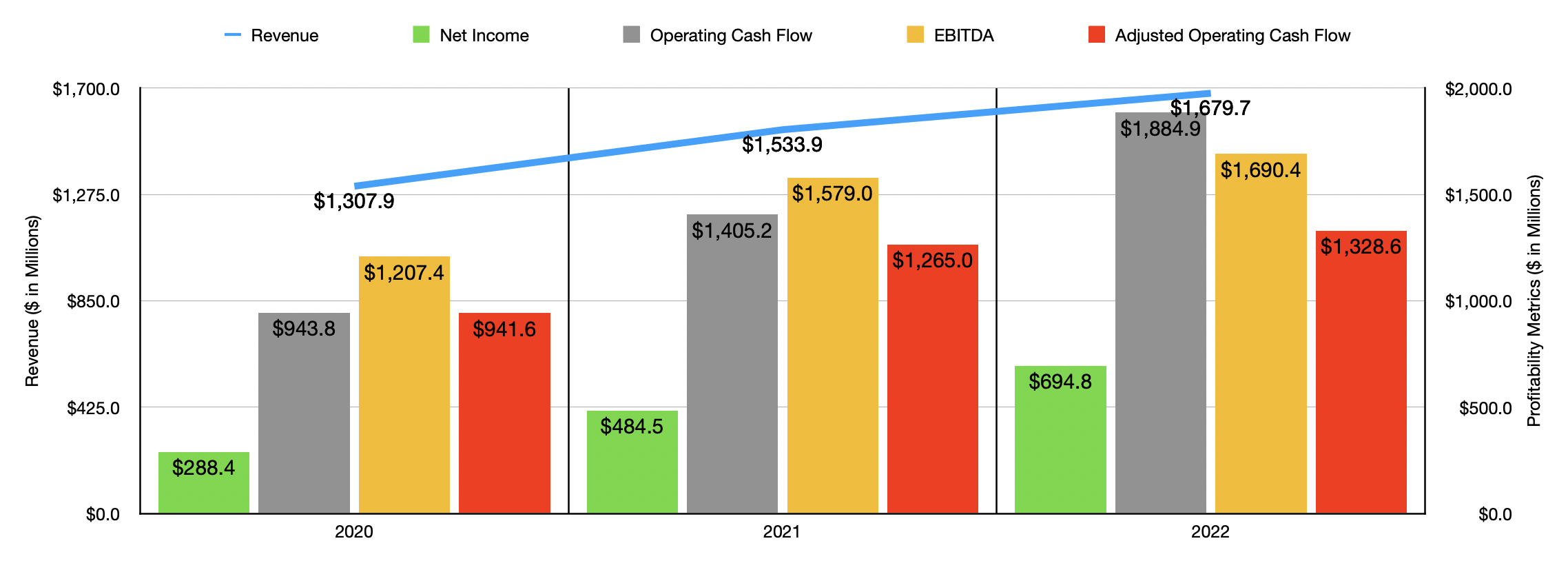

Over the past several years, the containerized cargo market has grown at a rather steady pace. Between 2012 and 2022, for instance, containerized cargo volumes expanded at a rate of about 3% per year. But of course, not every year is a good one. In 2022, for instance, global volumes dropped by roughly 3.2%. This has not stopped the company from generating strong performance. Overall leasing revenue with the business expanded from $1.31 billion in 2020 to $1.68 billion in 2022. Much of this growth was driven by a rise in units from 3.7 million to 4.2 million. But it is interesting to note that the number of units in 2021 was slightly higher at 4.3 million. This did not stop lease revenue from expanding by 9.5% year over year, even as the utilization rate of its portfolio dipped from 99.4% to 99.1%. The real driver, then, during that short window was a 4.9% jump in the average lease rate for its dry container product line, an increase in new dry containers that had higher lease rates, and a surge in finance lease revenue from $53.4 million to $115.2 million.

{kind=link}

On the bottom line, the picture has improved as well. Net income has grown from $288.4 million in 2020 to $694.8 million in 2022. Operating cash flow was also on the rise, essentially doubling from $943.8 million to $1.88 billion. If we adjust for changes in working capital, the picture is a little less bullish, with the metric climbing from $941.6 million to $1.33 billion. And finally, over the three-year window, EBITDA reported by the company expanded from $1.21 billion to $1.69 billion.

{kind=link}

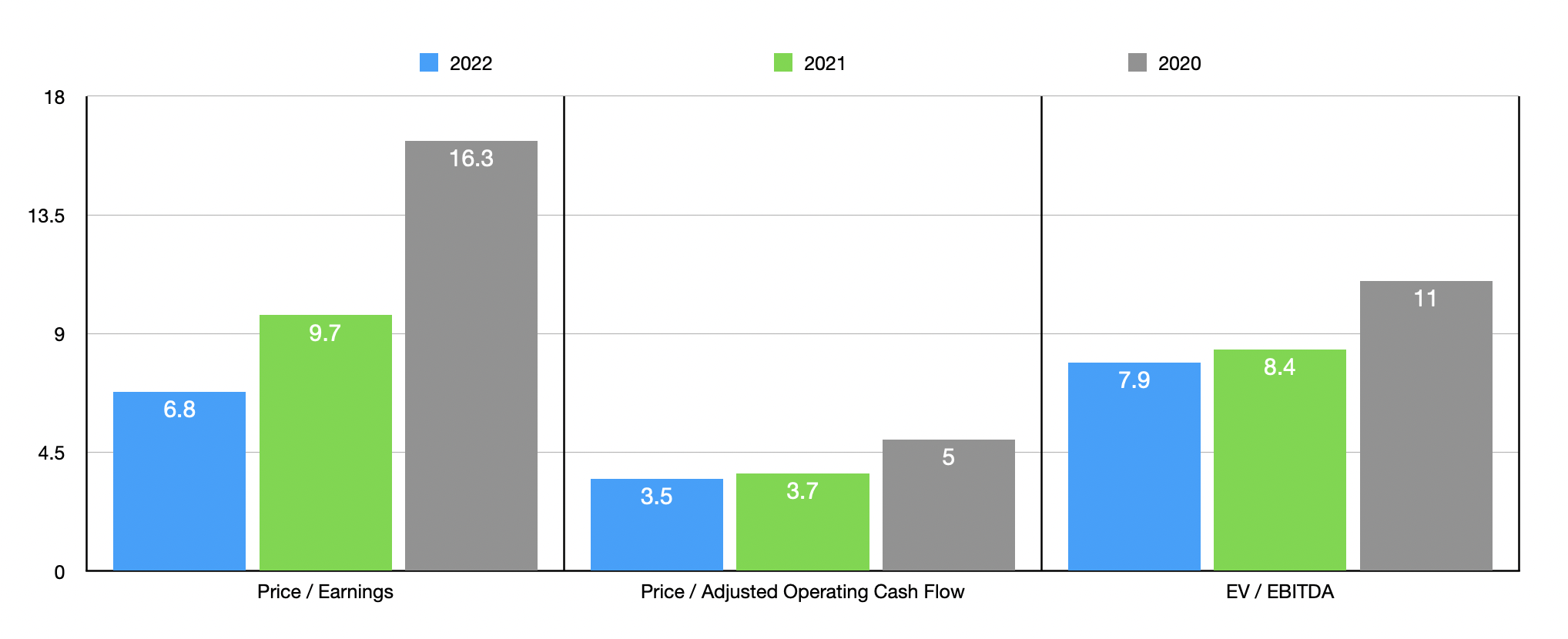

Investors would be right to point out that market conditions could change. And any change would likely be for the worse. After all, high inflation globally, combined with rising interest rates aimed at combating it, is not exactly a recipe for robust trade. But as you can see in the chart above, shares of the company look cheap, even if financial performance were to revert back to what it was in 2020. For context, a similar firm, Textainer Group Holdings Limited ( TGH ) is priced a bit lower using two of the three metrics. But on an EV to EBITDA basis, it is pricier than Triton International happens to be.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Triton International |

| 6.8 |

| 3.5 |

| 7.9 |

| Textainer Group Holdings |

| 5.3 |

| 2.0 |

| 9.2 |

Takeaway

Based on all the data provided at this time, I can understand why investors in Triton International would be excited. After all, the premium over where shares were trading previously was significant, and, assuming that Brookfield Infrastructure Partners increases from here, there could be even greater upside for investors moving forward. For those who are bullish on Brookfield Infrastructure Partners on its own, and who believe that the deal in question will be completed, buying up stock in Triton International would make a great deal of sense. However, for investors in Triton International at this time, I cannot help but to think that additional upside was left on the table.

For further details see:

Triton International And Brookfield Infrastructure Tie The Knot