TROX - Tronox: May Not Produce Adequate Returns

Summary

- Currently, Tronox Holdings plc is trading for nearly $2.5 billion. In contrast, it has produced over $286 million in the year 2021.

- The recent hike in profitability is primarily attributed to a one-time gain.

- Based on last year's earnings, it seems that Tronox Holdings plc is trading for a P/E of 9, which is a fair valuation for the cyclical stock during its cyclical uptrend.

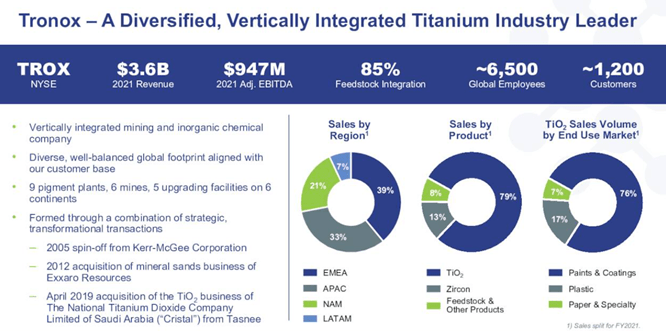

Tronox Holdings plc ( TROX ) is the world's second-largest TiO2 manufacturer, with a total market share of more than 13%. The company also operates titanium-bearing mineral sand mines, which produce feedstocks that can be processed into TiO2. A vertically integrated business model gives the company a significant competitive advantage over its competitors. With its wide customer base of over 1200, the company delivers low-cost, high-quality pigments to various enterprises throughout the world.

As a significant part of revenue comes from Asia pacific & African regions, Tronox has a substantial opportunity to serve such developing countries where the demand for TiO2 is expected to increase going forward.

Due to its presence in the commodity business, the operating results are going to depend on the industry prospects. I believe the current valuation of the business seems fair, and from this point, it may not give any adequate returns; instead, if a cyclical downturn hits the company, Tronox will have to dilute its equity to sustain its operation, which can affect the overall returns.

Historical performance

revenue (macrotrends.net )

After a significant drop in 2016, revenue has been increasing consistently. From a low of $1.3 billion in 2016, revenue touched $3.5 billion by 2021 . Also, the company has a long history of losses due to significant fluctuations in the price of TiO2. As a result of strong industry performance during the last two-year period, Tronox has posted over $303 million in net profits in the last year. But the performance is primarily attributed to strong demand and fair pricing for TiO2 products; if the demand drops, the company might face losses, as seen in the historical performance.

Furthermore, despite having a vertically integrated business model, the company has posted huge losses in the past years. In contrast, its competitors like Chemours (NYSE: CC ) and Kronos Worldwide (NYSE: KRO ) could manage to earn significant profits over the same period. Such huge losses might indicate that the company lacks pricing power over its customers. Also, to sustain in the business, the company has diluted significant stake over the last few years; as a result, total outstanding shares have increased from 99 million in 2012 to about 155 million by now.

share price (YCharts)

Also, over the course of the period, the stock price has seen substantial ups and downs, ranging from $3 per share in 2016 to about $27 per share in 2017. Despite significant losses and consistent equity dilution, the company has remained at a fair valuation, which shows that investors still have confidence in the business model; it might be due to the vertically integrated business model and a considerable market share in the global TiO2 industry.

I believe buying a cyclical stock during its cyclical downturn can give substantial returns, but buying the stock at a fair valuation might hurt the returns.

To clearly understand the cyclicality of the TiO2 industry and to take a glimpse of its competitor, the investor can read my recent article on Kronos , which can help the investor to make a better decision.

Strength in the business model

Business model (investors presentation)

{kind=link}

The vertically integrated business model of the company provides a significant competitive advantage over its competitors. Tronox produces its primary raw material internally; as a result, it can provide services at a very low cost. Also, the company's customer base is considerably diversified, which reduces the risk arising from customer concentration.

Although the cash reserves are very low, the company has significant fixed assets with moderate debt, which substantially strengthens the business model.

initiatives (investors presentation)

{kind=link}

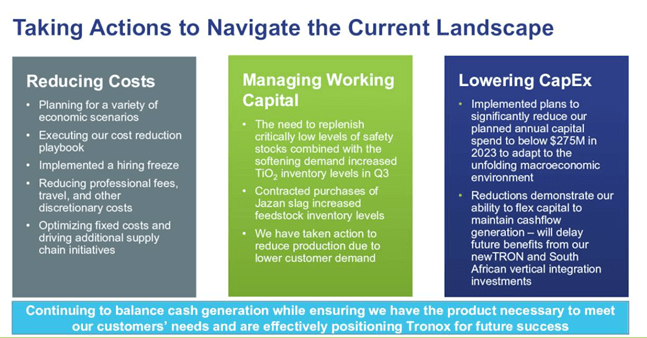

Recently management has been working extensively on various initiatives to drive operational efficiency; such efforts can help the company improve its profit margins and cash flow in the upcoming years.

Risk factors

Historically, Tronox Holdings plc management has been focused on keeping cash reserves at adequate levels to cope with adverse cyclical downturns, but as a result of debt reduction initiatives, the overall cash reserves have gone down significantly to $91 million. Although it has over $1.9 billion in liquid assets, the debt levels seem considerably high as compared to cash reserves, which might bring concerns while obtaining debt refinancing.

Furthermore, over the last five years, cash flow from operations seems to have been increasing, which is a good sign for business stability; but consider that such performance is primarily attributed to the strong demand in the TiO2 markets. Therefore, any industry demand and supply imbalance might significantly hurt business performance.

Recent development

quarterly results (quarterly report)

In the recent quarter, net sales have increased from $870 million in the same quarter last year to about $895 million by now; as a result of strong revenue generation, Tronox Holdings plc could drive net profits to $121 million. Such a strong performance is primarily attributed to strong industry prospects. Also, due to the tax benefits received by the company over the last nine months, the company could achieve over $512 million in net profits; therefore, the investor must consider that such a hike in profitability is primarily attributed to a one-time gain.

As per the target set by the management, Tronox Holdings plc could achieve 2.5x net leverage on a TTM basis. Also, the company has been actively repurchasing shares and has been paying dividends.

Currently, the company is trading for nearly $2.5 billion. In contrast, it has produced over $286 million in the year 2021; based on the last year's earnings, the company has been trading for a PE of 9, which is a fair valuation for the cyclical stock during its cyclical uptrend.

TROX stock is trading for nearly $16.4 per share. Although the business performance looks strong, any significant reduction in demand from the TiO2 market or any new capacity addition might hurt the profitability; in such case, the stock price might drop significantly. (Historically, the TiO2 industry has seen substantial fluctuations in demand and prices.)

I believe Tronox Holdings plc stock is fairly valued, and from this point, it may not give any adequate returns for the shareholders. Also, buying the stock at its cyclical high or mid-level might bring substantial risk; therefore, I assign sell ratings to Tronox Holdings plc stock.

For further details see:

Tronox: May Not Produce Adequate Returns