TFC - Truist Bank: Top Value Pick From Beaten-Down Banks

2023-10-19 14:48:43 ET

Summary

- Truist Financial has taken prudent action to maintain and improve its capital positioning and secure its dividend amidst the bank turmoil of early 2023.

- The reaction by private companies and federal funding to the bank crisis suggests that a bank of Truist's size would not be allowed to fail.

- Truist Financial has been quick to shore up capital and improve its balance sheet, positioning itself to survive a potentially rough 2024 with the dividend intact.

Thesis

The bank turmoil of early 2023 caused a severe decline in the value of almost all regional bank shares. Now more than six months away, many banks with stable balance sheets are still trading at rock-bottom multiples. I believe that Truist Financial ( TFC ) has taken prudent and timely action to maintain and improve its capital positioning and secure its dividend. While I see near-term headwinds from defaults and NIM pressures, I rate the stock a buy on dividend yield and value.

Company Overview

Truist Financial is a diversified consumer bank with operations focused in the Southeastern and Mid-Atlantic United States. The company operates in consumer banking and wealth, corporate and commercial banking, and insurance. The 2019 merger between Atlanta-based SunTrust and Winston-Salem-based BB&T formed Truist, and the conglomerate emerged as a top 10 US bank by asset holdings. After trading at over $50 in February, the collapse of SVB and the following bank distress hit the stock hard, and Truist is now trading under $30. However, I believe that the response to the bank upheaval, combined with the scope of Truist and the underlying realities of the bank's holdings signal that solvency risk is relatively low.

Regulatory Reaction

The reaction to the bank crisis of this spring by both private companies and federal funding was sufficient to convince me that a bank of Truist's size would not be allowed to fail. While the Federal Reserve never deviated from its path to stem inflation, every other tool at its disposal was used to quiet the crisis. For starters, they essentially turned the bank run into a dinosaur , fully guaranteeing deposits both insured and uninsured in the Silicon Valley Bank seizure. While deposit flight phenomena will obviously still exist, I see the precedent being set that all depositors be fully insured- and find it a truly rare day when regulators hand back power and funding. The Fed also provided short-term liquidity and allowed banks to lend on the par value of U.S. Treasuries and other high-quality assets. The Federal Reserve remains highly vested in preventing widespread banking catastrophe, and letting a bank with over $500 billion in assets fail would have widespread calamitous results.

Financials

Income Statement

While I believe Truist is undervalued and fundamentally sound, there are areas of weakness caused by macroeconomic trends reflected in the income statement. Near-term headwinds include cost of funding, write-off increases, and deposit competition. First, I believe that NIM has peaked for banks during the current interest rate cycle. While the market is just reaching, or almost at the terminal fed funds rate, and will likely need to hold steady for the foreseeable future, NIM pressure will arise as rates eventually drop.

{kind=link}

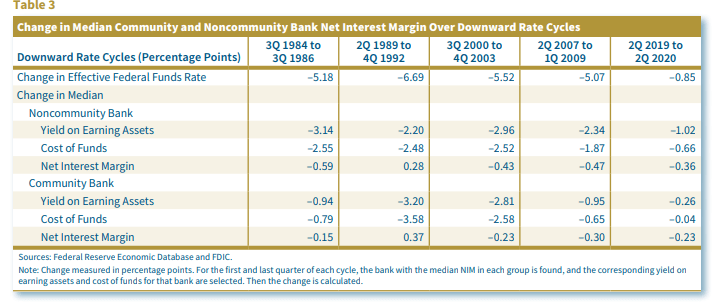

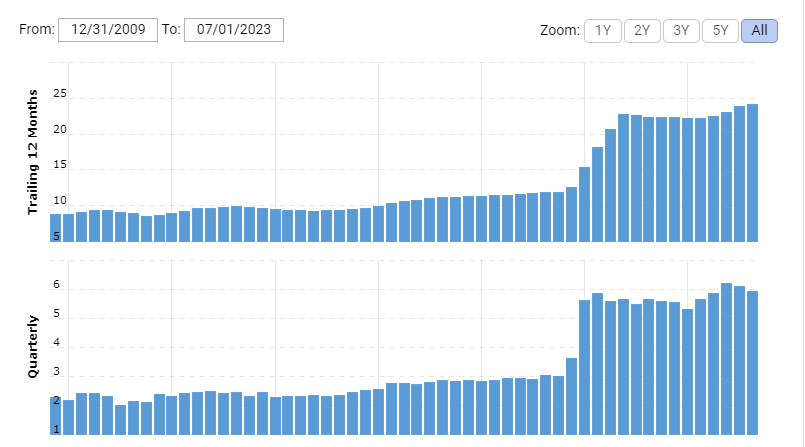

While by no means a perfect relationship, it is clear that overall, the cutting cycles of the federal funds rate result in NIM contraction for banks, though less pronounced in community banks. Even prior to this cutting it appears NIM has peaked for Truist and other such banks, with peak NIM appearing to have peaked 4Q22. This is attributable to the cost of funding rising higher than the return on assets, as consumers have become more selective with funds, and attracting deposits has come at higher costs.

{kind=link}

However, the company's management has been taking action to ensure they can weather uncertainty. I will analyze the Fed's stress test results for Truist more in the balance sheet/capital positioning segment, but materially to income, the company has begun to cut costs by reducing headcount and streamlining technology and footprint. The cumulative impact of this is that the company expects savings of up to $750 million on non-interest expenses next year. I consider this a prudent and positive action as the company and management focus on controlling the controllables and staying lean in a challenging period.

Let me be clear though, I believe that Truist is well-positioned to survive and grow in the future. Banking is an extremely profitable and established industry, and while cyclical factors such as NIM may compress margins temporarily, the long-run growth is worth buying while collecting the large dividend. Indeed, the large banks have started the earnings season off strong, and Truist too will report- another profitable quarter with an increase in capital.

{kind=link}

Balance Sheet/Capital Positioning

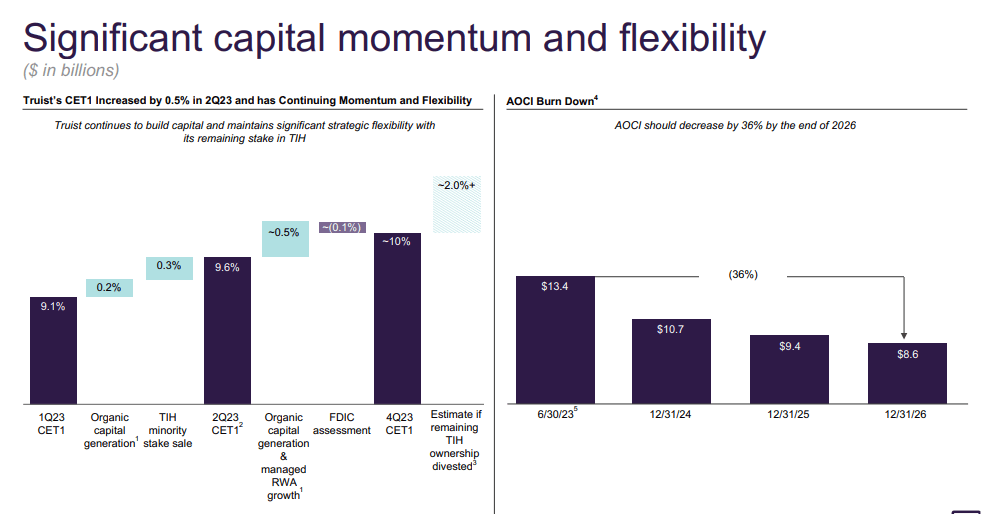

Truist Financial has been quick to shore up capital and improve the balance sheet since this spring, and I believe they have positioned themselves to survive a potentially rough 2024 with the dividend intact. However, I believe the bank was whooped this spring for a reason. Truist compared to peers has a relatively low CET1 ratio and also faced a high percent of unrealized losses on their bond holdings, but never meaningfully faced widespread deposit outflows.

The bank has since worked to improve its positioning drastically. Besides the expense cuts that will help maintain dividend coverage, Truist has begun the process of selling its insurance business. I believe this is an incredibly accretive sale by management for both the company and investors, as it will drastically change the capital position.

{kind=link}

The company is already working to build up reserves, a cushion of capital, and now is working to sell the insurance portion of the business at a $10 billion valuation that would raise the capital ratio by up to 2%. I believe that this transaction would be an opportunity for the market to significantly re-rate the riskiness of the stock.

However, another reason the stock trades lower at the moment is the possibility of a recession in the future. This would lead to higher losses on loans and the need to increase write-off rates above forecasted levels. However, because banking is so core to functioning economies, it is also highly regulated and the government tests banks on their ability to weather just these situations. I highly recommend these Fed stress tests for those interested in a light read.

Fed reserve board

As you can see, in the severely adverse simulation created by the Federal Reserve, Truist holds up better than the average bank. While they do still drop lower in CET1, this shows the resilience of the balance sheet and loan portfolio. It is also worth noting, that this is a worst-case situation , with the Fed conducting the simulation under the conditions of a severe global recession, with a particularly weak market for commercial and residential real estate as well as a hobbled debt market. Even in this case, the Reserve Board determined that banks would have adequate funding and liquidity to continue to lend.

Valuation

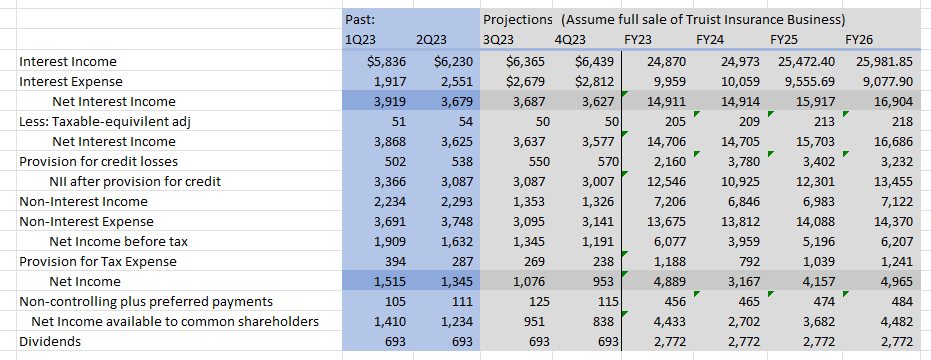

In valuing Truist I modeled with a pessimistic forecast in mind to determine the validity of the 7% dividend yield. My forecast is based on a decline in NIM characteristic of this phase of the rate cycle, a modest uptick in cost of funding and write-offs, and made with the assumption that the rest of the sale of the insurance business will proceed as planned.

{kind=link}

I also left growth rates low to account for the loss of some of the loan portfolio and to build in margin of error into the valuation. I believe that this model is realistic and shows both why the stock is currently distressed, but also why it has upside potential ahead. As you can see, in my projections the company remains profitable next year but does have more dividend payments than income, resulting in a slight reduction in retained earnings. However, in my opinion, the company is committed to the dividend, and the sale of the insurance business will allow it to maintain the dividend.

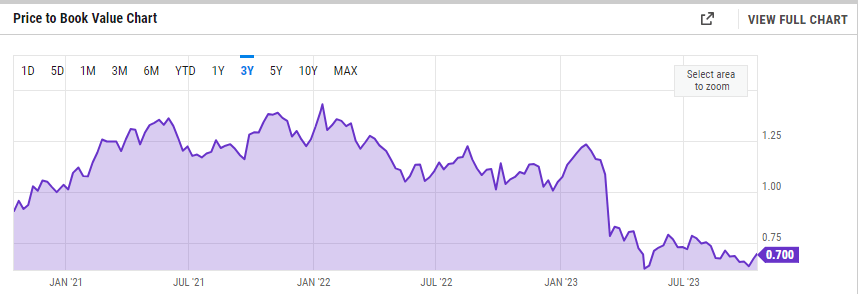

Therefore, in my opinion, the base case is the dividend is held steady and the stock slowly appreciates to the level of book value. Right now the stock is trading far below book much closer to tangible book value. However, history shows that once the market becomes more optimistic it will likely rebound.

{kind=link}

If the company can return to book value by the end of 2025 and the company pays out the same level of dividend, an investor would return 22% annually, shattering the average market return. Therefore, I put a strong buy rating on the stock at any price below $35 based on yield and return to book value. I believe that this represents a massive opportunity for the common investor to capitalize on the pessimism of the market and lock in a market-crushing yield.

Threats to Thesis

While the company is already acting upon the balance sheet issues to create a fortress for any coming storms, investing in Truist still has some risk. One is the double pressure put on NIM from the rising cost of lending and the competition over deposits. Another is macro-conditions and the threat that next year could be worse than originally anticipated. Finally, the losses on long term bond holdings have deepened during recent bank earnings, and I expect that Truist too will put up a massive amount of unrealized losses. However, it is my belief that Truist will never have a liquidity crisis, and therefore these bonds will eventually be realized at par value. In my opinion, the current price of Truist realizes all of these threats without acknowledging the profit potential or cash flow distributions of the business.

Conclusion

Truist Financial represents one of the best possible value opportunities in the present market. The company has been rocked by issues in the sector, and now trades and extremely low multiples. However, the company has been pro-active and wise in shoring up the balance sheet for next year, as well as implementing expense cuts to maintain the dividend and bottom line. I believe the best investment thesis is simple, and waiting for a top-10 US bank to return to book value and appreciate 30% all while being paid a 7%+ dividend yearly makes buying Truist a potentially lucrative long-term investment for any value-inclined investor.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Truist Bank: Top Value Pick From Beaten-Down Banks