PACW - Truist: Don't Forget About This Deep Value Gem

2023-06-09 05:38:30 ET

Summary

- Truist Financial remains cheap in spite of positive industry developments.

- It's likely that investor sentiment in regional banks has already bottomed.

- We previously called out a profitable trade in TFC stock, and we think a similar trading opportunity now exists for income-oriented investors.

A few months ago, we wrote an article titled " Truist: Following Earnings, We're Ready To Start Buying ", which was centered around the recent flare up in our country's regional banking sector.

We highlighted the company's strong track record and attractive valuation, and concluded the article by arguing that the company was a buy, as the liquidity issues present for SIVB and other failed banks were not a material threat to Truist ( TFC ). Additionally, Truist's Commercial Real Estate exposure was (and still is) minimal, which reduced the risk of default for the company even if loans began going bad in that economically troubled industry.

We wrapped our thesis up by offering what we thought at the time was a great risk-reward trade opportunity; selling the June 2nd, $26 strike put options for $45 per contract (a 1.76% return over ~42 days).

Last week, that trade reached a successful conclusion, and we think a similar opportunity now exists in the stock.

Today, we'll review the company's value proposition, highlight a few new developments that make another put sale appealing, and dive into that trade's specifics for those who may be looking to get involved in Truist with a more income-oriented approach.

Review

In case you didn't read our previous article, or are new to Truist in general, here's some key information to help bring you up to speed:

1.) Truist Financial is a large regional bank that has been trading at a discount to its historical multiple due to concerns about deposit stickiness and commercial real estate exposure. However, we believe that these concerns are overblown and that TFC is a compelling buy at its current valuation.

2.) Truist has demonstrated consistent and impressive financial performance in recent years. Net margins briefly deteriorated in 2019 due to the merger but have since returned to pre-pandemic levels. Revenue has also grown by over 136% and free cash flow has almost doubled since 2018:

TradingView

3.) These strong results have been driven by a number of factors, including economies of scale, new digital product launches, and a solid, diverse loan book.

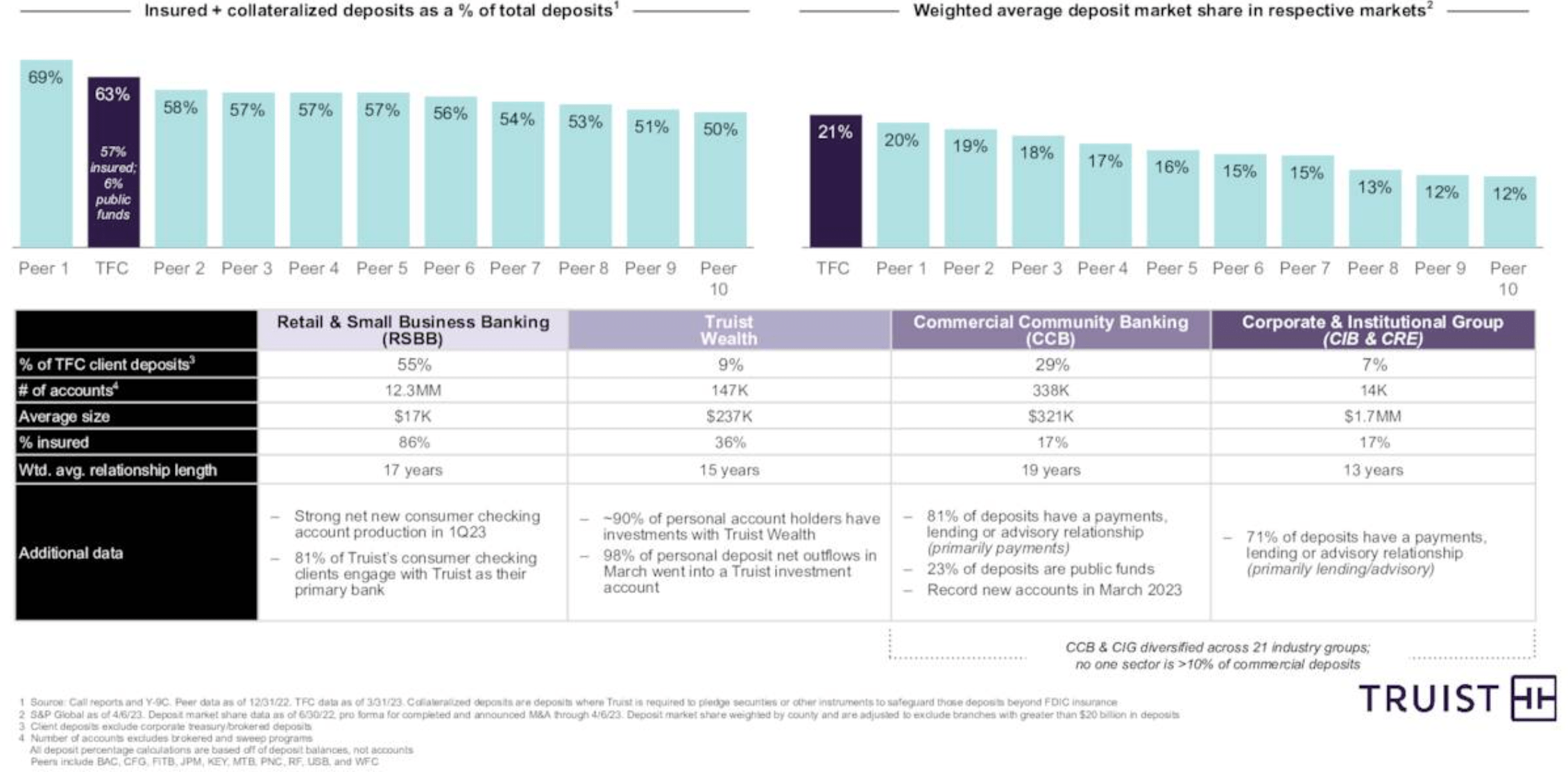

4.) TFC's core net interest margins are strong, and its deposit base is sticky. A high percentage of deposits are covered by FDIC insurance, and its average customer account age is over 15 years:

{kind=link}

5.) We believe that TFC's exposure to commercial real estate is suitably low. Only 11% of TFC's outstanding loans are CRE-related, and only 18% of those loans are to potentially economically suspect office-space owners.

Developments

Now that we're all up to speed on why we think the company offers compelling value, there's been some updates from the financial and regulatory community that are worth sharing here. In short, most of the news since our initial article has been good.

First up, in early May, J.P. Morgan began getting more constructive on regional banks. Up until that point, a lot of the news surrounding the industry was primarily "doom and gloom" as pundits and outlets speculated about how bad the fallout could be. This call by Steven Alexopoulos shifted the narrative somewhat, and people began talking about how it was possible sentiment had bottomed.

Next, in mid-May, Michael Burry's 13F came out and showed that the prescient investor (of "The Big Short" fame) had begun buying stakes in regional bank stocks, including NYCB , PACW , and WAL . This was another vote of confidence from a highly followed and respected investor.

A few days later, Fitch Ratings concluded a review of small and mid-sized regional banks in the U.S. and introduced no new ratings cuts, which was yet another positive sign that the majority of the bleeding had been stopped.

Finally, early this month, regional bank bonds have begun to rebound in price , indicating significantly improved investor sentiment surrounding bank risk.

Taken together, we think the environment has significantly improved, and the risk is mostly behind us. However, since our initial article, Truist stock is only up 5%. This seems like a tepid reaction to the news flow, and thus we are upgrading our rating on the stock to "Strong Buy".

The Trade

While the stock may be a strong buy, shares of companies in the industry continue to remain highly volatile on a day-to-day basis. Thus, we think a similar trade to our first successful recommendation a few months ago continues to be the most optimal way to deploy capital.

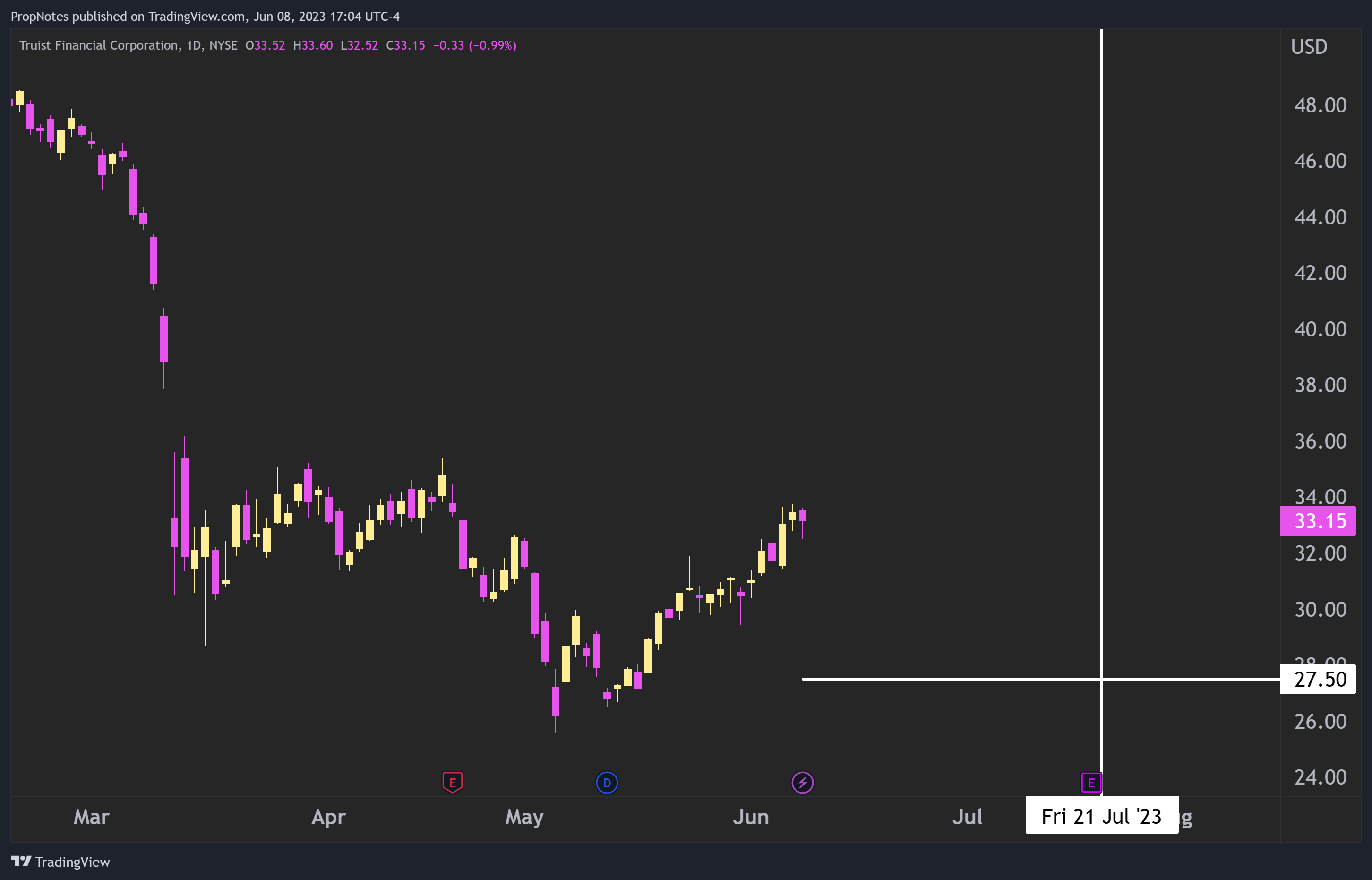

For us, we like shorting the July 21st, $27.50 strike puts that are currently trading for 0.40 cents on the bid:

{kind=link}

These contracts return 1.47% cash-on-cash, which annualizes to about 12.5%; a healthy return. In addition, these contracts boast a -18.2% breakeven point, which means that the stock has some room to drop, and the trade still may end up profitable.

Finally - if assigned, put sellers would be acquiring shares at a recent support level in the stock, as well as at a highly attractive ~4.5x free cash flow multiple.

To us, this setup seems like a win-win scenario.

Risks

While our idea has a significant probability of success and a solid return profile, there are some risks to be concerned about, just like last time:

Earnings : Company earnings are due out the day before option expiry, and the event could cause a large unfavorable dislocation in shares. Even if the numbers are solid, shares could slide considerably. With the trade we outlined, put sellers have an 18% margin of error, which is quite large when taking into account recent Truist earnings moves. However, anything can happen (as evidenced by a recent bad call we made).

Industry : Truist's shares are closely correlated with other stocks in the industry. If bad developments shake things up, then it's possible that TFC could trade down further, even if the company isn't materially impacted by whatever the event is.

Macro : Finally, Truist is subject to broader macroeconomic risks, including interest rate fluctuations, economic downturns, and changes in government policies that could impact the banking sector. Some recent conversations have focused about heightening capital requirements for banks with over 100 billion in assets, which would impact the industry significantly if implemented. This could also hurt capital return policies and may hurt total returns in the medium term.

There are some risks to be aware of, however, we think the potential for returns and upside far outweighs the concerns.

Summary

All in all, we remain bullish on Truist. The company has performed well in a tough market and is poised for more upside. It's also materially undervalued in light of continued positive developments.

We think a repeat trade, similar to the one we called out previously, is a great way to take advantage of the solid underlying fundamentals and potentially acquire a stake in this deep value gem at an even more attractive price.

For further details see:

Truist: Don't Forget About This Deep Value Gem