TFC - Truist Financial: A Secure Dividend And Attractive Valuation Create Opportunity

2023-09-25 04:00:48 ET

Summary

- Truist Financial shares have underperformed, but with shares near a 52-week low and a 7.4% dividend yield, investors should consider buying.

- TFC has faced challenges with rising credit costs and higher funding costs, leading to a decline in deposits and a compression of its net interest margin.

- The bank's capital position is solid, and while the dividend is secure, buybacks are unlikely until mid-2025 at the earliest.

Like many regional banks, shares of Truist Financial ( TFC ) have been a poor performer, losing over a third of their value. Last October , I recommended buying shares - a recommendation that has not worked well for investors, as I had not foreseen the extent of the banking crisis and fight for deposits we saw earlier this year. With shares near a 52-week low and offering a 7.4% dividend yield, I do think investors should buy TFC here and would reiterate a buy recommendation.

{kind=link}

In the company's second quarter , Truist earned $0.92, down 16% from last year as the company has been hit by both rising credit costs and higher funding costs. Given the aging of the economic cycle and fading of government stimulus, rising credit costs were to be expected but the headwinds from rising funding costs have been more severe than I expected last year.

This is of course due to the failure of Silicon Valley Bank, which set in motion significant deposit churn, particularly among uninsured depositors, and increased deposit costs. Frankly, Truist managed through the deposit fight worse than I would have hoped, though it has begun to find its footing.

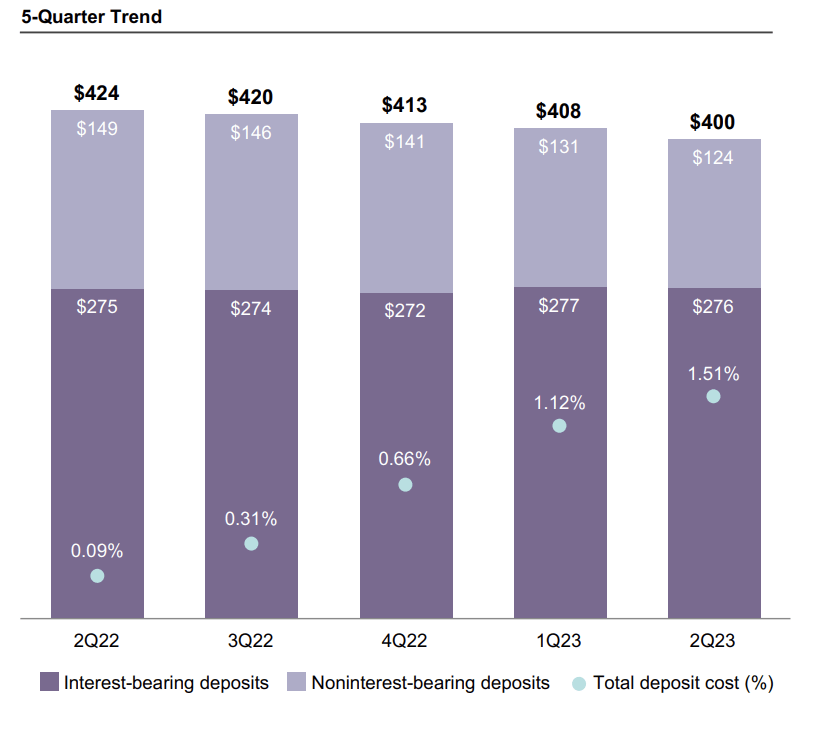

On average, deposits fell 2% sequentially and 6% from last year to $400 billion. Commercial bank deposit balances have fallen by 4% from last year , so TFC has underperformed this trend, meaning it has lost deposit market share. Given its size and focus on faster-growing Southeast markets, I would have hoped it would be a safe-haven winner, able to take share from smaller banks.

{kind=link}

As you can see from the above chart, TFC's entire deposit attrition has been from noninterest bearing accounts. With the ability to earn over 5% in money market funds, companies and consumers are taking down cash balances here as much as possible. At the same time, TFC has been forced to raise deposit yields significantly to retain interest-bearing deposits. Deposit costs were up 39bp sequentially and 142bp from last year, averaging about 2.19%. We will likely see deposit yields rise again in Q3 as deposit rate increases taken during Q2 have their full impact, alongside the July Fed rate hike.

Ultimately, TFC may have been too aggressive in not passing along higher rates to its depositors last year, which left it vulnerable to losing depositors to other banks offering higher rates and forced the more aggressive increase in yields in recent months. Fortunately, the recent hikes do appear to have stabilized things. While deposits on average fell in Q2, on an end-of-period basis, they rose by $1 billion in Q2 to $406 billion.

This rise in funding cost has compressed Truist's net interest margin ((NIM)), which was rising throughout last year, reaching 3 .25% in Q4 2022 . It now sits at 2.91%. Loan yields of 5.89% were up 17bp sequentially and 234bp from one year ago, which only partially offset the rise in deposit costs last quarter. In addition, whereas its loan book is primarily floating rate, its securities portfolio is largely fixed rate, and so that yield only rose by 3bp to 2.17%. As with most banks, TFC has a large unrealized loss on its securities portfolio. The portfolio shrank by $3 billion last quarter to $138 billion, and I would expect it to allow maturities to gradually shrink the portfolio over time and reduce funding needs.

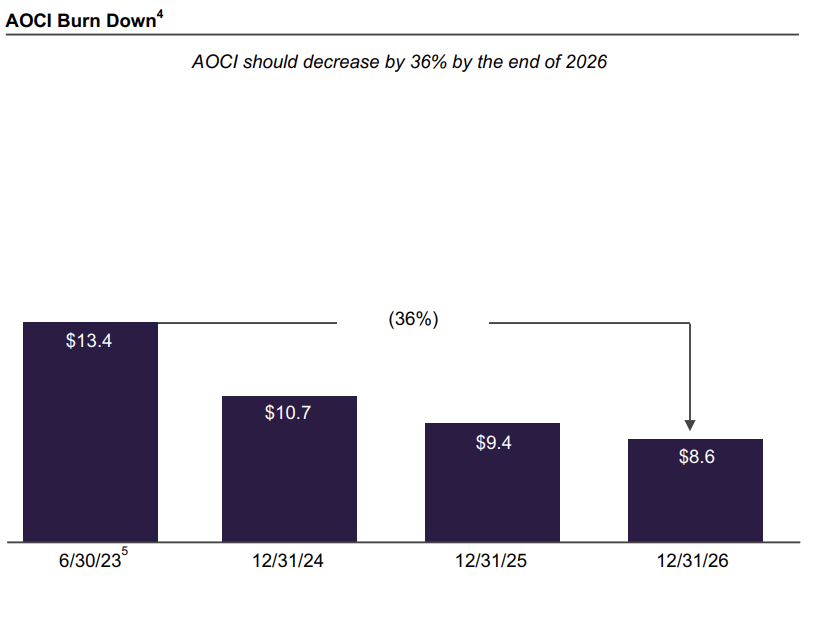

As the portfolio winds down, bonds mature, and others gradually accrete back towards par, the unrealized loss, which sits in accumulated other comprehensive income (AOCI) will decline. Based on rates prevailing at end of Q2, Truist expected losses to shrink from $13.4 billion to $8.6 billion by the end of 2026. As interest rates have risen since, this improvement in AOCI is likely to take longer. Still, the fact this will gradually get better as the portfolio matures is important to keep in mind later when we discuss TFC's capital positioning.

{kind=link}

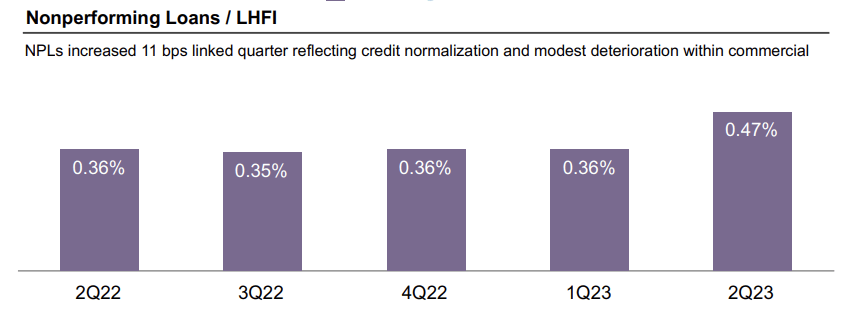

On the credit side, loans were down 1.7% sequentially, led by a reduction in student loans - excluding this, loans were down 0.2%. Truist took $538 million in provisions for credit loss, triple last year, and up 7% sequentially. The bank has $4.6 billion in reserves for credit losses, which covers 1.43% of loans, a 6bp increase due to economic uncertainty. This is triple the nonperforming loan ((NPL)) rate. That is adequate if we see stabilization at the higher level registered in Q2. We should see provisions start to align more closely with charge-offs, or $300-$400 million/quarter - higher than 2022 levels but lower than last quarter given the build that has occurred in reserve levels.

{kind=link}

Within its portfolio, office loans are a particular headwind. Office space accounts for 1.6% of its loan portfolio, and its nonperforming loan rate is 5.6%, more than 10x the 0.47% nonperforming loan rate on the entire portfolio. Loan-loss reserves are 6.2%. If we assume a 50% loss on default, a conservative assumption, TFC could see a 12% default, more than double the current NPL rate, before reserves are exhausted. As such, while the office portfolio is likely to see losses, they look properly reserved for already.

Noninterest income was a bright spot, up nearly 3% to $2.29 billion, thanks to record insurance revenue. I would note the bank did a Truist completes previously announced sale of a minority stake in Truist Insurance Holdings to Stone Point Capital of a 20% stake in its insurance unit at a $14.8 billion valuation. This has helped its capital position, and there is the potential for TFC to divest more of its stake over time. Mortgage activity will be a headwind for noninterest income as higher rates reduce the number of transactions.

The common equity tier 1 ratio (CET1) was up 50bps to 9.6% sequentially, thanks in part to the sale of the insurance unit. Capital should reach 10% by year-end thanks to retained earnings and managing risk-weighted assets lower, namely by letting its securities portfolio roll off. This is a solid capital position. However, capital is just 6.6% in theory when one is including its $13.4 billion AOCI loss.

Fortunately, Truist will have four years to phase-in AOCI into this calculation based on regulatory changes. As noted above, by then, the AOCI loss will be smaller as bonds under water today mature. Additionally, based on my earnings expectation, TFC can retain about $1.5 billion in capital/year after its dividend. That means by the end of 2026, even factoring the entire AOCI loss (ahead of the regulatory schedule), CET1 will be back above 9%. Based on this, I view the dividend as secure but any buybacks as unlikely until mid-2025 at the earliest.

One caveat to this would be if TFC sells more of its insurance unit, which would provide up to 200bps of capital accretion. By doing so, it would more quickly have capital where it wants to, enabling buybacks to turn back on more quickly. Such a transaction could make sense if TFC can get a valuation better than where its common stock is trading, but for now, I am assuming further large-scale divestitures are unlikely.

Tangible book value per share finished Q2 at $20.44. Excluding AOCI, it would be about $30.50, a modest premium to where shares are trading today.

Assuming another 20bp of NIM compression and a $400 million credit loss rate, alongside a 2% decline in noninterest income from lower mortgage activity, Truist would face a combined $0.11 headwind to quarterly earnings from Q2 levels for a run-rate of $0.80-$0.82. That is about $3.25 in full year earnings power. This assumes no growth in assets or deposits, which I view as conservative, particularly given its favorable Southern geographic footprint.

Today, shares are 9x earnings, and I view this as an attractive opportunity given much of the headwinds from higher deposit costs are already in results. Additionally, with the bank, even at this lower earnings rate, retaining significant earnings after its dividend, I view that 7.4% yield as secure. As such, investors are being well compensated to be patient and hold shares. I would expect shares to get to 10x earnings, as there is greater confidence about results having troughed or a $32-$33 price target, which combined with the dividend, affords an 18-20% return potential. Now is a good time for investors to buy in or add to TFC positions.

For further details see:

Truist Financial: A Secure Dividend And Attractive Valuation Create Opportunity