TFC - Truist Financial And U.S. Bancorp Q3 Earnings: A Caveat Hidden In Plain Sight

2023-10-13 11:50:39 ET

Summary

- U.S. Bancorp and Truist Financial Corporation will report their third-quarter results next week on Wednesday, October 18, and Thursday, October 19, respectively.

- I share my expectations for the two banks given the choppy environment and recent signs that the yield curve is beginning to flatten (and ultimately normalize).

- I will also take a look at TFC and USB's deposit trends and loan portfolio quality and share my expectations for the recently concluded third quarter.

- In addition, I will discuss an important risk indicator related to the still significant - but no longer widely discussed - issue of unrealized losses on Truist's and U.S. Bancorp's balance sheets.

Introduction

Truist Financial Corporation (TFC) and U.S. Bancorp (USB) are two of the "smaller" major banks in the U.S. whose stocks have fallen dramatically in response to the collapse of Silicon Valley Bank ( SIVBQ ) in March of this year. As I have explained in my various articles on the two banks (e.g., HTM and AFS portfolio discussion, analysis of stress test results ), they are clearly not without issues, but their stocks have been excessively punished, in my view.

With U.S. Bancorp due to report its third-quarter results pre-market next Wednesday, October 18 , and Truist due to report its earnings pre-market a day later , it's time to take a fresh look at what to expect from the two banks given the choppy environment and the recent indications of the yield curve beginning to flatten. In addition to my expectations for the upcoming quarterly results of USB and TFC, I will take a look at deposit trends and the quality of the loan portfolios. I will also discuss an important risk indicator related to the still significant - but no longer widely addressed - issue of unrealized losses on their balance sheets. Recall that SVB collapsed due to a bank run triggered in response to the rather obvious and at some point no longer sustainable maturity mismatch between its investment portfolio and its deposits.

What To Expect From Truist Financial's And U.S. Bancorp's Upcoming Earnings Reports?

A Look At The Yield Curve

The yield curve is still inverted and therefore continues to weigh on banks' earnings. As I have explained in this article , there are three basic ways in which conventional banks make money, one of which is by deliberately mismatching the overall maturities of their assets and liabilities. For this to contribute positively to earnings, the yield curve must have a regular shape, meaning that short-term interest rates are lower than long-term rates.

Of course, this is a potentially risky endeavor that requires sound risk management and a capable treasury department, but it is fair to say that the zero-interest rate environment to some extent forced banks to engage in potentially inappropriately risky behavior.

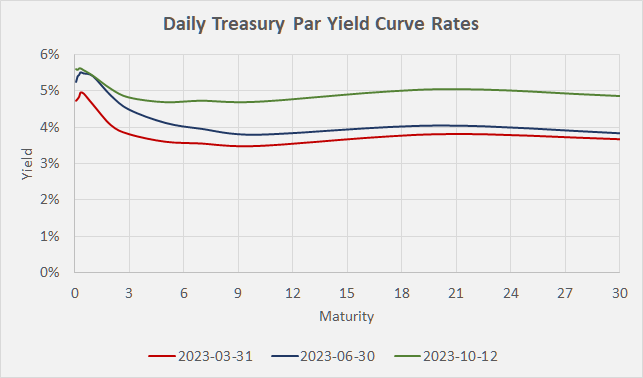

With short-term interest rates eventually coming down and long-term rates remaining in the mid-single digits (the market seems to currently price-in a "higher for longer" scenario, Figure 1), the maturity spread on the yield curve will likely be considerably wider than it was in recent years, improving banks' profit outlook from this perspective. But of course, no one can predict with sufficient accuracy when the yield curve will normalize, and a positive impact on bank earnings cannot be expected in the near term. Nonetheless, it will be interesting to hear if Truist or U.S. Bancorp management has anything to say on this hot topic during the earnings calls next week.

Figure 1: Daily Treasury par yield curve rates from March 31, June 30, and October 12, 2023 (own work, based on data from home.treasury.gov)

{kind=link}

Deposit Trends - Positive For U.S. Bancorp (At Least On The Surface)

In light of the March 2023 banking crisis, it is obviously important to keep a close eye on deposit trends.

However, I do not mean to imply that U.S. Bancorp or Truist are on the brink of falling victim to a run on deposits. After all, they ranked 5th and 7th , respectively, in terms of total assets at the end of the second quarter. And while I don't like the term "too big to fail" (because it usually doesn't help shareholders), I think the two banks are indeed too big to fail, which definitely helps depositor confidence.

Fears that depositors would aggressively withdraw their savings from banks that have significant unrealized losses in their held-to-maturity ((HTM)) portfolios have largely dissipated over time - however, isn't it ironic that it is precisely these bank runs that trigger the otherwise unnecessary realization of the paper losses?

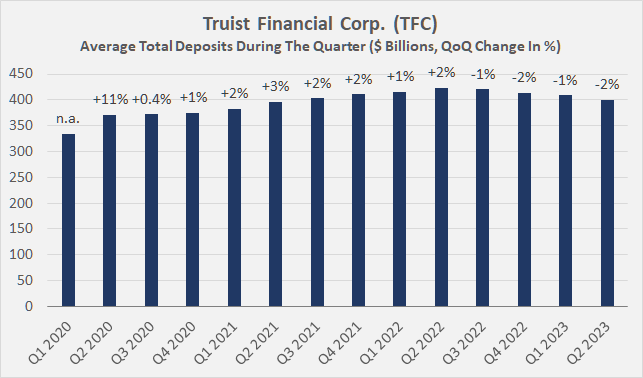

Figure 2, which shows Truist's average deposits on a quarterly basis, shows that the bank has now been losing deposits for four quarters in a row. And while I do not believe that a causal link between outflows and the bank's unrealized HTM losses can be constructed from this development, it is still worth keeping an eye on the situation. As I explained in my previous article on Truist , the decline is largely due to high depositor interest rate awareness, so it is reasonable to expect Truist to report another sequential decline next week. However, I wouldn't over-interpret the risks associated with a continued decline in deposits - Truist is working to give depositors a good deal on their savings, and as one of the largest banks in the U.S., it can actually afford to pay a little less than its - perceived as potentially less trustworthy - smaller competitors.

Figure 2: Truist Financial Corp. (TFC): Average total deposits during the quarter (own work, based on company filings)

{kind=link}

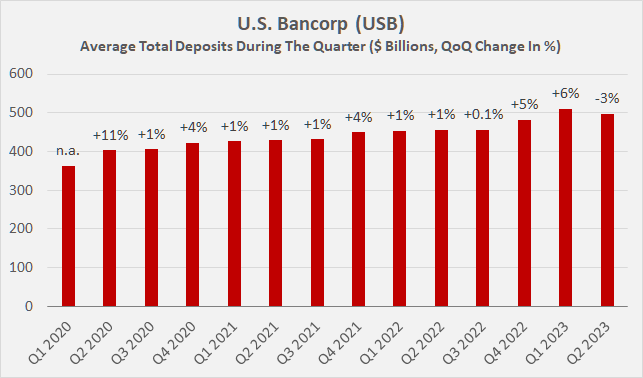

U.S. Bancorp also had to report a quarter-over-quarter decline in average total deposits in the second quarter, likely for the same reasons as Truist (Figure 3). But compared to the second quarter of 2022, average deposits were a whopping 8.9% higher. However, it should be noted that U.S. Bancorp acquired Mitsubishi UFJ Financial Group ( MUFG ) in December 2022. For this reason, I would not overinterpret U.S. Bancorp's apparent outperformance. In the context of the recently completed conversion of MUFG, investors should keep an eye on merger synergies in the upcoming report, which management hinted at during its second-quarter earnings release.

Figure 3: U.S. Bancorp (USB): Average total deposits during the quarter (own work, based on company filings)

{kind=link}

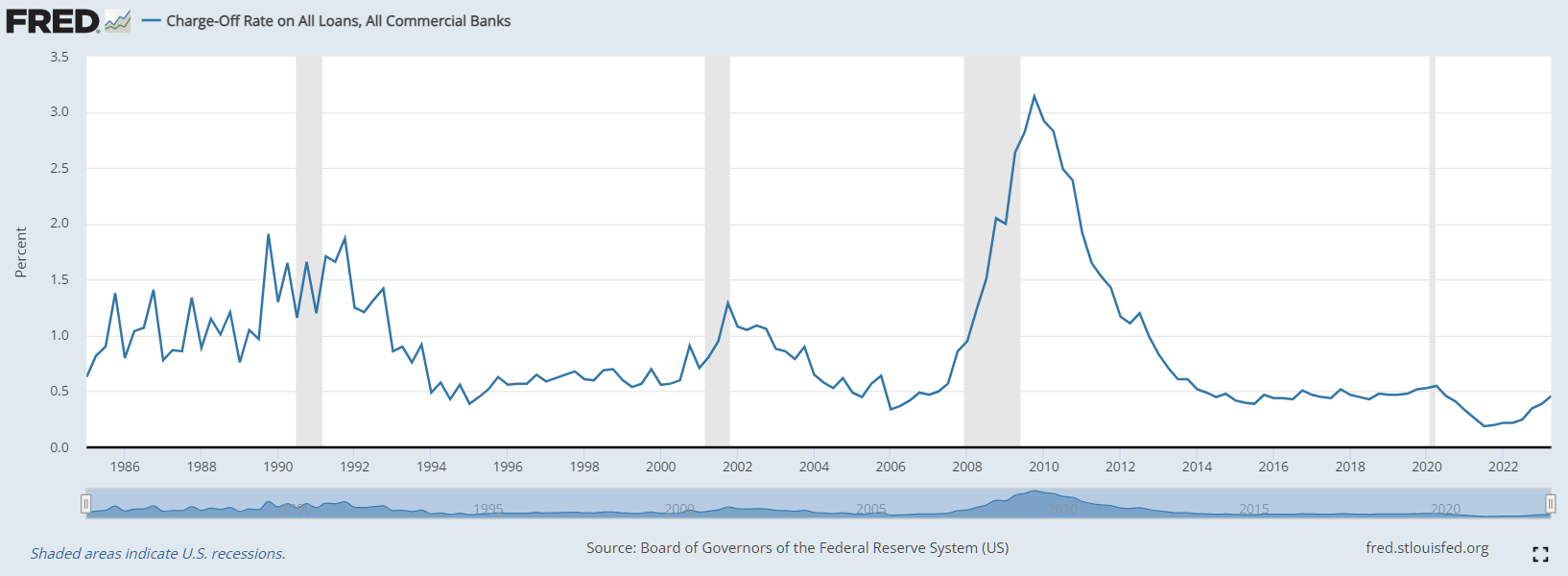

U.S. Bancorp's and Truist Financial's Net Charge-Off Rate

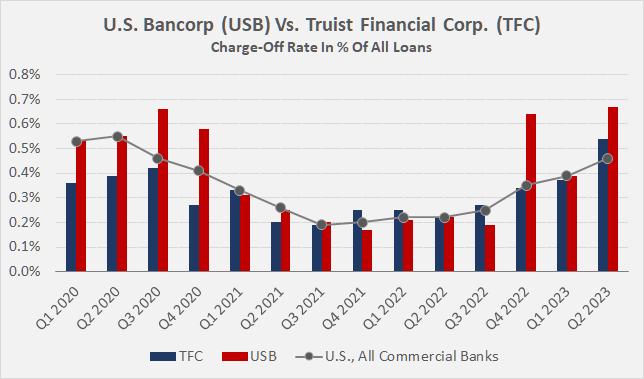

The development of Truist's and U.S. Bancorp's net charge-off rate suggests that the quality of their loan portfolios remains good. This is particularly evident when the figure is compared with the charge-off rate for all commercial banks in the U.S. (Figure 4).

Figure 4: U.S. Bancorp (USB) vs. Truist Financial Corp. (TFC): Charge-off rates as a percentage of all loans, compared with the average for all commercial banks in the United States. (own work, based on company filings)

{kind=link}

Granted, Q2 2023 rates were slightly higher than the average for both USB and TFC, but the numbers should also be viewed in a historical context (Figure 5). Going forward, charge-off rates are expected to continue their upward trend - which I view largely as a mean reversion effect. In my view, it is positive that charge-off rates are rising only slowly - which is not self-evident, considering that the number of "zombie companies" has risen considerably since at least the Great Recession ( see my analysis ).

Figure 5: Charge-off rate on all loans - CORALACBN - Board of Governors of the Federal Reserve System (US) (retrieved from FRED, Federal Reserve Bank of St. Louis)

{kind=link}

But of course, the net charge-off rate is only one indicator of credit quality, and it is important to keep an eye on this and other numbers released next week, including in the context of the banks' commercial real estate portfolios (see, for example, Figure 10 in my previous article on Truist).

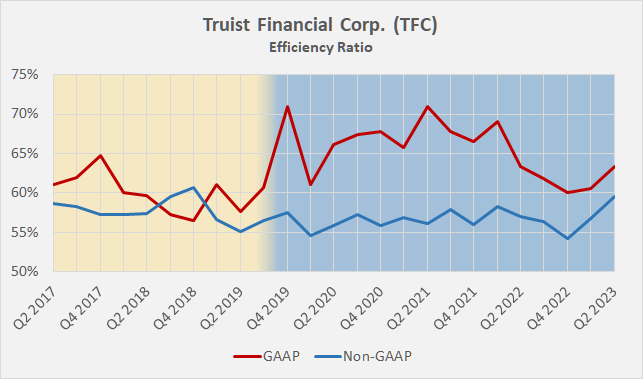

A Note On Operational Profitability

One aspect that I consider particularly important in the context of the upcoming earnings reports concerns Truist. Recall that the bank was formed through the merger of BB&T and SunTrust in late 2019. Truist has so far failed to realize material synergies. While it seemed only natural that the process would take longer than initially expected due to the turmoil caused by the pandemic and related lockdown measures, let's not forget that Truist will soon celebrate its fourth birthday.

Truist's Q2 2023 earnings report was particularly disappointing (as discussed in my last article) - the bank cut its guidance and announced full-year expenses to rise faster than previously expected. Those interested should take a look at the Q2 earnings call transcript , in which analyst Mike Mayo is very direct about management's still rather vague plan.

Truist's efficiency ratio, on both a GAAP and adjusted basis, has deteriorated significantly since the beginning of the year (Figure 6), so this is an important performance indicator to keep a close eye on in the coming quarters. While management has acknowledged that there is still much room for improvement - which is evident but at the same time disappointing given the long time since the merger - I remain patient. Staff rationalization should improve Truist's efficiency ratio in the near term (ignoring severance packages which I expect are excluded from adjusted numbers), but more patience is needed in other areas. Consolidation and realignment of various business units, optimization of operations and contact centers, and increased technology spending will require upfront investment before savings are reflected in the bottom line.

Figure 6: Truist Financial Corp. (TFC): GAAP and non-GAAP efficiency ratios before (yellow) and after the BB&T and SunTrust merger (blue) (own work, based on company filings)

{kind=link}

Therefore, it is only reasonable to expect things to get (at least somewhat) worse before they get better. Depending on how management communicates the expected poor performance in this context in the upcoming earnings release, investors may react with disappointment - especially given the current jittery environment. As a long-term investor, I am of course looking past this temporary nervousness, but keeping a close eye on Truist's spending and the progress it is making - hopefully sooner rather than later.

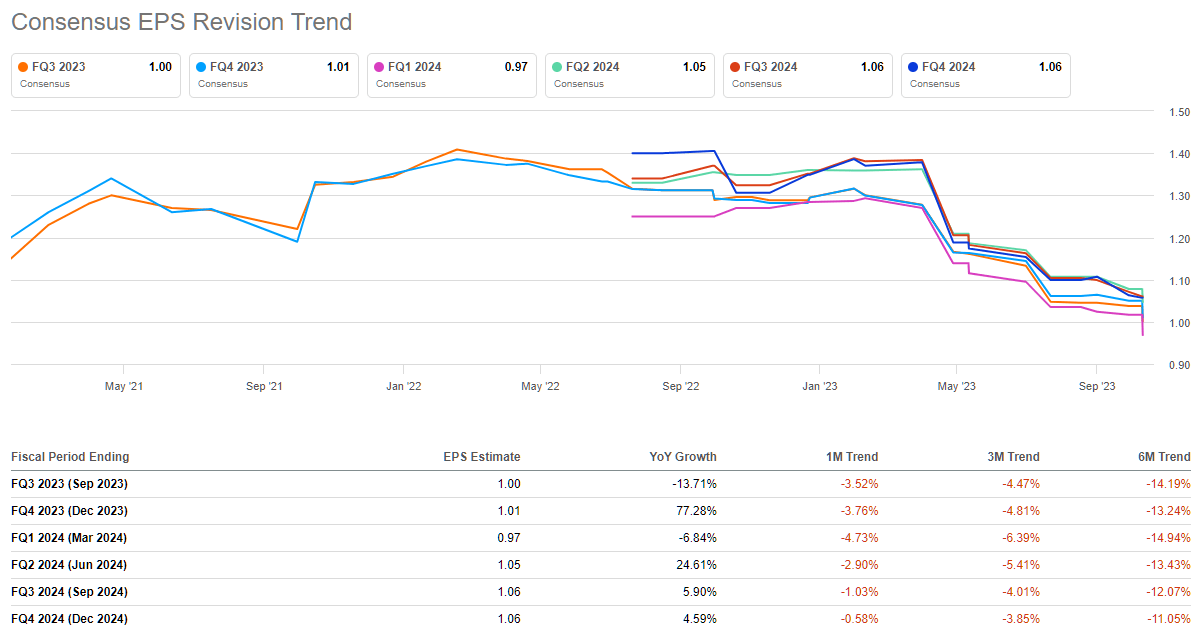

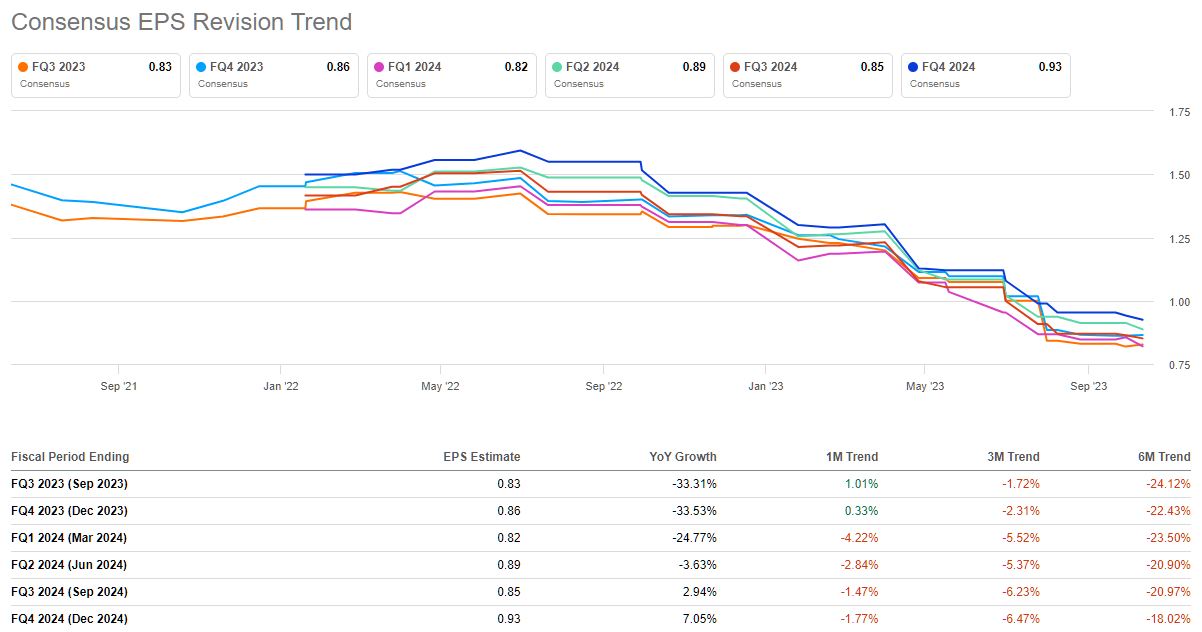

For U.S. Bancorp, the outlook is better from an operational perspective, but of course earnings expectations are also quite subdued. The trend in earnings per share revisions (Figure 7) paints a fairly negative picture, as does the trend for Truist (Figure 8), but investors need to be aware that banks are currently facing headwinds from several directions.

Figure 7: U.S. Bancorp (USB): Earnings per share revision trend on a quarterly basis (Seeking Alpha) Figure 8: Truist Financial Corp. (TFC): Earnings per share revision trend on a quarterly basis (Seeking Alpha)

{kind=link}

{kind=link}

I am not expecting a great report from either bank, but as a long-term investor, I can ride out this period of weakness, which I believe will eventually subside. Investors should be aware that Truist and U.S. Bancorp shares are currently trading at significant discounts to their long-term average valuations, and I believe the weaker earnings outlook is more than priced into valuations.

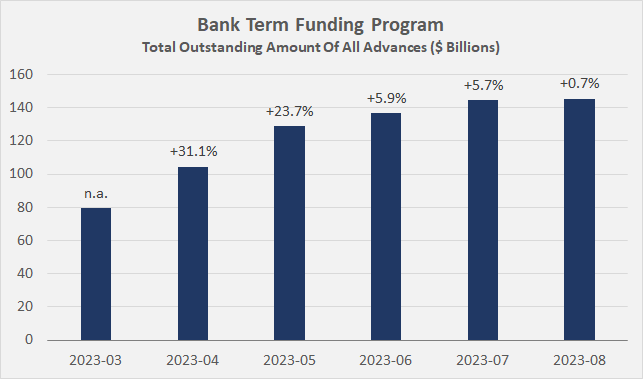

The Still Strongly Used Bank Term Funding Program

Recall that in March 2023, the Federal Reserve moved quickly to announce the Bank Term Funding Program ((BTFB)), which offers short-term loans to banks and other financial institutions for which they post Treasuries and other assets as collateral. Importantly, these assets are valued at par. In my view, one of the main objectives - in addition to providing a form of emergency liquidity to banks - was to create an easy-to-understand measure that would boost depositor confidence. Based on deposit performance to date at Truist and U.S. Bancorp, it can be concluded that deposit outflows due to fears of a possible bank failure are insignificant, but of course the situation is probably quite different at much smaller banks.

The Federal Reserve publishes the utilization of the BTFP on a monthly basis. In my view, this is a good indicator of the current level of stress in the context of the apparently no longer widely discussed issue of unrealized losses on bank balance sheets. While the still heavy utilization of the program is worrisome, it is important to keep in mind that interest rates at the long end have continued to rise and that the bonds in banks' HTM portfolios that are underwater are only gradually maturing off their balance sheets.

Figure 9 shows a continued slowdown in growth, which I take as an indicator that the risk remains manageable. However, it is critical to keep a close eye on the drawdown of the BTFP, as no advances will be made under the program after March 11, 2024. However, the program can be extended if the Board of Governors of the Federal Reserve System and the Secretary of the Treasury deem it necessary - which seems likely given current expectations for long-term interest rates. As an aside, the figure for September 30, 2023, is likely to be released any day now, given past publication dates .

Figure 9: Utilization of the Federal Reserve's Bank Term Funding Program - month-end figures (own work, based on data from federalreserve.gov)

{kind=link}

Conclusion

U.S. Bancorp and Truist Financial will report their third-quarter results next week, on Wednesday and Thursday , respectively.

Earnings expectations are quite low and analysts have become rather cautious in recent months. This was to be expected, given Truist's particularly weak second quarter results, for example.

The increasingly flat yield curve suggests that we are moving in the right direction, but a positive earnings contribution from a maturity transformation perspective should obviously not be expected any time soon. That said, while the two banks increased their exposure to bonds that are now underwater when interest rates were at historic lows, they are now in the process of securing fairly high long-term yields as they replace maturing bonds in their HTM portfolios with new ones. When interest rates eventually fall again, the banks will continue to benefit from a comparatively higher net interest margin for several years.

Deposits have been trending somewhat negative in recent quarters, and I expect this trend to continue for some time. However, I attribute the outflows to the interest rate environment and only to a very small (if any) extent to depositors losing confidence in these very large banks. Nonetheless, it will be important to keep an eye on deposits (and deposit costs) in the upcoming earnings reports.

I expect U.S. Bancorp and Truist to report higher net charge-off rates for the third quarter, and as noted above, it is only reasonable to expect this trend to continue given the persistently high interest rate environment. That said, charge-off rates remain very manageable, are in line with the U.S. average, and are still very modest by historical standards. In this environment, this is definitely good news.

Similarly, the continued slowdown in the growth of Bank Term Funding Program drawdowns suggests that the previously widely covered risk of unrealized losses in held-to-maturity portfolios remains manageable. Nonetheless, it remains a very important risk indicator, and investors should keep an eye on BTFP drawdowns (the September figure is due any day), even in light of its expected end in March 2024 (if the situation permits).

Finally, Truist investors should carefully review management's remarks on the previously announced efficiency measures. It has been nearly four years since the merger of BB&T and SunTrust, and the combined entity continues to struggle from an efficiency standpoint. The bank recently announced its intention to divest the remaining 80% of its insurance business (recall the sale of a 20% stake in February for $1.95 billion), and investors can expect management to provide some information on the potential $10 billion deal in the upcoming earnings release. Suffice it to say that given Truist's fairly weak operating performance to date, I am somewhat ambivalent about the company's intention to sell what is undoubtedly a strong asset.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

Truist Financial And U.S. Bancorp Q3 Earnings: A Caveat Hidden In Plain Sight